Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

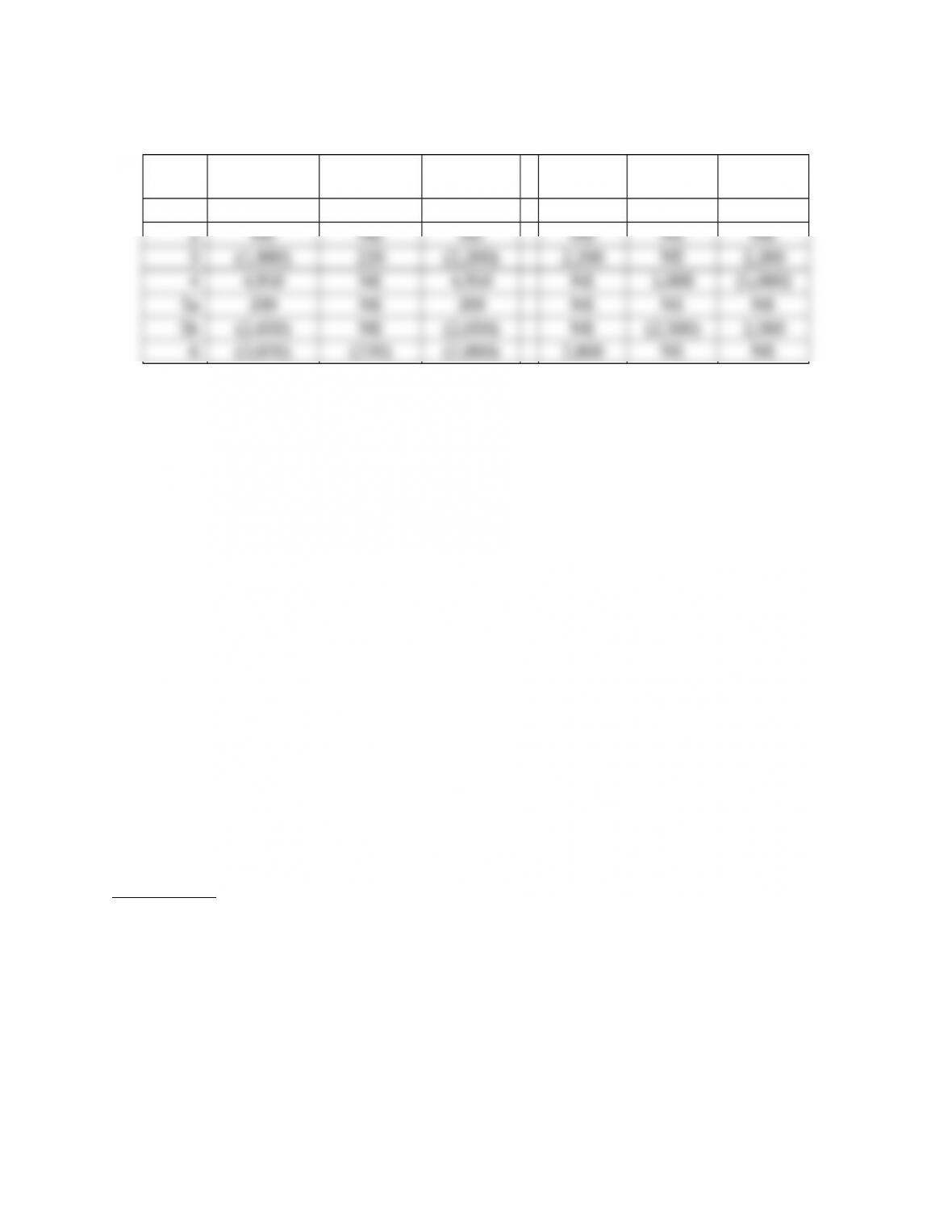

(2) Indicate the effects of each transaction on the accounting equation of the Capital

Projects Fund and on the General Capital Assets and General Long-Term Liabilities

accounts. If an element is not affected, put “NE” in the appropriate box.

41

Copyright © 2013 Pearson Education, Inc.

Answers:

# Accounts Debit Credit

A (2) Effects of journal entries

Trans

# Assets Liabilities

Fund

Balance GCA GLTL

Net

Position

42

Copyright © 2013 Pearson Education, Inc.

# Accounts Debit Credit

B (2) Effects of journal entries

Trans

# Assets Liabilities

Fund

Balance GCA GLTL

Net

Position

43

Copyright © 2013 Pearson Education, Inc.

Problem 2 – Bond Issue Issues

There are 4 separate scenarios for bond issuances below. For each scenario, prepare the journal

entry or entries for the transaction for the Capital Projects Fund and indicate the effects of each

scenario on the Capital Projects Fund balance sheet equation and the General Capital Assets and

General Long-Term Liabilities accounts.

Scenarios:

A. $3,000 in 6%, 15-year serial bonds are issued at par in a private placement.

B. $4,000 in 5%, 20-year serial bonds are issued at par. Bond issue costs were $100.

C. $5,000 in 4%, 25-year serial bonds are issued at 104. Bond issue costs were $150.

D. $6,000 in 4%, 30-year bonds were issued at 97. Bond issue costs were $200.

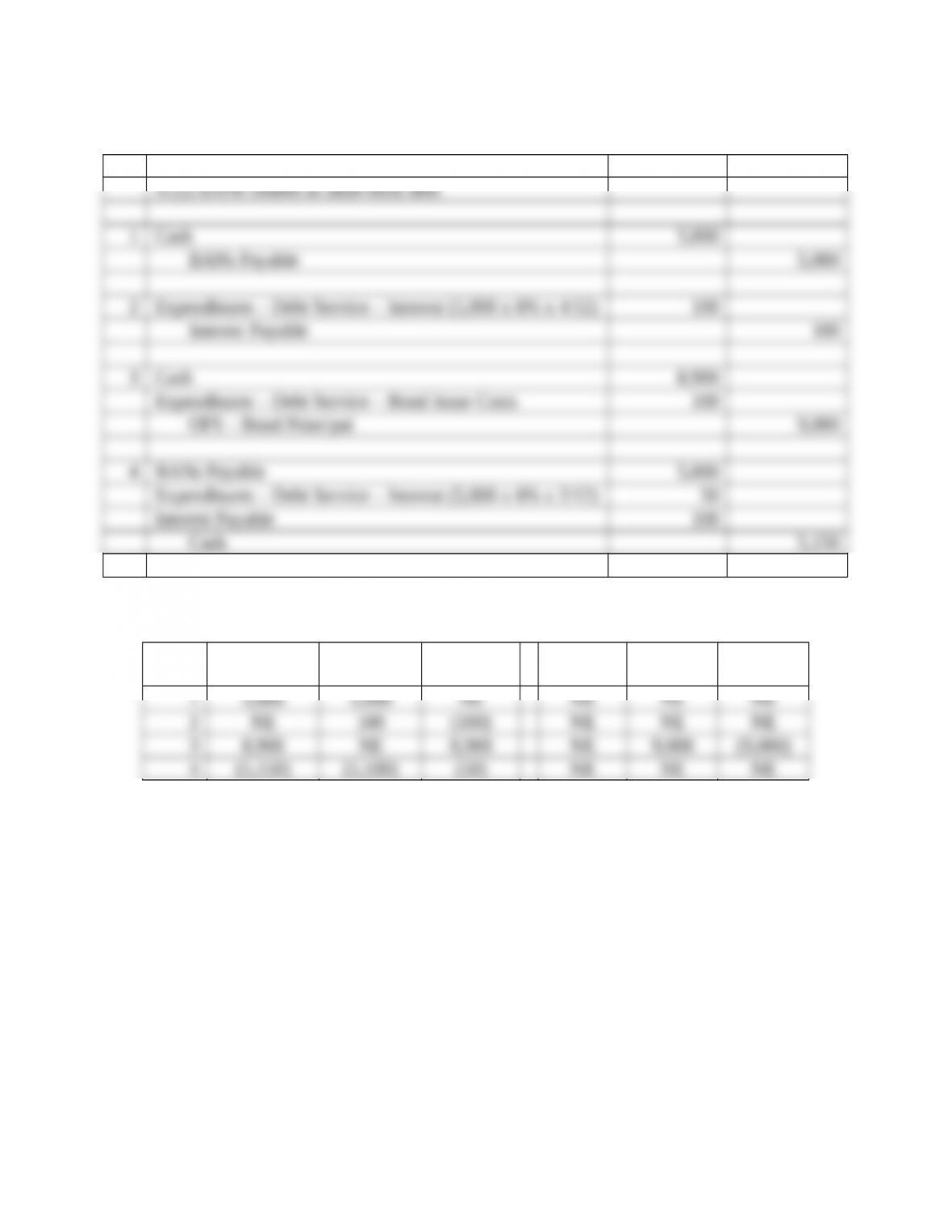

Answers: Journal entries

# Accounts Debit Credit

A Cash 3,000

Effects of journal entries

Trans

# Assets Liabilities

Fund

Balance GCA GLTL

Net

Position

44

Copyright © 2013 Pearson Education, Inc.

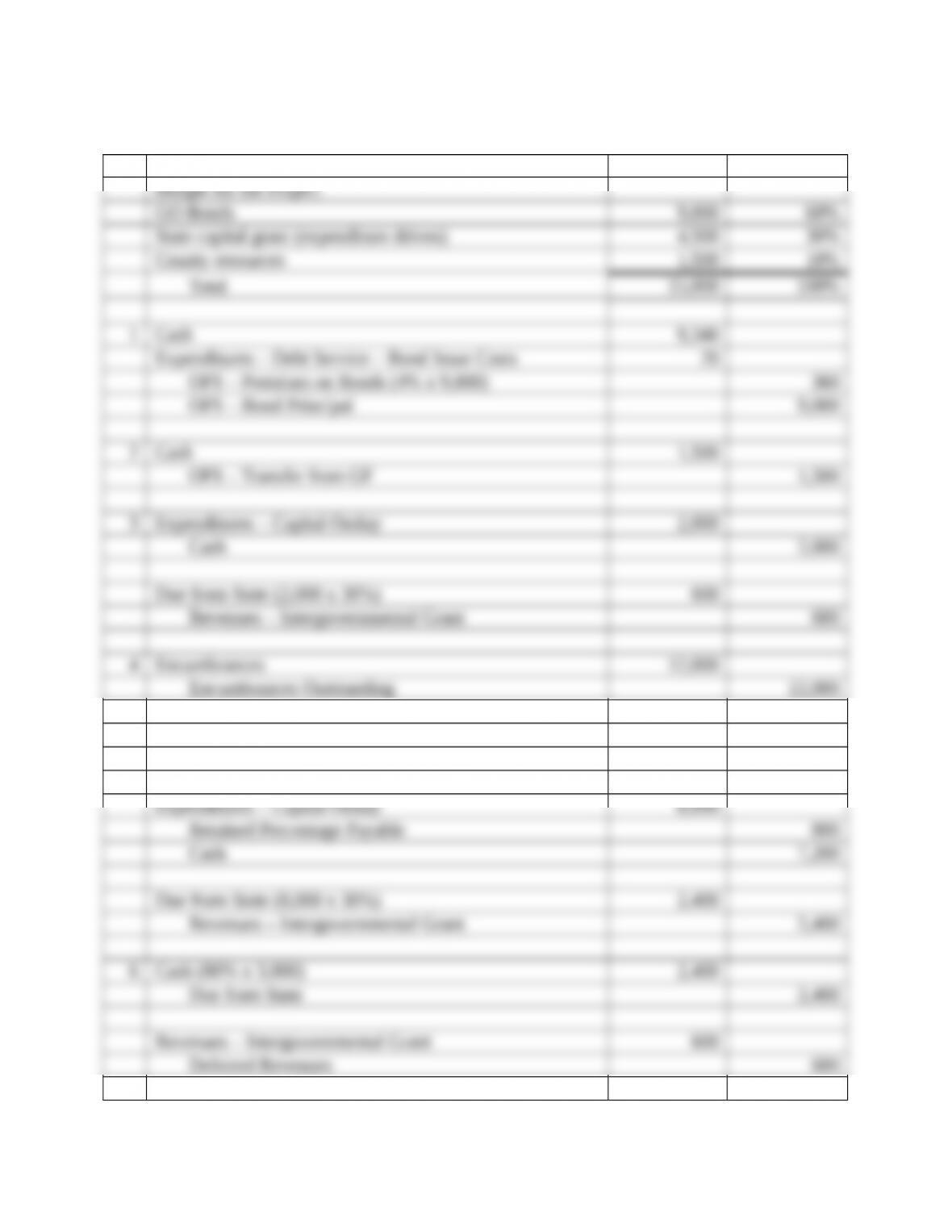

Problem 3 – Comprehensive Capital Projects Fund Problem

Requirements:

1. Prepare all the entries required in the Jail Addition Capital Projects Fund for Franklin

County for the following transactions and events. No explanations are required. If no

entry is required, state “No entry required” and state why. Assume that the bond

anticipation notes meet the criteria for being treated as long-term debt. June 30 is the

fiscal year end for Franklin County. All amounts are in thousands of dollars.

2. Indicate the effects of each transaction on the accounting equation of the Capital Projects

Fund and on the General Capital Assets and General Long-Term Liabilities accounts. If

an element is not affected, put “NE” in the appropriate box.

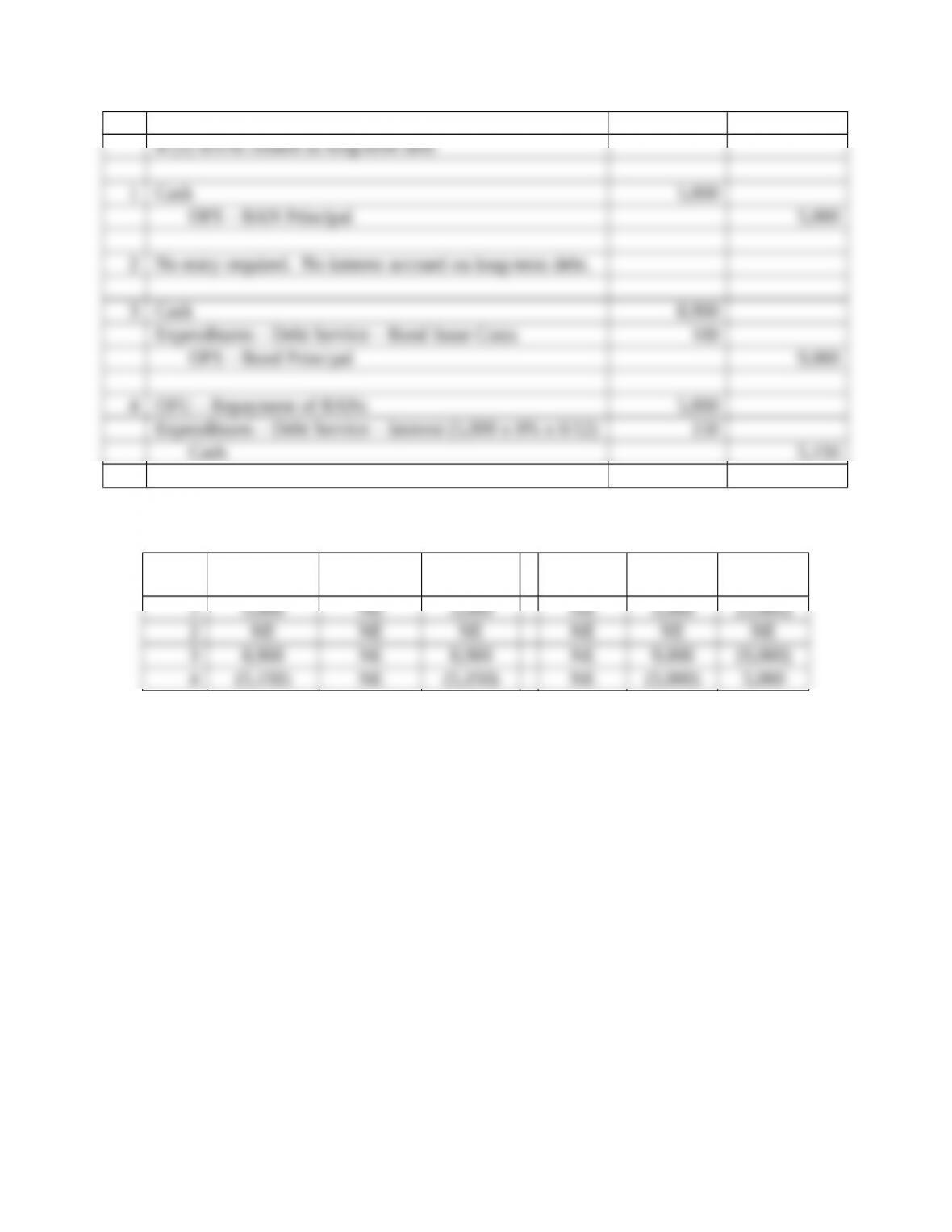

Transactions:

1. The county issued $2,500 of 8-month, 9% bond anticipation notes on August 1, 20X3.

The proceeds are to be used to begin construction of a recently approved addition to the

county jail.

2. On July 10, the county signed a contract for $5,000,000 for construction of the addition.

3. On November 30, the contractor billed the county for 40% of the work on the jail

addition. The actual cost of the work was $2,200. The county paid all but 10% of the

amount billed. The balance is to be paid upon completion and approval of the project.

4. The county issued $5,000 of 10-year, 8% bonds at par on March 31, 20X4. Bond issue

costs of $50 were withheld from the proceeds. Interest and one-tenth of the principal are

payable annually on the bonds. The bond proceeds are to be used to repay the bond

anticipation notes and to finance construction of the jail addition.

5. On March 31, the county transferred $200 from the General Fund to the Jail Addition

Capital Projects Fund to provide additional funding for the project. The BANs and

interest also were paid on that date.

6. In May the contractor billed the county $2,800 for the remainder of the work on the jail.

The county approved the facility and paid the contractor all amounts owed.

45

Copyright © 2013 Pearson Education, Inc.

Answers: 1. Journal Entries

# Accounts Debit Credit

1 Cash 2,500

OFS – BAN Principal 2,500

46

Copyright © 2013 Pearson Education, Inc.

2. Effects of journal entries

Trans

# Assets Liabilities

Fund

Balance GCA GLTL

Net

Position

1 2,500 NE 2,500 NE 2,500 (2,500)

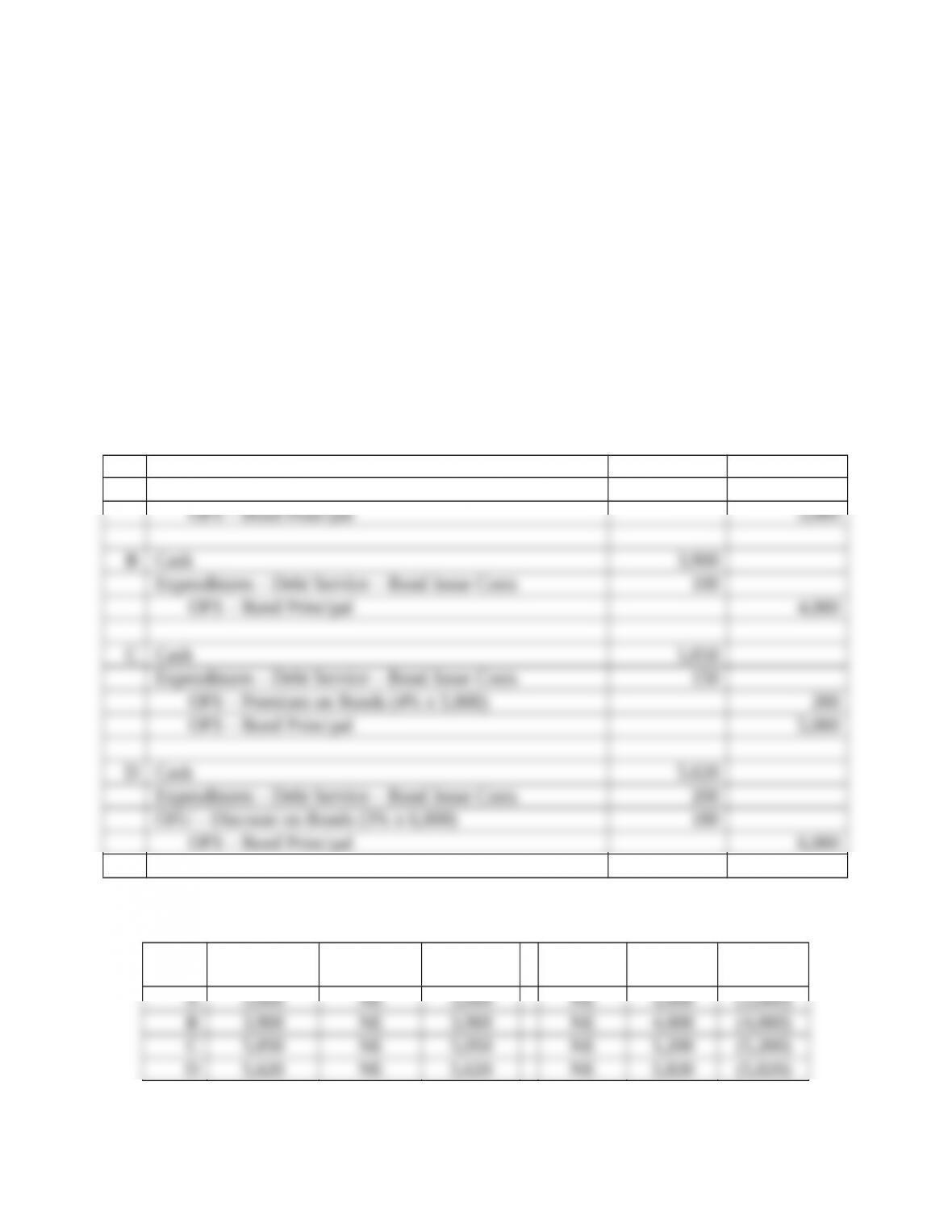

Problem 4 – Comprehensive Capital Projects Fund Problem with Budget

Moore County is developing a new all-sports county park. The estimated cost of the project is

$15,000 (all amounts are in thousands of dollars). Funding is being provided for the project

based on the following schedule:

General Obligation Bonds, 8%, 30-year serial bonds........................ 9,000

State capital grant (expenditure driven)............................................. 4,500

County resources (transfers from the General Fund)......................... 1,500

Total resources................................................................................... 15,000

Transactions:

1. The bonds were issued at 104 and with $20 in bond issue costs.

2. The funding from the General Fund was received.

3. The county purchased land for the project paying $2,000 in cash.

4. A contract for construction of the required facilities 12,000.

5. During the year, the county was billed $8,000 for the project. It was projected that this

billing is for 75% of the construction project. The county paid all but 10% of the amount.

The balance will be paid when the contract is completed.

6. Near the end of the fiscal year, the state paid the amount owed, less 20% that is in

question. This amount will be paid no earlier than 90 days into the following fiscal year.

Requirements:

1. Prepare all the entries required in the Park Capital Projects Fund for Moore County for

these transactions and events. No explanations are required. If not entry is required, state

“No entry required” and state why. All amounts are in thousands of dollars.

2. Indicate the effects of each transaction on the accounting equation of the Capital Projects

Fund and on the General Capital Assets and General Long-Term Liabilities accounts. If

an element is not affected, put “NE” in the appropriate box.

47

Copyright © 2013 Pearson Education, Inc.

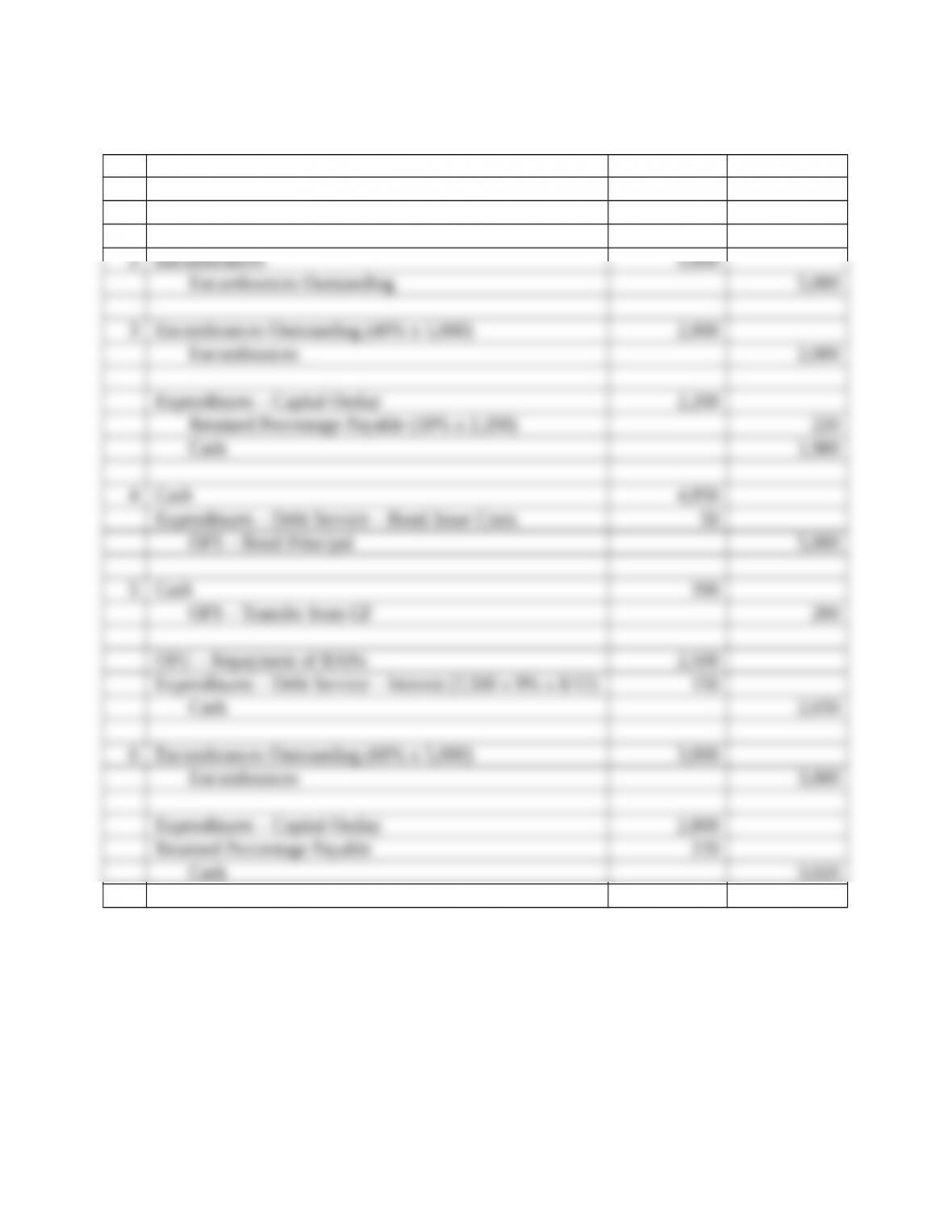

1. Journal entries

# Accounts Debit Credit

5 Encumbrances Outstanding (75% x 12,000) 9,000

Encumbrances 9,000

48

Copyright © 2013 Pearson Education, Inc.

2. Effects of transactions

Trans

# Assets Liabilities

Deferred

Inflows

Fund

Balance GCA GLTL

Net

Position

Governmental and Nonprofit Accounting: Theory and Practice, 10e (Freeman)

Problems – Chapter 8

Problem 1 – General Government Refunding Transactions

The City of Dandridge has $8,000 par value of general government, general obligation bonds

payable outstanding. The bonds have a call option at 102. The city has decided to call the bonds

at their call date. The city uses a Debt Service Fund for all refunding transactions. All amounts

are in thousands of dollars.

Transactions:

SITUATION A

1. The city issued $8,160 refunding bonds at par.

2. The city paid $8,160 to bondholders to retire the bonds at the call date.

SITUATION B

1. The city issued $4,000 of refunding bonds at par.

2. The city transferred $4,160 from the General Fund to the Debt Service Fund to provide

the additional resources needed to call the bonds.

3. The city paid $8,160 to bondholders to retire the bonds at the call date.

Requirements:

1. Prepare the journal entries required in a Debt Service Fund to record these transactions,

49

Copyright © 2013 Pearson Education, Inc.

assuming the bond anticipation notes do not qualify for long-term debt treatment. If no

entry is required, state “No entry required” and explain why.

2. Indicate the effects of each transaction on the accounting equation of the Debt Service

Fund and on the General Capital Assets and General Long-Term Liabilities accounts. If

an element is not affected, put “NE” in the appropriate box.

50

Copyright © 2013 Pearson Education, Inc.