Archives

Accounting Chapter 1 Which of the following characteristics does NOT pertain

Chapter 1 – Introduction to management accounting MULTIPLE CHOICE 1. ____ is devoted to providing information for external users. a. Management accounting b. Financial accounting c. Internal accounting d. Cost accounting 2. Management accounting and financial accounting differ in that […]

Accounting Chapter 10 However Todays Business Environment Few Products Services

Chapter 10 – Activity-based costing MULTIPLE CHOICE 1. Products might consume overhead in different proportions due to a. differences in product size. b. differences in setup times. c. differences in product complexity. d. all of the above. 2. The activity-based […]

Accounting Chapter 11 1 The use of unit-based activity drivers to assign

Chapter 11 – Pricing decisions and profitability analysis MULTIPLE CHOICE 1. The use of unit-based activity drivers to assign costs tends to a. overcost low-volume products. b. overcost high-volume products. c. undercost all products. d. overcost all products. 2. Riley, […]

Accounting Chapter 11 Identify The Activities That Belong Each Pool

PTS: 1 REF: 11.5 2. Discuss how volume-based unit-level analysis underestimates and/or overestimates the cost of products. 3. The most critical step in activity-based costing is identifying cost drivers. Explain this statement. ANS: The activity cost driver for a particular […]

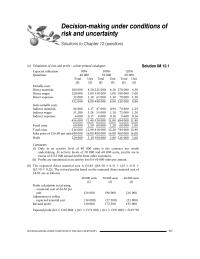

Accounting Chapter 12 The Possible Types Environment That May Occurans

Chapter 12 – Decision-making under conditions of risk and uncertainty MULTIPLE CHOICE 1. Which of the following represent states of nature? a. a potential set of outcomes expressed in monetary terms b. the most likely result that is going to […]

Accounting Chapter 13 Firm Considering Project With Annual Cash

Chapter 13 – Capital investment decisions: appraisal methods MULTIPLE CHOICE 1. Projects that, if accepted, preclude the acceptance of competing projects are a. priority projects. b. mutually exclusive projects. c. independent projects. d. equity projects. 2. ____ are capital budgeting […]

Accounting Chapter 13 The System Has Positive Net Present Value

60. Which of the following capital investment models would be preferred when choosing among mutually exclusive alternatives? a. payback period b. accounting rate of return c. IRR d. NPV ANS: D PTS: 1 REF: 13.8 61. Five mutually exclusive projects […]

Accounting Chapter 14 Tax savings from tax allowable depreciation

Chapter 14 – Capital investment decisions: the impact of capital rationing, taxation, inflation and risk MULTIPLE CHOICE 1. ____ is the process of altering key variables to assess the effect on the original outcome. a. Alteration analysis b. Experimentation c. […]

Accounting Chapter 15 One fourth of the purchases are paid for in

c. 82,000 units d. 42,000 units 64. Gerald Company manufactures books. Manufacturing a book takes 10 units of A1 and 1 unit of A2. Scheduled production of books for the next two months is 1,000 and 1,200 units, respectively. Beginning […]

Accounting Chapter 15 The Following Forecasted Sales Pertain Reject

Chapter 15 – The budgeting process MULTIPLE CHOICE 1. Which of the following is NOT a criticism of the traditional master budget? a. results oriented b. Interdependencies are recognized. c. static d. department oriented 2. If a department plans forward […]

Accounting Chapter 16 Controllable costs are those that a manager

42. Controllable costs are those that a manager a. has no authority over. b. cannot avoid. c. does not participate in authorizing. d. can influence through decision making. ANS: D PTS: 1 REF: 16.9 43. Which budget should be used […]

Accounting Chapter 16 Which The Following Not Potential Disadvantage

Chapter 16 – Management control systems MULTIPLE CHOICE 1. Which of the following is not an objective of responsibility accounting? a. to redesign processes to be more effective b. to align individual and organizational goals c. to influence behaviour d. […]

Accounting Chapter 17 April The Actual Quantity Materials Used Must

Chapter 17 – Standard costing and variance analysis 1 MULTIPLE CHOICE 1. To determine the unit standard cost for a particular input, a company must decide how much a. input should be used per unit of output and how much […]

Accounting Chapter 17 Orient’s materials price variance would be

54. Fixed overhead was budgeted at £500,000 and 25,000 direct labour hours were budgeted. If the fixed overhead volume variance was £12,000 favourable and the fixed overhead spending variance was £16,000 unfavourable, fixed overhead applied must be a. £516,000. b. […]

Accounting Chapter 18 Variable inspection costs consist of materials

Chapter 18 – Standard costing and variance analysis 2: Further aspects MULTIPLE CHOICE Figure 18-1 Froelech Company has developed capacity standards. Information is as follows: Standard cost of the activity capacity acquired £150,000 Standard cost of the activity capacity used […]

Accounting Chapter 19 Types of responsibility centres include

Chapter 19 – Divisional financial performance measures MULTIPLE CHOICE 1. Types of responsibility centres include all of the following EXCEPT a. profit centres. b. contribution centres. c. investment centres. d. cost centres. 2. The Marketing Department is most likely considered […]

Accounting Chapter 2 A supervisor’s salary of £2,000 per month is an example

Chapter 2 – An introduction to cost terms and concepts MULTIPLE CHOICE 1. A supervisor’s salary of £2,000 per month is an example of a a. fixed cost. b. variable cost. c. step cost. d. mixed cost. 2. Fixed cost […]

Accounting Chapter 20 A transfer pricing system should satisfy which

Chapter 20 – Transfer pricing in divisionalized companies MULTIPLE CHOICE 1. Transfer pricing is used when: a. multiple cost centres are conducting business within the company. b. a decentralized company has profit centres or investment centres. c. the return on […]

Accounting Chapter 21 How does activity analysis help reduce costs

2. What is kaizen costing? How does activity analysis help reduce costs? 3. For each following activity, determine the amount of value-added and nonvalue-added costs. a. The company keeps 7 days of materials inventory on hand to avoid shutdowns due […]

Accounting Chapter 21 Kanban Specifies a How Much Should Produced Replace

Chapter 21 – Cost Management MULTIPLE CHOICE 1. The major source of information for the activity cost management system is a. cost driver analysis. b. an activity- based costing system. c. a performance measurement system. d. product information. 2. Which […]

Accounting Chapter 22 The Advantage Balanced Scorecard Approach That Can

Chapter 22 – Strategic management accounting MULTIPLE CHOICE 1. An example of a lag measure is a. hours of employee training. b. customer profitability. c. employee capabilities. d. none of the above. 2. The five key core objectives of the […]

Accounting Chapter 23 Koch Sa Believes Their Electricity Costs

60. In a simple least-squares regression where X refers to the number of sales calls made by a sales department and Y refers to the monthly total cost of the sales department, the value of X in the regression output […]

Accounting Chapter 23 Weaknesses of the high-low method include all of

Chapter 23 – Cost estimation and cost behaviour MULTIPLE CHOICE 1. Which of the following decision-making tools would NOT be useful in determining the slope and intercept of a mixed cost? a. linear programming b. least-squares method c. high-low method […]

Accounting Chapter 24 Quantitative models for the planning and control of

Chapter 24 – Quantitative models for the planning and control of stocks MULTIPLE CHOICE 1. If inventory is purchased from an outside supplier, the inventory-related costs are a. ordering and carrying costs. b. setup and carrying costs. c. ordering and […]

Accounting Chapter 25 The application of linear programming to management

Chapter 25 – The application of linear programming to management accounting MULTIPLE CHOICE 1. A linear programming problem has an objective function of 10X + 12Y. If the optimal solution provided by the model is to produce and sell 400 […]

Accounting Chapter 3 Manufacturing Has Four Categories Overhead The Four

Maintenance £360,000 Inspection 750,000 The plant currently applies overhead using direct labour hours and expected capacity of 100,000 direct labour hours. The following data has been assembled for use in developing a bid for a proposed job. Bid prices are […]

Accounting Chapter 3 What system would a manufacturer of unique special

Chapter 3 – Cost assignment MULTIPLE CHOICE Figure 3-1 The Xiang plant has two categories of overhead: maintenance and inspection. Costs expected for these categories for the coming year are as follows: Maintenance £50,000 Inspection 75,000 The plant currently applies […]

Accounting Chapter 4 Company Produces Calculators Assembly Line Singlestep

Chapter 4 – Accounting entries for a job costing system MULTIPLE CHOICE 1. ____ is the recognition and recording of costs. a. Cost accumulation b. Cost measurement c. Cost assignment d. Job order costing 2. Assume the following information for […]

Accounting Chapter 5 Equivalent Units Production For Conversion Costs Using

Chapter 5 – Process costing MULTIPLE CHOICE 1. The sum of direct labour and factory overhead is referred to as a. period costs. b. conversion costs. c. prime costs. d. direct product costs. 2. Conversion costs do NOT include a. […]

Accounting Chapter 5 Unit cost of materials for a department using

39. Refer to Figure 5-7. Units started and completed in Corn Corporation’s second department during June would be a. 48,000. b. 37,000. c. 29,000. d. 55,000. Figure 5-9 The following information is available for Department Z for the month of […]

Accounting Chapter 6 Additional processing costs of specific products

Profit increases £28,000 43. The decision of whether or NOT to process joint products beyond their split-off point is a. based on the total cost of the finished product including joint costs. b. based on joint costs only. c. based […]

Accounting Chapter 6 which are produced simultaneously by the same

Chapter 6 – Joint and by-product costing MULTIPLE CHOICE 1. ____ are products with substantial value which are produced simultaneously by the same process up to a split-off point. a. By-products b. Joint products c. Minor products d. Both a […]

Accounting Chapter 7 Compare and contrast absorption and variable

SHORT ANSWER 1. Compare and contrast absorption and variable costing. 2. Since fixed product costs are eventually recorded as expenses under both variable and absorption costing by the time the inventory is sold, why does it matter whether fixed overhead […]

Accounting Chapter 7 Income effects of alternative cost accumulation

Chapter 7 – Income effects of alternative cost accumulation systems MULTIPLE CHOICE 1. The efficient level of activity performance is called a. activity capacity. b. practical capacity. c. unused capacity. d. acquired capacity. 2. Which of the following costs would […]

Accounting Chapter 8 The vertical Axis Represents Costs And The Horizontal

c. Linear analysis likely overstates total costs at high activity levels. d. Linear analysis of high activity levels fails to capture the fact that total fixed costs decrease as more units are produced. 49. Information about two products is as […]

Accounting Chapter 8 Total contribution margin is calculated by subtracting

Chapter 8 – Cost-volume-profit analysis MULTIPLE CHOICE 1. Total contribution margin is calculated by subtracting a. cost of goods sold from total revenues. b. fixed costs from total revenues. c. total manufacturing costs from total revenues. d. total variable costs […]

Accounting Chapter 9 in what sequence should orders be filled

The company has the capacity to produce 80,000 units. The product regularly sells for £90. A wholesaler has offered to pay £75 each for 2,000 units. If Bridge’s special order is accepted, the effect on operating income would be a […]

Accounting Chapter 9 Measuring relevant costs and revenues for decision

Chapter 9 – Measuring relevant costs and revenues for decision-making MULTIPLE CHOICE 1. Tactical decision-making relies a. only on relevant cost information. b. on qualitative factors. c. on relevant costs as well as other qualitative factors. d. on neither relevant […]

Chapter 10 For a particular contract estimate the number of day

Chapter 11 Organizations may decide not to use or to abandon

Chapter 12 It would be preferable to construct a probability distribution

Chapter 13 A discussion of why the accounting rate of return is widely

Chapter 14 The implication of this is that it will be necessary

Chapter 15 So there is a strong possibility that managers might

Chapter 16 A large proportion of non-manufacturing costs are of a

Chapter 17 It reports only an expenditure variance for fixed overheads

Chapter 18 Actual costs for each cost element should be reported

Chapter 19 The main behavioral and control consequences which may arise

Chapter 2 The fixed production overhead rate per unit of output

Chapter 20 Where there is a shortage of supply of the raw materials

Chapter 21 Much less emphasis will be placed on detailed inventory

Chapter 22 which adopts a balanced scorecard perspective for measuring

Chapter 23 An insufficient number of observations is used to derive

Chapter 24 The model assumes that annual demand can be predicted

Chapter 25 The optimal production programme is found using linear

Chapter 3 Different cost classification might result in different

Chapter 4 leaving costs associated with completing the appropriate

Chapter 5 It would appear that a job costing system provides more

Chapter 6 The answer should stress that joint cost apportionment should not

Chapter 7 For cost control purposes flexible budgets should be used

Chapter 8 Both models are based on single value estimates of total