10. Cash received from a capital grant, $5,000.

11. Cash paid for construction costs that qualify under the capital grant, $1,500.

12. The City acquired land for future plant expansion, $750, by issuing a 10-year bond in the

same amount.

13. Cash received from operating grants, $500.

14. Cash paid for salaries covered by operating grant, $85.

15. The City had an unrealized gain on investments of $12.

16. The Enterprise Fund incurred $10,000 in operating expenses, including $1,000 in

depreciation, $3,000 for employees, and $6,000 paid to suppliers. All but $500 of the

salary expenses were paid by year end.

17. Cash paid for equipment purchased with the proceeds of an operating grant, $34.

18. Cash received from the General Fund to cover part of the cost of plant expansion, $1,000.

19. Cash proceeds from the sale of fund capital assets, $23.

20. Cash received from another fund as a 6-month loan for the sole purpose of financing

purchase of equipment, $90.

The balance of cash and cash equivalents at October 1, 20X1, was $313. The balance of cash

and cash equivalents at year end (9/30/20X2) is $26,250.

Requirement: Prepare the City of Jimtown Enterprise Fund Statement of Cash Flows for the

year ended September 30, 20X2. You may exclude the reconciliation of operating

income to cash flows from operating activities.

81

Copyright © 2013 Pearson Education, Inc.

Answer:

City of Jimtown

Enterprise Fund

Statement of Cash

For the Year Ended September 30, 20X2

Cash Flows from Operating Activities

Cash received from customers $12,500

Cash received from other funds 2,500

Cash paid to employees (85 + 3,000 – 500) (2,585)

Cash paid to suppliers (6,000) $6,415

Cash Flows from Noncapital Financing Activities

Cash paid for interfund transfers (300)

Cash received from operating grants 500 200

82

Copyright © 2013 Pearson Education, Inc.

Problem 5 – Statement of Revenues, Expenses, and Changes in Fund Net Position

Using the information provided below for the Water Utility Enterprise Fund of the City of Rice,

prepare a statement of revenues, expenses, and changes in fund net position for 20X3.

Charges for service…………………………………………………………………….………….…….. $3,300

Interest received…………………………………………………………………………………..………. 105

Increase in fair value of investments……………………………………………….………….….. 12

Gain on sale of capital assets………………………………………………………….…….……….. 8

Operating transfers from the General Fund……………………………………………….…….. 450

Capital Grant………………………………………………………………………………………….….… 1,200

Salaries expense………………………………………………………………………………….……….. 1,000

Contractual services used………………………………………………………………………………. 300

Supplies used………………………………………………………………………….……….………….. 400

Depreciation………………………………………………………………………………………….….…. 1,100

Interest expense……………………………………………………………………………………………. 250

Unrestricted Net Position, January 1, 20X3……………………………………………………… 1,000

Restricted Net Position, January 1, 20X3……………………………………………..…………. 200

Net Investment in Capital Assets, January 1, 20X3………………………………………..…. 1,800

Answer:

City of Rice

Water Utility Enterprise Fund

Statement of Revenues, Expenses, and Changes in Fund Net Position

For the Year Ended December 31, 20X3

Operating Revenues – Charges for Services $3,300

83

Copyright © 2013 Pearson Education, Inc.

Governmental and Nonprofit Accounting: Theory and Practice, 10e (Freeman)

Problems – Chapter 11

Problem 1 – Statement of Cash Flows

The five sections for reporting items in an Internal Service Fund Statement of Cash Flows

prepared using the direct method (excluding the reconciliation of operating income to cash flows

from operations) are:

A. Operating Activities

B. Noncapital Financing Activities

C. Capital and Related Financing Activities

D. Investing Activities

E. Noncash Investing, Capital, and Financing Activities

Using these five sections, indicate in which section each of the following Internal Service Fund

transactions should be reported. If a transaction should not be reported on the Statement of Cash

Flows, indicate it using the letter “X”.

1. Purchase of an Internal Service Fund capital asset for cash.

2. Providing services to other funds on a cash basis.

3. Issuing refunding bonds to refinance bonds issued 10 years ago to provide financing for

capital asset acquisitions.

4. Sale of Internal Service Fund capital assets for cash.

5. Transfer from a Special Revenue Fund for the specific purpose of financing an Internal

Service Fund capital asset purchase.

6. Payment of office workers’ salaries.

7. Amortization of the Deferred Interest Expense Adjustment created when the capital asset

debt was refunded.

8. Transfer to a Capital Projects Fund to provide financing for a general government capital

asset construction project.

9. Purchases of investments with cash received from issuing bonds to finance construction

of Internal Service Fund capital assets.

10. Transfer to the General Fund for the purpose of financing specific operating costs of a

department accounted for in that fund.

11. Issuing bonds to provide operating cash for the Internal Service Fund.

12. Signing a capital lease for equipment to be used by activities accounted for in the Internal

Service Fund.

13. Interest received during the year earned on investments.

14. Transfer the proceeds from the sale of an Internal Service Fund capital asset to the

General Fund.

15. Depreciation on Internal Service Fund capital assets.

16. Proceeds of bonds issued to finance construction of Internal Service Fund capital assets.

17. Interest paid on bonds issued to finance construction of an Internal Service Fund capital

asset.

84

Copyright © 2013 Pearson Education, Inc.

18. Principal retirement payments on bonds issued to finance construction of Internal Service

Fund capital assets

19. Unrealized gain on investments held at year end.

20. Receipt of a capital grant for an ongoing Internal Service Fund capital asset construction

project.

Answers:

Problem 2 – Internal Service Fund Journal Entries

Listed below are selected transactions for the Maury County Internal Service Fund.

Transactions:

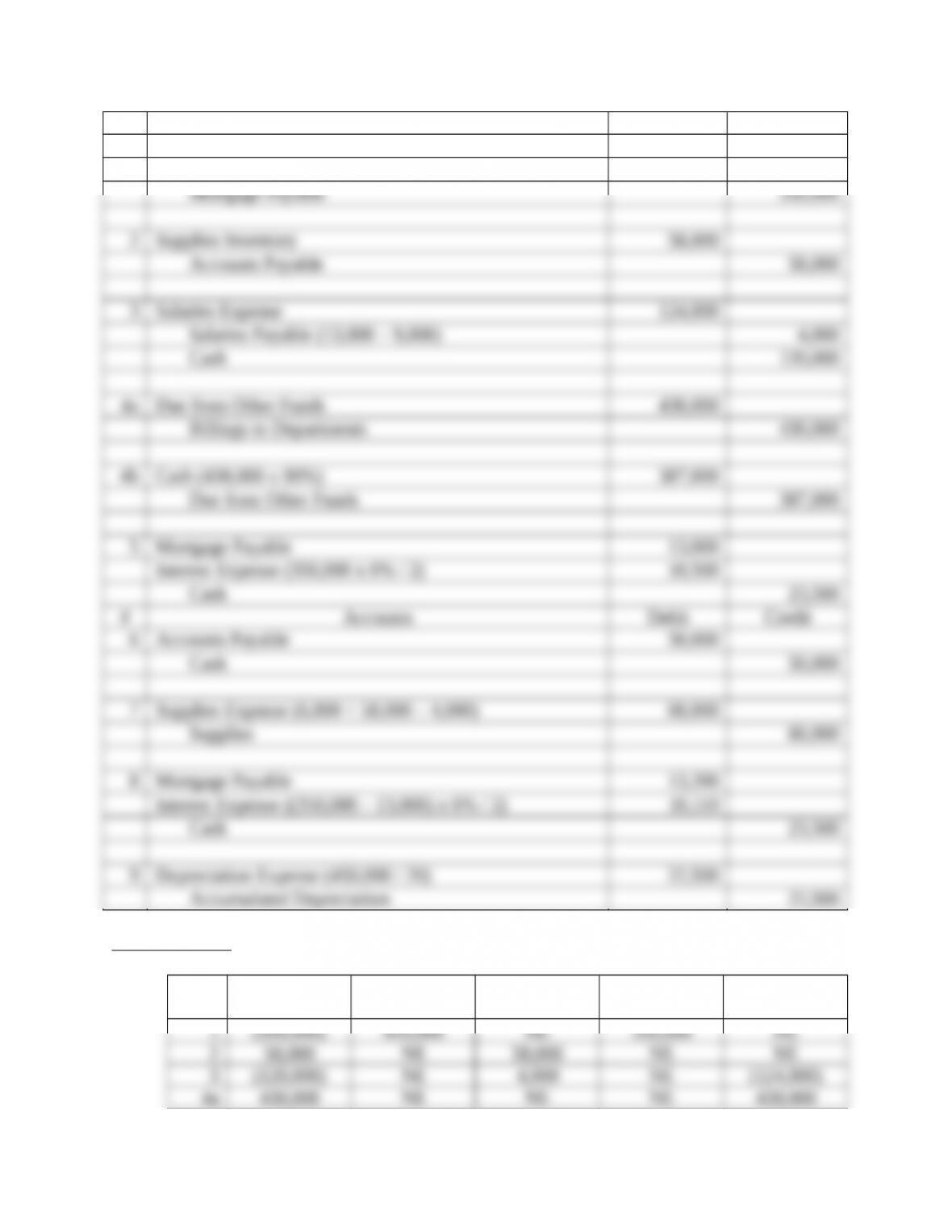

1. Purchased a building on January 2, 20X2, by paying $100,000 down and borrowing

$350,000 on a 6%, 10-year mortgage. Assume semi-annual mortgage payments are due

each June 30 and December 31, beginning this year. The building will be depreciated

over 20 years with no salvage value using the straight-line method.

2. Purchased supplies on account, $58,000. The fund uses the perpetual inventory method

when accounting for supplies.

3. Paid employee salaries, $120,000. Accrued salaries at year end were $13,000. Accrued

salaries at the beginning of the year were $9,000.

4. Billed General Fund departments $400,000 for services provided to those departments.

Billings to the Enterprise Fund totaled $30,000. 90% of these billings were collected by

year end. The remaining 10% is not expected to be collected from the other funds until

85

Copyright © 2013 Pearson Education, Inc.

the second quarter of the next fiscal year.

5. The first semi-annual mortgage payment of $23,500 was made.

6. Paid $50,000 on account.

7. Supplies on hand at year end have a cost of $4,000. The beginning of the year inventory

was $6,000.

8. The second semi-annual mortgage payment of $23,500 was made.

9. Record depreciation on the building for the year.

Requirements:

7. Prepare the journal entries required in the Internal Service Fund. If no entry is required,

state “No entry required” and explain why.

8. Indicate the effects of each transaction on the accounting equation of the Internal Service

Fund accounts. If an element of the equation is not affected or if the net effect is zero,

put “NE” in the appropriate box. Do not leave any boxes blank.

Answers:

Requirement #1

86

Copyright © 2013 Pearson Education, Inc.

# Accounts Debit Credit

1 Building 450,000

Cash 100,000

Requirement #2

Trans

#

Current

Assets

Noncurrent

Assets

Current

Liabilities

Noncurrent

Liabilities

Net

Position

87

Copyright © 2013 Pearson Education, Inc.

4b NE NE NE NE NE

88

Copyright © 2013 Pearson Education, Inc.

Problem 3 – Financial Statement Preparation

The accounts listed below are taken from an Internal Service Fund adjusted trial balance (all

amounts are in thousands):

Accounts DR CR

Accounts Payable $44

Accumulated Depreciation – Buildings 200

Accumulated Depreciation – Vehicles and Equipment 210

Billings to Departments 981

Buildings $319

Capital Contribution 60

Cash 243

Construction in Progress 20

Depreciation Expense 50

Due from Other Funds 60

Due to Other Funds 24

Net Position, July 1, 20X2 729

Interest Expense 11

Interest Revenue 15

Investments 160

Land 120

Maintenance Expense 35

Mortgage Payable 50

Personnel Services Expense 630

Restricted Cash – Construction 90

Supplies Expense 251

Supplies Inventory 73

Transfer from General Fund 75

Vehicles and Equipment 326

$2,388 $2,388

Requirements: Prepare Statement of Fund Net Position and Statement of Revenues, Expenses,

and Changes in Fund Net Position for the year ended June 30, 20X3, for the City

of Bell Buckle.

Answers: See Excel file Ch11P-3S.xlsx.

Governmental and Nonprofit Accounting: Theory and Practice, 10e (Freeman)

Problems – Chapter 12

Problem 1 – Agency Fund Entries

Shelby County collects property taxes levied by the county for its General Fund. It also collects

89

Copyright © 2013 Pearson Education, Inc.

the taxes levied by two towns within the county—Ford’s Way and Foote’s Corner. The county

charges the towns a collection fee equal to 1% of taxes collected for those entities. Two percent

of the property taxes have been uncollectible historically. All amounts are in thousands of

dollars.

Transactions:

1. Taxes levied for 20X6 were $12,000 for the county, $5,000 for Ford’s Way, and $3,000

for Foote’s Corner.

2. During the year tax collections for the county totaled $9,000; $4,000 was collected for

Ford’s Way and $2,200 was collected for Foote’s Corner.

3. One percent of the gross taxes receivable were written off as uncollectible during the

year.

4. All cash collected, less the collection fee, was remitted to the appropriate fund or entity.

5. The collection fee was remitted to the appropriate fund or entity.

Requirement: Prepare the entries required in the Shelby County General Fund and in the

Shelby County Tax Agency Fund to record the transactions. . If no entry is

required, state “No entry required” and explain why.

90

Copyright © 2013 Pearson Education, Inc.