54. Fixed overhead was budgeted at £500,000 and 25,000 direct labour hours were budgeted. If the fixed

overhead volume variance was £12,000 favourable and the fixed overhead spending variance was

£16,000 unfavourable, fixed overhead applied must be

a.

£516,000.

b.

£512,000.

c.

£504,000.

d.

£528,000.

55. Fortensky Construction planned to produce 275,000 units using 34,375 machine hours. Actual output

was 290,000 units using 37,425 machine hours. Fortensky’s volume variance

a.

was favourable.

b.

was unfavourable.

c.

was zero.

d.

cannot be determined from the information given.

Figure 17-6

Budgeted fixed overhead for the year

£300,000

Budgeted direct labour hours for the year

30,000

Actual fixed overhead for August

£24,000

Actual variable overhead for August

£10,000

Direct labour hours worked in August

2,600

Standard variable overhead cost per direct labour hour

£4

Standard direct labour hours allowed for August production

2,750

56. Refer to Figure 17-6. The standard rate for total overhead is

a.

£14.

b.

£13.

c.

£10.

d.

£4.

57. Refer to Figure 17-6. The variable overhead spending variance would be

a.

£2,000 favourable.

b.

£1,200 favourable.

c.

£400 favourable.

d.

£200 favourable.

58. Refer to Figure 17-6. The variable overhead efficiency variance would be

a.

£1,000 favourable.

b.

£600 favourable.

c.

£400 favourable.

d.

£200 favourable.

59. Refer to Figure 17-6. The fixed overhead spending variance would be

a.

£2,500 unfavourable.

b.

£2,500 favourable.

c.

£1,000 unfavourable.

d.

£1,000 favourable.

60. Refer to Figure 17-6. The fixed overhead volume variance would be

a.

£2,500 unfavourable.

b.

£2,500 favourable.

c.

£1,000 unfavourable.

d.

£1,000 favourable.

Figure 17-7

Orient Company has developed the following standards for one of its products:

Direct materials

10 pounds £8 per pound

Direct labour

6 hours £20 per hour

Variable overhead

6 hours £6 per hour

The following activities occurred during the month of November:

Materials purchased

8,000 pounds costing £70,000

Materials used

6,500 pounds

Units produced

600 units

Direct labour

4,200 hours costing £75,600

Actual variable overhead

£26,400

The company records materials price variances at the time of purchase.

61. Refer to Figure 17-7. Orient’s materials price variance would be

a.

£22,000 unfavourable.

b.

£18,000 unfavourable.

c.

£6,000 unfavourable.

d.

£4,000 unfavourable.

62. Refer to Figure 17-7. Orient’s materials usage variance would be

a.

£22,000 unfavourable.

b.

£12,000 favourable.

c.

£10,000 unfavourable.

d.

£4,000 unfavourable.

63. Refer to Figure 17-7. Orient’s labour rate variance would be

a.

£12,000 unfavourable.

b.

£12,000 favourable.

c.

£8,400 favourable.

d.

£3,600 unfavourable.

64. Refer to Figure 17-7. Orient’s labour efficiency variance would be

a.

£12,000 unfavourable.

b.

£12,000 favourable.

c.

£8,400 favourable.

d.

£3,600 unfavourable.

65. Refer to Figure 17-7. Orient’s variable overhead spending variance would be

a.

£4,800 favourable.

b.

£4,800 unfavourable.

c.

£3,600 unfavourable.

d.

£1,200 unfavourable.

66. Refer to Figure 17-7. Orient’s variable overhead efficiency variance would be

a.

£1,200 unfavourable.

b.

£3,600 unfavourable.

c.

£4,800 unfavourable.

d.

£4,800 favourable.

67. If actual fixed overhead was £164,000 and there was a £4,800 favourable spending variance and a

£1,000 unfavourable volume variance, budgeted fixed overhead must have been

a.

£168,800.

b.

£167,800.

c.

£165,000.

d.

£163,000.

e.

£159,200.

68. Fixed overhead was budgeted at £210,000 and 25,000 direct labour hours were budgeted. If the fixed

overhead volume variance was £8,000 unfavourable and the fixed overhead spending variance was

£3,000 favourable, fixed overhead applied must be

a.

£218,000.

b.

£213,000.

c.

£207,000.

d.

£205,000.

e.

£202,000.

Figure 17-8

The following information was extracted from the accounting records of Noelle Company:

STANDARD COST CARD

PER UNIT

Direct materials:

8 pounds £1.20 per pound

£ 9.60

Direct labour:

3 hours £20 per hour

60.00

Variable overhead:

3 hours £6 per hour

18.00

Fixed overhead

___?__

Total standard cost per unit

___?__

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on

an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company’s operations for the period:

Units produced

10,500

Direct labour

29,000 hours costing £590,000

Overhead incurred:

Variable

£182,000

Fixed

£430,000

69. Refer to Figure 17-8. Noelle’s standard fixed overhead rate is

a.

£14.82.

b.

£14.48.

c.

£14.34.

d.

£14.00.

70. Refer to Figure 17-8. Noelle’s variable overhead spending variance would be

a.

£7,000 favourable.

b.

£8,000 unfavourable.

c.

£15,000 favourable.

d.

£23,000 unfavourable.

71. Refer to Figure 17-8. Noelle’s variable overhead efficiency variance would be

a.

£7,000 favourable.

b.

£8,000 unfavourable.

c.

£15,000 favourable.

d.

£23,000 unfavourable.

72. Refer to Figure 17-8. Noelle’s fixed overhead spending variance would be

a.

£10,000 unfavourable.

b.

£11,000 unfavourable.

c.

£21,000 favourable.

d.

£31,000 favourable.

73. Refer to Figure 17-8. Noelle’s fixed overhead volume variance would be

a.

£10,000 unfavourable.

b.

£11,000 unfavourable.

c.

£21,000 favourable.

d.

£31,000 favourable.

74. Taylor Company’s budgeted sales were 10,000 units at £200 per unit. Actual sales were 9,200 units at

£210 per unit.

Taylor’s sales price variance is

a.

£68,000 (U).

b.

£100,000 (U).

c.

£8,000 (U).

d.

£92,000 (F).

75. The sales price variance is created by a difference between

a.

actual and standard contribution margin.

b.

actual and expected sales price.

c.

expected and standard net income.

d.

actual and expected sales volume.

76. Franklin Company expected sales were 2,000 units at £100 per unit. During 2011, it had actual sales of

1,800 units at £110 per unit. Budgeted variable costs were £60 per unit.

What is Franklin’s sales price variance?

a.

£8,000 (U)

b.

£20,000 (U)

c.

£18,000 (F)

d.

£2,000 (U)

77. A sales volume variance will be favourable when:

a.

actual units sold is greater than budgeted sales volume.

b.

actual units sold is less than budgeted sales volume.

c.

actual selling price is greater than budgeted selling price.

d.

actual contribution margin is greater than budgeted contribution margin.

78. The volume variance is caused by:

a.

the difference between the activity allowed for the actual output and the budgeted activity

used in computing the fixed overhead rate.

b.

the difference between total budgeted fixed overhead and total standard fixed overhead

assigned to production.

c.

the difference between the activity allowed for the actual output and the total standard

fixed overhead assigned to production.

d.

the difference between the standard fixed overhead rate and the actual fixed overhead rate.

79. For planning and control purposes, fixed overhead is NOT included in the standard cost per unit

because:

a.

it is incurred based on the number of units produced.

b.

the number of units produced do not vary from period to period.

c.

it can best be controlled on a lump-sum basis.

d.

of all of the above

PROBLEM

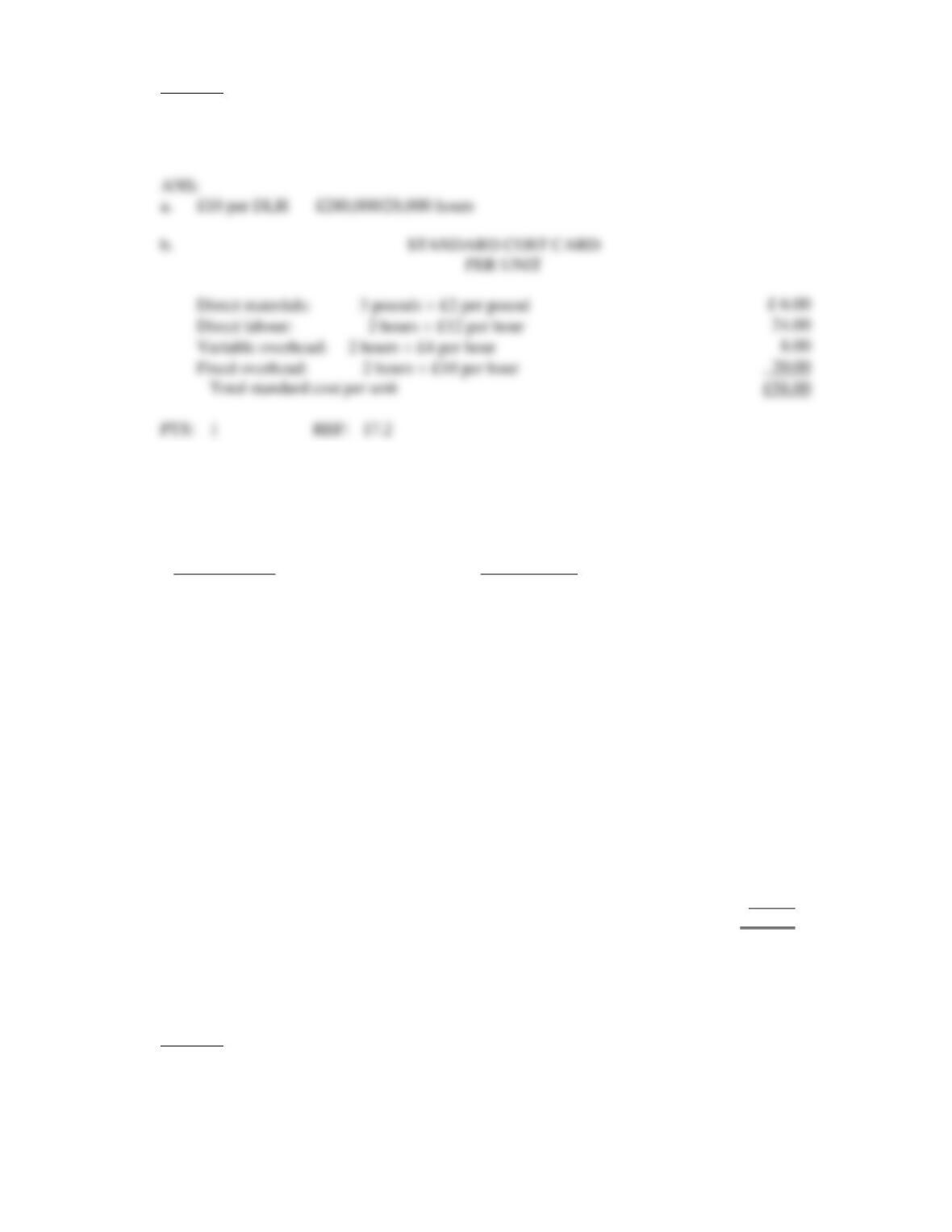

1. The following standard costs were developed for one of Commodore Company’s products:

STANDARD COST CARD

PER UNIT

Direct materials:

4 pounds £5 per pound

£20.00

Direct labour:

1.5 hours £20 per hour

30.00

Variable overhead:

£10 per hour

?

Fixed overhead

Total standard cost per unit

The following information is available regarding the company’s operations for the period:

Units produced

15,000

Materials purchased

90,000 pounds at £3.60 per pound

Materials used

80,000 pounds

Direct labour

9,000 hours at £16.50 per hour

Overhead incurred:

Variable

£220,000

Fixed

£640,000

Budgeted fixed overhead for the period is £600,000, and expected capacity for the period is 20,000

direct labour hours.

Required:

a.

Calculate the standard fixed overhead rate.

b.

Complete the standard cost card for the product.

2. The following standard costs were developed for one of Commodore Company’s products:

STANDARD COST CARD

PER UNIT

Direct materials:

3 pounds £2 per pound

£ 6.00

Direct labour:

2 hours £12 per hour

24.00

Variable overhead:

£4 per hour

?

Fixed overhead

___?__

Total standard cost per unit

?

The following information is available regarding the company’s operations for the period:

Units produced

12,000

Materials purchased

50,000 pounds at £2 per pound

Materials used

40,000 pounds

Direct labour

25,000 hours at £13 per hour

Overhead incurred:

Variable

£90,000

Fixed

£300,000

Budgeted fixed overhead for the period is £280,000, and expected capacity for the period is 28,000

direct labour hours.

£30 per DLH £600,000/20,000 hours

b.

Direct materials:

4 pounds £5 per pound

1.5 hours £20 per hour

Variable overhead:

1.5 hours £10 per hour

Fixed overhead:

1.5 hours £30 per hour

Total standard cost per unit

Required:

a.

Calculate the standard fixed overhead rate.

b.

Complete the standard cost card for the product.

3. Mills Company uses standard costing for direct materials and direct labour. Management would like to

use standard costing for variable and fixed overhead.

The following monthly cost functions were developed for overhead items:

Overhead Item

Cost Function

Indirect materials

£0.30 per DLH

Indirect labour

£0.20 per DLH

Utilities

£0.25 per DLH

Insurance

£2,000

Depreciation

£10,000

The cost functions are considered reliable within a relevant range of 70,000 to 100,000 direct labour

hours. The company expects to operate at 80,000 direct labour hours per month.

Information for the month of September is as follows:

Actual overhead costs incurred:

Indirect materials

£22,500

Indirect labour

15,000

Utilities

21,000

Insurance

2,500

Depreciation

_10,000

Total

£71,000

Actual direct labour hours worked

85,000

Standard direct labour hours

allowed for production achieved

82,000

Required:

a.

Calculate the following standard overhead rates based upon expected capacity:

Variable overhead rate

£10 per DLH £280,000/28,000 hours

b.

Direct materials: 3 pounds £2 per pound

Direct labour: 2 hours £12 per hour

Variable overhead: 2 hours £4 per hour

Fixed overhead: 2 hours £10 per hour

Total standard cost per unit

Fixed overhead rate

Total overhead rate

b.

Calculate the following variances:

Variable overhead spending variance

Variable overhead efficiency variance

Fixed overhead spending variance

Fixed overhead volume variance

4. The following budgeted and actual contribution statement is for a component sold by Dark, Inc. for

June of this year:

Actual

Budget

Unit sales

18,000

20,000

Unit selling price

£3.70

£4.00

Sales revenue

£66,600

£80,000

Cost of goods sold

36,000

40,000

Gross profit

£30,600

£40,000

Operating costs (all fixed)

20,000

24,000

Contribution to corporate costs and profits

£10,600

£16,000

Required:

a.

Compute the sales price variance, the net sales volume variance, and the operating cost

variance for June.

b.

Use the calculations in part a. to reconcile the budgeted and actual contribution to

corporate costs and profits.

c.

How would you evaluate the performance of Dark, Inc.‘s manager?

ANS:

Sales price variance = (£3.70 – £4.00) 18,000 = £5,400 (U);

£4,000 (U);

Variable overhead rate:

£0.75 per DLH

(£0.30 + £0.20 + £0.25)

Fixed overhead rate:

£0.15 per DLH

[(£2,000 + £10,000)/80,000 hours]

Total overhead rate:

£0.90 per DLH

(£0.75 + £0.15)

[(£22,500 + £15,000 + £21,000)-(85,000 hours £0.75)]

Variable overhead efficiency variance:

[(85,000 hours £0.75)-(82,000 hours £0.75)]

Fixed overhead spending variance:

(£12,500 – £12,000)

Fixed overhead volume variance:

[£12,000 -(82,000 hours £0.15)]

5. The Chair Division operates as a revenue centre and has the following relevant information for 2011:

Sales price variance

£1,000 (U)

Sales volume variance

£2,000 (F)

Net sales volume variance

£1,200 (F)

Budgeted unit contribution margin per unit

£6

The actual selling price was £1 less than the budgeted selling price.

Required:

a.

Calculate the budgeted sales price.

b.

Calculate the actual sales price.

c.

Calculate actual unit sales.

d.

Calculate budget unit sales.

Net sales volume variance = (AS – BS) BCM

b.

£10 – £1 = £9

c.

Sales price variance = (ASP – BSP)AS = – £1,000

Operating costs variances = (£20,000 – £24,000) = £4,000 (F)

Budgeted contribution

Sales price variance

Net sales volume variance

Operating costs variance

Actual contribution

competition appears to have forced a price reduction that did NOT increase sales in units.