Trans

# Assets Liabilities

Fund

Balance GCA GLTL

Net

Position

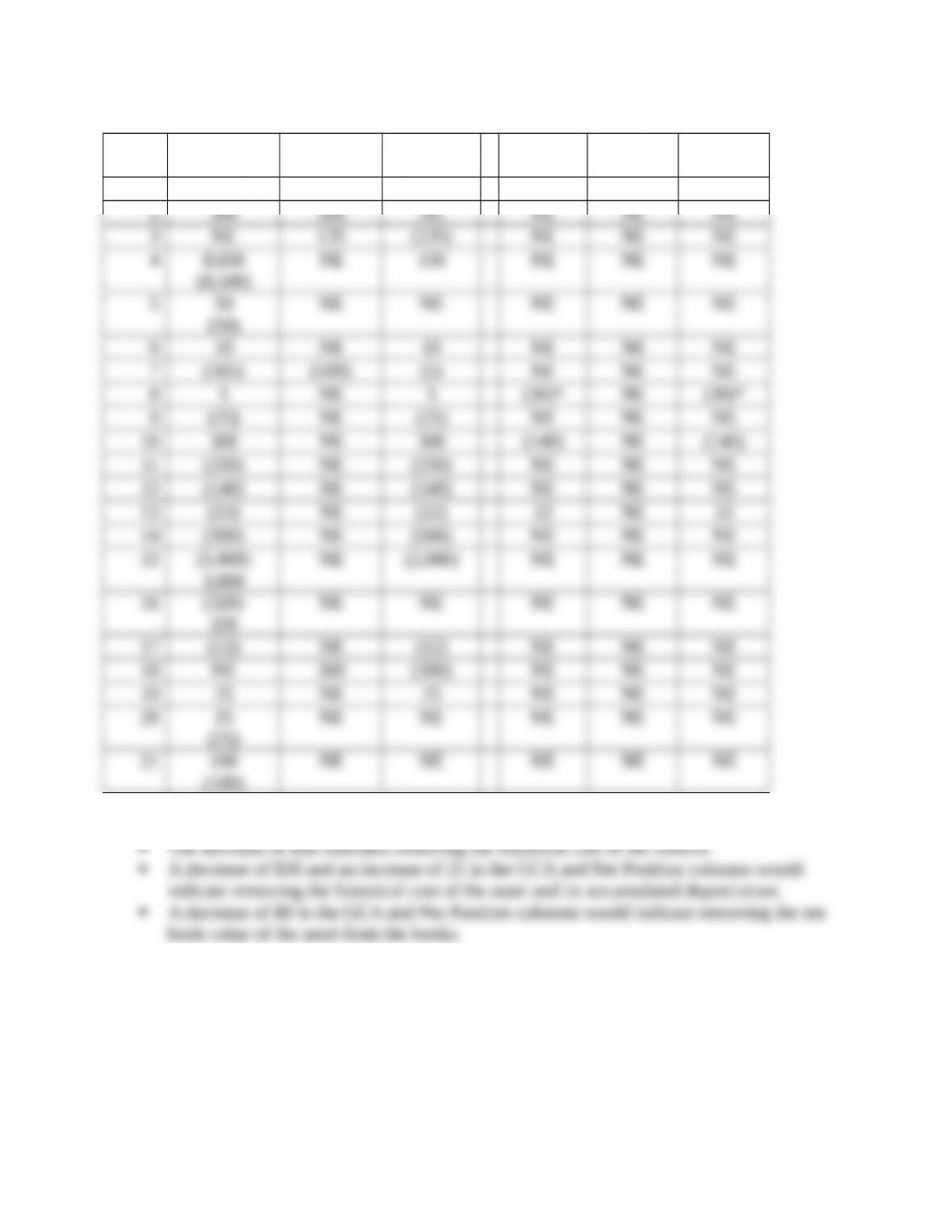

1 9,700 NE 9,700 NE NE NE

There are several possible answers to this question, all of them correct at this stage of the book:

Problem 4 – Financial Statement Preparation/Presentation

11

Copyright © 2013 Pearson Education, Inc.

(A) Prepare, using good form, a skeleton Statement of Revenues, Expenditures, and Changes in

Fund Balances.

(B) Next, insert the number representing each of the following items in the appropriate location

in the statement. If any item is not reported in the statement, explain why not.

1. Property taxes levied for and collected in the current year

2. Estimated cost of goods ordered but not received by year end

3. Transfer to another fund

4. Salary costs incurred during the year

5. Payment to retire long-term note principal

6. Payment of interest on long-term note

7. Accrued interest on long-term note

8. Receipt of proceeds of short-term note

9. Payment of interest on short-term note

10. Accrued interest on short-term note

11. Payment to retire principal of short-term note

12. Payment to establish an Enterprise Fund activity; no repayment expected

13. Long-term loan from the General Fund to an Internal Service Fund

14. Short-term loan from the General Fund to a Capital Projects Fund

15. Purchase of equipment

16. Purchase of temporary investment in securities

17. Receipt of proceeds from sale of fixed asset

18. Property taxes collected in advance on next year’s tax levy

19. Depreciation of equipment

20. Purchase of electricity from the Electric Enterprise Fund

12

Copyright © 2013 Pearson Education, Inc.

Answers:

Name of Government

Name of Fund

Statement of Revenues, Expenditures, and Changes in Fund Balance

For the Year Ended …

Not reported:

Problem 5 – Property Tax Entries

13

Copyright © 2013 Pearson Education, Inc.

Selected transactions for the Jackson Independent School District are presented below. All

amounts are in thousands of dollars.

1. On January 1 the school district levied property taxes of $8,000.The due date for the

taxes is March 31.The school district expects to collect all except $200 either by the end

of the fiscal year or within 60 days thereafter. The other $200 is expected to be

uncollectible.

2. During the first quarter (ending March 31) the school district collected $6,800 of its

current year’s property taxes. The rest of the taxes are past due.

3. On June 12 the school district wrote off $88 of property taxes as uncollectible.

4. From March 31 to December 31 the school district collected $700 of the property taxes

that were levied on January 1. The school district expects to collect an additional $300 of

these taxes during the first two months of the next fiscal year.

Instructions: Prepare the necessary journal entries. Dates and explanations may be omitted. If a

transaction requires no entry, do not leave it blank: state “No Entry Required” and explain why.

Answers:

# Accounts Debit Credit

Problem 6 – Fund Balance Calculations

14

Copyright © 2013 Pearson Education, Inc.

The City of Armona had the following assets and liabilities at June 30, 20X3, the end of its fiscal

year (all amounts are in thousands):

Assets

Cash

Investments

Taxes Receivable

Allowance for Uncollecible Taxes

Due from Special Revenue Fund

Inventory

Advance to Enterprise Fund

Total Assets

5,250

250

1,300

(200)

150

200

150

7,100

Liabiliies

Vouchers Payable

Short-Term Note Payable

Accrued Wages Payable

Due to Internal Service Fund

Total Liabiliies

750

1,000

200

50

2,000

Additional information:

1. The city received a state grant of $300 stipulating that it could be spent at any time on

equipment. To date, none of the money has been spent.

2. The city council, in a formal vote, decided to set aside another $500 for equipment

purchases.

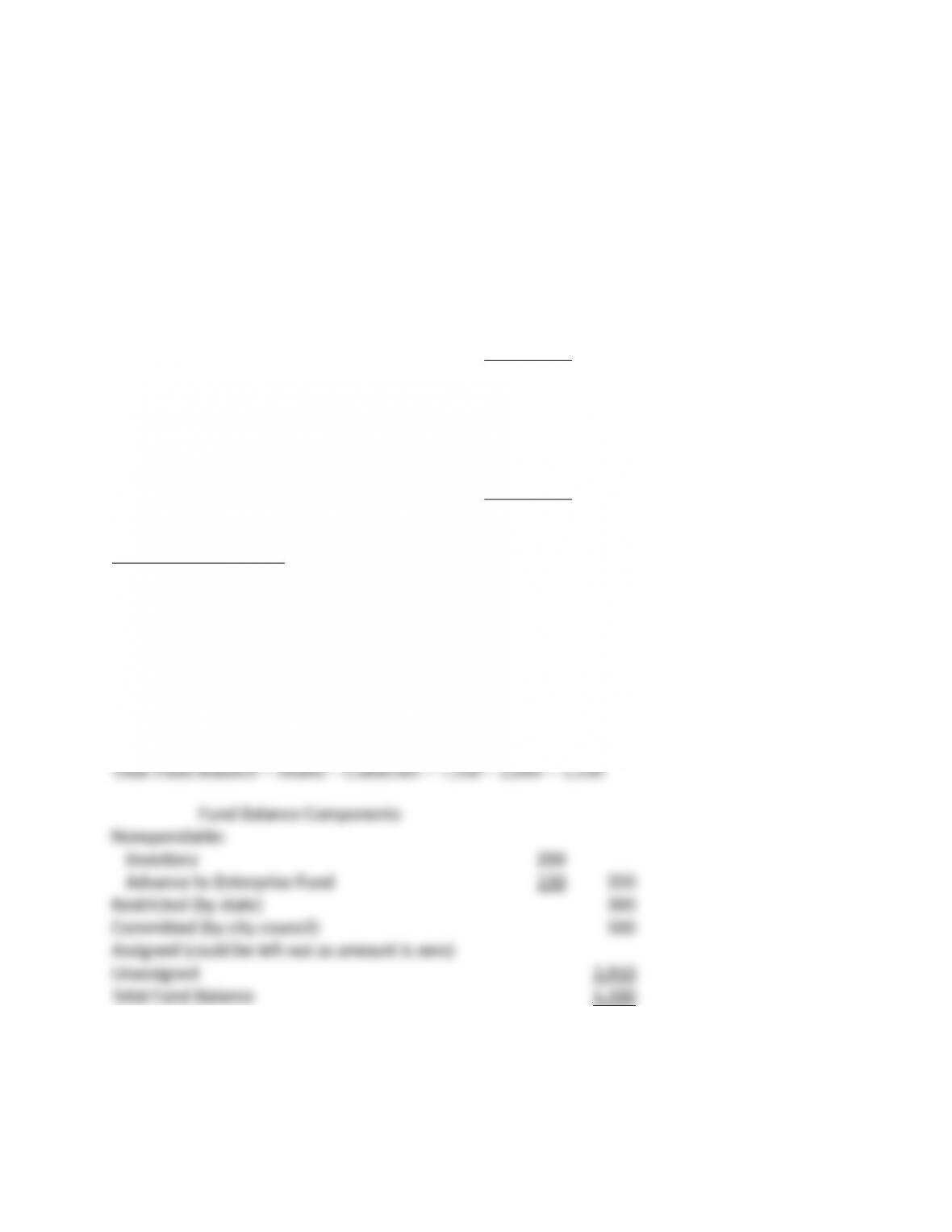

Requirement: Calculate the five components of Fund Balance.

Answer:

Governmental and Nonprofit Accounting: Theory and Practice, 10e (Freeman)

Problems – Chapter 4

15

Copyright © 2013 Pearson Education, Inc.

Problem 1 –Journal Entries, Subsidiary Ledger Effects, Transaction Analysis

5Selected transactions of the City of Miser Station General Fund for the 20X1 fiscal year are

presented on the following page. All amounts are in thousands of dollars.

General instructions:

f. Dates and formal explanations may be omitted, but number your entries appropriately.

g. All interest rates are annual percentage rates (APRs).

h. Record your entries on the lined paper provided with your answer pages. Sufficient space has

been provided to allow you to skip lines between entries.

i. When recording Revenues, classify them as Revenues–Property Taxes or Revenues–Other. When

recording expenditures, classify them as Expenditures–Operating, Expenditures–Debt Service, or

Expenditures–Capital Outlay. Additional detail for budgetary entries is not required.

j. Show all work for any amount required in an entry that is not given in the exam (except when

recording the amount necessary to balance the journal entry).

Requirements:

3. Prepare the general ledger journal entries for the transactions. If no entry is required, do not leave

it blank. State “No Entry Required” and briefly explain why.

4. Indicate the effects of the transaction on the accounting equations for the General Fund and the

General Capital Assets and General Long-Term Liabilities accounts. Do not leave a cell blank. If

a transaction has no effect on a particular element, use “NE”.

5. Maintain the subsidiary ledgers for Revenues – Property Taxes and Expenditures – Operating for

all appropriate entries.

Transactions:

22. The City Council approved the following budget for the fiscal year:

Appropriations…………………………………………………………..………………… 14,000

Estimated Revenues…………………………………………………………….……….. 12,000

Of these amounts, $8,000 is for operating expenditures and $10,000 is for property tax

revenues.

23. The property tax levy was recorded, $10,000, of which 3% will probably prove uncollectible.

24. The city ordered $200 in supplies.

25. The City borrowed $500 from the Blount National Bank on a two-month, 6% note.

26. Cash receipts were (see entry #2):

Property Taxes………………………………………………………………………..…..…..….. 8,500

License and Permits………………………………………………………………………….….. 150

Total Receipts……………………………………………………………………………..…. 8,650

27. The City Council revised the budget (see entry #1). Appropriations were reduced $3,000 and

Estimated Revenues were reduced $2,000 (Appropriations for Expenditures – Operating were

reduced $1,000; property tax revenues were not affected).

28. Of the previous supplies order (Entry #3), 75% of the order was received. The actual cost of the

goods received was $135. The amount due the vendor will be paid at a later date.

16

Copyright © 2013 Pearson Education, Inc.

29. City employees were paid, $25.

30. The city ordered a new police car. The estimated cost is $21.

31. The City repaid the short-term note (see entry #4) when due.

32. Wrote off $100 of taxes receivable as uncollectible (see entry #2).

33. Paid $12 to the Special Revenue Fund to repay it for General Fund employee salaries that were

inadvertently recorded as expenditures of that fund.

34. The city received the police car (see entry #9). The actual cost was $22. The vendor will be paid

at a later date.

35. The city collected $50 for licenses.

36. The city paid $157 on account.

Answers:

Requirement #1

# Accounts Debit Credit

Requirement #1 (continued)

# Accounts Debit Credit

17

Copyright © 2013 Pearson Education, Inc.

18

Copyright © 2013 Pearson Education, Inc.

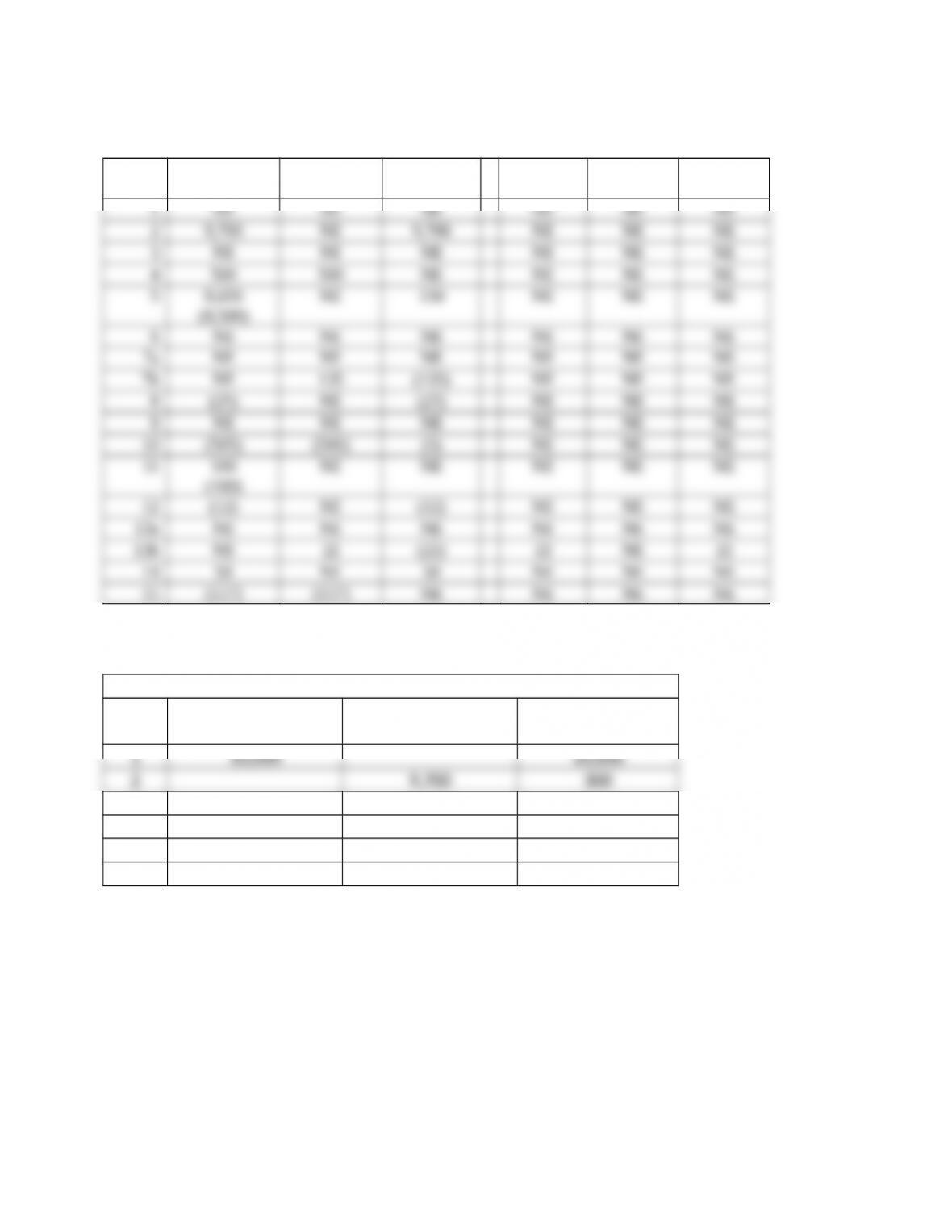

Requirement #2

Trans

# Assets Liabilities

Fund

Balance GCA GLTL

Net

Position

Requirement #3a

Revenues – Property Taxes

Trans

#

Dr.

Esimated Revenues

(Cr.)

Revenues

Dr. (Cr.)

Balance

19

Copyright © 2013 Pearson Education, Inc.

Requirement #3b

Expenditures – Operaing

Trans

#

Dr. (Cr.)

Encumbrances

Dr.

Expenditures

(Cr.)

Appropriaions

Dr. (Cr.)

Unencumbered

Balance

1 (14,000) (14,000)

Problem 2 – Closing Entries

Listed below (in alphabetical order) are the general ledger and budgetary accounts for the City of

Walland. All balances are year end, unless otherwise noted. All accounts have a normal balance.

At the end of the year, the City Council passed an ordinance that all outstanding orders would be

honored in the following fiscal year. Also, the Finance Officer set aside $40 for equipment

replacement.

Requirements:

1. Prepare the Statement of Revenues, Expenditures, and Changes in Fund Balance for the year

ended June 30, 20X4.

2. Prepare the Balance Sheet for the year ended June 30, 20X4.

3. Prepare all necessary closing entries.

20

Copyright © 2013 Pearson Education, Inc.