2. What is kaizen costing? How does activity analysis help reduce costs?

3. For each following activity, determine the amount of value-added and nonvalue-added costs.

a.

The company keeps 7 days of materials inventory on hand to avoid shutdowns due to

materials shortages. Carrying costs are £50,000 per day.

b.

A time-and-motion study revealed that it should take 10 minutes to produce a product that

now takes 50 minutes to produce. labour is £18 per hour.

c.

Warranty work costs the firm £500,000 per year. Warranty costs for the industry average

£100,000 per year.

Value-added costs = £0

Nonvalue-added costs = (£50,000 7) = £350,000

Value-added costs = (£18 10/50) = £3.60

Value-added costs = £0

Nonvalue-added costs = £500,000

4. Clark, SA., sells one of its products for £150 each. Sales volume averages 800 units per year. Recently,

its main competitor reduced the price of its product to £130. Clark expects sales to drop dramatically

unless it matches the competitor’s price. In addition, the current profit per unit must be maintained.

Information about the product (for production of 800) is as follows:

SQ

AQ

Actual Cost

Materials (kgs)

14,400

15,000

£30,000

Labour (hours)

2,000

2,400

18,000

Setups (hours)

0

1,400

8,000

Material handling (moves)

0

600

4,000

Warranties (number repaired)

0

400

20,000

Required:

a.

Calculate the target cost for maintaining current market share and profitability.

b.

Calculate the nonvalue-added cost per unit.

c.

If nonvalue-added costs can be reduced to zero, can the target cost be achieved?

1.

2.

Activity selection

3.

Activity reduction

4.

Activity sharing

5. Park, SA., sells one of its products for £40 each. Sales volume averages 2,000 units per year. Recently,

its main competitor reduced the price of its product to £28. Park expects sales to drop dramatically

unless it matches the competitor’s price. In addition, the current profit per unit must be maintained.

Information about the product (for production of 2,000) is as follows:

SQ

AQ

Actual Cost

Materials (kgs)

4,900

5,000

£20,000

Labour (hours)

1,200

1,250

10,000

Setups (hours)

0

200

6,000

Material handling (moves)

0

350

2,000

Warranties (number repaired)

0

250

10,000

Required:

a.

Calculate the target cost for maintaining current market share and profitability.

b.

Calculate the nonvalue-added cost per unit.

c.

If nonvalue-added costs can be reduced to zero, can the target cost be achieved?

Current selling price

Less: Current cost (£48,000/2,000)

Current profit per unit

Current selling price

Less: Current cost (£80,000/800)

Current profit per unit

Selling price to maintain market share

Less: Desired profit per unit

Target cost

b.

Materials:

£30,000/15,000 = £2 per kg

(15,000 – 14,400) £2

Labour:

(2,400 – 2,000) £7.50

Setups

Material handling

Warranties

Nonvalue-added costs

Nonvalue-added cost per unit (£36,200/800 units)

6. Describe how the activity-based management model combines the process and costing views. What

are the steps involved in each? What are the objectives of the activity-based management system?

7. Craig, SA., sells one of its products for £500 each. Sales volume averages 1,000 units per year.

Recently, its main competitor priced their competing product at 10 per cent below Craig’s price. Craig

expects its sales to drop dramatically unless it matches the competitor’s price. Despite the anticipated

price reduction, Craig would like to maintain its current profit per unit.

Information regarding the inputs required to produce 1,000 units of product is as follows:

SQ

AQ

Actual Cost

Materials (kgs)

7,800

8,000

£160,000

Labour (hours)

600

720

108,000

Setups (hours)

-0-

600

34,000

Selling price to maintain market share

Target cost

b.

Materials:

(5,000 – 4,900) £4

£10,000/1,250 = £8 per hour

(1,250 – 1,200) £8

Material handling

Warranties

Material handling (moves)

-0-

300

58,000

Warranties (number repaired)

-0-

200

60,000

Required:

a.

Calculate the target cost for maintaining current market share and profitability.

b.

Calculate the nonvalue-added cost per unit.

c.

If nonvalue-added costs can be reduced to zero, can the target cost be achieved?

8. For each activity listed below, determine the amount of value-added and nonvalue-added costs.

a.

The company keeps seven days of raw materials inventory on hand to avoid shutdowns due

to raw materials shortages. Carrying costs are £25,000 per day.

Value-added costs:

Nonvalue-added costs:

b.

A time and motion study revealed that it should take 5 minutes to produce a product that

now takes 50 minutes to produce. Labour is £24 per hour.

Value-added costs:

Nonvalue-added costs:

c.

Warranty work costs the firm £250,000 per year. Warranty costs for the industry average

£50,000 per year.

£370

Current selling price

Current cost (£420,000/1,000 units)

Current profit per unit

Desired profit per unit

Target cost

b.

£174.00 per unit

Materials

(£160,000/8,000 kgs) = £20 per kg

(8,000 kgs – 7,800 kgs) £20

Labour

(£108,000/720 hours) = £150 per hour

(720 hours – 600 hours) £150

Setups

Material handling

Warranties

Nonvalue-added costs

Nonvalue-added cost per unit (£174,000/1,000)

c.

Yes. If nonvalue-added costs can be reduced to zero, the cost per unit would be £246 (£420

– £174), which is below the target cost of £370.

Value-added costs:

Nonvalue-added costs:

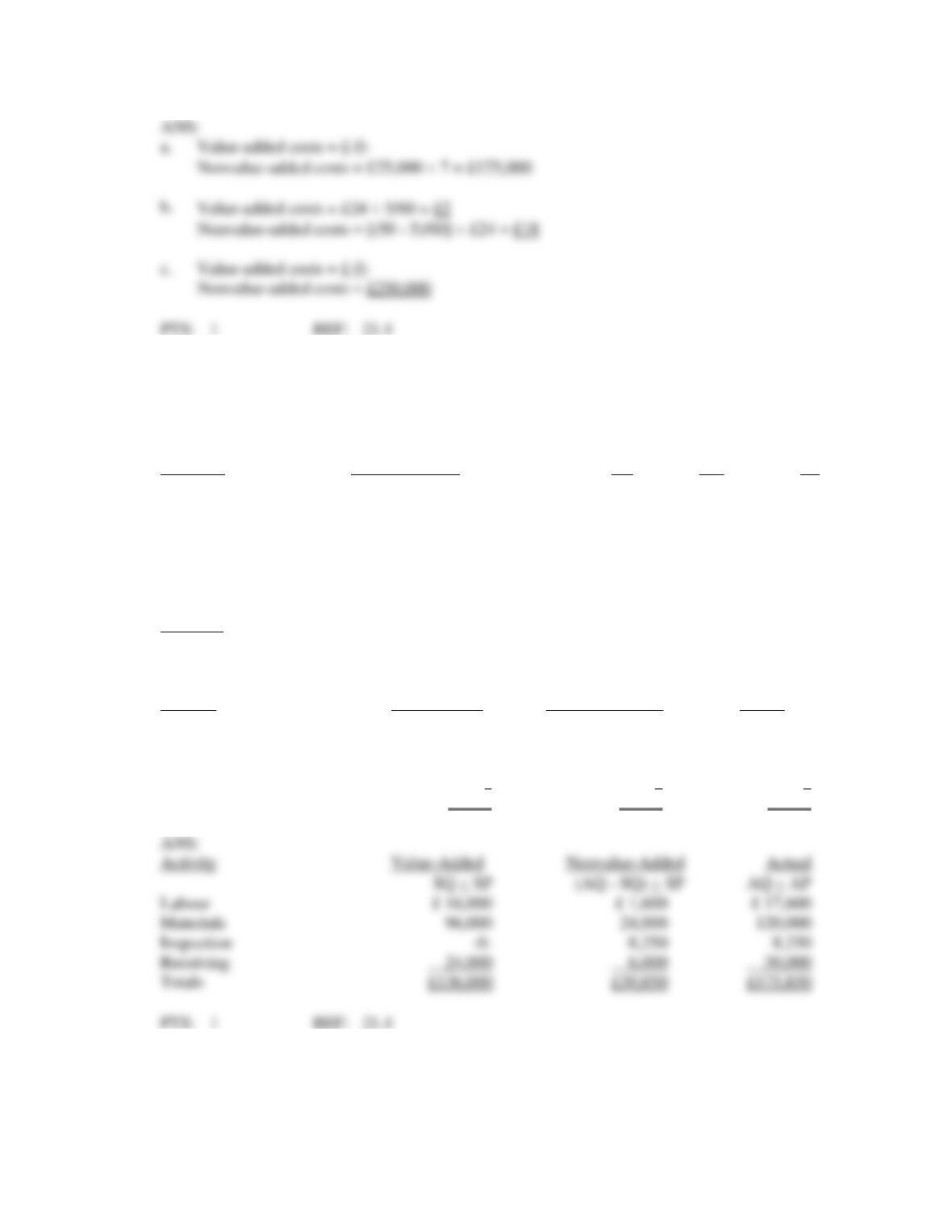

9. Grayson, SA., has developed ideal standards for four activities: labour, materials, inspection, and

receiving.

Information is as follows:

Activity

Activity Driver

SQ

AQ

SP

Labour

Hours

1,000

1,100

£ 16

Materials

kgs

4,000

5,000

£ 24

Inspection

Inspection hours

-0-

750

£ 11

Receiving

Orders

60

75

£400

The actual prices paid per unit of each activity driver were equal to the standard prices.

Required:

Complete the following cost report:

Activity

Value-Added

Nonvalue-Added

Actual

Labour

£ ?

£ ?

£ ?

Materials

?

?

?

Inspection

?

?

?

Receiving

_____?

_____?

_____?

Totals

£ ?

£ ?

£ ?

Activity

Value-Added

Materials

24,000

Inspection

8,250

Receiving

Totals

Value-added costs = £-0-

Nonvalue-added costs = £25,000 7 = £175,000

Value-added costs = £24 5/60 = £2

Nonvalue-added costs = [(50 – 5)/60] £24 = £18

Value-added costs = £-0-

Nonvalue-added costs = £250,000

10. Palms, SA., sells one of its products for £80 each. Sales volume averages 2,000 units per year.

Recently, its main competitor reduced the price of its product to £56. Palms expects its sales to drop

dramatically unless it matches the competitor’s price. In addition, the current profit per unit must be

maintained.

Information about the product (for production of 2,000) is as follows:

SQ

AQ

Actual Cost

Materials (kgs)

9,800

10,000

£40,000

Labour (hours)

2,400

2,500

20,000

Setups (hours)

-0-

400

12,000

Material handling (moves)

-0-

700

4,000

Warranties (number repaired)

-0-

500

20,000

Required:

a.

Calculate the target cost for maintaining current market share and profitability.

b.

Calculate the nonvalue-added cost per unit.

c.

If nonvalue-added costs can be reduced to zero, can the target cost be achieved?

11. Answer the following questions pertaining to just-in–time inventory management:

£24

Current selling price

Current cost (£96,000/2,000 units)

Current profit per unit

Selling price to maintain market share

Desired profit per unit

Target cost

b.

£18.80 per unit

Nonvalue-Added Costs

Materials

(£40,000/10,000 kgs) = £4 per kg

(10,000 kgs – 9,800 kgs) £4

Labour

(£20,000/2,500 hours) = £8 per hour

(2,500 hours – 2,400 hours) £8

Setups

Material handling

Warranties

Nonvalue-added costs

Nonvalue-added cost per unit (£37,600/2,000)

– £18.80), which is above the target cost of £24.

a.

Identify key elements of the JIT philosophy.

b.

What elements of the JIT approach contribute to reducing materials inventory?

c.

Why do proponents of JIT believe inventory is an enemy?

12. The following reasons have been offered for holding inventories:

1.

To balance ordering or setup costs and carrying costs

2.

To satisfy customer demand (e.g., meet delivery dates)

3.

To avoid shutting down manufacturing facilities because of

(a) machine failure

(b) defective parts

(c) unavailable parts

4.

Unreliable production processes

5.

To take advantage of discounts

6.

To hedge against future price increases

Required:

a.

Explain how the JIT approach responds to each of these reasons and, consequently, argues for

insignificant levels of inventories.

b.

The theory of constraints (TOC) criticizes the JIT approach to inventory management, arguing

that it fails to protect throughput. Explain what this means and describe how TOC addresses

this issue.

a.

Key elements of the JIT philosophy include inventory reduction, reduced production times,

13. Using the abbreviations listed below, indicate for each of the costs whether the cost should be

classified as:

P

=

Prevention

D

=

Detection

I

=

Internal Failure

E

=

External Failure

N

=

None of the above

1.

Cleaning up contaminated soil

2.

Designing processes

3.

Recycling scrap

4.

Auditing environmental activities

5.

Testing for contamination

6.

Losing a lake for recreational use

7.

Measuring contamination levels

8.

Recycling products

9.

Maintaining pollution equipment

10.

Evaluating and selecting suppliers

1.

Cleaning up contaminated soil

P

2.

Designing processes

I

3.

Recycling scrap

D

4.

Auditing environmental activities

D

5.

Testing for contamination

6.

Losing a lake for recreational use

D

7.

Measuring contamination levels

defects), and building the right kind of relationship with suppliers.

6.

JIT emphasizes long-term contracts that stipulate prices and acceptable quality levels.

14. Using the abbreviations listed below, indicate for each of the costs whether the cost should be

classified as:

P

=

Prevention

D

=

Detection

I

=

Internal Failure

E

=

External Failure

N

=

None of the above

1.

Inspecting products and processes

2.

Verifying supplier environmental performance

3.

Testing for contamination

4.

Obtaining ISO 14001 certification

5.

Carrying out environmental studies

6.

Operating pollution control equipment

7.

Cleaning up a polluted lake

8.

Recycling scrap

9.

Recycling products

10.

Cleaning up oil spills

ANS:

D

1.

Inspecting products and processes

2.

Verifying supplier environmental performance

D

3.

Testing for contamination

P

4.

Obtaining ISO 14001 certification

5.

Carrying out environmental studies

I

6.

Operating pollution control equipment

E

7.

Cleaning up a polluted lake

I

8.

Recycling scrap

P

9.

Recycling products

Cleaning up oil spills

15. At the beginning of the year, Paris, SA., initiated an environmental cost reduction program. To help

assess the impact of the environmental cost reduction improvement program, the following data was

collected for the current and preceding year:

Preceding Year

Current Year

Operating costs

£4,000,000

£4,000,000

Designing products

18,000

20,000

Auditing environmental activities

40,000

64,000

Recycling scrap

200,000

180,000

Restoring land to natural state

360,000

320,000

Operating pollution control equipment

250,000

240,000

Testing for contamination

80,000

80,000

I

9.

Maintaining pollution equipment

P

10.

Evaluating and selecting suppliers

Required:

a.

Compute each category of environmental quality costs as a percentage of operating costs for

each year.

Prevention costs

Detection costs

Internal failure costs

External failure costs

b.

How much has profit increased as a result of the environmental cost reduction improvements?

16. At the beginning of the year, Sherwood Company initiated a quality improvement program. The

program was successful in reducing scrap and rework costs. To help assess the impact of the quality

improvement program, Sherwood’s managers collected the following data for the current and

preceding year:

Preceding Year

Current Year

Sales

£20,000,000

£20,000,000

Quality training

40,000

65,000

Scrap

400,000

350,000

Materials inspection

80,000

70,000

Rework

550,000

500,000

Product inspection

100,000

150,000

Product warranty

700,000

600,000

Required:

a.

Compute prevention costs, appraisal costs, internal failure costs, and external failure costs as a

percentage of sales for the preceding year and the current year.

b.

How much has profit increased as a result of quality improvements?

c.

If quality costs can be reduced even further to 2.5 per cent of sales, how much additional profit

would result?

Prevention costs:

£40,000/£20,000,000

£65,000/£20,000,000

Appraisal costs:

(£80,000 + £100,000)/£20,000,000

(£70,000 + £150,000)/£20,000,000

Prevention costs

Detection costs

Internal failure costs

b.

£44,000

£948,000 – £904,000

17. At the end of the current year, Sugarbaker Ltd.collected the following data about its quality program:

Sales (50,000 £40)

£2,000,000

Training program

24,000

Rework

80,000

Scrap

60,000

Warranty repairs

80,000

Complaints

40,000

Inspection labour

50,000

Test labour

60,000

Supplier evaluation

6,000

Required:

Prepare a quality cost report by quality cost category.

Prevention costs:

Training program

Appraisal costs:

Inspection labour

Test labour

Supplier evaluation

Total appraisal costs

Internal failure costs:

Rework

Scrap

Total internal failure costs

External failure costs:

Warranty repairs

(£400,000 + £550,000)/£20,000,000

(£350,000 + £500,000)/£20,000,000

External failure costs:

£700,000/£20,000,000

£600,000/£20,000,000

b.

£135,000 £1,870,000 – £1,735,000

£1,235,000 £1,735,000 -(2.5% £20,000,000)

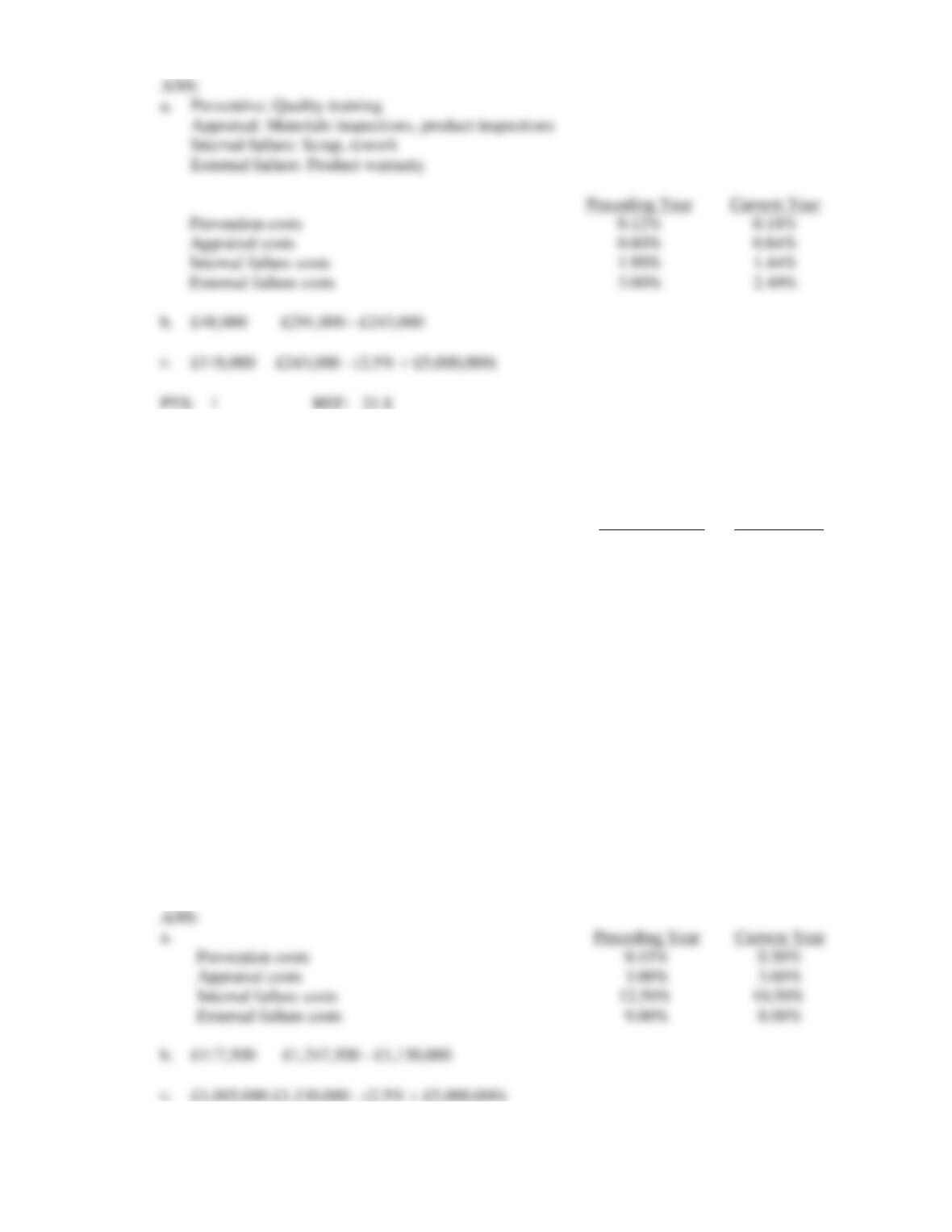

18. At the beginning of the year, Bing Company initiated a quality improvement program. The program

was successful in reducing scrap and rework costs. To help assess the impact of the quality

improvement program, Bing’s managers collected the following data for the current and preceding

year:

Preceding Year

Current Year

Sales

£10,000,000

£10,000,000

Quality training

45,000

50,000

Materials inspection

100,000

140,000

Scrap

500,000

450,000

Product warranty

900,000

800,000

Rework

750,000

600,000

Product inspection

200,000

220,000

Required:

a.

Compute prevention costs, appraisal costs, internal failure costs, and external failure costs as a

percentage of sales for the preceding year and the current year.

b.

How much has profit increased as a result of quality improvements?

c.

If quality costs can be reduced even further to 2.5 per cent of sales, how much additional profit

would result?

Prevention costs:

£45,000/£10,000,000

£50,000/£10,000,000

Appraisal costs:

(£100,000 + £200,000)/£10,000,000

(£140,000 + £220,000)/£10,000,000

Internal failure costs:

(£500,000 + £750,000)/£10,000,000

(£450,000 + £600,000)/£10,000,000

External failure costs:

£900,000/£10,000,000

£800,000/£10,000,000

b.

£235,000 £2,495,000 – £2,260,000

£2,010,000 £2,260,000 – (2.5% £10,000,000)

19. Using the abbreviations listed below, indicate for each of the costs whether the cost should be

classified as:

P

=

Prevention

A

=

Appraisal

Total external failure costs

Total quality costs

I

=

Internal Failure

E

=

External Failure

N

=

None of the above

1.

Cost of recalling defective products

2.

Design reviews

3.

Downtime due to defects

4.

Field testing

5.

Inspection of work in process

6.

Lost sales due to poor product performance

7.

Process acceptance

8.

Quality training programs

9.

Scrap

10.

Supplier evaluations

20. At the beginning of the year, Randy Company initiated a quality improvement program. The program

was successful in reducing scrap and rework costs. To help assess the impact of the quality

improvement program, the following data were collected for the current and preceding years:

Preceding Year

Current Year

Sales

£5,000,000

£5,000,000

Quality training

6,000

9,000

Material inspections

15,000

12,000

Scrap

80,000

60,000

Rework

15,000

12,000

Product inspection

25,000

30,000

Product warranty

150,000

120,000

Required:

a.

Compute each category of quality costs as a percentage of sales for each year.

Prevention costs

Appraisal costs

Internal failure costs

External failure costs

b.

How much has profit increased as a result of quality improvements?

c.

If quality costs can be reduced to 2.5 per cent of sales, how much additional profit would

result?

P

2.

Design reviews

I

3.

Downtime due to defects

A

4.

Field testing

A

5.

Inspection of work in process

E

6.

Lost sales due to poor product performance

A

7.

Process acceptance

P

8.

Quality training programs

I

9.

Scrap

P

10.

Supplier evaluations

21. At the beginning of the year, Ball Company initiated a quality improvement program. The program

was successful in reducing scrap and rework costs. To help assess the impact of the quality

improvement program, the following data were collected for the current and preceding years:

Preceding Year

Current Year

Sales

£5,000,000

£5,000,000

Quality training

22,500

25,000

Material inspections

50,000

80,000

Scrap

250,000

225,000

Product warranty

450,000

400,000

Rework

375,000

300,000

Product inspection

100,000

100,000

Required:

a.

Compute each category of quality costs as a percentage of sales for each year.

Prevention costs

Appraisal costs

Internal failure costs

External failure costs

b.

How much has profit increased as a result of quality improvements?

c.

If quality costs can be reduced to 2.5 per cent of sales, how much additional profit would

result?

Prevention costs

Appraisal costs

Internal failure costs

External failure costs

b.

£117,500 £1,247,500 – £1,130,000

£1,005,000 £1,130,000 – (2.5% £5,000,000)

a.

Preventive: Quality training

Appraisal: Materials inspections, product inspections

Internal failure: Scrap, rework

External failure: Product warranty

Prevention costs

Appraisal costs

Internal failure costs

External failure costs

b.

£48,000 £291,000 – £243,000

£118,000 £243,000 – (2.5% £5,000,000)

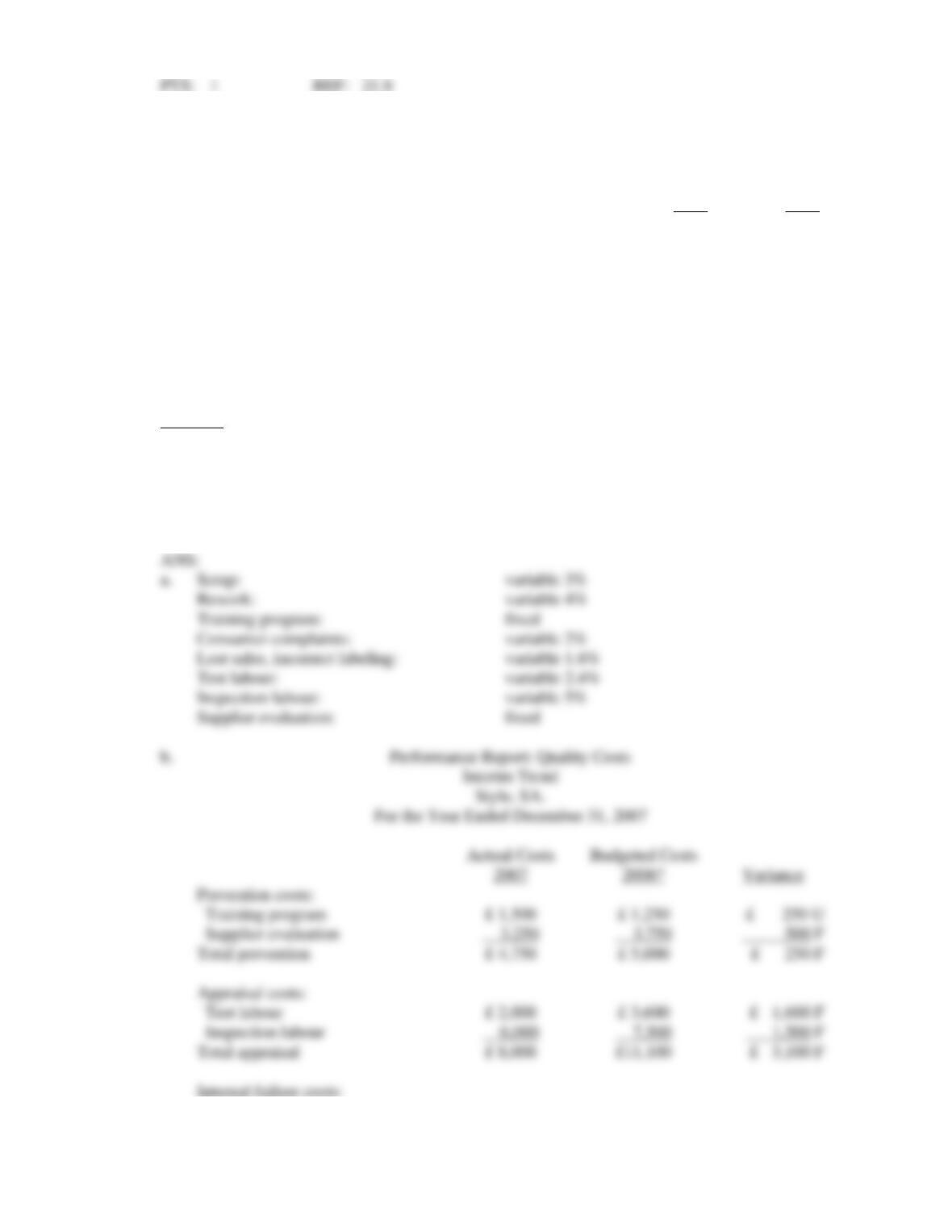

22. In 2006, Style, SA., instituted a quality improvement program. At the end of 2007, the management of

the company requested a report to show the amount saved by the measures taken during the year. The

actual sales and actual quality costs for 2006 and 2007 are as follows:

2006

2007

Sales

£125,000

£150,000

Scrap

3,750

3,750

Rework

5,000

2,500

Training program

1,250

1,500

Consumer complaints

2,500

1,250

Lost sales, incorrect labeling

2,000

—

Test labour

3,000

2,000

Inspection labour

6,250

6,000

Supplier evaluation

3,750

3,250

Required:

a.

Classify each cost as variable or fixed with respect to sales and compute the variable cost

ratio. Be careful-costs may change because of quality improvement, not cost behaviour.

b.

How much did profits increase because of quality improvements made in 2007, assuming all

reductions in quality costs are attributable to quality improvements?

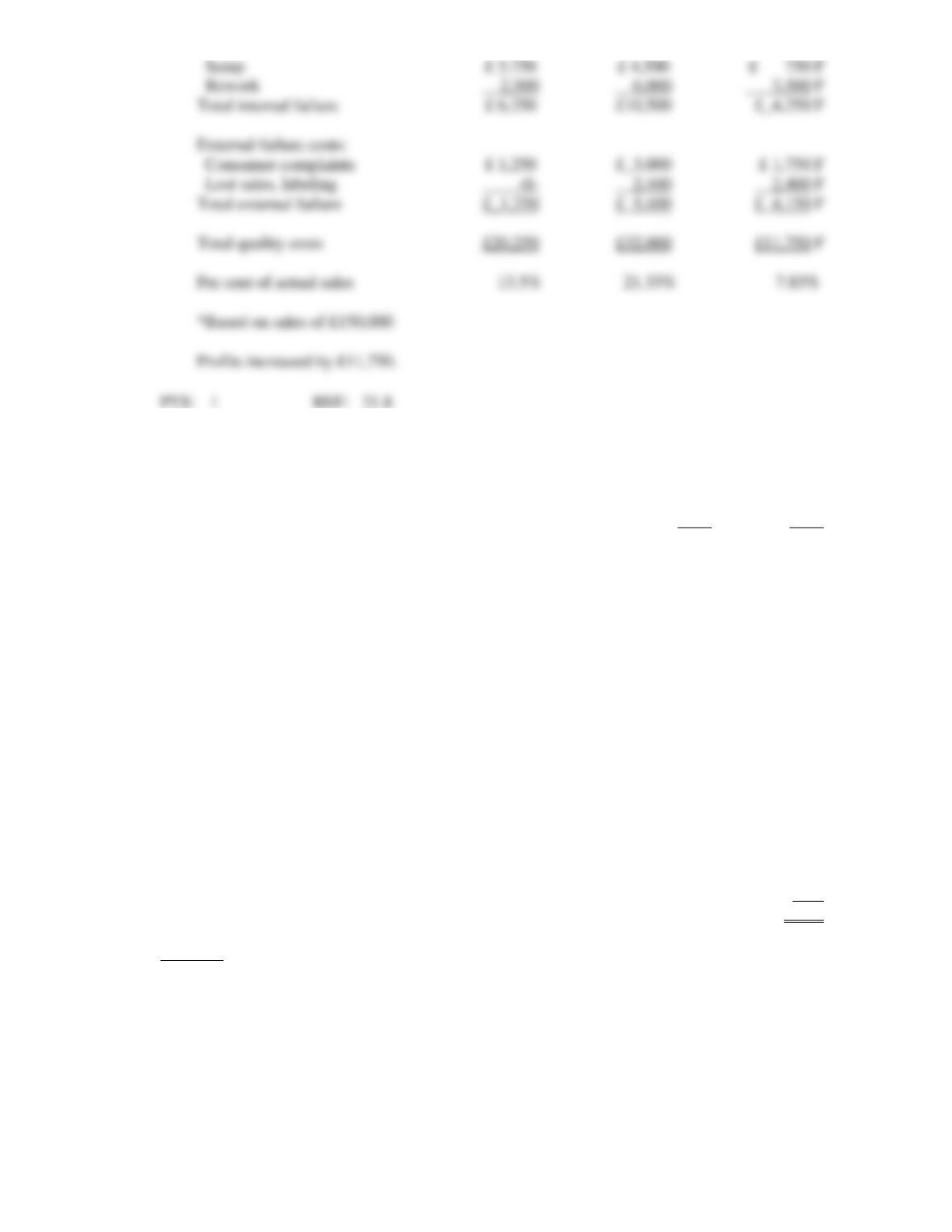

Scrap:

variable 3%

Rework:

variable 4%

Training program:

fixed

Consumer complaints:

variable 2%

Lost sales, incorrect labeling:

variable 1.6%

Test labour:

variable 2.4%

Inspection labour:

variable 5%

Supplier evaluation:

fixed

Prevention costs:

Training program

Supplier evaluation

Total prevention

Appraisal costs:

Test labour

Inspection labour

Total appraisal

Internal failure costs:

23. In 2006, Shelby Foods instituted a quality improvement program. At the end of 2007, the management

of the company requested a report to show the amount saved by the measures taken during the year.

The actual sales and actual quality costs for 2006 and 2007 are as follows:

2006

2007

Sales

£1,000,000

£1,200,000

Scrap

30,000

30,000

Rework

40,000

20,000

Training program

10,000

12,000

Consumer complaints

20,000

10,000

Lost sales, incorrect labeling

16,000

—

Test labour

24,000

16,000

Inspection labour

50,000

48,000

Supplier evaluation

30,000

26,000

Shelby’s management believes that quality costs can be reduced to 2.5 per cent of sales within the next

five years. At the end of Year 2011, Shelby’s sales are projected to have grown to £1,500,000. The

relative distribution of quality costs at the end of Year 2011 is as follows:

Scrap

15%

Training

20%

Supplier evaluation

25%

Test labour

25%

Inspection

_15%

Total quality costs

100%

Required:

a.

Prepare a long-range performance report that compares the quality costs incurred at the end of

2006 with the quality-cost structure expected at the end of 2011.

b.

Are the targeted costs in Year 2011 all value-added costs?

c.

What would be the increase in profits in 2011 if the 2.5 per cent performance standard is met

in that year?

Scrap

Rework

Total internal failure

External failure costs:

Consumer complaints

Lost sales, labeling

Total external failure

Total quality costs

Per cent of actual sales

*Based on sales of £150,000

Profits increased by £11,750.

ESSAY

1. Describe activity-based performance measurement.