297

CHAPTER 10

ACCOUNTING SYSTEMS FOR

MANUFACTURING OPERATIONS

CLASS DISCUSSION QUESTIONS

1. Managerial accounting differs from financial

accounting in the following ways:

(1) Financial accounting records and re-

(2) Financial accounting reports information

on a periodic basis (monthly, quarterly,

or yearly), while managerial accounting

2. For a company that produces desktop com-

3. Product cost information is used by manag-

c. Process cost systems accumulate costs

for each department or process within a

factory.

are issued to indicate release of the proper

amount of materials from the storeroom.

7. a. The clock card is a means of recording

the hours spent by employees in the

a. Summary of the materials requisitions

9. The use of a predetermined factory over-

head rate in job order cost accounting as-

298

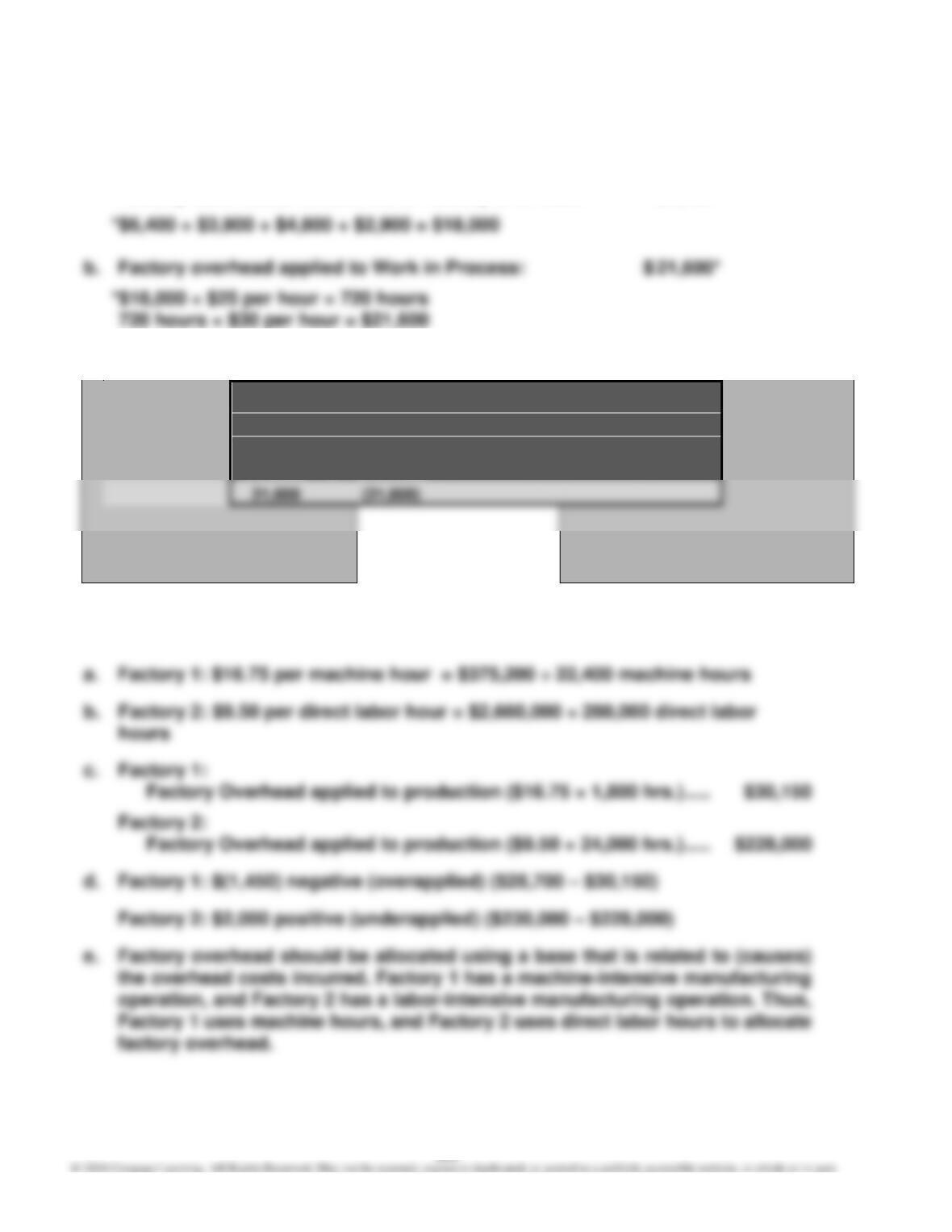

10. a. The predetermined factory overhead

rate is determined by dividing the bud-

11. a. (1) If the amount of factory overhead

12. The simplest satisfactory procedure for

14. Job order cost accumulation would be most

appropriate for professional service firms

head would be applied using a predeter-

mined overhead rate. The costs accumu-

cost, and instant availability.

b. JIT processing combines traditional

EXERCISES

E10–1

E10–2

a. Direct materials cost

f. Factory overhead cost

E10–3

E10–4

a. Period cost

j. Product cost

E10–5

a. period

e. direct materials

300

E10–6

E10–7

a.

Cost of goods sold:

b.

Direct materials cost:

c.

Direct labor cost:

301

E10–8

a.

RECEIVED ISSUED BALANCE

Receiving

Report

Number

Quantity

Unit

Price

Materials

Requi-

sition

Number

Quantity

Amount

Date

Quantity

Amount

Unit

Price

b. Ending wire cable balance:

302

E10–9

b.

Balance Sheet

Statement of Assets =Liabilities +Stockholders’ Equity Income

Cash Flows Work in Factory Statement

Materials + Process +Overhead

E10–10

a. Materials purchases ……………………………………………… $1,060,000*

c.

Polyester

Fabric Filling Lumber Glue

303

E10–11

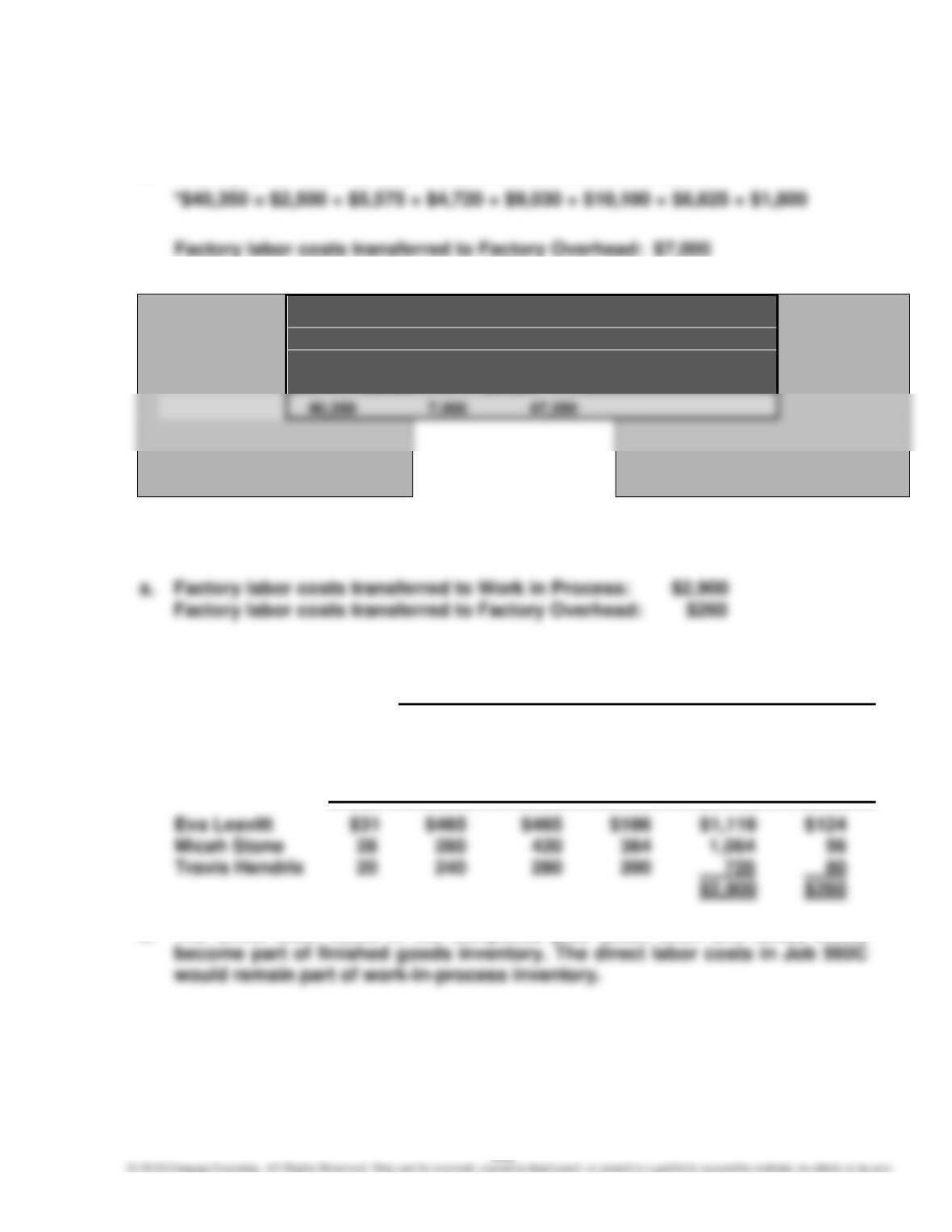

a. Factory labor costs transferred to Work in Process: $40,350*

b.

Balance Sheet

Statement of Assets =Liabilities +Stockholders’ Equity Income

Cash Flows Work in Factory Wages Statement

Process +Overhead =Payable

E10–12

Supporting Calculations:

Labor Costs (Hourly Rate × Hours)

Direct

Labor

Hourly (sum of Indirect

Rate Job 560A Job 560B Job 560C job costs) Labor

b. The direct labor costs in the completed jobs (Jobs 560A and 560B) would

304

E10–13

a. Factory labor costs transferred to Work in Process: $ 18,000*

Factory labor costs transferred to Factory Overhead: $1,750

c.

Balance Sheet

Statement of Assets =Liabilities +Stockholders’ Equity Income

Cash Flows Work in Factory Statement

Process + Overhead

E10–14

305

E10–15

The estimated shop overhead is determined as follows:

Shop and repair equipment depreciation ………………………………….. $ 91,000

E10–16

a. Estimated annual operating room overhead: $1,260,000

Estimated operating room activity base (number of operating room hours):

b. Shirlee Greer’s procedure: