Answers:

Requirement #1

# Accounts Debit Credit

Situation A

Requirement #2

Situation A

Trans

# Assets Liabilities

Fund

Balance GCA GLTL

Net

Position

Situation B

Trans

# Assets Liabilities

Fund

Balance GCA GLTL

Net

Position

51

Copyright © 2013 Pearson Education, Inc.

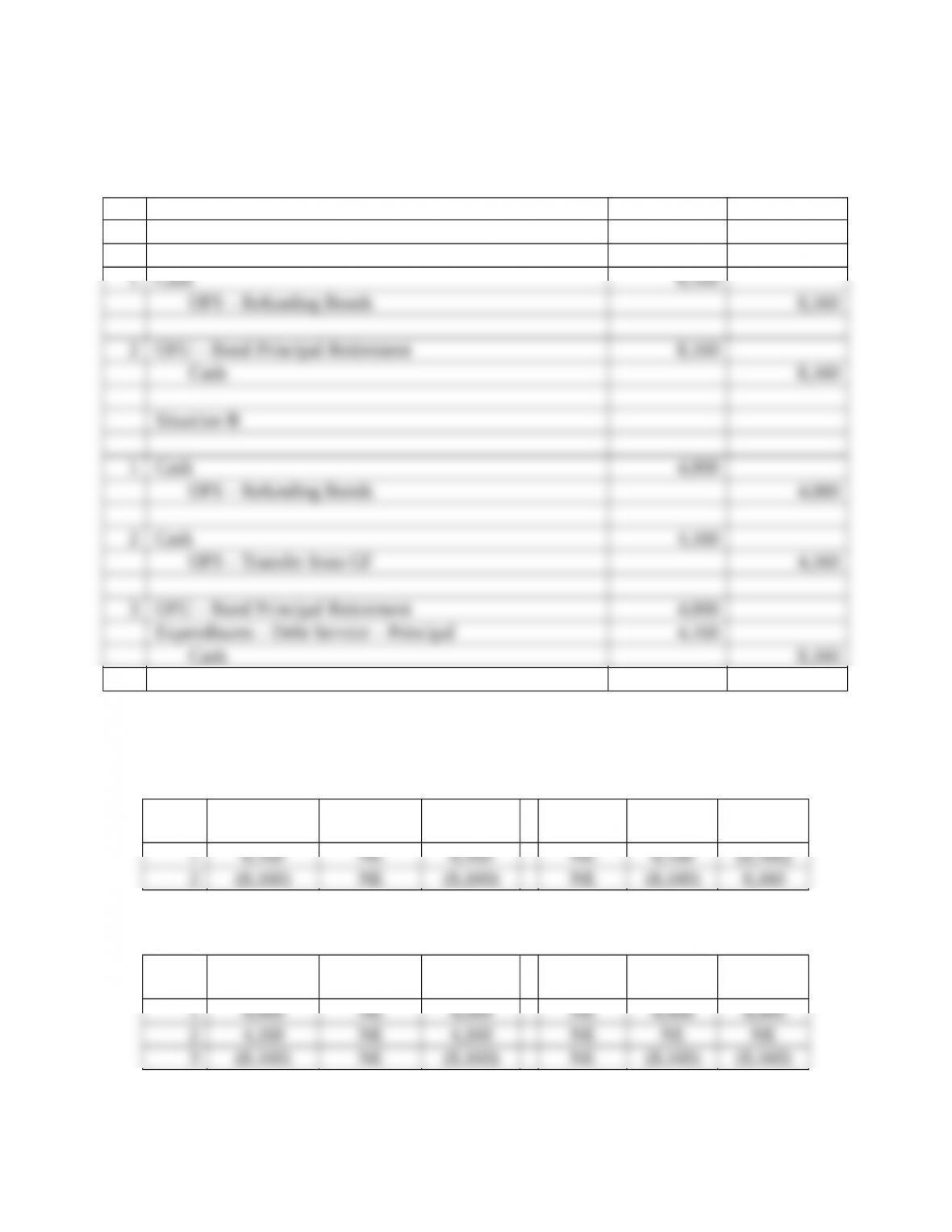

Problem 2 – Advance Refunding

The City of Armona has decided to refinance $8,000 par value of general government, general

obligation bonds outstanding. The bonds had a related unamortized bond premium of $200. The

city issues $6,000 of refunding bonds and transfers $2,700 from the General Fund to the Debt

Service Fund. The city paid $8,700 from the Debt Service Fund into an irrevocable trust to cover

future payments on the original bonds. All amounts are in thousands of dollars.

Requirements:

1. Record the above transactions in the Debt Service Fund assuming the refinancing meets

the conditions for treatment as a defeasance in substance.

2. Record the above transactions in the Debt Service Fund assuming the refinancing does

not meet the conditions for treatment as a defeasance in substance.

3. For both requirements (1) and (2), indicate the effects of each transaction on the

accounting equation of the Debt Service Fund and on the General Capital Assets and

General Long-Term Liabilities accounts. If an element is not affected, put “NE” in the

appropriate box.

Answers:

# Accounts Debit Credit

Requirement 1

1 Cash 6,000

52

Copyright © 2013 Pearson Education, Inc.

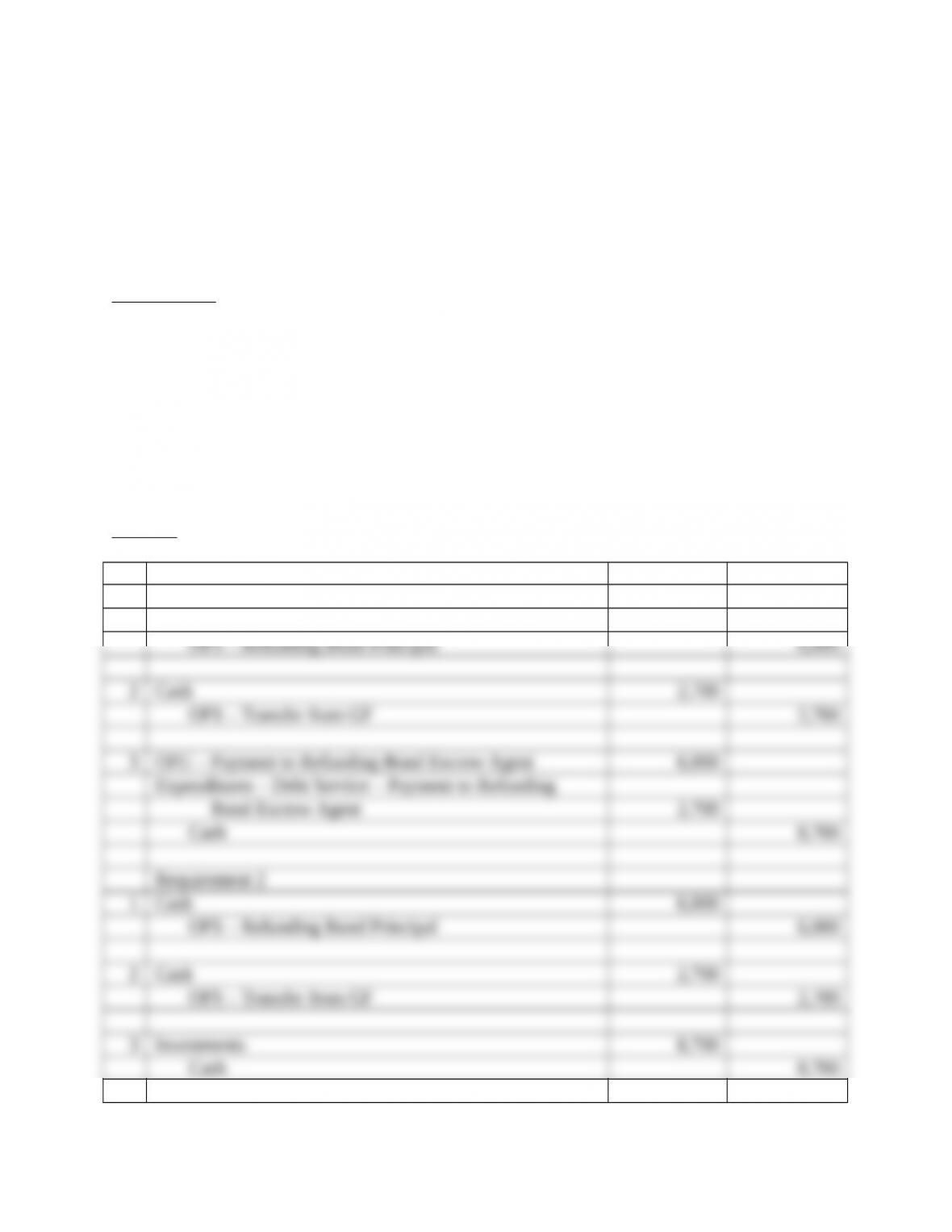

Requirement 3

Refunding

Trans

# Assets Liabilities

Fund

Balance GCA GLTL

Net

Position

Investment (non-Refunding)

Trans

# Assets Liabilities

Fund

Balance GCA GLTL

Net

Position

53

Copyright © 2013 Pearson Education, Inc.

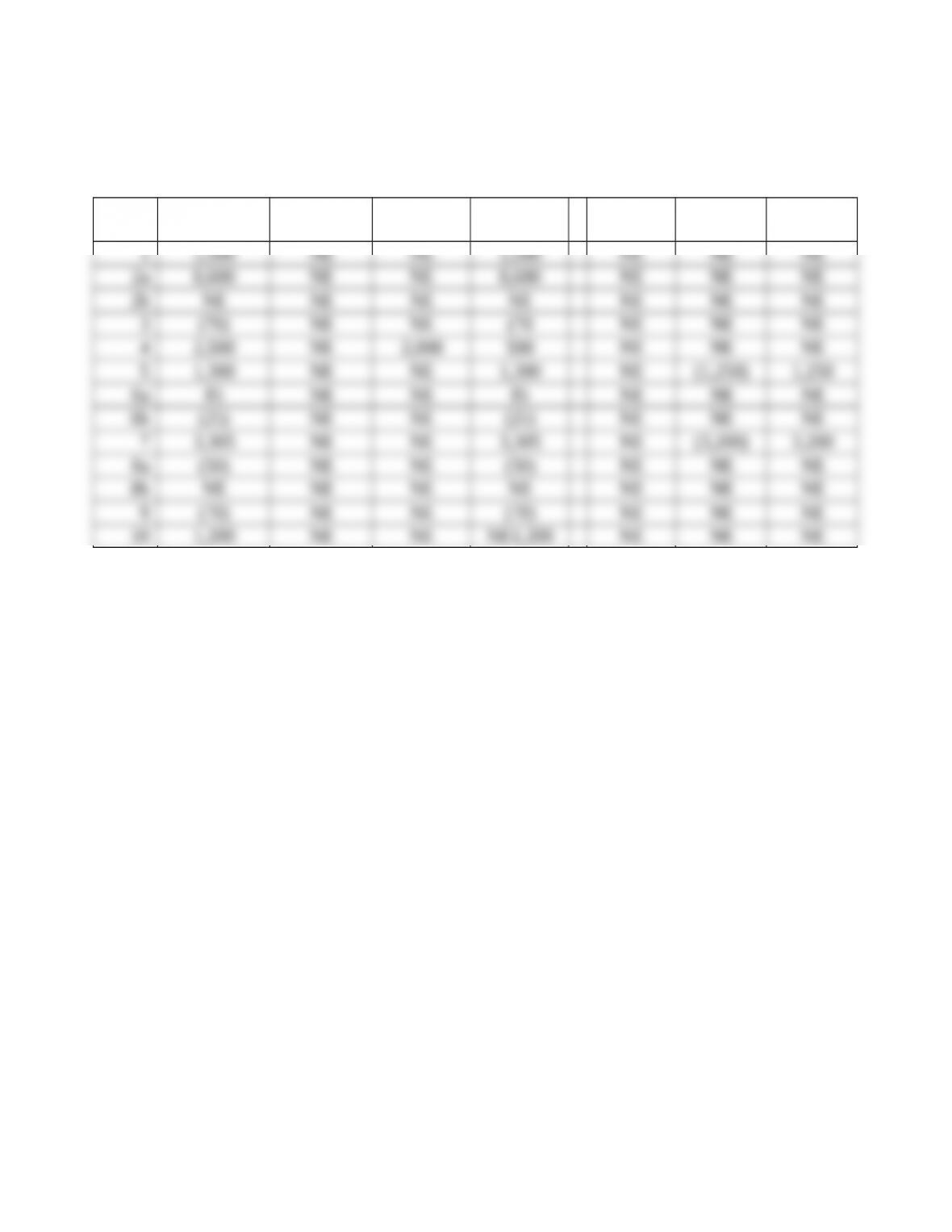

Problem 3 – Debt Service Fund Transactions

Listed below are selected transactions from a Loudon County Debt Service Fund (all amounts

are in thousands of dollars).

1. The remaining funds of a Capital Projects Fund, $1,500, were transferred to the Debt

Service Fund to be used in the repayment of debt and interest on that debt that was issued

to finance and expansion of the county courthouse.

2. The county General Fund transferred $8,600 to the Debt Service Fund to provide

financing for principal, interest, and fiscal agent fees for debt service transactions during

the year. $6,000 of the transfer from the General Fund and all of the transfer from the

CPF was invested.

3. The semi-annual payment of interest on bonds issued several years ago by a Capital

Projects Fund came due and was paid. The outstanding principal of these 20-year, 4%

face rate, term bonds is $3,000. The unamortized discount on these bonds is $100. The

bonds were issued 15 years ago on this date. The payment includes fiscal agent fees of

$10.

4. The county has agreed to set up a small water treatment facility for the remote District 7,

now that the local water supply has been polluted by a hog farm upstream. The cost of

the facility, $2,500, is to be financed over 5 years by special assessments on the

homeowners in that district, although the debt is guaranteed by the county. The

assessment principal is paid annually, although the interest (4%) is paid semi-annually.

The first interest payment is due in 6 months, with the first principal payment due in one

year (60 days after year-end).

5. The annual payment of serial bonds issued 10 years ago by the county came due. The

amount owed is $1,250 in principal, $20 interest, and $5 in fiscal agent fees. The amount

due was paid.

6. The county received interest on its investments, $85. In addition, investments that

originally cost $4,000 were sold for $3,975. (See entry #2)

7. Another term bond issued 20 years ago by the county came due and was paid. The face

amount and rate was $3,200 and 3%, respectively, and pays interest semi-annually. The

fiscal agent fees were $60.

8. The semi-annual payment for interest on the outstanding special assessment bonds was

paid when due. Also, $300 has been collected for the principal payment due next year.

9. The regular semi-annual interest payment on the term bonds came due and was paid. (See

entry #3)

10. A serial bond issued in the current year has its first annual payment of principal and

interest due on the third day of the next fiscal year. As is required by the debt covenant

and following the general procedures for all debt issues of the county, $1,200 ($1,000 for

principal, $180 for interest, and $20 for fiscal agent fees) has been transferred from the

General Fund to the Debt Service Fund to make this payment.

54

Copyright © 2013 Pearson Education, Inc.

Requirements:

1. Record the above transactions in the Debt Service Fund.

2. Indicate the effects of each transaction on the accounting equation of the Debt Service

Fund and on the General Capital Assets and General Long-Term Liabilities accounts. If

an element is not affected, put “NE” in the appropriate box.

Answers:

Requirement #1

55

Copyright © 2013 Pearson Education, Inc.

# Accounts Debit Credit

1 Cash 1,500

56

Copyright © 2013 Pearson Education, Inc.

Requirement #2

Trans

# Assets Liabilities

Deferred

Inflows

Fund

Balance GCA GLTL

Net

Position

Governmental and Nonprofit Accounting: Theory and Practice, 10e (Freeman)

Problems – Chapter 9

Problem 1 – Comprehensive Interfund Transactions

9Prepare the general journal entries to properly record each of the following transactions and

events in the appropriate general ledger accounts of the appropriate funds for the year ended

June 30, 2011. The City of Middlesettlements uses a series of each type of nominal account

(e.g., Revenues–Property Taxes, Revenues–Other, Expenditures–Operations, Expenditures–

Capital Outlay, Expenditures–Debt Service–Interest, OFS–Bond Principal, OFU–Transfer to GF,

etc.), except for budgetary entries where no additional detail is required. The General Capital

Assets and General Long-term Liability accounts are updated whenever a relevant transaction

occurs.

ADDITIONAL INFORMATION:

■ The fiscal year for the City is July 1 to June 30.

■ All premiums on bonds payable, net of bond issue costs, are transferred to the DSF that

will be used to service the debt. The amounts transferred are used for future bond interest

payments.

■ When bonds are issued at a discount or bond issue costs are incurred, a special transfer is

made from the GF to the fund issuing the bonds to reimburse it for the discount and issue

costs. This transfer is over and above any previously authorized transfers from the GF to

that fund.

57

Copyright © 2013 Pearson Education, Inc.

■ The City uses the consumption method / periodic inventory system to account for

supplies.

The City is constructing a new municipal building. Capital Projects Fund #1 will be used to

account for this construction. The expected cost of and the sources of proportional financing for

the municipal building are:

Bond issue (authorized July 1, 2010, 6%, 30-year serial bonds)…………..….…. $3,000

State grant (expenditure driven)……………………………………………………………… 1,500

Transfer from the General Fund……………………………………………………………… 500

Total sources and cost of building…………………………………….….…….…….. $5,000

All amounts are in thousands of dollars.

Transactions:

1. A computer has been leased for the City for its accounting and payroll operations. The

lease has a fair market value (and a net present value) of $2,000. The lease will be

serviced through the General Fund.

2. A contract for the construction of the new municipal building was accepted by Swann &

Hall (S&H) Construction Company for $4,500. The required transfer from the General

Fund to the Capital Projects Fund was made.

3. $400 in 6-month, 4%, bond anticipation notes (BANs) were issued to finance

expenditures in advance of the bond issue. The BANs are to be repaid from the proceeds

of the previously authorized bond issue—as required by the debt covenant—by CPF #1.

4. The City accounts for its supplies in the General Fund. The City started the year with

$100 in its supply account and purchased $200 in supplies to augment its inventory.

5. The first capital lease payment on the computer, $150 (including $100 in interest), was

paid. (See entry 1)

6. 5 acres of land were purchased for $200 for the new municipal building. This purchase

had not been previously encumbered, but it is included in the budget for the project.

7. The bonds authorized on July 1, 2010, were issued at 102 on October 1, 20X1. Bond

issue costs were $20. The bonds pay interest on March 31 and September 30. Principal

payments occur evenly over the life of the bonds each year (1/30 each September 30).

DSF #1 was established to service this debt. (See entries 3 & 8)

8. The BANs were paid when due. (See entries 3 and 7)

9. The City issued $125 in supplies to its departments.

10. Expenditures totaling $2,500 were made for the construction project. These expenditures

had originally been encumbered for $2,600. The amount was vouchered for payment to

S&H Construction net of a 10% retainage. (See entry 2)

11. Sufficient funds were transferred from the General Fund to the DSF #1 to finance one

year’s principal retirement, interest, and fiscal agent fees ($10) for the municipal building

bonds. (See entries 7 and 13)

12. The City issued another $100 in supplies to its departments.

13. DSF #13 made the required March 31 bond payments. (See entries 7 and 11)

14. At year-end an inventory of supplies revealed that $80 were on hand. The appropriate

adjustments were made. (

58

Copyright © 2013 Pearson Education, Inc.

Requirement: Prepare the general journal entries for the City of Middlesettlements, using

standard fund-type terminology, identifying the fund or list for which the entry

is being prepared. Appropriate abbreviations are acceptable (e.g., GF, SRF,

CPF, DSF, GCA, GLTL, OFS, OFU). If no entry is required, write “No Entry

Required” and briefly explain why. Do not include formal entry explanations or

dates, but include any important assumptions made and all calculations. If an

amount is not given in the exam, you must show your work to demonstrate how

you determined the amount.

59

Copyright © 2013 Pearson Education, Inc.

Answers:

60

Copyright © 2013 Pearson Education, Inc.