Management Information Systems, 13TH ED.

MANAGING THE DIGITAL FIRM

Kenneth C. Laudon ● Jane P. Laudon

continued

Learning Track 4: E-commerce Payment Systems

For the most part, existing payment mechanisms have been able to be adapted

to the online environment, albeit with some significant limitations that have

led to efforts to develop alternatives. In addition, new types of purchasing rela–

TABLE 5.7 Major Trends in E-Commerce Payments 2012–2013

•Paymentbycreditand/ordebitcardremainsthedominantformofonlinepay–

ment.

•PayPalremainsthemostpopularalternativepaymentmethodonline.

Chapter 10:E-Commerce:DigitalMarkets,DigitalGoods

Chapter 10 Learning Track 4 2

continued

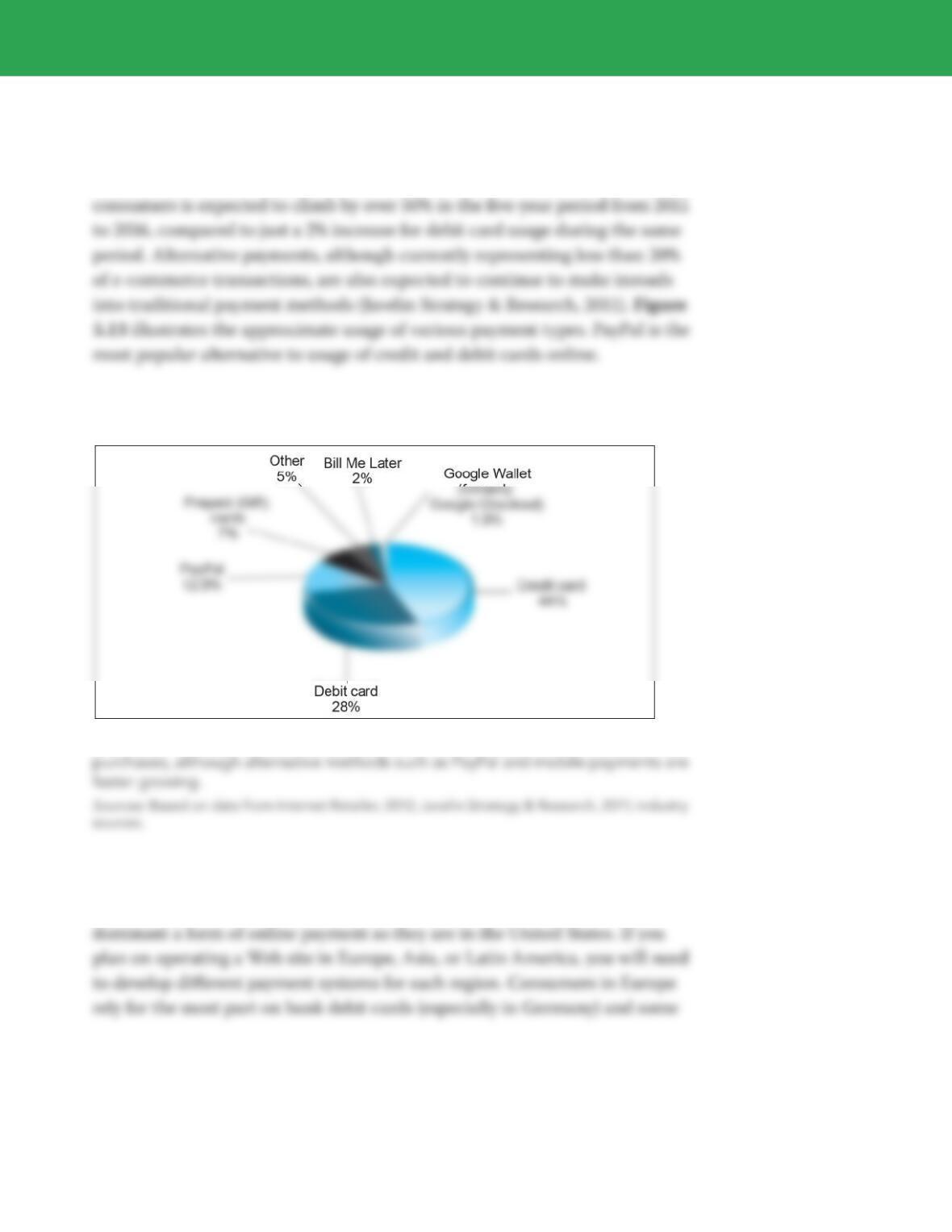

In the United States, the primary form of online payment is still the exist–

ing credit card system. Although credit card usage slipped somewhat during

the recession, the total payments volume for online use of credit cards by U.S.

FIGURE 5.13 Online Payment Methods in the United States

Traditional credit cards are still the dominant method of payment for online

In other parts of the world, e-commerce payments can be very different

depending on traditions and infrastructure. Credit cards are not nearly as

Chapter 10 Learning Track 4 3

continued

credit cards. Online purchases in China are typically paid for by check or cash

when the consumer picks up the goods at a local store. In Japan, consum-

ers use postal and bank transfers and CODs, using local convenience stores

ONLINECREDITCARDTRANSACTIONS

Because credit and debit cards are the dominant form of online payment, it

is important to understand how they work and to recognize the strengths

and weaknesses of this payment system. Online credit card transactions are

processed in much the same way that in-store purchases are, with the major

differences being that online merchants never see the actual card being

Figure 5.14 illustrates the online credit card purchasing cycle. ere are five

parties involved in an online credit card purchase: consumer, merchant, clear-

inghouse, merchant bank (sometimes called the “acquiring bank”), and the

consumer’s card–issuing bank. In order to accept payments by credit card,

Chapter 10 Learning Track 4 4

continued

FIGURE 5.14 How an Online Credit Card Transaction Works

As shown in Figure 5.14, an online credit card transaction begins with a

purchase (1). When a consumer wants to make a purchase, he or she adds the

item to the merchant’s shopping cart. When the consumer wants to pay for

the items in the shopping cart, a secure tunnel through the Internet is created

Credit Card E-commerce Enablers

Companies that have a merchant account still need to buy or build a means of

handling the online transaction; securing the merchant account is only step

Chapter 10 Learning Track 4 5

continued

one in a two-part process. Today, Internet payment service providers (some-

times referred to as payment gateways) can provide both a merchant account

and the software tools needed to process credit card purchases online.

Limitations of Online Credit Card Payment Systems

ere are a number of limitations to the existing credit card payment system.

e most important limitations involve security, merchant risk, administrative

and transaction costs, and social equity.

e existing system offers poor security. Neither the merchant nor the

consumer can be fully authenticated. e merchant could be a criminal orga-

nization designed to collect credit card numbers, and the consumer could

be a thief using stolen or fraudulent cards. e risk facing merchants is high:

Chapter 10 Learning Track 4 6

continued

ALTERNATIVEONLINEPAYMENTSYSTEMS

e limitations of the online credit card system have opened the way for

the development of a number of alternative online payment systems. Chief

among them is PayPal. PayPal (purchased by eBay in 2002) enables individu–

account. PayPal transfers the amount from your credit or checking account

to the merchant’s bank account. e beauty of PayPal is that no personal

credit information has to be shared among the users, and the service can be

used by individuals to pay one another even in small amounts. Issues with

PayPal include its high cost (in addition to paying the credit card fee of 3.5%,

PayPal tacks on a variable fee of from 1.5%–3% depending on the size of the

transaction) and its lack of consumer protections when a fraud occurs or a

charge is repudiated. PayPal is discussed in further depth in the case study

at the end of the chapter.

Bill Me Later also appeals to consumers to do not wish to enter their credit

card information online. Bill Me Later describes itself as an open-ended credit

account. Users select the Bill Me Later option at checkout and are asked to

provide their birth date and the last four digits of their social security number.

Chapter 10 Learning Track 4 7

ey are then billed for the purchase by Bill Me Later within 10 to 14 days. Bill

Me Later is currently offered by more than 1,000 online merchants.

Like Dwolla, Stripe is another company that is attempting to provide an alter–

native to the traditional online credit card system. Stripe focuses on the

merchant side of the process. It provides simple software code that enables

MOBILEPAYMENTSYSTEMS:YOURSMARTPHONEWALLET

e use of mobile devices as payment mechanisms is already well established

in Europe, Japan, and South Korea and is expanding rapidly in the United

States, where the infrastructure to support mobile payment is finally being

put in place, especially with the advent of smartphones equipped with near

NFC targets can be very simple forms such as tags, stickers, key fobs, or

readers. NFC peer–to-peer communication is possible where both devices

are powered. An NFC-equipped smartphone, for instance, can be swiped by

a merchant’s reader to record a payment wirelessly and without contact. In

September 2011, Google introduced Google Wallet, a mobile app designed to

work with NFC chips. Google Wallet currently works with the MasterCard

Chapter 10 Learning Track 4 8

continued

Android smartphones that are equipped with NFC chips, although, as of

In 2012, mobile retail purchases are expected to total around $11.6 billion.

e promise of riches beyond description to a firm that is able to dominate the

DIGITALCASHANDVIRTUALCURRENCIES

Although the terms digital cash and virtual currencies are often used synon–

ymously, they actually refer to two separate types of alternative payment

to as “mining,” that requires extensive computing power. Like real curren–

cy, Bitcoins have a uctuating value tied to open-market trading. Like cash,

Bitcoins are anonymous—they are exchanged via a 34-character alphanumer–

ic address that the user has, and do not require any other identifying informa-

tion. Bitcoins have recently attracted a lot of attention as a potential money

laundering tool for cybercriminals, and have also been plagued by security

issues, with some high-profile heists. For example, in September 2012, hackers

Chapter 10 Learning Track 4 9

virtual