Archives: Quiz

Accounting Chapter 23 4 Perkins Company provides the following data developed for its

Operating expenses: Fixed ……………………………………….. $12,000 Variable ……………………………………. 40,000 52,000 Income from operations ……………………….. $ 48,000 The company’s actual activity tor the year follows: Sales (21,000 units) ……………………………. $651,000 Cost of goods sold: Direct materials …………………………….. $231,000 Direct labor ………………………………… 168,000 […]

Accounting Chapter 23 3 The Difference Between The Actual Price Item

23–41 95. Bok Company’s output for the current period was assigned a $200,000 standard direct materials cost. The direct materials variances included a $5,000 favorable price variance and a $3,000 unfavorable quantity variance. What is the actual total direct materials […]

Accounting Chapter 23 2 The difference between the overhead costs actually incurred

23–21 60. Kyle, Inc. has collected the following data on one of its products. The direct materials quantity variance is: Direct materials standard (4 lbs. @ $1/lb.) $4 per finished unit Total direct materials cost variance—unfavorable $13,750 Actual direct materials […]

Accounting Chapter 23 1 Standard costs can serve as a basis for evaluating actual performance

Chapter 23 FLEXIBLE BUDGETS AND STANDARD COSTS 1. Standard costs can serve as a basis for evaluating actual performance. Answer: True Blooms: Remember AACSB: Communication AICPA BB: Resource Management AICPA FN: Measurement Difficulty: 1 Easy Learning Objective: 23-C1 Topic: Standard […]

Accounting Chapter 22 5 Sweeny Co. is preparing a cash budget for the second quarter of

149. Sweeny Co. is preparing a cash budget for the second quarter of the coming year. The following data have been forecasted: April May Sales ………………………………………………. $150,000 $157,500 Merchandise purchases …………………………… 107,000 112,400 Operating expenses: Payroll …………………………………………. 13,600 14,280 Advertising […]

Accounting Chapter 22 4 Cambridge, Inc., is preparing its master budget for the quarter ended

22–65 January February March Sales budget: Sales in Units 1,200 1,000 1,600 Price per unit * $25 * $25 * $25 Dollar Sales $30,000 $25,000 $40,000 Cash receipts table: Cash sales (40% of current mo. sales) $ 12,000 $ 10,000 […]

Accounting Chapter 22 2 A plan that reports the units or costs of merchandise to be purchased

63. A plan that lists dollar amounts to be received from disposing of plant assets and dollar amounts to be spent on purchasing additional plant assets is called a: A. Cash budget. B. Capital expenditures budget. C. Rolling budget. D. […]

Accounting Chapter 22 1 Consulting the persons affected by a budget when it is prepared

Chapter 22 MASTER BUDGETS AND PLANNING 1. Consulting the persons affected by a budget when it is prepared can provide an effective means of motivation and cooperation. Answer: True Blooms: Remember AACSB: Communication AICPA BB: Resource Management AICPA FN: Measurement […]

Accounting Chapter 22 3 Selling Expense Budget j Rolling Budgets 1 Plan

April May June June Sales in Units ……….. 240 280 300 240 Although each month’s ending inventory of finished units should be 60% of the next month’s sales, the March 31 finished goods inventory is only 100 units. A finished […]

Accounting Chapter 21 5 Round Your Answers The Nearest Whole Unit or

Answer: (a) Profit area; (b) Loss area; (c) Breakeven point Blooms: Understand AACSB: Analytic AICPA BB: Resource Management AICPA FN: Measurement Difficulty: 2 Medium Learning Objective: 21-P3 Topic: Graphing Costs and Sales 168. The sales mix of Palm Company is […]

Accounting Chapter 21 4 Contribution Margin fixed Costs income Before Income Taxes

145. A firm produces and sells a product with a contribution margin of $32 per unit. The firm is presently selling 90,000 units and earning $240,000 in after-tax income. Taxes are $80,000 at a 25% tax rate. If the firm […]

Accounting Chapter 21 3 Wayward Enterprises manufactures and sells three distinct styles

104. Camden Corporation sells three products (M, N, and O) in the following mix: 3:1:2. Unit price and cost data are: M N O Unit sales price ……………………………… $7 $4 $6 Unit variable costs ………………………… 3 2 3 Total fixed […]

Accounting Chapter 21 2 The budgeted income statement presented below is for Griffith

21–21 65. Use the following information to determine the margin of safety in dollars: Unit sales 50,000 Units Dollar sales ………………………………………………………… $500,000 Fixed costs ………………………………………………………… $204,000 Variable costs …………………………………………………….. $187,500 A. $ 88,500. B. $108,500. C. $173,600. D. $326,400. E. […]

Accounting Chapter 21 1 Total variable costs change proportionately with changes in output activity

Chapter 21 COST-VOLUME-PROFIT ANALYSIS 1. Total variable costs change proportionately with changes in output activity. Answer: True Blooms: Remember AACSB: Communication AICPA BB: Resource Management AICPA FN: Measurement Difficulty: 1 Easy Learning Objective: 21-C1 Topic: Different Types of Cost Behavior […]

Accounting Chapter 20 5 Prepare journal entries to record the following production activities

Costs incurred this period $2,400,000 $5,120,000 Total costs incurred $2,976,000 5,520,000 Equivalent units of production 96,000 92,000 Cost per EUP $31.00 $60 Costs of units transferred out Direct materials (90,000 * $31) $2,790,000 Direct labor & Overhead (90,000 * $60) […]

Accounting Chapter 20 4 Dipping Department The Indiana Factory for The Month

20–61 Blooms: Apply AACSB: Analytic AICPA BB: Industry AICPA FN: Measurement Difficulty: 3 Hard Learning Objective: 20-C2 Learning Objective: 20-C4 Topic: Equivalent Units Topic: Process Costing using FIFO 136. Refer to the following information about the Painting Department in the […]

Accounting Chapter 20 3 the production department of a process manufacturing system completed

A. Debit Raw Materials Inventory $87,000; credit Accounts Payable $87,000. B. Debit Raw Materials Inventory $87,000; credit Finished Goods Inventory $87,000. C. Debit Cost of Goods Sold $87,000; credit Finished Goods Inventory $87,000. D. Debit Goods in Process Inventory $87,000; […]

Accounting Chapter 20 2 The cost of units transferred from Goods in Process Inventory

66. Since the process cost summary describes the activities of a production department for a specified reporting period, it does not present information about any costs incurred in prior periods. Answer: False Blooms: Remember AACSB: Communication AICPA BB: Industry AICPA […]

Accounting Chapter 20 1 Process manufacturing usually reflects a manufacturer that produces

20-1 Chapter 20 PROCESS COST ACCOUNTING 1. The managers of process manufacturing systems focus on the series of processes needed to complete the production of products. 2. Process manufacturing usually reflects a manufacturer that produces large quantities of identical products. […]

Accounting Chapter 19 5 Determine The Predetermined Overhead Rate For The

Factory equipment rental…………………… 100,000 (a) Calculate the predetermined overhead rate and calculate the overhead applied during the year. (b) Determine the amount of over- or underapplied overhead and prepare the journal entry to eliminate the over- or underapplied overhead assuming […]

Accounting Chapter 19 4 Purchase Raw Materials Account b Assignment Materials Costs

Fill in the blanks for the following: (1) The total cost of the direct materials, direct labor, and factory overhead applied in the December 31 goods in process inventory is $_______________________. (2) The company’s overhead application rate is __________________% (3) […]

Accounting Chapter 19 3 Docksider Boats uses a job order cost accounting system

Feedback: OH rate = $396,000/$220,000 = 180% 105. Hancock Manufacturing allocates overhead to production on the basis of direct labor costs. At the beginning of the year, Hancock estimated total overhead of $396,000; materials of $410,000 and direct labor of […]

Accounting Chapter 19 2 A source document that production managers use to request

19–21 64. A source document that production managers use to request materials for production and that is used to assign materials costs to specific jobs or to overhead is a: A. Job cost sheet. B. Production order. C. Materials requisition. […]

Accounting Chapter 19 1 Flow Overhead Costs Job Order Cost Accounting36

Chapter 19 JOB ORDER COST ACCOUNTING 1. Cost accounting systems accumulate costs and then assign them to products or services. Answer: True Blooms: Remember AACSB: Communication AICPA BB: Industry AICPA FN: Measurement Difficulty: 1 Easy Learning Objective: 19-C1 Topic: Features […]

Accounting Chapter 18 5 The model whose goal is to eliminate waste while satisfying the customer

18-76 Beginning raw materials inventory _______ ______ Ending raw materials inventory _______ ______ Raw material purchases _______ ______ Depreciation of factory building _______ ______ Cost of goods manufactured _______ ______ 167. Information for Gifford, Inc., as of December 31 follows. […]

Accounting Chapter 18 4 Also Indicate With X for Each Item Product

141. There are many differences between financial and managerial accounting. Identify and explain at least three of these differences. 18-60 Answer: The differences include: (1) Users and decision makers – Financial accounting focuses on external decision makers and managerial accounting […]

Accounting Chapter 18 3 Total manufacturing costs incurred during the year do not include

111. If beginning and ending goods in process inventories are $5,000 and $15,000, respectively, and cost of goods manufactured is $170,000, what is the total manufacturing cost for the period? A. $180,000. B. $155,000. C. $160,000. D. $175,000. E. $165,000. […]

Accounting Chapter 18 2 The Cost Labor That Not Clearly Associated

Blooms: Remember AACSB: Communication AICPA BB: Resource Management AICPA FN: Decision Making Difficulty: 1 Easy Learning Objective: 18-C6 Topic: Trends in Managerial Accounting 66. The model whose goal is to eliminate waste while satisfying the customer and providing a positive […]

Accounting Chapter 18 1 Financial Statements38 The Main Difference Between The

Chapter 18 MANAGERIAL ACCOUNTING CONCEPTS AND PRINCIPLES 1. Managerial accounting assists in analysis, planning, and control of costs. Answer: True Blooms: Remember AACSB: Communication AICPA BB: Industry AICPA FN: Decision Making Difficulty: 1 Easy Learning Objective: 18-C1 Topic: Purpose of […]

Accounting Chapter 17 5 170 The Following Summaries From The Income

(a) working capital (b) acid-test ratio (c) current ratio (d) debt ratio (e) equity ratio (f) debt-to-equity ratio Cash……………………….. $ 40,000 Current liabilities …………. $ 64,000 Accounts receivable………. 35,000 Long-term liabilities……….72,000 Inventory………………….. 60,000 Common stock……………..100,000 Equipment………………… 150,000 Retained earnings…………. 49,000 […]

Accounting Chapter 17 3 Yield 3 Accounts Receivable Turnover 4 Days

17–41 A. 36.4% for Year 2 and 41.1% for Year 1. B. 55.0% for Year 2 and 56.0% for Year 1. C. 119.4% for Year 2 and 100.0% for Year 1. D. 117.2% for Year 2 and 100.0% for Year […]

Accounting Chapter 17 2 Intra-company standards for financial statement analysis

72. Standards for comparisons in financial statement analysis include: A. Intra-company standards. B. Competitors’ standards. C. Industry standards. D. Guidelines (rules of thumb). E. All of the choices are standards for comparisons. Answer: E Blooms: Remember AACSB: Communication AICPA BB: […]

Accounting Chapter 17 4 What The Company’s Return Common Stockholders Equity answer

Cash $ 569 $ 448 Accounts receivable 2,234 2,337 Merchandise inventory 1,062 1,071 Plant assets 2,432 2,138 Bonds payable 1,164 1,666 Equity 2,777 2,894 Answer: Cash [($569 – $448)/$448] * 100 = 27.0% increase Accounts receivable [($2,234 – $2,337)/$2,337] * […]

Accounting Chapter 17 1 Financial statement analysis lessens the need for expert judgment

Chapter 17 ANALYSIS OF FINANCIAL STATEMENTS 1. Financial statement analysis is the application of analytical tools to general-purpose financial statements and related data for making business decisions. Answer: True Blooms: Remember AACSB: Communication AICPA BB: Industry AICPA FN: Decision Making […]

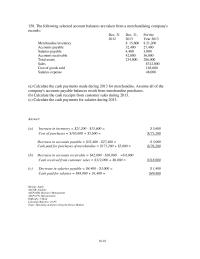

Accounting Chapter 16 5 Cash and cash equivalents, beginning-year balance

158. The following selected account balances are taken from a merchandising company’s records: Dec. 31 Dec. 31, For the 2012 2013 Year 2013 Merchandise inventory $ 15,600 $ 21,200 Accounts payable 32,400 27,400 Salaries payable 4,400 3,000 Accounts receivable 42,000 […]

Accounting Chapter 16 6 Assuming That This company Uses The Indirect Method

16–95 Answer: (1) Crockett Company Cash flows from operating activities: Net income $ 51,500 Adjustments to reconcile net income to net cash provided by operating activities: Increase in accounts receivable (32,000 ) Decrease in merchandise inventory 14,000 Decrease in prepaid […]

Accounting Chapter 16 4 Capital Excess Par Value retained Earnings total Equity total Liabilities

140. Describe the format of the statement of cash flows, including the reporting of significant noncash investing and financing activities. Answer: The statement of cash flows involves reporting cash receipts and cash payments organized into three categories: operating, financing, and […]

Accounting Chapter 16 3 Calculate The New Cash Provided used Operating Activities

16–41 110. The accountant for Robinson Company is preparing the company’s statement of cash flows for the fiscal year just ended. The following information is available: Retained earnings balance at the beginning of the year $156,000 Cash dividends declared for […]

Accounting Chapter 16 2 Cash flows from selling trading securities are usually reported

69. If a company borrows money from a bank, the interest paid on this loan should be reported on the statement of cash flows as a(n): A. Operating activity. B. Investing activity. C. Financing activity. D. Noncash investing and financing […]

Accounting Chapter 16 1 The statement of cash flows reports and proves the net change

Chapter 16 REPORTING THE STATEMENT OF CASH FLOWS 1. The primary purpose of the statement of cash flows is to report all major cash receipts (inflows) and cash payments (outflows) during a period. Answer: True Blooms: Remember AACSB: Communication AICPA […]

Accounting Chapter 15 5 This Document May Not Copied Scanned Duplicated

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 15 4 Year Year However Did Increase Its total Asset

Blooms: Understand AACSB: Analytic AICPA BB: Global AICPA FN: Measurement Difficulty: 2 Medium Learning Objective: 15-C3 Topic: Foreign Exchange Rates and Currency 143. Define the return on total assets and explain how it is used to measure a company’s financial […]

Accounting Chapter 15 3 Seamark Buys 300000 Eiders Five year Bonds Payable

Answer: A Blooms: Remember AACSB: Communication AICPA BB: Industry AICPA FN: Measurement Difficulty: 1 Easy Learning Objective: 15-P4 Topic: Accounting for Equity Securities with Significant Influence 107. Vans purchased 40,000 shares of Skechs common stock for $232,000. This represents 40% […]

Accounting Chapter 15 2 All of the following statements regarding equity securities are true

Blooms: Remember AACSB: Analytic AICPA BB: Industry AICPA FN: Measurement Difficulty: 1 Easy Learning Objective: 15-P1 Topic: Accounting for Trading Securities 63. All of the following statements regarding equity securities are true except: A. Equity securities should be recorded at […]

Accounting Chapter 15 1 Accounting For Trading Securities36 Trading Securities Are

Chapter 15 INVESTMENTS AND INTERNATIONAL OPERATIONS 1. Long-term investments are usually held as an investment of cash for use in current operations. Answer: False Blooms: Remember AACSB: Communication AICPA BB: Decision Making AICPA FN: Measurement Difficulty: 1 Easy Learning Objective: […]

Accounting Chapter 14 5 January Year And The second Annual Installment Payment

Plus Unamortized Premium on Bonds Payable ……………………………………………… 368,035 $5,368,035 (c) 6/30 Bond Interest Expense ($5,368,035 x 0.12 x ½) 322,082 Premium on Bonds Payable ($350,000 – $322,082) 27,918 Cash ($5,000,000 x 0.14 x ½) ………………….. 350,000 (d) 6/30 Bond Interest […]

Accounting Chapter 14 4 Hornet Corporation has a loan agreement that provides it with

148. Shin Company has a loan agreement that provides it with cash today, and the company must pay $25,000 4 years from today. Shin agrees to a 6% interest rate. The present value factor for 4 periods, 6% is 0.7921. […]

Accounting Chapter 14 3 Bonds That Are Made Payable Whoever Holds

14–41 113. A company issued 5-year, 7% bonds with a par value of $100,000. The market rate when the bonds were issued was 6.5%. The company received $101,137 cash for the bonds. Using the effective interest method, the amount of […]

Accounting Chapter 14 2 Bonds that mature at different dates with the result

67. The contract between the bond issuer and the bondholders, which identifies the rights and obligations of the parties, is called a(n): A. Debenture. B. Bond indenture. C. Mortgage. D. Installment note. E. Mortgage contract. Answer: B Blooms: Remember AACSB: […]

Accounting Chapter 14 1 Term bonds are scheduled for maturity on one specified date

Chapter 14 LONG-TERM LIABILITIES 1. The legal contract between the issuing corporation and the bondholders is called the bond indenture. Answer: True Blooms: Remember AACSB: Communication AICPA BB: Legal AICPA FN: Decision Making Difficulty: 1 Easy Learning Objective: 14-A1 Topic: […]