E8–16

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Common

Paid-In Capital in

Statement

Land*

=

Stock

+

Excess of Par—

Common Stock

E8–17

E8–18

E8–19

d.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Treasury

Paid-In Capital

Statement

Cash

=

Stock

+

from Treasury Stock

E8–20

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Cash Dividends

Retained

Statement

Payable

+

Earnings

June 1.

July 15. No entry required.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Cash Dividends

Statement

Cash

=

Payable

Aug. 14.

(1,200,000)

Financing

E8–21

Stockholders’

Assets Liabilities Equity

E8–22

E8–23

Stockholders’ Equity

Paid-in capital:

Common stock, $40 par

(100,000 shares authorized,

E8–24

Stockholders’ Equity

Paid-in capital:

Preferred 2% stock, $80 par

PROBLEMS

P8–1

1. Plan 1 Plan 2 Plan 3

Earnings before interest and income tax …… $1,000,000 $1,000,000 $1,000,000

Deduct interest on bonds …………………………. 0 0 (200,000)

2. Plan 1 Plan 2 Plan 3

3. The principal advantage of Plan 1 is it involves only the issuance of common

stock, which does not require a periodic interest payment or return of

P8–1, Concluded

Plan 2 provides an EPS of $0.16 when earnings before interest and income

P8–2

2.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Employee

FICA

Bond

Group

Statement

Income Tax

Payable

+

Tax

Payable

+

Deduction

Payable

+

Ins.

Payable

+

Salaries

Payable

+

Retained

Earnings

Oct. 4.

17,000

6,750

2,000

6,000

58,250*

(90,000)

Oct. 4.

Office salaries exp.

(20,000)

P8–2, Concluded

4.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

FICA Tax

SUTA

FUTA

Retained

Statement

Payable

+

Payable

+

Payable

+

Earnings

P8–3

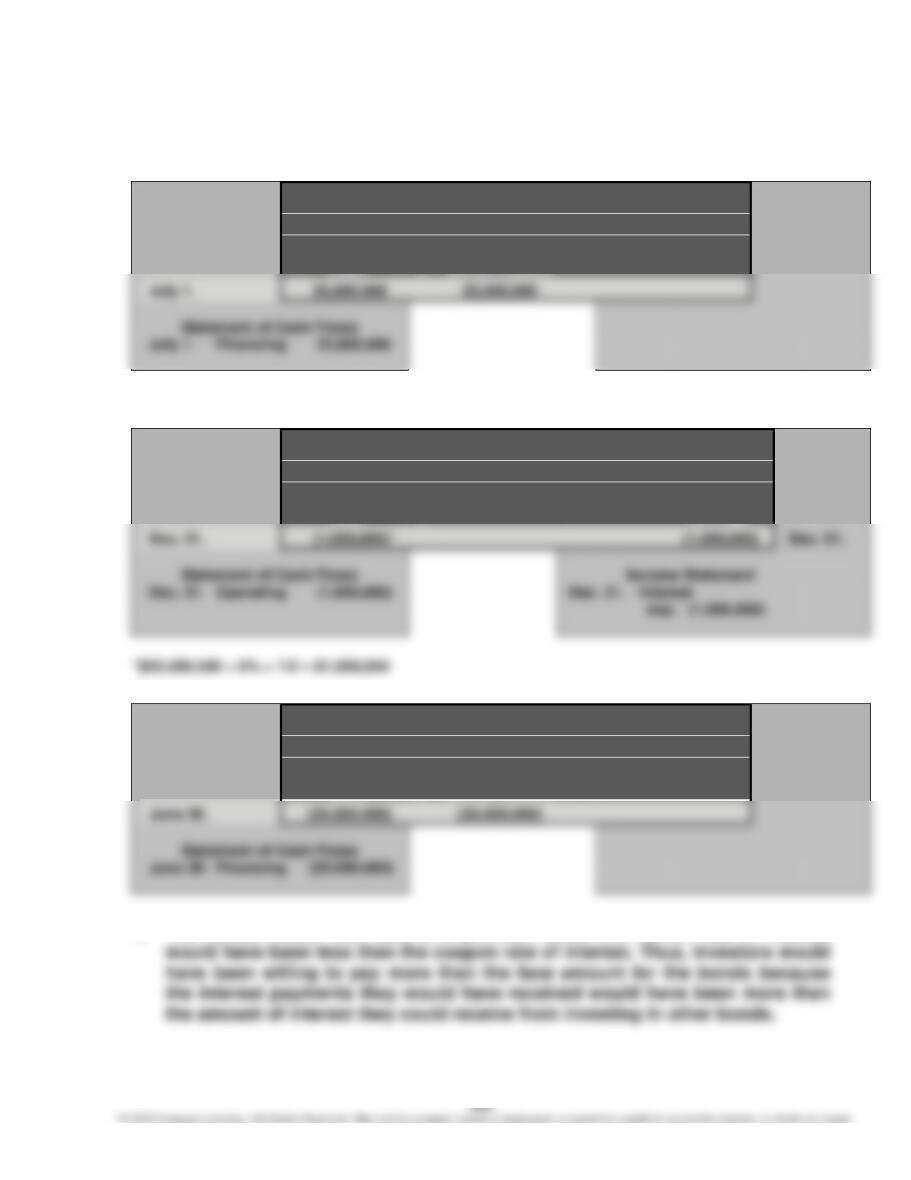

1.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Statement

Cash

=

Bonds Payable

2.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Retained

Statement

Cash

=

Earnings

3.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Statement

Cash

=

Bonds Payable

(25,000,000)

4. The bonds would have sold at a premium since the market rate of interest