Profit increases

£28,000

43. The decision of whether or NOT to process joint products beyond their split-off point is

a.

based on the total cost of the finished product including joint costs.

b.

based on joint costs only.

c.

based on selling price at split-off point.

d.

based on additional revenues versus additional costs of processing further.

44. Which of the following costs is NOT relevant to a decision to sell a product at split-off or to process

the product further and then sell the product?

a.

the joint costs allocated to the product

b.

the selling price of the product at split-off

c.

the additional processing costs after split-off

d.

the selling price of the product after further processing

45. A joint producft should be processed beyond split-off if additional revenue from further processing

exceeds

a.

joint costs.

b.

allocated joint costs.

c.

allocated joint costs and additional costs of further processing.

d.

additional costs of further processing.

46. Which of the following costs is NOT relevant to a decision to sell a product at split-off or process the

product further and then sell the product?

a.

joint costs allocated to the product

b.

the selling price of the product at split-off

c.

the additional processing costs after split-off

d.

the selling price of the product after further processing

Figure 6-9

Stars Manufacturing Company produces Products A1, B2, C3, and D4 through a joint process. The

joint costs amount to £200,000.

If Processed Further

Sales Value

Additional

Product

Units Produced

at Split-Off

Costs

Sales Value

A1

3,000

£10,000

£2,500

£15,000

B2

5,000

30,000

3,000

35,000

C3

4,000

20,000

4,000

25,000

D4

6,000

40,000

6,000

45,000

47. Refer to Figure 6-9. If Product B2 is processed further, profits will

a.

increase by £30,000.

b.

decrease by £3,000.

c.

increase by £32,000.

d.

increase by £2,000.

48. Refer to Figure 6-9. Which product(s) should be sold at split-off to maximize profits in the short run?

a.

Product A1

b.

Product D4

c.

Product B2

d.

Products A1 and D4

Revenues

£5,000

£2,500

£5,000

£5,000

£1,000

£5,000

(£1,000)

Figure 6-10

Manning Company uses a joint process to produce products W, X, Y, and Z. Each product may be sold

at its split-off point or processed further. Additional processing costs of specific products are entirely

variable. Joint processing costs for a single batch of joint products are £120,000. Other relevant data

are as follows:

Sales Value

Additional

Sales Value of

Product

at Split-Off

Processing Costs

Final Product

Y

£ 20,000

£ 32,000

£120,000

Z

28,000

20,000

32,000

W

40,000

60,000

80,000

X

__12,000

____4,000

__20,000

£100,000

£116,000

£252,000

49. Refer to Figure 6-10. Which products should Manning process further?

a.

all

b.

all except Z

c.

Y and X

d.

none

Additional

Y

£68,000

50. Refer to Figure 6-10. Processing Y further will cause profits to

a.

increase by £120,000.

b.

increase by £52,000.

c.

increase by £68,000.

d.

decrease by £32,000.

51. Information about three joint products follows:

A

B

C

Anticipated production

5,000 kgs.

1,000 kgs.

2,000 kgs.

Selling price/kg. at split-off

£10

£30

£16

Additional processing costs/kg.

after split-off (all variable)

£ 6

£12

£24

Selling price/kg. after further

processing

£20

£40

£50

The cost of the joint process is £60,000. Which of the joint products should be sold at split-off?

a.

A

b.

B

c.

C

d.

both A and B

Process Further

£10

£20 – £6 = £14

£30

£40 – £12 = £28

*Sell now

£16

£50 – £24 = £26

Figure 6-11

Information about three joint products follows:

X

Y

Z

Anticipated production

12,000 kgs.

8,000 kgs.

7,000 kgs.

Selling price/kg. at split-off

£16

£26

£48

Additional processing costs/kg.

after split-off (all variable)

£ 8

£20

£20

Selling price/kg. after further

Sell now

Sell now

4,000

Process on

52. Refer to Figure 6-11. Which of the joint products should be processed further?

a.

X

b.

Y

c.

Z

d.

both X and Y

53. Refer to Figure 6-11. If the firm is currently processing all three products beyond split-off, the firm’s

income would be

a.

£736,000.

b.

£654,000.

c.

£596,000.

d.

£514,000.

54. Refer to Figure 6-11. Assuming all of the sell now or process further decisions were correctly made,

what will be the firm’s income?

a.

£736,000

b.

£654,000

c.

£596,000

d.

£610,000

Ottawa Ltd. produces two products from a joint process. Information about the two joint products is as

follows:

Product

Product

____X____

____Y____

Anticipated production (in kgs)

2,000

4,000

Selling price per kg at split-off

£30

£16

Additional processing costs per kg

after split-off (all variable)

£15

£30

Selling price per kg after

further processing

£40

£50

The cost of the joint process is £85,000.

55. Refer to Figure 6-12. Which of Ottawa’s joint products should be sold at split-off?

a.

Product X only

b.

Product Y only

c.

both Product X and Product Y

d.

neither Product X nor Product Y

Product X

Product Y

56. Refer to Figure 6-12. Ottawa currently sells both products at the split-off point. If Ottawa makes

decisions that maximize profit, Ottawa’s profit will increase by

a.

£16,000.

b.

£4,000.

c.

£50,000.

d.

£10,000.

Product X

Product Y

57. Refer to Figure 6-12. Which of Ottawa’s joint products should be processed further?

a.

Product X only

b.

Product Y only

c.

both Product X and Product Y

d.

neither Product X nor Product Y

58. Moore Manufacturing Company makes two products from a common input. Joint processing costs up

to the split-off point total £23,400. The company allocates the joint costs to the products on the basis

of their total sales values at split-off. The total sales value at split-off for both products is the same.

Each product may be sold at the split-off point or processed further. Data concerning one of these

products are as follows:

Sales value at split-off

£15,000

Cost of further processing

10,000

Sales value after further processing

30,000

What is the minimum amount the company would accept for this product if it is to be sold at the

split-off point?

a.

£10,000

b.

£21,700

c.

£20,000

d.

£26,700

PROBLEM

1. Lake Ltd. manufactures two products, AA and BB, from a joint process. A production run costs

£20,000 and results in 500 units of AA and 2,000 units of BB. Both products must be processed past

the split-off point, incurring separable costs of £5 per unit for AA and £10 per unit for BB. The market

price is £25 for AA and £20 for BB.

Required:

a.

Allocate joint production costs to each product using the physical units method.

b.

Allocate joint production costs to each product using the net realizable value method.

c.

Allocate joint production costs to each product using the constant gross margin percentage

method.

Allocation

Product X

Product Y

2. Anderson Company pays a flat fee of £500 for the right to retrieve stray golf balls from lakes and

ponds at golf and country clubs. The recovered balls are then cleaned, graded as to quality (birdie,

bogey, or duffer), and sold to sporting goods stores at the following prices per dozen: birdie quality,

£5; bogey quality, £4; and duffer quality, £3. Last month £8,000 of cost was incurred retrieving the

following quantities of golf balls: birdie quality, 1000 dozen; bogey quality, 3,000 dozen; and duffer

quality, 2,000 dozen.

Required:

(Calculate relative quantity to three decimal points.)

a.

Determine the cost and gross profit per cent for each type of golf ball using the physical units

method of joint cost allocation.

b.

Repeat part (a) using the sales-value-at-split-off method of joint cost allocation.

c.

The company has an opportunity to sell bogey quality balls for £4.50 per dozen to a company

that operates golf driving ranges; however, the balls will have to be painted and striped. The

company estimates that the cost of painting and striping will be 60 cents per dozen. Assuming

the physical unit method is used to allocate joint costs, should the offer be accepted?

Relative

Product

Allocation

5/25 £20,000 =

AA: 10/30 £20,000 = £6,667

BB: 20/30 £20,000 = £13,333

Sales (500 £25) + (2,000 £20) = £52,500

Costs (500 £5) + (2,000 £10) + £20,000 = £42,500

COGS Percentage = £42,500/£52,500 = 80.9524%

AA: (500 £25 80.9524%) – £2,500 = £7,619.05

BB: (2,000 £20 80.9524%) – £20,000 = £12,380.96

3. Maddux Company manufactures products X, Y, and Z in a joint process. The following information is

available:

Products

X

Y

Z

Total

Units produced

12,000

?

?

24,000

Sales value

at split-off

?

?

£50,000

£200,000

Joint costs

£48,000

?

?

£120,000

Sales value if

processed further

£110,000

£90,000

£60,000

£260,000

Additional cost if

processed further

£18,000

£14,000

£10,000

£42,000

Joint product costs are allocated using the sales value at split-off approach.

Required:

a.

What is the sales-value-at-split-off for Product X?

b.

What is the amount of joint costs allocated to Product Y using the sales-value-at-split-off

method?

c.

If the company used the physical units method to allocate joint cost, how much joint cost

would be allocated to Product X?

Sales price/dozen

£4.00

Sales

£6,000

Joint costs

_2,664

Gross profit

£3,336

Gross profit %

b.

Product

Allocation

Bogeys

Total

Joint costs

2,080

Gross profit

£ 7,840

Gross profit %

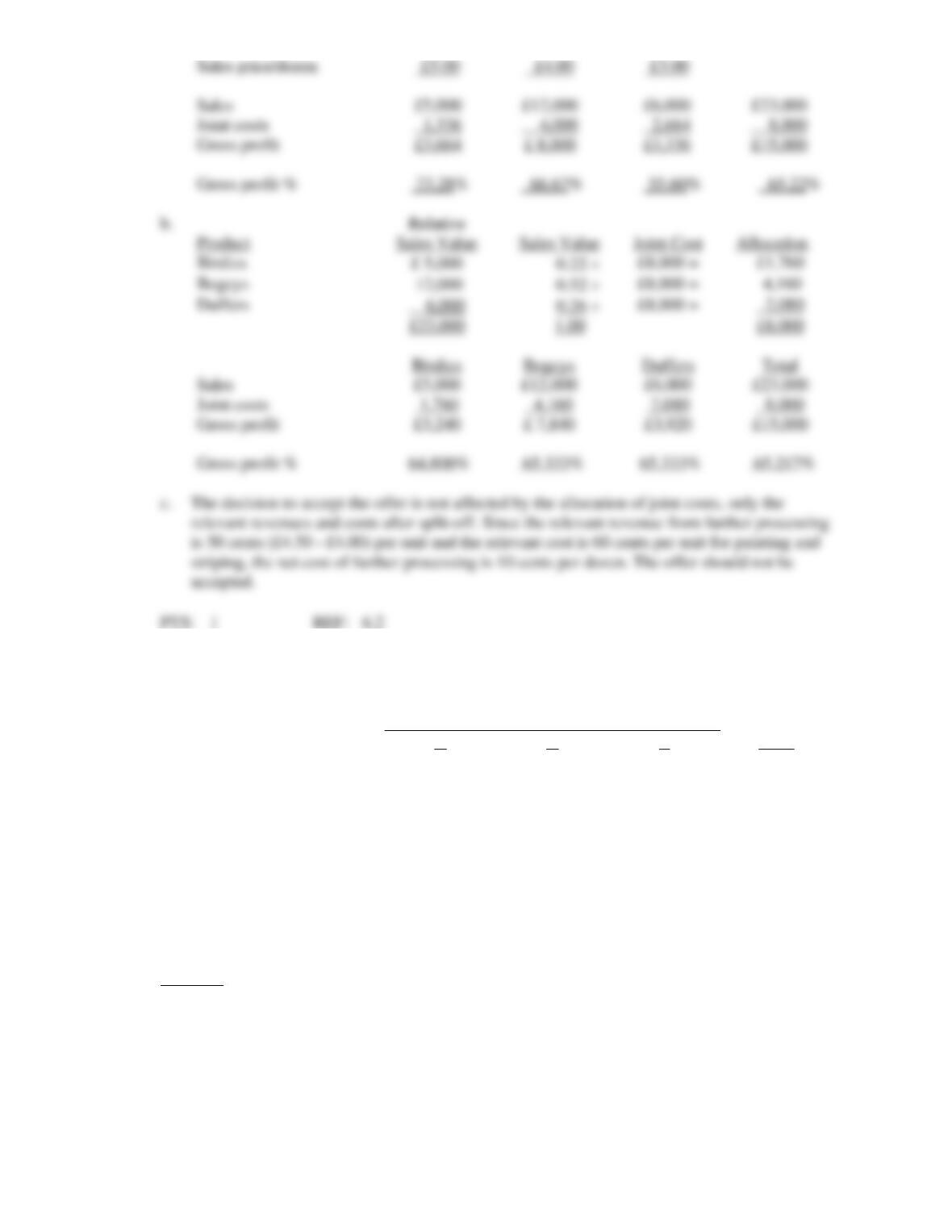

4. Nelson SA. obtains two products and a by-product from its production process. By-product revenues

are treated as other income and a noncost approach is used to assign costs to them. During the period,

1,200 units were processed at a cost of £12,000 for materials and conversion costs, resulting in the

following:

Sales Value

Costs after

Final

Product

Units

at Separation

Separation

Value

X

200

£4,000

£2,000

£10,000

Y

400

5,000

6,000

12,000

By-product

150

500

500

1,500

Required:

a.

Account for all costs using a physical basis for allocation.

b.

Account for all costs using net realizable value as the basis for allocation.

c.

Account for all costs using final sales value as the basis for allocation.

d.

How much joint costs should be allocated to the by-product?

Product

Units

200

Product

Total

£ 4,000

£ 6,000

6,000

Product

Sales

£ 8,000

_6,000

£8,000

Product

Total

£ 6,857

£ 8,857

6,000

Product

Sales

12/22

6,545

Product

Total

£2,000

£48,000/£120,000 £200,000 = £80,000

{£120,000 – £48,000 – [(£50,000/£200,000) £120,000]} = £42,000

12,000/24,000 £120,000 = £60,000

5. Explain how joint cost allocation may be misleading in managerial decision making.

6. Park Company produces three products in a joint process: A, B, and C. The joint costs are described as

follows:

Direct materials

£45,000

Direct labour

60,000

Overhead

30,000

The split-off values for A, B, and C are £100,000, £120,000 and £80,000, respectively. If management

processes A beyond the split-off point, the sales value of A would increase to £150,000. In order to

process A further, the company must rent another facility for £24,000, as well as incur additional

materials and labour costs equal to £15,000.

Required:

a.

What is the amount of joint costs allocated to products A, B, and C if the sales value at

split-off value method is used?

b.

Should the division process A further or sell it at split-off? What is the effect of the

decision on gross profit?

Joint Cost

b.

Additional revenues

(£150,000 – £100,000)

Additional costs

(£24,000 + £15,000)

Profit would increase by

7. Mickey Company manufactures three joint products: X, Y, and Z. The cost of the joint process is

£30,000. Information about the three products follows:

X

Y

Z

Anticipated production

5,600 kgs.

10,000 kgs.

2,500 kgs.

Selling price/kg. at split-off

£2.00

£1.00

£3.00

Additional processing costs/kg.

after split-off (all variable)

£1.50

£1.25

£.75

Selling price/kg. after

further processing

£2.50

£3.75

£6.25

Allocated joint costs

£12,000

£10,500

£7,500

Required:

a.

Determine whether each product should be sold at split-off or processed further. Show all

supporting calculations in good form.

b.

Determine the firm’s income if the firm processed all three products beyond split-off.

8. Arcadia, SA, uses a joint process to produce Products W, X, Y, Z. Each product may be sold at its

split-off point or processed further. Additional processing costs of specific products are entirely

variable. Joint processing costs for a single batch of joint products are £200,000. Other relevant data

are as follows:

Sales Value

Additional

Sales Value of

Product

at Split-off

Processing Costs

Final Product

W

£ 40,000

£24,000

£ 70,000

X

16,000

10,000

20,000

Y

20,000

10,000

48,000

Z

__24,000

_16,000

__36,000

£100,000

£60,000

£174,000

Required:

a.

Determine which products should be processed further.

b.

How will processing each product further affect profits?

Process Further

X

£11,200

£14,000

_(8,400)

£ 5,600

Y

£37,500

£25,000

Z

£ 7,500

£15,625

£13,750

b.

£14,350 (£13,750 + £25,000 + £5,600 – £30,000)

9. Maxwell Company manufactures two products from a joint process. Information about the two joint

products is as follows:

Product ABC

Product XYZ

Anticipated production (in gallons)

40,000

50,000

Selling price per gallon at split-off

£50

£60

Additional processing costs per gallon

after split-off (all variable)

£25

£95

Selling price per gallon after further

processing

£100

£140

The cost of the joint process is £1,500,000.

Required:

a.

Which of Maxwell’s joint products should be processed further?

b.

Assume that Maxwell currently sells both products at the split-off point. What is Maxwell’s

income?

c.

Assume that Maxwell makes decisions about its joint products that maximize profit. What is

Maxwell’s income?

Product ABC should be processed further; Product XYZ should be sold at split-off.

Product ABC

Product XYZ

b.

£3,500,000

Product ABC (40,000 gallons £50)

Product XYZ (50,000 gallons £60)

Less: Joint process costs

Income

£4,500,000

Product ABC (40,000 gallons £100)

12,000

10. Jazzmyne Company manufactures two products from a joint process. Information about the two joint

products is as follows:

Product X

Product Y

Anticipated production (in units)

10,000

15,000

Selling price per unit at split-off

£60

£100

Additional processing costs per unit

after split-off (all variable)

£100

£55

Selling price per unit after further

processing

£150

£175

The cost of the joint process is £1,750,000.

Required:

a.

Which of Jazzmyne’s joint products should be processed further?

b.

Assume that Jazzmyne currently sells both products at the split-off point. What is Jazzmyne’s

income?

c.

Assume that Jazzmyne makes decisions about its joint products that maximize profit. What is

Jazzmyne’s income?

Process Further

Product X

Product Y

b.

£350,000

(10,000 units £60)

(15,000 units £100)

Less: Joint process costs

Income

£650,000

£2,400,000

Less: Joint process costs

_1,750,000

Income

£ 650,000

Product XYZ (50,000 gallons £60)

Less: Joint process costs

Income