#

Fund or

Nonfund

Accounts Accounts Debit Credit

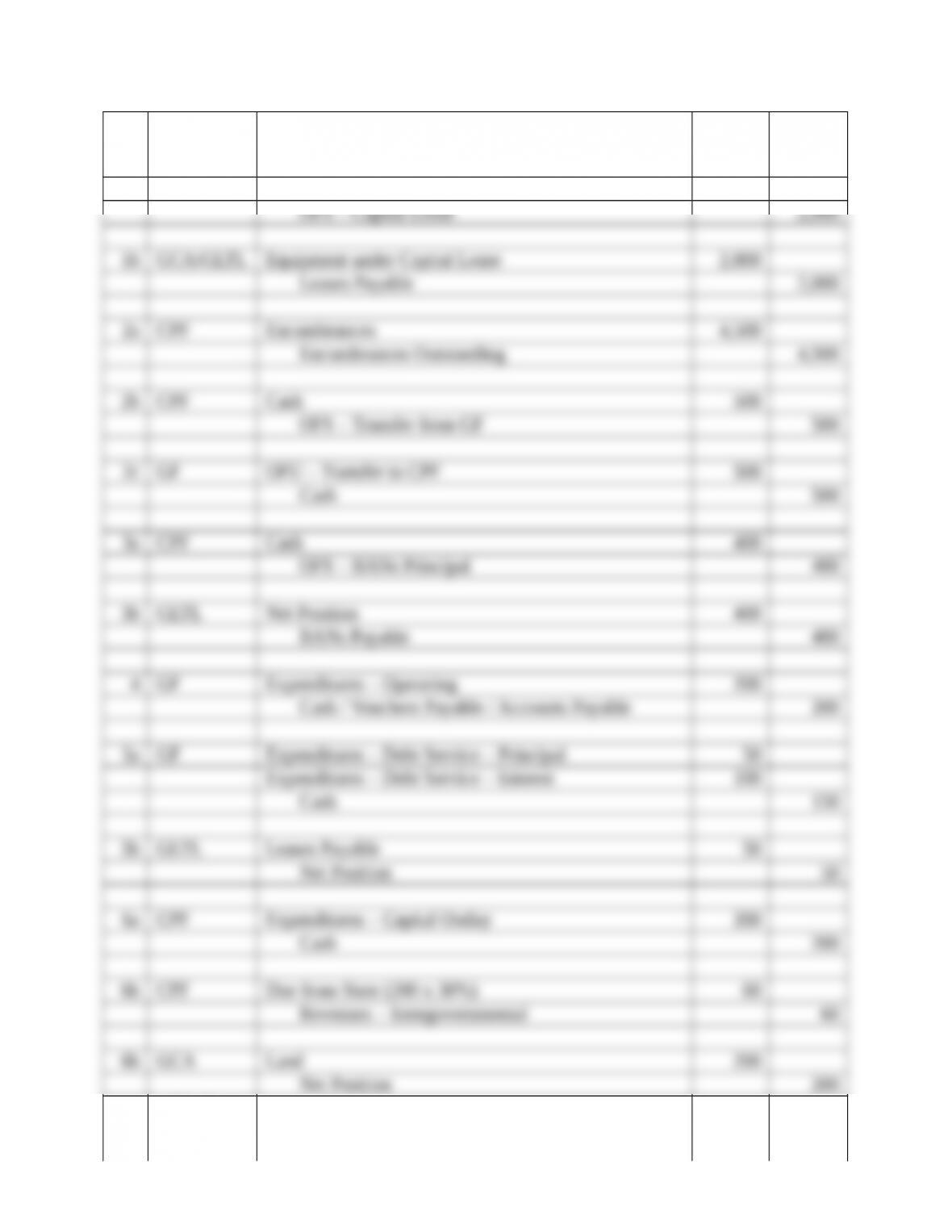

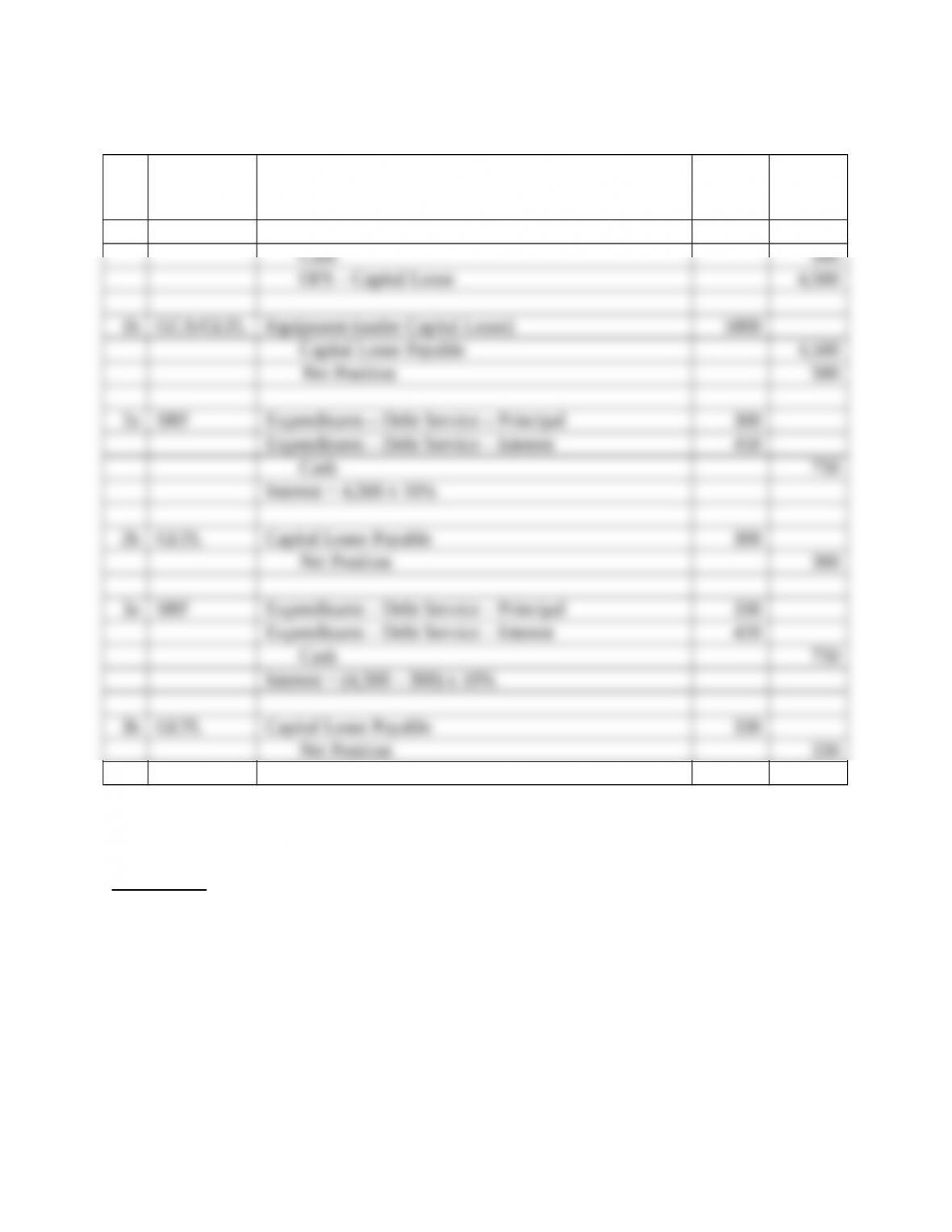

1a GF Expenditures – Capital Outlay 2,000

Fund or 61

Copyright © 2013 Pearson Education, Inc.

Problem 2 – Other Interfund Transactions: Transfers

Transactions:

1. The $10 assets (cash) from a terminated Capital Projects Fund (CPF) were received by

the General Fund.

2. General Fund resources of $250 were paid to a newly established Capital Projects Fund.

The resources will not be repaid to the General Fund.

3. The government ordered that $140 be paid from its General Fund to the fund that services

its long-term debt.

4. The government directed that $200 be moved from the General Fund to the Jail Addition

Capital Projects Fund to provide additional funding for the project. The actual payment

will occur at the beginning of the next fiscal year.

Requirement: Prepare the general journal entries using standard fund-type terminology,

identifying the fund or nonfund accounts for which the entry is being prepared.

Appropriate abbreviations are acceptable (e.g., GF, SRF, CPF, DSF, GCA, GLTL,

OFS, or OFU). If no entry is required, write “No Entry Required” and briefly

explain why. Do not include formal entry explanations or dates, but include any

important assumptions made and all calculations.

62

Copyright © 2013 Pearson Education, Inc.

Answers:

#

Fund or

Nonfund

Accounts Accounts Debit Credit

1a GF Cash 10

OFS – Transfer from CPF 10

Problem 3 – Other Interfund Transactions: Loans

Transactions:

37. A loan of $50 was made from the General Fund to the Gasoline Tax Fund (GTF), which

is accounted for as a Special Revenue Fund. The loan will be repaid in five years.

38. The General Fund loaned $320 to the Capital Projects Fund—to be repaid in 90 days.

Requirement: Prepare the general journal entries using standard fund-type terminology,

identifying the fund or nonfund accounts for which the entry is being prepared.

Appropriate abbreviations are acceptable (e.g., GF, SRF, CPF, DSF, GCA, GLTL,

OFS, or OFU). If no entry is required, write “No Entry Required” and briefly

63

Copyright © 2013 Pearson Education, Inc.

explain why. Do not include formal entry explanations or dates, but include any

important assumptions made and all calculations.

Answers:

#

Fund or

Nonfund

Accounts Accounts Debit Credit

Problem 4 – Other Interfund Transactions: Capital Leases

Transactions:

1. A government Special Revenue Fund leased specialized equipment under a multi-year,

noncancelable lease agreement that qualifies as a capital lease. The lease required a

down payment of $500 and the present value of the minimum lease payments (i.e., the

capitalizable cost of the leased asset) was $5,000. The implicit rate of interest on the

lease is 10%.

2. The government made the first lease payment of $750.

3. The government made the second lease payment of $750.

Requirement: Prepare the general journal entries using standard fund-type terminology,

identifying the fund or nonfund accounts for which the entry is being prepared.

Appropriate abbreviations are acceptable (e.g., GF, SRF, CPF, DSF, GCA, GLTL,

OFS, or OFU). If no entry is required, write “No Entry Required” and briefly

explain why. Do not include formal entry explanations or dates, but include any

important assumptions made and all calculations.

64

Copyright © 2013 Pearson Education, Inc.

Answers:

#

Fund or

Nonfund

Accounts Accounts Debit Credit

1a SRF Expenditures – Capital Outlay 5,000

Problem 5 – Other Interfund Transactions: Capital Asset Acquisitions and Disposals

Transactions:

1. A pickup truck purchased seven years ago for $30 with General Fund money was sold for

$5. The government’s proprietary funds usually depreciate this type of asset over a 10-

year period using straight-line depreciation with zero (0) salvage value and disposes of

assets at the end of its useful life.

2. Sold land for $300, which had been used many years ago as a public park. The land had

been purchased for $140.

3. The county purchased a police vehicle for $22 and paid cash.

65

Copyright © 2013 Pearson Education, Inc.

4. The government signed a contract for $5,000 for construction of an addition to the jail.

5. The contractor billed the county for 40% of the work on the jail addition. The actual cost

of the work was $2,200. The county paid all but 10% of the amount billed. The balance

is to be paid upon completion and approval of the project. The state was billed for its

30% of the project based on an expenditure-driven grant. (See entry #4 and #6)

6. The contractor billed the county $2,800 for the remainder of the work on the jail. The

county approved the facility and paid the contractor all amounts owed. The state was

billed for its portion of the work. (See entries #4, #5, and #7)

7. The state reimbursed only $1,400. Other costs were disallowed for reimbursement. (See

entries #5 and #6)

Requirement: Prepare the general journal entries using standard fund-type terminology,

identifying the fund or nonfund accounts for which the entry is being prepared.

Appropriate abbreviations are acceptable (e.g., GF, SRF, CPF, DSF, GCA, GLTL,

OFS, OFU). If no entry is required, write “No Entry Required” and briefly

explain why. Do not include formal entry explanations or dates, but include any

important assumptions made and all calculations.

Answers:

66

Copyright © 2013 Pearson Education, Inc.

#

Fund or

Nonfund

Accounts Accounts Debit Credit

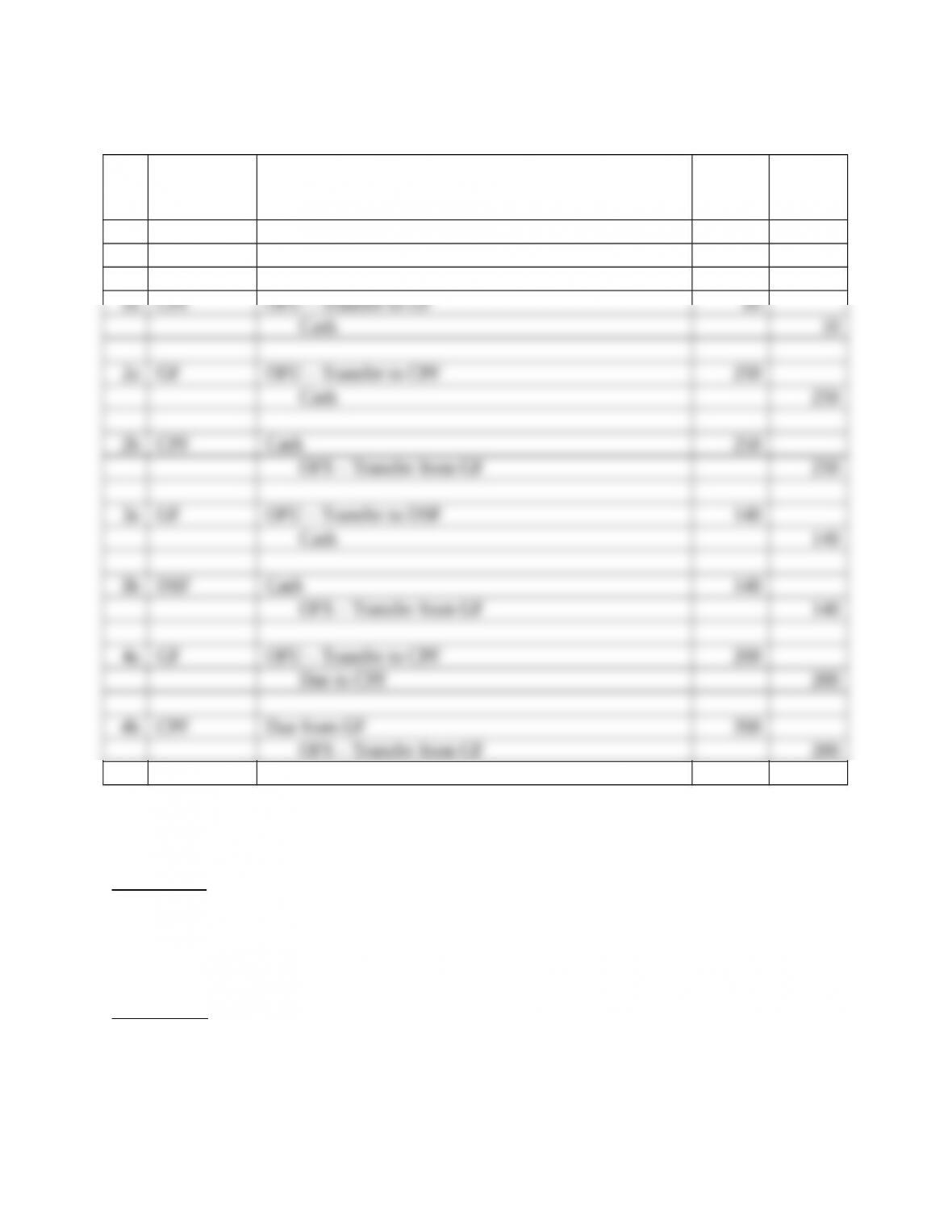

1a GF Cash 5

OFS – Proceeds from Sale of Vehicle 5

67

Copyright © 2013 Pearson Education, Inc.

Problem 6 – Other Interfund Transactions: BANs and Long-Term Debt

Transactions:

1. The government issued $2,500 of 8-month, 9% bond anticipation notes. The notes meet

the requirements to be accounted for as long-term debt. The proceeds are to be used to

begin construction of a recently approved addition to the county jail.

2. The government issued $5,000 of 10-year, 8% bonds at par. Bond issue costs of $50

were withheld from the proceeds. Interest and one-tenth of the principal are payable

annually on the bonds. The bond proceeds are to be used to repay the bond anticipation

notes and to finance construction of the jail addition. (See entries #1 and #3)

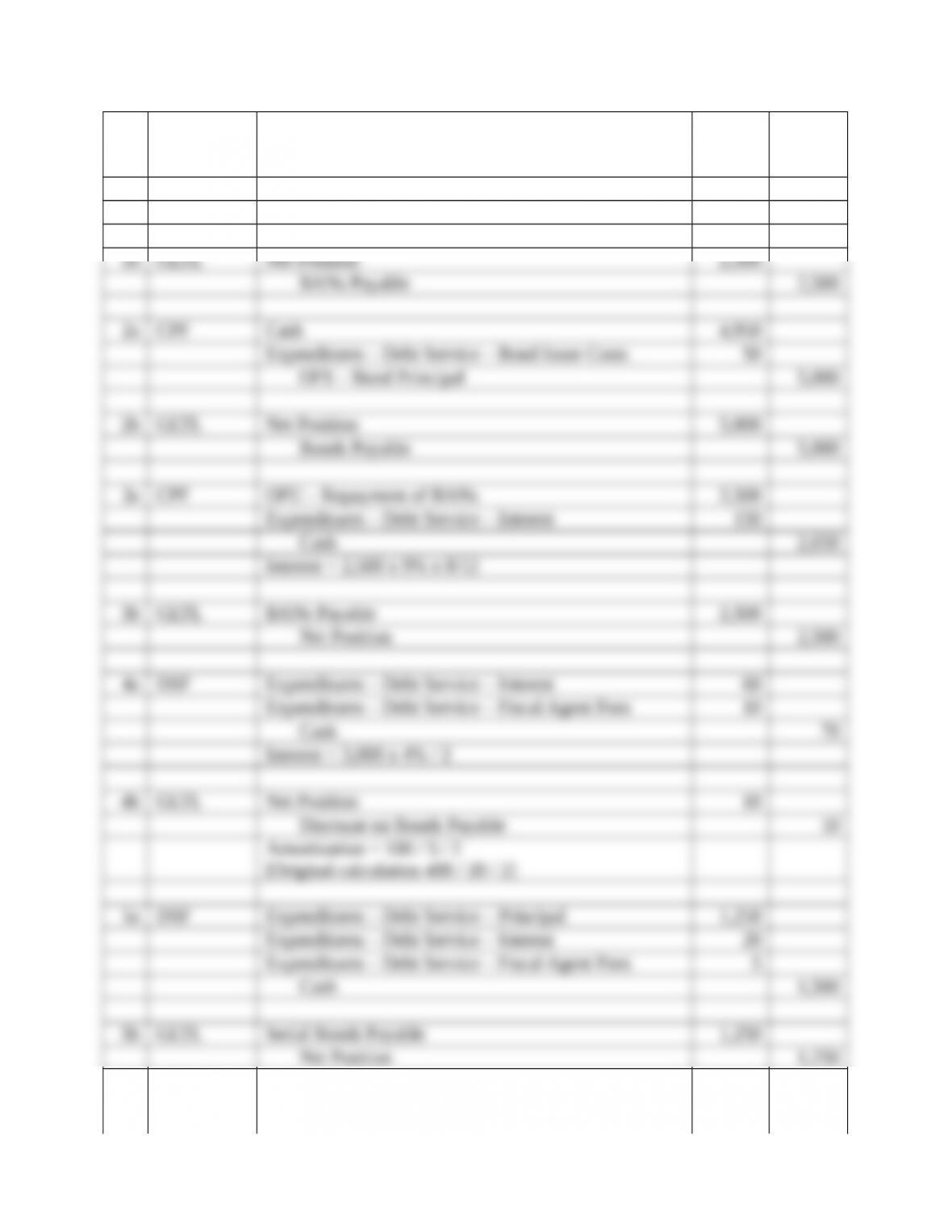

3. The BANs and interest were paid on their due date. (See entries #1 and #2)

4. The semi-annual payment of interest on bonds issued several years ago by a Capital

Projects Fund came due and was paid. The outstanding principal of these 20-year, 4%

face rate, term bonds is $3,000. The unamortized discount on these bonds is $100. The

bonds were issued 15 years ago on this date. The payment includes fiscal agent fees of

$10.

5. The annual payment of serial bonds issued 10 years ago by the government came due.

The amount owed is $1,250 in principal, $20 interest, and $5 in fiscal agent fees. The

amount due was paid.

6. Another term bond issued 20 years ago by the government came due and was paid. The

face amount and rate was $3,200 and 3%, respectively, and pays interest semi-annually.

The fiscal agent fees were $60.

7. A serial bond issued in the current year has its first annual payment of principal and

interest due on the third day of the next fiscal year. As is required by the debt covenant

and following the general procedures for all debt issues of the county, $1,200 ($1,000 for

principal, $180 for interest, and $20 for fiscal agent fees) has been transferred from the

General Fund to the Debt Service Fund to make this payment.

Requirement: Prepare the general journal entries using standard fund-type terminology,

identifying the fund or nonfund accounts for which the entry is being prepared.

Appropriate abbreviations are acceptable (e.g., GF, SRF, CPF, DSF, GCA, GLTL,

OFS, OFU). If no entry is required, write “No Entry Required” and briefly

explain why. Do not include formal entry explanations or dates, but include any

important assumptions made and all calculations.

68

Copyright © 2013 Pearson Education, Inc.

Answers:

69

Copyright © 2013 Pearson Education, Inc.

#

Fund or

Nonfund

Accounts Accounts Debit Credit

1a CPF Cash 2,500

OFS – BAN Principal 2,500

#

Fund or

Nonfund

Accounts Accounts Debit Credit

70

Copyright © 2013 Pearson Education, Inc.