# Accounts Debit Credit

1 Cash 300

# Accounts Debit Credit

121

Copyright © 2013 Pearson Education, Inc.

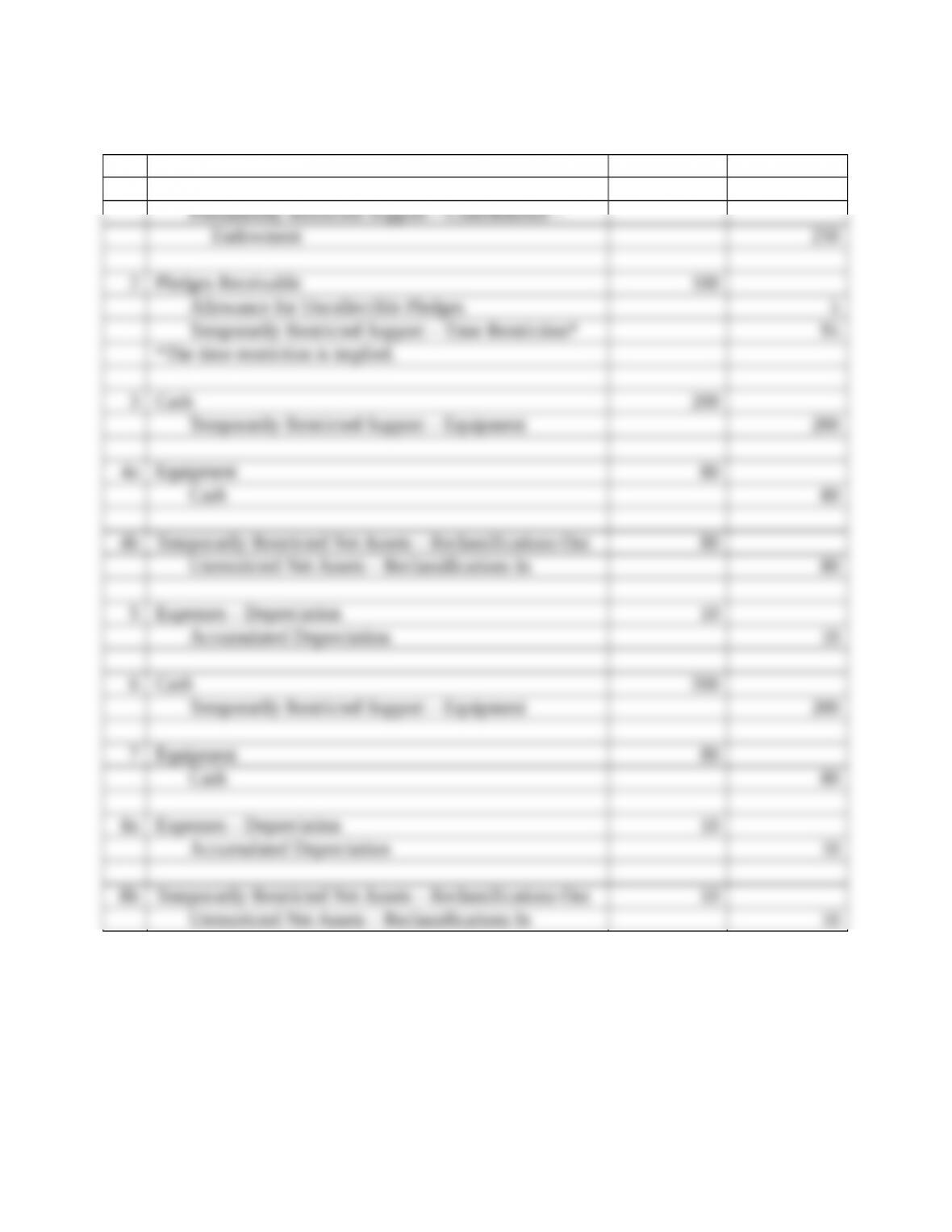

Problem 2 – Accounting for Restricted Gifts

Listed below are two transactions for an alcohol rehabilitation treatment program. All amounts

are in thousands of dollars.

Transactions:

1. Received pledges of $300 and cash gifts of $100 during the year to be used only for

alcohol rehabilitation treatment programs.

2. Incurred expenses of $220 for its alcohol rehabilitation program but paid the expenses

from unrestricted resources, not from available restricted resources.

Requirement: Prepare the journal entries for these transactions.

Answers:

# Accounts Debit Credit

Note that the FASB considers the restrictions met if restricted resources could have been used for

the expenses—even if they were not used.

Problem 3 – Reporting for Not-for-Profit Organizations

Requirements: Explain the way a nongovernmental, not-for-profit organization must report the

following items in its statement of activities:

A. Receipt of unrestricted contributions

B. Pledges restricted to a specific program

C. Collections, in a subsequent year, of pledges restricted to a specific purpose

D. Pledges restricted to fixed asset construction

E. Earnings on restricted investments

Answers:

122

Copyright © 2013 Pearson Education, Inc.

A. Unrestricted contributions received in cash are reported as revenues in the changes in

unrestricted net assets section of the statement of activities in the period received. If the

B. Pledges restricted to a specific program are reported as contributions in the changes in

The depreciation expense and the net assets released from restrictions are not necessarily

equal in amount. For instance, while they may be recognized over the same period,

residual value would not be taken into account in computing the net assets released from

restrictions—even if the same time period is appropriate.

Problem 4 – Statement of Activity for a Nongovernmental, Not-for-Profit Organization

Selected accounts of the Weinstein Musical Society, a nongovernment, not-for-profit

123

Copyright © 2013 Pearson Education, Inc.

organization for the year ended December 31, 20X5 is presented below in alphabetical order (all

amounts are in thousands of dollars and all accounts have a normal balance):

Administrative salaries……………………………………………………………………………………….. $45

Cash contributions restricted for Classical Music Appreciation Program………..….….…. 250

Collections of unrestricted pledges from prior year………………………….….….….….….….. 300

Depreciation—Office Equipment………………………………………………………….….….……... 2

Depreciation—Equipment—Classical Music Appreciation Program..….….…..…….….… 12

Depreciation—Maestro Program…………………………………………………………………….…... 5

Fundraising expenses………………………………………………………………………………..….….… 75

Investment Income…………………………………………………………………………………………..… 100

Materials and supplies used—Maestro Program…………………………………..….….….….…. 330

Payment of interest on note…………………………………………………………………………………. 22

Payment to retire long-term note that matured during the year……………………….….….… 250

Pledges during year (and outstanding at year end) to support Maestro Program…......... 1,200

Rent—Performance Halls—Professional Program…………………………………………………. 500

Salaries—Professional Program………………………………………………………..….….….….….. 379

Teacher salaries—Classical Music Appreciation Program…………………………..….….…... 23

Teacher salaries—Maestro Program…………………………………………………………..….….…. 77

Temporarily restricted net assets, January 1, 20X5……………………………..….….….….…... 1,100

Ticket sales—Performances of Musicians in the Professional Program…….…..….……... 150

Unrestricted cash contributions……………………………………………………………………………. 800

Unrestricted net assets, January 1, 20X5……………………………………………….….….….…... 320

Unrestricted pledges during year (and outstanding at year end)……………………………….. 540

Unrestricted earnings on investments of temporarily restricted investments…..…..….…. 58

All expenses of the Maestro and the Classical Music Appreciation Programs are payable from

donor restricted resources.

Requirement: Prepare the Statement of Activity for the Society

Answer:

124

Copyright © 2013 Pearson Education, Inc.

Weinstein Musical Society

Statement of Activities

For the Year Ended December 31, 20X5

125

Copyright © 2013 Pearson Education, Inc.

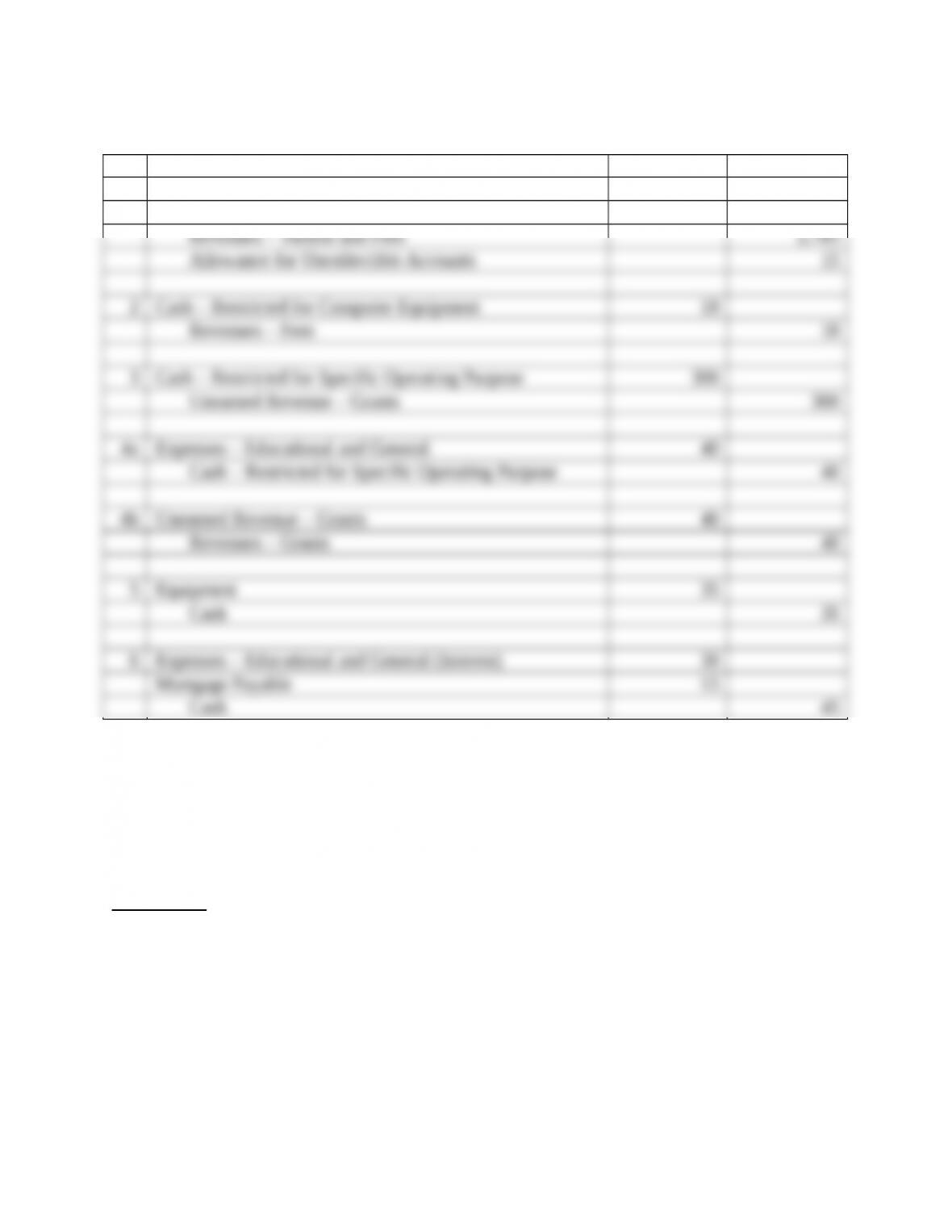

Problem 5 – Additional Journal Entries for a Nongovernmental, Not-for-Profit Organization

Transactions: The following selected transactions occurred for a nongovernment, not-for-profit

organization. All amounts are in thousands of dollars.

1. Received a contribution of stock to establish an endowment fund. The income from the

endowment is unrestricted. The donor had acquired the stock for $23 about 20 years

earlier. Its estimated fair value when donated was $250.

2. Pledges receivable at year end were $100, all from pledges received during the year. The

pledges are unrestricted and 5% percent of the pledges are estimated to be uncollectible.

The pledges expect to be collected early next year.

For questions 3-5, assume that the organization has adopted a policy that restrictions on

donations made for capital purposes are met when the capital item is purchased.

3. A cash gift of $200 was received restricted for the purchase of equipment.

4. Equipment of $80 was purchased from the gift restricted for this purpose.

5. Depreciation expense for the year on the equipment purchased is $10.

For questions 6-8, assume that the organization has adopted a policy that restrictions on

donations made for capital purposes are not met when the capital item is purchased.

6. A cash gift of $200 was received restricted for the purchase of equipment.

7. Equipment of $80 was purchased from the gift restricted for this purpose.

8. Depreciation expense for the year on the equipment purchased is $10.

Requirement: Prepare the journal entries for the above transactions.

126

Copyright © 2013 Pearson Education, Inc.

Answers:

# Accounts Debit Credit

1 Investments 250

Governmental and Nonprofit Accounting: Theory and Practice, 10e (Freeman)

Problems – Chapter 17

Problem 1 – Government College Journal Entries

127

Copyright © 2013 Pearson Education, Inc.

Below are selected transactions for the Lake County Community College (LCCC). LCCC

reports as a special government engaged only in business-type activities. All amounts are in

thousands of dollars.

Transactions:

1. Tuition and fees charged for the fall 20X3 semester totaled $2,800. Of this, $98 was

waived as a result of scholarship allowances, and another $15 is expected to be

uncollectible.

2. For the winter 20X4 semester LCCC collected a general student fee of $18. The full

amount of this fee is restricted for the purchase of computer equipment and software

needed to establish computer labs at the college.

3. The college received a reimbursement grant restricted to research on composite materials,

$300.

4. Salaries paid to researchers in the Composite Materials Lab of $40 qualified under the

research grant received.

5. The college purchased equipment for use in its building and grounds maintenance

department at a cost of $35. Unrestricted resources were used for this purpose.

6. The college paid $30 interest and $15 principal on one of its mortgages.

Requirement: Prepare the necessary journal entries to record these transactions.

128

Copyright © 2013 Pearson Education, Inc.

Answers:

# Accounts Debit Credit

1 Accounts Receivable 2,702

Revenue Deduction – Scholarship Allowances 98

Problem 2 – Governmental University Journal Entries

Selected transactions of Shelbyville State University are listed below. The university reports as a

special purpose government engaged in only business-type activities. All amounts are in

thousands of dollars.

Transactions:

1. Tuition and fees assessed total $4,500; 70% is collected immediately; scholarships

allowances are granted for $120; and $45 is expected to prove uncollectible.

2. Revenues collected from sales and services of the university bookstore, an auxiliary

enterprise, were $275.

3. Salaries and wages paid, $1,500; $62 of this was for employees of the university

bookstore.

4. Tuition remissions were granted in the amount of $35 for employees.

5. Mortgage payments totaled $520; $290 of this was for interest.

129

Copyright © 2013 Pearson Education, Inc.

6. Restricted contributions for the Master of Accountancy (MAcc) program were received,

$250.

7. Expenditures for the MAcc program were incurred and paid, $230.

8. Equipment was purchased from unrestricted resources, $34.

Requirement: Prepare the necessary journal entries to record these transactions.

Answers:

# Accounts Debit Credit

1 Cash (4,500 x 70%) 3,150

Accounts Receivable 1,230

Revenue Deduction – Scholarship Allowances 120

130

Copyright © 2013 Pearson Education, Inc.