385

P12–5, Concluded

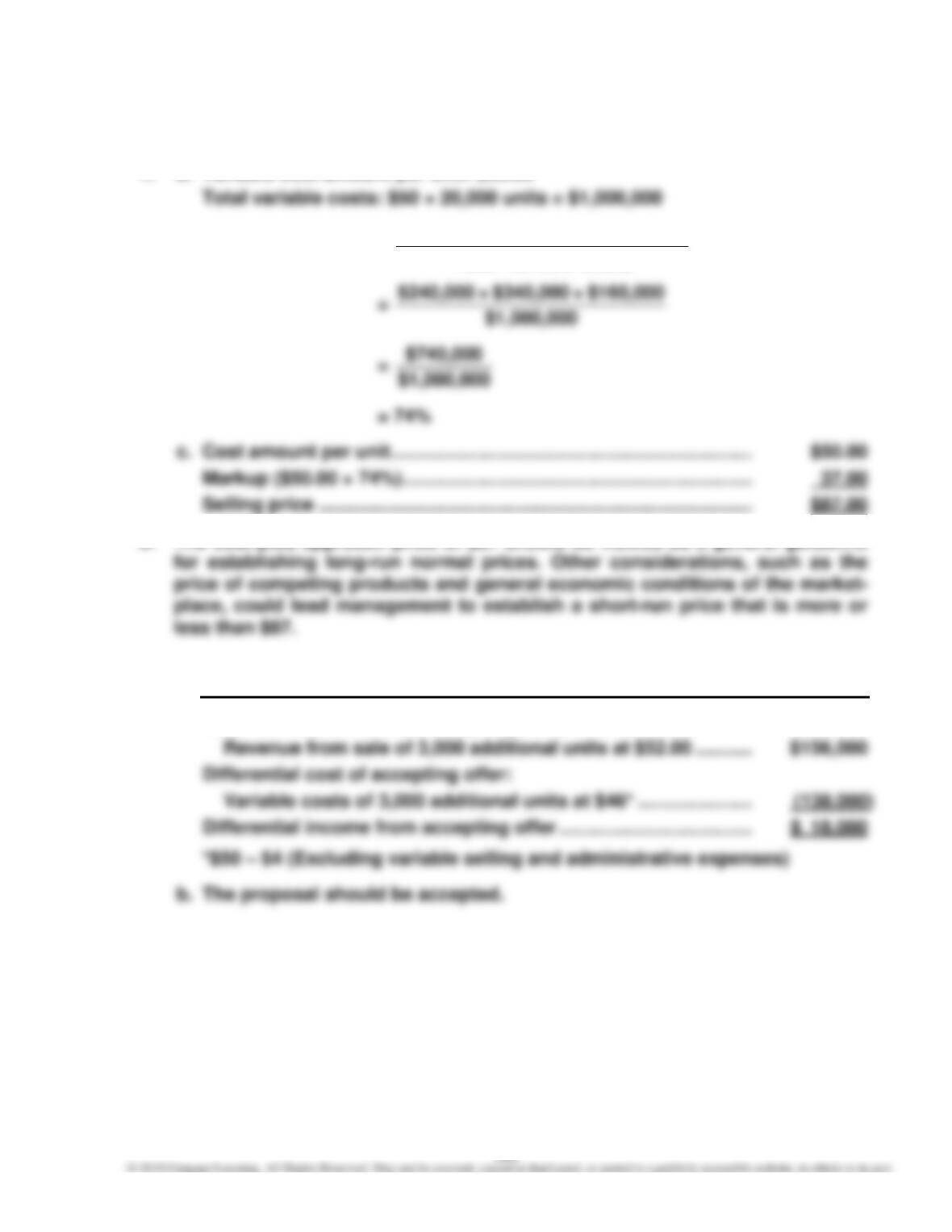

4. a. Variable cost amount per unit: $50.00

b. Markup Percentage = Costs VariableTotal

Costs Fixed Total +Profit Desired

5. The cost-plus approach price of $87 should be viewed as a general guideline

6. a. TWILIGHT LUMINA COMPANY

Proposal to Sell to Contech Inc.

Differential revenue from accepting offer:

386

METRIC-BASED ANALYSIS

MBA 12–1

Determine the contribution margin per furnace hour as follows:

Type A1 Type B3 Type E6

Revenue ……………………………………………… $ 400,000 $ 578,000 $ 300,000

Variable cost ………………………………………. (250,000) (380,000) (270,000)

MBA 12–2

a. Mirror Laminated Regular Total

Units produced …………………. 10,000 10,000 10,000

b. The Regular glass product is the most profitable in a bottleneck operation,

demonstrated as follows:

Mirror Laminated Regular

Unit contribution margin ……………………….. $ 18 $ 10 $ 5

387

MBA 12–3

2.

Selling Price Reduced Unit Variable

Unit Contribution

–

for Mirror Glass Cost for Mirror Glass

=

per Constraint for Furnace Hours for Mirror Glass

Regular Glass

3.

Selling Price Reduced Unit Variable

Unit Contribution

–

for Mirror Glass Cost for Mirror Glass

=

per Constraint for Reduced Furnace Hours for Mirror Glass

Regular Glass

388

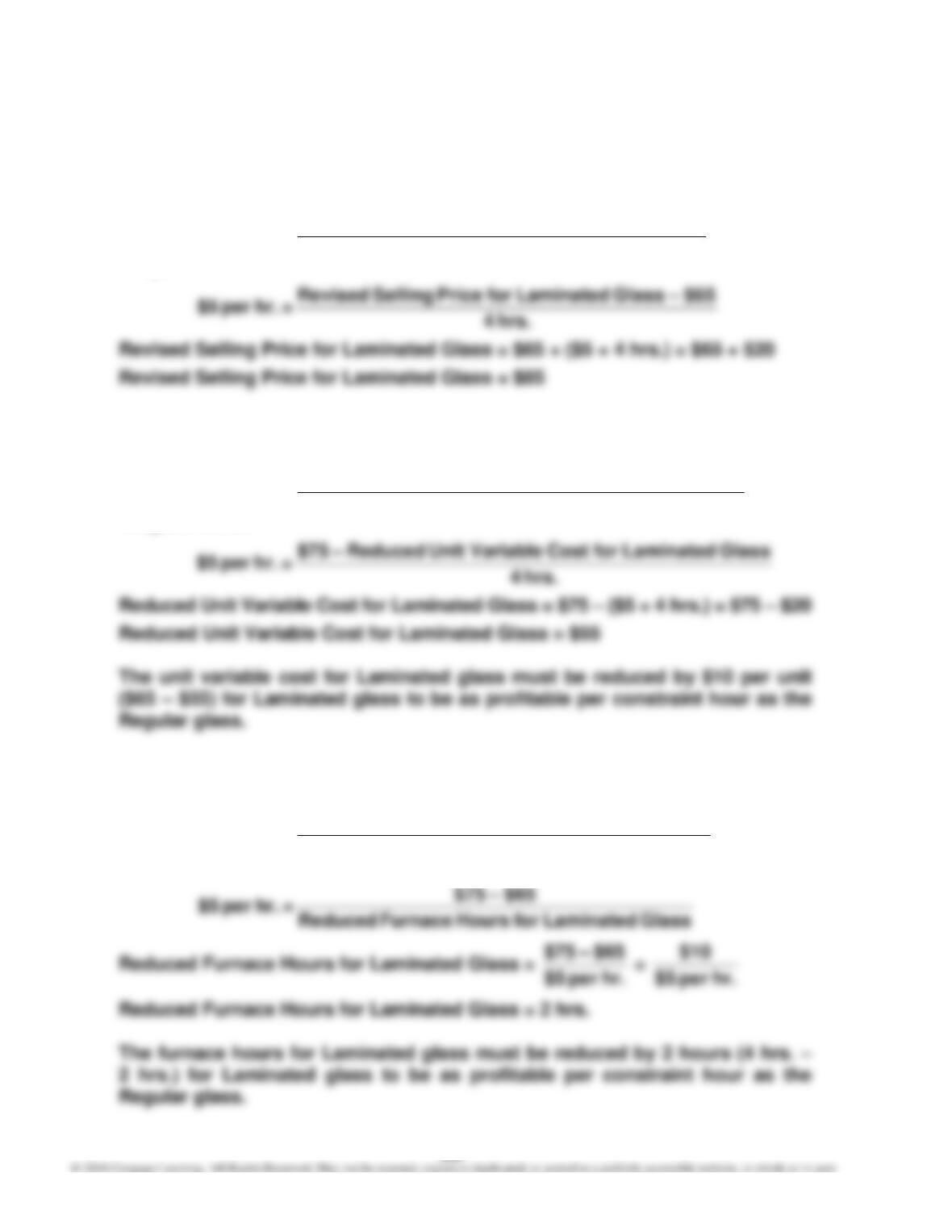

MBA 12–4

1.

Revised Selling Price Unit Variable Cost

Unit Contribution

–

for Laminated Glass for Laminated Glass

=

per Constraint for Furnace Hours for Laminated Glass

Regular Glass

2.

Selling Price Reduced Unit Variable

Unit Contribution

–

for Laminated Glass Cost for Laminated Glass

=

per Constraint for Furnace Hours for Laminated Glass

Regular Glass

3.

Selling Price Unit Variable Cost for

Unit Contribution

–

for Laminated Glass Laminated Glass

=

per Constraint for Reduced Furnace Hours for Laminated Glass

Regular Glass

389

MBA 12–5

1.

Ethylene Butane Ester

Selling price ……………………………………………. $ 400 $ 350 $ 250

Variable conversion cost per unit …………….. $(120)1 $(120)1 $ (80)2

2. The contribution margin per unit may give false signals when an organization

has production bottlenecks. Instead, Chavez Chemical Company should use

the contribution margin per bottleneck hour to determine relative product

profitability as follows:

Ethylene Butane Ester

Contribution margin per unit ……………………. $100 $ 100 $ 80

390

MBA 12–5, Concluded

3. One way to revise the pricing would be to increase the price to the point

where all three products produce profitability equal to the highest profit

product. This would be determined as follows:

Revised Price of Ethylene:

Revised Price of Butane:

Reactor per Margin

onContributi Unit

Butane of Butane of Cost VariableUnit _ Price Revised

CASES

Case 12–1

No, it would be unethical for Bev to attend the meeting. Such a meeting would be

Case 12–2

The contribution margin is $3 ($12 – $9) per dozen on the special order. Thus,

Coastal Sporting Goods’ manager can contribute to fixed costs by accepting the

order. However, there are some additional considerations the manager must con-

sider before accepting this order.

1. Have we ever done business overseas? Exports require additional adminis-

trative activities. Have these additional administrative costs been considered

4. Will the overseas customer want to do business in the future, or is this just a

5. Is there a possibility of another customer being willing to purchase the golf

392

Case 12–3

First, Marriott has excess capacity for this day. Thus, it should not be concerned

about using its capacity to accept business from the Priceline.com customer. The

Priceline.com customer is incremental revenue that will not crowd out other

393

Case 12–4

1. Dean believes that the fixed costs should be treated as a sunk cost and ig-

nored in the pricing decision. In essence, Dean is suggesting that the new

2. Target costing provides a different perspective to the pricing issue. Under

target costing, Redwood Computer Company should begin with the price the

394

Case 12–5

1. This activity is designed to have students access a number of products and

services on the Internet to see their commercial potential. Each of the listed

sites will provide product descriptions and pricing.

The list of costs in the products will not be determined at the Internet site but

must be assumed. Some examples include:

Delta Air Lines—Airline tickets Fixed or Variable?

Fuel ……………………………………………………………………… V

schedule.

Amazon.com—Books Fixed or Variable?

Cost of books (purchased for resale) …………………….. V

2. The product with the largest markup on variable cost is the airline ticket. The

portion of variable cost to total cost for an airline ticket will be much smaller