Archives: Solution Manual

Chapter 14 There is judgment in classifying the metrics and initiatives

483 MBA 14–4 1. Financial 2. Internal process 3. Customer 4. Learning and innovation 5. Customer 6. Learning and innovation 7. Learning and innovation 8. Customer 9. Financial 10. Learning and innovation 11. Learning and innovation 12. Internal process 13. […]

Chapter 14 The Touring Bike Division has a higher investment

473 P14–4 1. Return on Investment = Profit Margin × Investment Turnover Return on Investment = Operating Income Sales × AssetsInvested Sales Jet Ski Division: ROI = 0$12,000,00 $1,680,000 × 0$15,000,00 0$12,000,00 = 14.0% × 0.80 = 11.2% 2. AMAZING […]

Chapter 14 Studio Entertainment has a strong profit margin and

463 E14–12 a. 1.50 = 12% ÷ 8% b. 20% = 16% × 1.25 c. 20% = 24% ÷ 1.20 d. 1.50 = 15% ÷ 10% e. 17% = 10% × 1.70 E14–13 a. Return on Investment = Profit Margin […]

Chapter 14 The report for the plant managers would contain more

453 CHAPTER 14 DECENTRALIZED OPERATIONS CLASS DISCUSSION QUESTIONS 1. In a cost center, the department manager is responsible for and has authority over costs only. In a profit center, the manager’s re- sponsibility and authority extend to costs and revenues. […]

Chapter 13 The underlying reason for this decrease in passenger

445 MBA 13–5 1. January: 49,000 patient beds used (24,500 patients × 2.0 nights) February: 41,400 patient beds used (23,000 patients × 1.8 nights) March: 55,440 patient beds used (25,200 patients × 2.2 nights) 2. January: 55,800 available patient beds: […]

Chapter 13 Report errors can cause doctors to draw incorrect

435 P13–4, Concluded c. Direct Labor Cost Variance Rate variance: Direct Labor Rate Variance = (Actual Rate per Hour – Standard Rate per Hour) × Actual Hours = ($18.75 – $18.00) × 2,160 hrs.* = $1,620 Unfavorable Variance *60 employees […]

Chapter 13 William chairs from the production budget multiplied

425 P13–1, Continued 3. A B C D E F 1 ROYAL BRITISH FURNITURE COMPANY 2 Direct Materials Purchases Budget 3 For the Month Ending March 31 4 Direct Materials 5 Fabric (sq. yds.) Wood (lineal ft.) Filler (cu. ft.) […]

Chapter 13 Determine the standard direct materials and direct labor

415 E13–24 Rate variance: Direct Labor Rate Variance = (Actual Rate per Hour – Standard Rate per Hour) × Actual Hours = ($18.50 – $19.00) × 1,100 hrs. = $(550) Favorable Variance Time variance: Direct Labor Time Variance = (Actual […]

Chapter 13 For the Month Ending August 314 Variable factory

405 E13–11 A B C 1 NUTTY CANDY COMPANY 2 Factory Overhead Cost Budget 3 For the Month Ending August 31 4 Variable factory overhead costs: 5 Manufacturing supplies $ 45,000 6 Power and light 28,000 7 Production supervisor wages […]

Chapter 13 The three major objectives of budgeting are

395 CHAPTER 13 BUDGETING AND STANDARD COSTS CLASS DISCUSSION QUESTIONS 1. The three major objectives of budgeting are (1) to establish specific goals for future oper- ations, (2) to direct and coordinate plans to achieve the goals, and (3) to […]

Chapter 12 The cost-plus approach price of $87 should be viewed as

385 P12–5, Concluded 4. a. Variable cost amount per unit: $50.00 Total variable costs: $50 × 20,000 units = $1,000,000 b. Markup Percentage = Costs VariableTotal Costs Fixed Total +Profit Desired = $1,000,000 $160,000+$340,000+$240,000 = $1,000,000 $740,000 = 74% c. […]

Chapter 12 Revenue from sale of 125,000 additional units at

375 E12–12 a. MADISON INDUSTRIES INC. Sell to Story Mills Company Differential Analysis Report Differential revenue from accepting the offer: Revenue from sale of 125,000 additional units at $41 ……………. $5,125,000 Differential cost of accepting the offer: Variable costs from […]

Chapter 12 This decision is an example of a make-or-buy decision

365 CHAPTER 12 DIFFERENTIAL ANALYSIS AND PRODUCT PRICING CLASS DISCUSSION QUESTIONS 1. a. Differential revenue is the amount of increase or decrease in revenue ex– pected from a particular course of action compared with an alternative. b. Differential cost is […]

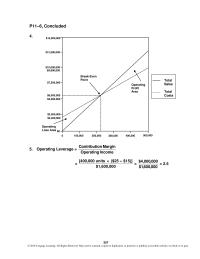

Chapter 11 They are really longer-term investments

357 P11–6, Concluded 4. $12,500,000 $7,500,000 $6,000,000 $5,000,000 $10,000,000 $9,900,000 Break-Even Point Operating Profit A rea Total Sales Total Costs 5. Operating Leverage = Contribution Margin Operating Income = [400,000 units × ($25 –– $15)] $1,600,000 = 000,600,1$ 000,000,4$ = […]

Chapter 11 Units because the sales mix is weighted more toward

349 P11–3 1. Break-Even Sales (units) = arginMonContributiUnit CostsFixed = 70$ 000,420$ = 6,000 units 2. Sales (units) = Fixed Costs + Target Profit Unit Contribution Margin = 70$ 000,490$ = 70$ 000,70$+000,420$ = 7,000 units 3. 4. $140,000 = […]

Chapter 11 The contribution margin earned per new subscriber is essentially

340 E11–14 Break-Even Sales (units) = arginM onContributiUnit Costs Fixed = $40,000 $40 – $X = 8,000 cookbooks Variable cost per cookbook: $40,000 = 8,000 cookbooks × ($40 – $X) Variable cost per cookbook: cookbooks 000,8 000,40$ = $40 – […]

Chapter 11 CVP analysis depends on five primary assumptions

331 CHAPTER 11 COST-VOLUME-PROFIT ANALYSIS CLASS DISCUSSION QUESTIONS 1. Total variable costs vary in direct proportion to changes in the level of activity. Unit varia- ble costs remain the same with changes in the level of activity. 2. a. Variable […]

Chapter 10 A good first look would be to isolate materials costs

323 MBA 10–4, Concluded c. The Friday–Monday phenomenon is likely related to the workforce, but the same cannot be said about the larger increasing trend over the four weeks. It could be caused by any number of factors. A good […]

Chapter 10 Only the direct assembly labor has yet to be applied

315 P10–2, Concluded 4. Schedule of completed jobs on hand, April 30, 20Y4*: Direct Direct Factory Job Materials Labor Overhead Total Finished Goods, April 30 (Job 405) …………………….. $3,200 $4,000 $960 $8,160 *This schedule supports the finished goods account as […]

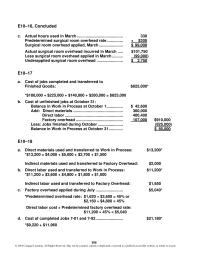

Chapter 10 Work-in-process inventory Materials used in production

306 E10–16, Concluded c. Actual hours used in March …………………………………… 330 Predetermined surgical room overhead rate …………… × $300 Surgical room overhead applied, March …………………. $ 99,000 Actual surgical room overhead incurred in March ….. $101,750 Less surgical room overhead […]

Chapter 10 which enables management to adjust future pricing policies

297 CHAPTER 10 ACCOUNTING SYSTEMS FOR MANUFACTURING OPERATIONS CLASS DISCUSSION QUESTIONS 1. Managerial accounting differs from financial accounting in the following ways: (1) Financial accounting records and re- ports transactions and events using generally accepted accounting prin- ciples (GAAP), while […]

Chapter 9 The times interest earned of 8.3 implies that there is little

291 Case 9–4 1. a. Return on Total Assets = AssetsTotal Average Expense Interest + Income Net Year 3: $752 + $12 $9,760 = 7.8% Year 2: $845 + $4 $9,467 = 9.0% Year 1: $734 + $45 $9,288 = […]

Chapter 9 The Elk head management should consider the risk of not

283 P9–4 1. Working capital: $2,790,000 $3,690,000 – $900,000 2. Current ratio: 4.1 $3,690,000 ÷ $900,000 3. Quick ratio: 2.5 $2,250,000 ÷ $900,000 4. Accounts receivable turnover: 16.0 $10,000,000 ÷ [($740,000 + $510,000) ÷ 2] 5. Day’s sales in receivables: […]

Chapter 9 Gain from discontinued operations Net income

274 E9–19 a. Debt ratio = Total Liabilities Total Assets $4,000,000 $15,300,000* = 26.14% * Total Assets = Total Liabilities + Total Stockholders’ Equity $15,300,000 = $4,000,000 + $11,300,000 b. Ratio of Fixed Assets to Long-Term Liabilities = sLiabilitie ermT–Long […]

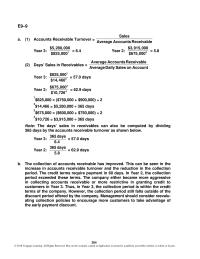

Chapter 9 The company either became more aggressive in collecting

264 E9–9 a. (1) Accounts Receivable Turnover = Sales A verage Accounts Receivable Year 3: 1 $5,280,000 $825,000 = 6.4 Year 2: 3 $3,915,000 $675,000 = 5.8 (2) Days’ Sales in Receivables = Accounton Sales Daily Average Receivable AccountsAverage Year […]

Chapter 9 The inventory turnover could be high because the quantity

255 CHAPTER 9 METRIC ANALYSIS OF FINANCIAL STATEMENTS CLASS DISCUSSION QUESTIONS 1. Horizontal analysis is the percentage analy- sis of increases and decreases in compara- tive financial statements. Each item on the most recent statement is compared with the related […]

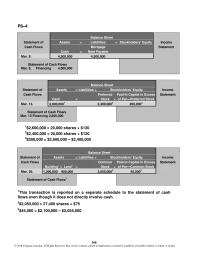

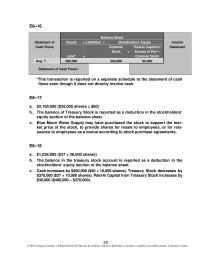

Chapter 8 This transaction is reported on a separate schedule

246 P8–4 Balance Sheet Statement of Assets = Liabilities + Stockholders’ Equity Income Cash Flows Mortgage Statement Cash = Note Payable Mar. 8. 4,500,000 4,500,000 Statement of Cash Flows Mar. 8. Financing 4,500,000 Balance Sheet Statement of Assets = Liabilities […]

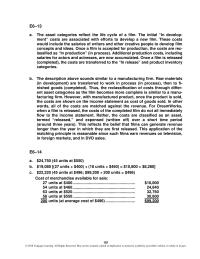

Chapter 8 Supply may have purchased the stock to support the market

E8–16 Balance Sheet Statement of Assets = Liabilities + Stockholders’ Equity Income Cash Flows Common Paid-In Capital in Statement Land* = Stock + Excess of Par— Common Stock Aug. 7. 280,000 200,000 80,000 Statement of Cash Flows* *This transaction is […]

Chapter 8 The primary purpose of a stock split is to bring

227 CHAPTER 8 LIABILITIES AND STOCKHOLDERS’ EQUITY CLASS DISCUSSION QUESTIONS 1. Accounts payable and accruals 2. Short-term notes payable may be issued to purchase merchandise or other assets or to satisfy an account payable which was cre- ated earlier. 3. […]

Chapter 7 This is an unfavorable change and implies that JetBlue

MBA 7–7 1. Year 2 Year 1 Fixed asset turnover: ($5,817 ÷ $5,431) ………………………….. 1.07 ($5,441 ÷ $5,043) ………………………….. 1.08 2. JetBlue’s asset turnover decreased slightly by 0.01 from 1.08 in Year 1 to 1.07 in Year 2. This is […]

Chapter 7 Land improvements do lose their ability to provide services

212 E7–18 a. Property, Plant, and Equipment (in millions): Year 2 Year 1 Land and buildings ……………………………………………. $ 2,439 $ 2,059 Machinery, equipment, and internal-use software .. 15,743 6,926 Office furniture and equipment …………………………… 241 184 Other fixed assets related […]

Chapter 7 Fixed assets have the following characteristics

205 CHAPTER 7 FIXED ASSETS, NATURAL RESOURCES, AND INTANGIBLE ASSETS CLASS DISCUSSION QUESTIONS 1. Fixed assets have the following characteris- tics: (a) They exist physically and, thus, are tan- gible assets. (b) They are owned and used by the com- […]

Chapter 6 Apple has a much higher inventory turnover

197 MBA 6–7, Concluded 6. HP’s accounts receivable turnover in Year 2 of 6.3 has increased slightly from 6.2 in Year 1. Days’ sales in receivables has decreased from 59 days in Year 1 to 58 days in Year 2. […]

Chapter 6 The asset categories reflect the life cycle of a film

181 E6–13 a. The asset categories reflect the life cycle of a film. The initial “In develop- ment” costs are associated with efforts to develop a new film. These costs would include the salaries of writers and other creative people […]

Chapter 5 Although the cash burn decreased in Year 4 to

165 MBA 5–3 1. Year 4 Year 3 Year 2 Year 1 Monthly cash expenses: $(5,026) ÷ 12 ……………………………… $(419) $(5,537) ÷ 12 ……………………………… $(461) $(4,203) ÷ 12 ……………………………… $(350) $(8,105) ÷ 12 ……………………………… $(675) 2. Ratio of cash to […]

Chapter 5 This violates the segregation of duties between the handling

157 PROBLEMS P5–1 Strengths: a, b, e, f Weaknesses: c. An independent person (for example, a supervisor) should count the cash in each cashier’s cash register, unlock the record, and compare the amount of cash with the amount on the […]

Chapter 5 This form should be delivered via intracompany mail to

149 E5–13 a. $9,380 b. $9,300 c. The cash overage of $80 should be recorded as Cash Short and Over. d. The cashier should receive additional training. E5–14 The use of the voucher system is appropriate, the essentials of which […]

Chapter 5 Fraud is unlikely without collusion between two

141 CHAPTER 5 INTERNAL CONTROL AND CASH CLASS DISCUSSION QUESTIONS 1. a. Congress passed the Sarbanes- Oxley Act because of the Enron, WorldCom, Tyco, Adelphia, and oth- er financial scandals that caused stockholders, creditors, and other in- vestors to lose […]

Chapter 4 the markup percent declined from 42.4% in Year 1

132 MBA 4–3 Metric Effects Liquidity Profitability Transaction Working Capital Gross Profit Percent Dec. 31 $(17,100) Decrease MBA 4–4 Metric Effects Liquidity Profitability Transaction Working Capital Ability to Achieve Gross Profit Percent of 30% July 31 $(7,500) Decrease (55.6%) Note: […]

Chapter 4 Estimated returns inventory Total property,

123 P4–3 1. Snipes Company Balance Sheet Statement of Assets =Liabilities +Stockholders’ Equity Income Cash Flows Accts. Retained Statement Cash + Rec. +Inv. = Earnings June 8. (400) 17,885* (10,000) 7,485 June 8. Statement of Cash Flows Income Statement June […]

Chapter 4 Interest revenue should be reported under the caption

113 E4–14 a. Balance Sheet Statement of Assets =Liabilities +Stockholders’ Equity Income Cash Flows Accts. Statement Inventory = Payable 84,280* 84,280 * $84,280 = $86,000 – ($86,000 × 2%) b. Balance Sheet Statement of Assets =Liabilities +Stockholders’ Equity Income Cash […]

Chapter 3 This raises a question of the viability of retail stores as a means

93 METRIC-BASED ANALYSES MBA 3–1 Metric Effects Transactions Liquidity Quick Assets Profitability Net Income – Accrual Basis a. Issued common stock $35,000 — b. Pur. supplies on credit — — c. Paid accounts payable (800) — d. Earned fees 31,300 […]

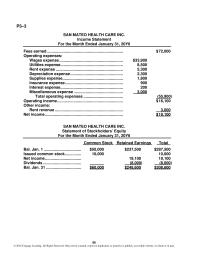

Chapter 3 Changes in noncash current operating assets and liabilities

P3–3 SAN MATEO HEALTH CARE INC. Income Statement For the Month Ended January 31, 20Y6 Fees earned …………………………………………………………… $ 72,000 Operating expenses: Wages expense …………………………………………………. $33,900 Utilities expense ………………………………………………… 8,500 Rent expense ……………………………………………………. 5,300 Depreciation expense ………………………………………… 2,300 Supplies expense […]

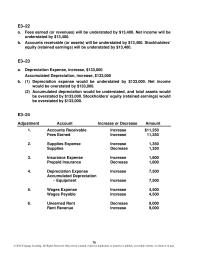

Chapter 3 Accumulated depreciation” should be deducted from the related fixed

76 E3–22 a. Fees earned (or revenues) will be understated by $13,400. Net income will be understated by $13,400. b. Accounts receivable (or assets) will be understated by $13,400. Stockholders’ equity (retained earnings) will be understated by $13,400. E3–23 a. […]

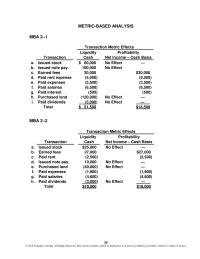

Chapter 2 The increase in cost of goods sold should be investigated as

59 METRIC-BASED ANALYSIS MBA 2–1 Transaction Metric Effects Liquidity Profitability Transaction Cash Net Income – Cash Basis a. Issued stock $ 60,000 No Effect — b. Issued note pay. 100,000 No Effect c. Earned fees 30,000 $30,000 d. Paid rent […]

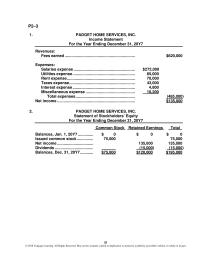

Chapter 2 his also affects the statement of stockholders’ equity and

51 P2–3 1. PADGET HOME SERVICES, INC. Income Statement For the Year Ending December 31, 20Y7 Revenues: Fees earned ………………………………………………………. $620,000 Expenses: Salaries expense ……………………………………………….. $272,000 Utilities expense ………………………………………………… 85,000 Rent expense …………………………………………………….. 70,000 Taxes expense …………………………………………………… 43,000 Interest expense […]

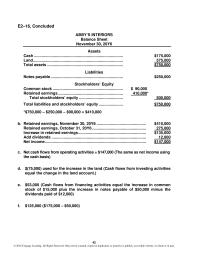

Chapter 2 Cash receipts from issuing notes payable

42 E2–16, Concluded ABBY’S INTERIORS Balance Sheet November 30, 20Y6 Assets Cash ……………………………………………………………………… $175,000 Land ………………………………………………………………………. 575,000 Total assets …………………………………………………………… $750,000 Liabilities Notes payable ………………………………………………………… $250,000 Stockholders’ Equity Common stock ………………………………………………………. $ 90,000 Retained earnings ………………………………………………….. 410,000* Total stockholders’ equity […]

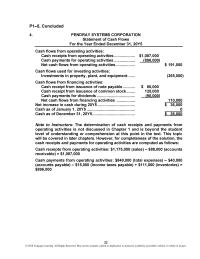

Chapter 1 This is due to the widespread acceptance and use of its products

23 P1–5, Concluded 4. PENDRAY SYSTEMS CORPORATION Statement of Cash Flows For the Year Ended December 31, 20Y5 Cash flows from operating activities: Cash receipts from operating activities ………………. $1,087,000 Cash payments for operating activities ………………. (896,000) Net cash flows […]

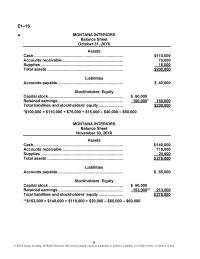

Chapter 1 The income statement of Dell would provide the most

8 E1–16 a. MONTANA INTERIORS Balance Sheet October 31, 20Y8 Assets Cash ……………………………………………………………………… $110,000 Accounts receivable ………………………………………………. 75,000 Supplies ………………………………………………………………… 15,000 Total assets …………………………………………………………… $200,000 Liabilities Accounts payable…………………………………………………… $ 40,000 Stockholders’ Equity Capital stock ………………………………………………………….. $ 60,000 Retained earnings ………………………………………………….. […]

Chapter 1 The objective of most businesses is to maximize profits

1 CHAPTER 1 THE ROLE OF ACCOUNTING IN BUSINESS CLASS DISCUSSION QUESTIONS 1. The objective of most businesses is to maximize profits. Profit is the difference between the amounts received from customers for goods or services pro- vided and the […]