City of Walland

Preclosing Trial Balance

For the Year Ended June 30, 20X4

Advance to Enterprise Fund……………………………………………………………………… 1,000

Allowance for Uncollectible Taxes……………………………………………………….…… 300

Appropriations……………………………………………………………………..….…….…….… 8,850

Budgetary Fund Balance………………………………………………………………………..… 150

Cash………………………………………………………………………………………………………. $5,000

Due from Special Revenue Fund………………………………………………………….…… 100

Encumbrances Outstanding………………………………………………….…….…….……... 60

Encumbrances……………………………………………………………………………….…….…. 60

Estimated Revenues……………………………………………………………………….…….…. 9,000

Expenditures – Capital Outlay……………………………………………………………….…. 2,500

Expenditures – Operating…………………………………………………….…….…….……... 6,340

Fund Balance (July 1, 20X3)……………………………………………………..….…….…… 9,505

Investments…………………………………………………………………………………….……... 2,500

OFS – Proceeds from Sale of Vehicle…………………………………………………..……. 50

OFS – Transfer from Capital Projects Fund…………………………..….…….…….…… 60

OFU – Transfer to Debt Service Fund………………………………………………….……. 100

OFU – Transfer to Enterprise Fund…………………………………………….…….…….… 200

Revenues – Other……………………………………………………………………………..….…. 1,250

Revenues – Property Taxes…………………………………………………………………….… 7,500

Salaries Payable………………………………………………………………………….…….……. 50

Special Item – Proceeds from Sale of Land……………………………………………..…. 350

Supplies…………………………………………………………………………………………………. 175

Taxes Receivable……………………………………………………………..…….…….…….….. 1,500

Vouchers Payable……………………………………………………………………………….…… 350

21

Copyright © 2013 Pearson Education, Inc.

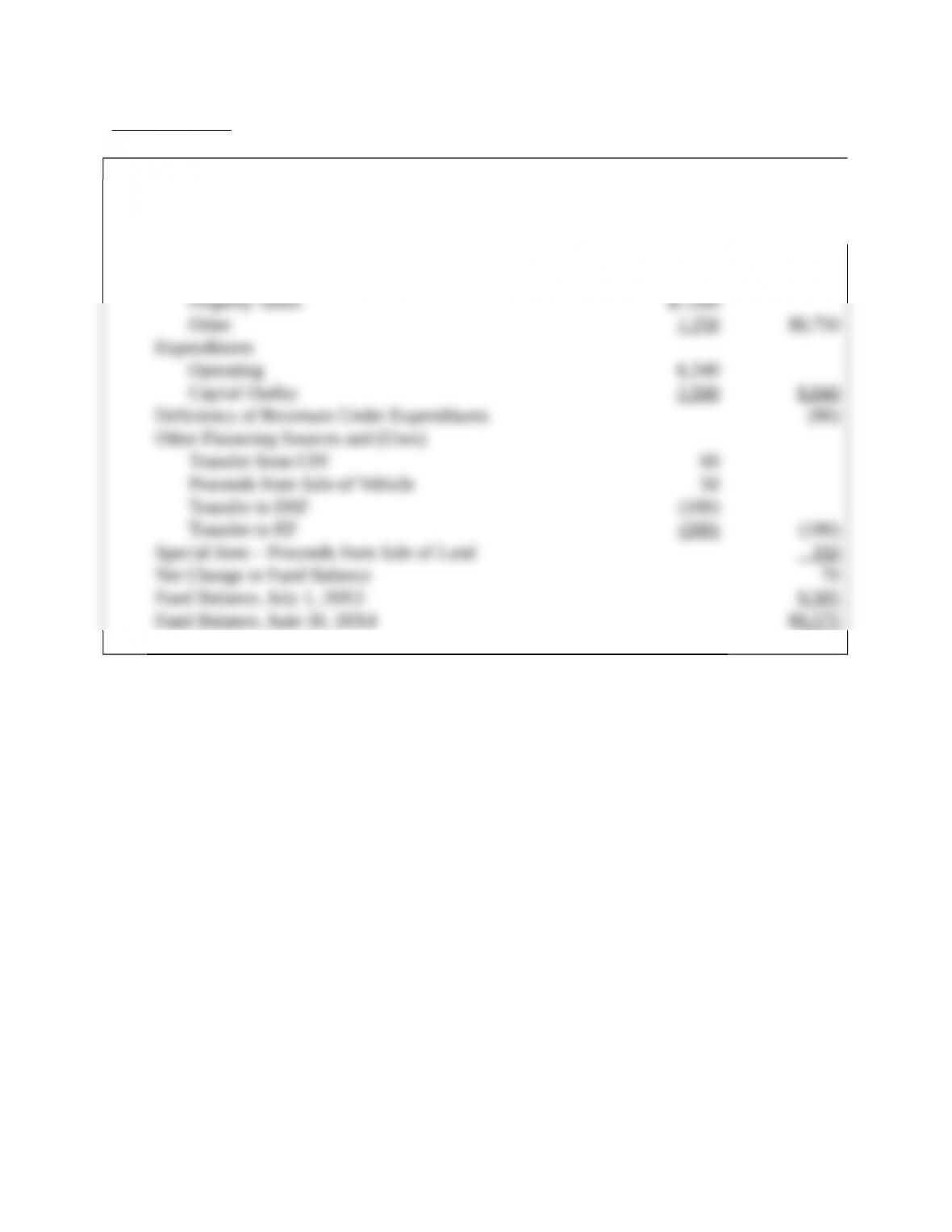

Requirement #1

City of Walland

General Fund

Statement of Revenues, Expenditures, and Changes in Fund Balance

For the Fiscal Year Ended June 30, 20X4

Revenues

22

Copyright © 2013 Pearson Education, Inc.

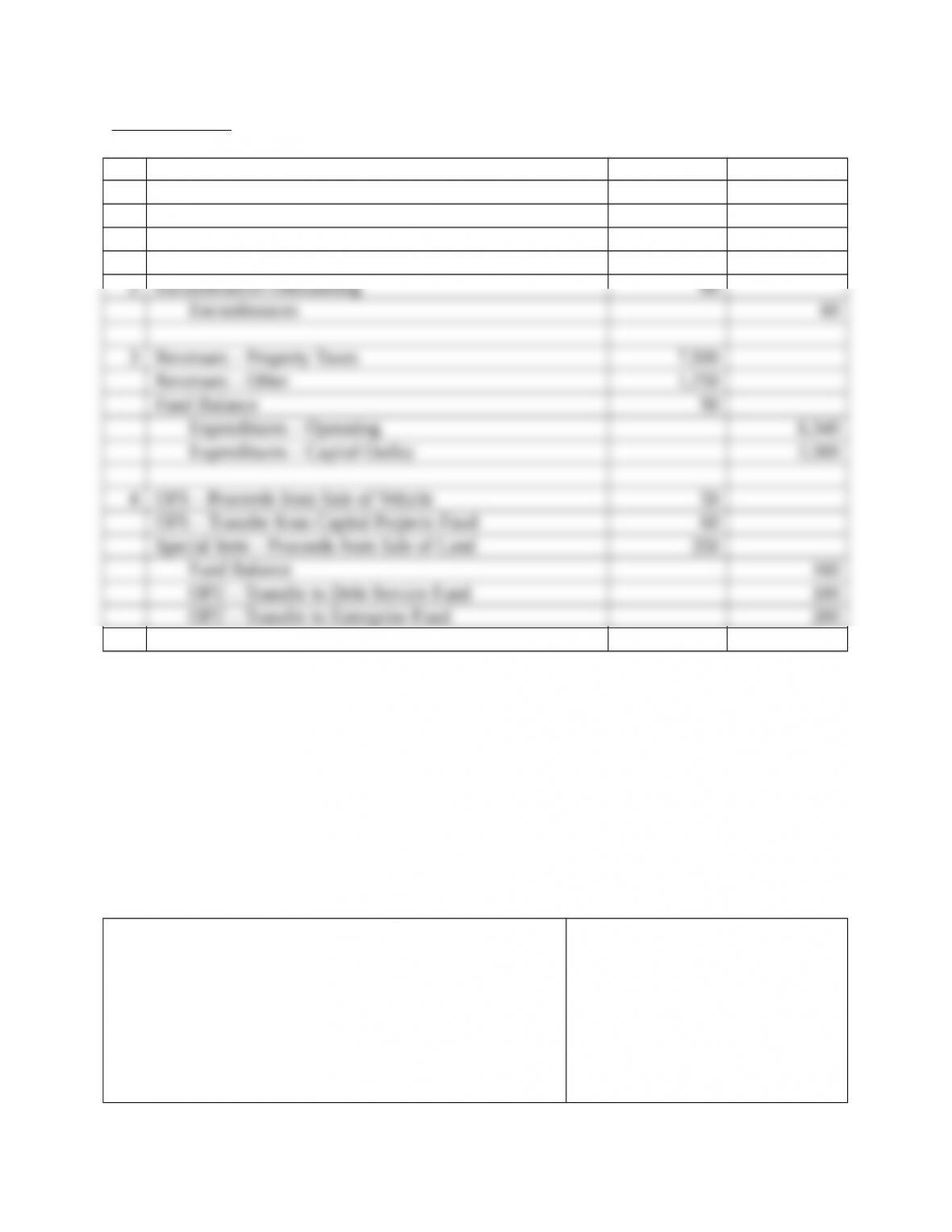

Requirement #2

City of Walland

General Fund

Balance Sheet

June 30, 20X4

Assets

Cash $5,000

Investments 2,500

23

Copyright © 2013 Pearson Education, Inc.

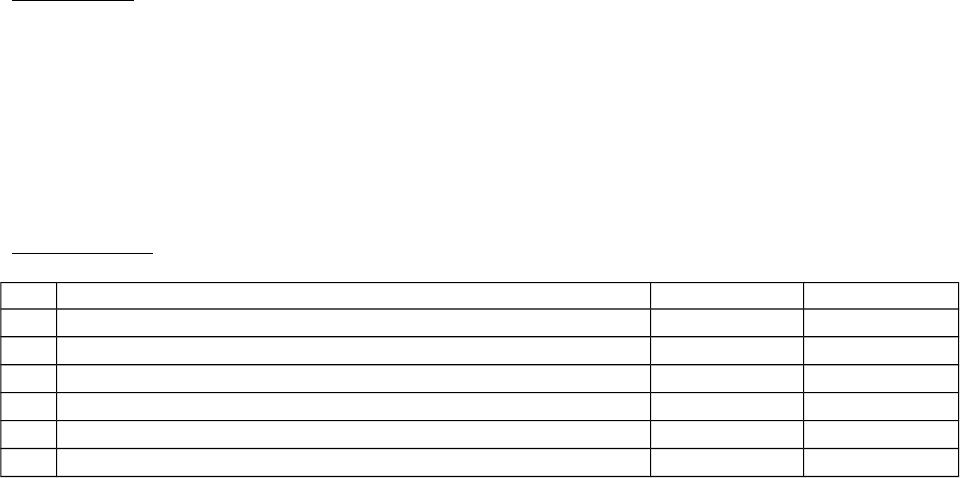

Requirement #3

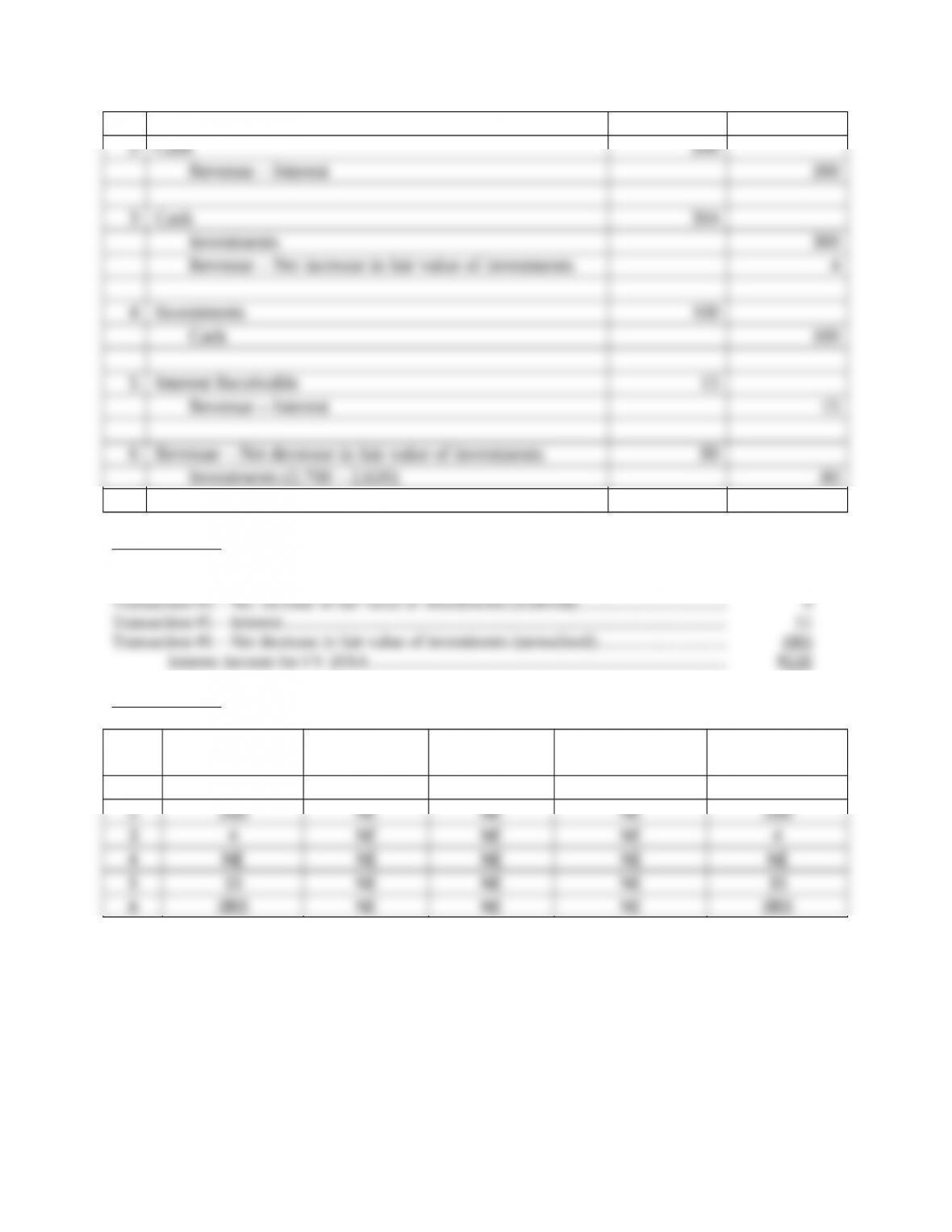

# Accounts Debit Credit

1 Appropriations 8,850

Budgetary Fund Balance 150

Estimated Revenues 9,000

Governmental and Nonprofit Accounting: Theory and Practice, 10e (Freeman)

Problems – Chapter 5

Problem 1 – Matching: Match the Resource Flow with the Type of Revenue

6Listed below in the left column are some events that may or may not be revenues for the General Fund.

Listed in the right column are the classifications of revenues for governmental funds. Correctly match

each event with the appropriate revenue classification. Unless specifically stated otherwise, assume all

amounts are earned, measurable, and available. If the event is not a revenue, state how the event would

be reported in the current year General Fund financial statements.

1. Sales taxes collected locally.

2. Ad valorem taxes for which the levy has been made but

are due and payable in the following fiscal year.

3. Billing for garbage services provided to the Enterprise

Fund by the Sanitation Department (accounted for in the

General Fund).

4. Realized gain from the sale of an investment.

5. Gas taxes collected by the state and allocated based on a

predetermined formula.

7A. Taxes

B. Licenses and Permits

C. Intergovernmental Revenues

D.Charges for Services

24

Copyright © 2013 Pearson Education, Inc.

6. Cash received from the issuance of long-term debt.

7. Property taxes levied, due, and payable in the prior fiscal

year and collected in the first 60 days of the current

fiscal year.

8. Payment from the Library Special Revenue Fund to the

General Fund for a utility bill originally paid from

General Fund resources for the entire government.

9. Payments made by the local university to the City in lieu

of paying property taxes on university-owned land.

10. Property taxes levied for the current year and collected

in the first 60 days of the following fiscal year.

11. Cash collections from speeding tickets enforced in

municipal court.

12. Unrealized loss on an investment at the end of the

current fiscal year.

13. Cash received from an operating grant where the time

restriction has not been reached.

14. Cash collected for electrical inspections made in new

home construction.

15. Interest earned on investments.

16. Pass through grant for which the City has administrative

responsibility.

17. Quarterly income tax payments from taxpayers.

18. Receipt of cash for a capital grant for which the

qualifying expenditures have not yet been made.

19. Cash received on next year’s property tax bill.

20. Cash received from a short-term borrowing.

E. Fines and Forfeits

F. Miscellaneous Revenues

G. Not a revenue

Answers:

25

Copyright © 2013 Pearson Education, Inc.

19. G – Unearned Revenue

20. G – Fund liability

Problem 2 – Property Tax Entries (enhanced)

The Jackson Independent School District began the year with the following accounts on its Balance Sheet

related to property taxes (all amounts are in thousands of dollars). All accounts have normal balances:

Taxes Receivable – Delinquent……………………………………………………………………………….. 2,000

Allowance for Uncollectible Taxes – Delinquent..…….…….…….………….…….………….......… 400

Deferred Revenues……………………………………………………………………………………………..…. 300

Selected transactions for the Jackson Independent School District are presented below.

5. On January 1 the school district levied property taxes of $8,000. The due date for the taxes is

March 31. Taxes are considered delinquent after that date. The school district expects to collect

all but 4% of the levy. In addition the district offers a 2% discount if the taxes are paid by

February 28. The district expects 40% of the tax to qualify for the discount.

6. Between January 2 and February 28, the district collected $4,800 of the taxes due. Of this

amount, $1,300 was due in the preceding fiscal year.

7. During March, an additional $3,500 of receivables were collected. Of this amount, $200 were for

the preceding fiscal year. The remaining delinquent taxes from the preceding fiscal year were

written off as uncollectible.

8. On April 1, the balance of the current year taxes is past due. A 10% penalty and 2% in interest

was immediately assessed on the delinquent debt. It is estimated that $30 of the total interest and

penalties will prove uncollectible.

9. On June 12 the school district wrote off $100 of property taxes, $10 in penalties, and $2 in

interest as uncollectible.

10. From March 31 to December 31 the school district collected $300 of the property taxes that were

levied on January 1. The school district expects to collect an additional $200 of these taxes during

the first two months of the next fiscal year.

Requirements:

1. Prepare the necessary journal entries. Dates and explanations may be omitted. If a transaction

requires no entry, do not leave it blank: state “No Entry Required” and explain why.

2. What was the total Revenues – Property Taxes earned in the current fiscal year.

3. Indicate the impact of each of the transactions on the Balance Sheet equation. If a transaction has

no effect or if the net effect is zero, indicate it with “NE”.

Answers:

Requirement #1

# Accounts Debit Credit

1 Deferred Revenues 300

Revenues – Property Taxes 300

Taxes Receivable – Current 8,000

Allowance for Uncollectible Taxes – Current 320

Allowance for Discounts on Taxes 64

26

Copyright © 2013 Pearson Education, Inc.

Revenues – Property Taxes 7,616

2 Cash 4,730

Allowance for Discounts on Taxes 64

Revenues – Property Taxes 6

Taxes Receivable – Delinquent 1,300

Taxes Receivable – Current 3,500

3 Cash 3,500

Taxes Receivable – Delinquent 200

Taxes Receivable – Current 3,300

Allowance for Uncollectible Taxes – Delinquent 400

Revenues – Property Taxes 100

Taxes Receivable – Delinquent 500

Requirement #2

Revenues deferred from previous year…………………………………………….…….…….…. 300

27

Copyright © 2013 Pearson Education, Inc.

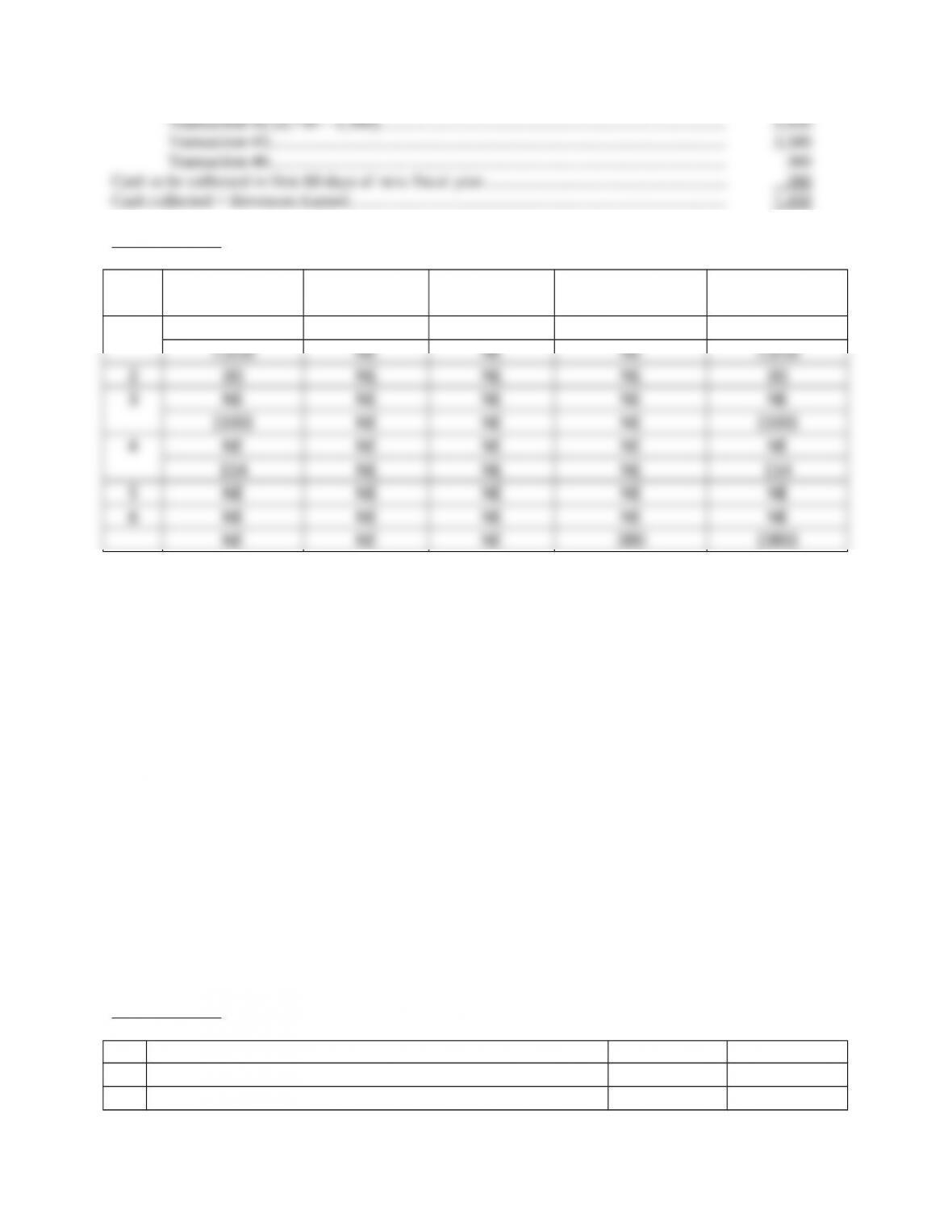

Requirement #3

Trans

# Assets

Deferred

Ouflows Liabiliies

Deferred

Inlows

Fund

Balance

1 NE NE NE (300) 300

Problem 3 – Investment Accounting

The following transactions occurred in the City of Mimosa during fiscal year 20X4 (all amounts are in

thousands of dollars):

1. Purchased investments in long-term participating, interest-bearing securities, $3,000.

2. Collected interest on its investments of $200.

3. Sold 10% of the investments for $304.

4. Purchased 6-month U.S. Treasury Bills for $100.

5. Accrued interest at year end amounted to $15.

6. The fair value of the investments in long-term participating, interest-bearing securities at

year end was $2,620. The fair value of the investments in U.S. Treasury Bills at year end

was $99.

Requirements:

1. Prepare the journal entries for each of these transactions.

2. What is the total interest revenue to be reported for FY 20X4?

3. Indicate the impact of each of the transactions on the Balance Sheet equation. If a transaction has

no effect or if the net effect is zero, indicate it with “NE”.

Requirement #1

# Accounts Debit Credit

1 Investments 3,000

Cash 3,000

28

Copyright © 2013 Pearson Education, Inc.

Requirement #2

Transaction #2 – Interest………………………………………………………………………………….…….. $200

Requirement #3

Trans

# Assets

Deferred

Ouflows Liabiliies

Deferred

Inlows

Fund

Balance

1 NE NE NE NE NE

Governmental and Nonprofit Accounting: Theory and Practice, 10e (Freeman)

Problems – Chapter 6

Problem 1 – Matching: Match the Resource Flow with the Type of Expenditure

8Listed below in the left column are events that may or may not be expenditures for the General Fund.

Listed in the right column are the classifications of expenditures for governmental funds. Correctly

29

Copyright © 2013 Pearson Education, Inc.

match each event with the appropriate expenditure classification. Unless specifically stated otherwise,

assume all amounts have been incurred. If the event is not an expenditure, state how the event would be

reported in the current year General Fund financial statements.

21. Interest on short-term debt.

22. Purchase of a vehicle that will be used in the Library

(accounted for as a Special Revenue Fund).

23. Signing a capital lease.

24. Claim against the government to be paid in a future

year.

25. Borrowing money with a short-term note.

26. Year-end accrual of interest on long-term debt.

27. Compensated absences earned and paid during the year.

28. Paying salaries and wages.

29. Amounts withheld from salaries and wages for taxes

and Social Security/Medicare.

30. Ordering supplies and materials (assume the purchases

method is used).

31. Receiving supplies (assume the purchases method is

used).

32. Using supplies (assume the purchases method is used).

33. Ordering supplies and materials (assume the

consumption method is used).

34. Issuing long-term debt.

35. Receiving supplies (assume the consumption method is

used).

36. Using supplies (assume the consumption method is

used).

37. Capital lease principal payment.

38. The General Fund reimbursed the Special Revenue

Fund (SRF) for salaries paid originally from SRF

resources.

39. Capital lease interest payment.

40. Repayment of a short-term note.

41. The General Fund received a payment from the Library

Fund (SRF) for its portion of the government electricity

bill.

42. Year-end accrual of interest on short-term note.

43. Compensated absences earned in the current year but to

be paid in future years.

44. Claim against the government to be paid in the current

year.

45. The General Fund received an electric bill for the entire

government. The General Fund paid the bill.

46. The General Fund transferred money to the Capital

Projects Fund to provide financing for the construction

of a major facility.

A. Expenditures – Operating

B. Expenditures – Intergovernmental

C. Expenditures – Capital Outlay

D. Expenditures – Debt Service –

Principal

E. Expenditures – Debt Service –

Interest

F. Not an expenditure

G. Event reduces expenditure (also

identify which of above

expenditures would be reduced)

Answers:

30

Copyright © 2013 Pearson Education, Inc.