Management Information Systems, 13TH ED.

MANAGING THE DIGITAL FIRM

Kenneth C. Laudon ● Jane P. Laudon

Learning Track 3: The Rise of Mobile Platform: M-commerce

In a few years, the primary means of accessing the Internet both in the U.S. and worldwide will

be through mobile devices like tablet and smartphone computers, and not traditional desktop or

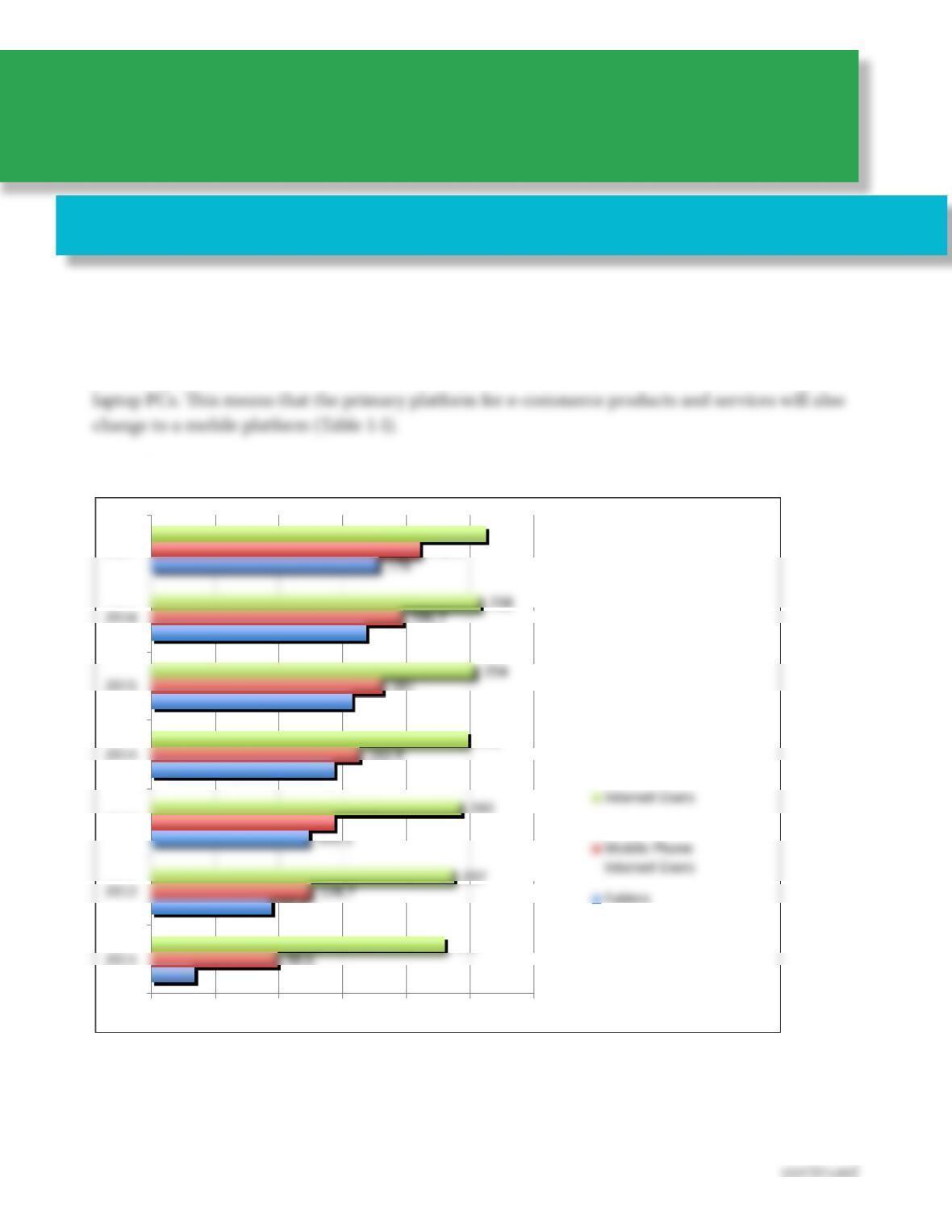

FIGURE 1.1 U.S. Internet and Mobile Internet Users, 2011-2017 (millions)

33.5

93.9

143.2

157.1

168.1

143.2

210.2

230

248

262

050 100 150 200 250 300

2013

2017

Mobile Internet—Smartphones and tablets are the fastest growing form of Internet access. Mobile

Internet users will be 45% of all Internet users in 2013, and grow to 64% by 2016.

Source: eMarketer, 2013

Chapter 1: Information Systems in Global Business Today

Chapter 1 Learning Track 3 2

continued

You can see this sea change in technology platform today whenever you travel and watch busi-

ness people peck away at their Blackberries in airports and train stations; kids in school text away

madly to their friends on cell phones, many using Twitter; high school and college kids are often

buried in games, movies, TV shows, emails, and text on their smartphones; and people on trains

e changing platform is a challenge for even the dominant Internet players. Google finds its

PC-based ad business must somehow shift to the mobile platform and make up for slowing growth

in its traditional search engine-based marketing engine. Apple struggles against the growing popu-

larity of cheaper Samsung Android phones, and tries to develop a mobile advertising platform

(iAd) to rival the leader in mobile ads (Google). Microsoft and Intel both struggle to develop mobile

FIGURE 1.2 Internet, Mobile, and Tablet Users Penetration (% of Internet Users)

0.00% 20.00% 40.00% 60.00% 80.00% 100.00%

2016

2017

Internet % Population

While PCs are expected to remain the largest % of Internet users by 2017, table and phone Internet

access is expected to grow much faster and nearly equal the penetration of PCs.

Source: eMarketer, 2013

Chapter 1 Learning Track 3 3

continued

Mobile Is Global

e rapid growth of the mobile Internet platform is a global phenomenon, and not just a U.S.

phenomenon. Figure 1.3 illustrates the changing global Internet platform.

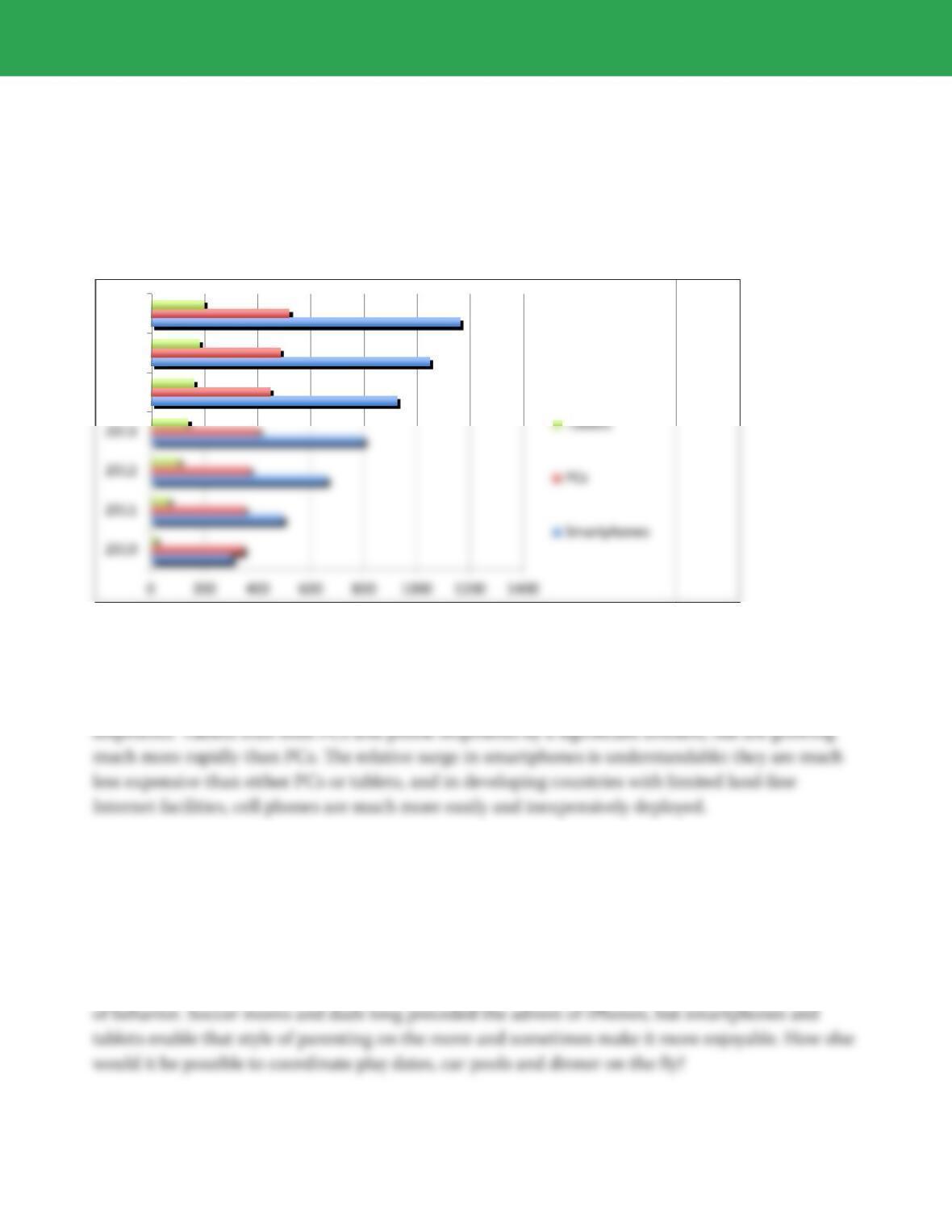

FIGURE 1-3 Global PC, Smartphone and Tablet Shipments, 2010–2016

2014

2015

2016

Source: IDC, 2012

In 2013, 800 million smartphones were shipped worldwide, while only 400 million PCs were

shipped. By 2016, the gap will increase to 1.1 million phone shipments and only 520 million PC

It Isn’t Just the Technology: Changes in Consumer and

Corporate Behavior

While the emerging mobile digital platform is certainly a hardware event, it also involves changes

in software, as well as changes in our society and culture which sometimes drive the technology in

certain directions, and in other cases are driven by the technology to enable and support new kinds

Chapter 1 Learning Track 3 4

continued

In 2013 the U.S. labor force has about 155 million workers. Cellular industry experts believe about

60% of the US labor force uses mobile devices as a part of their jobs. Half of the federal labor force

uses mobile devices at work. e new mobile workforce is composed of full and part–time knowl-

edge workers who can work at home, at a coffee shop, airport or on a train; extended day workers

The Mobile Platform: Technology

Smartphones are a disruptive technology which radically alters the personal computing and

e-commerce landscape. Smartphones involve a major shift in computer processors, and software

that is disrupting the forty year dual monopolies established by Intel Corporation and Microsoft,

whose chips, operating systems and software applications have dominated the PC market since

1982. Virtually no cell phones use Intel chips, which power 90% of the worlds PCs; Only 12% of

Smart phones use Microsoft’s operating systems and that’s mostly in Asia (Windows mobile).

continued

milliwatts at idle, and 1 watt writing and reading, ash memory chips consume about 50 milliwatts

writing and reading data (twenty times less power).

Powerful, energy ecient client devices are only one-half of the emerging digital platform. Without

second and third generation cellular networks, and Wi-Fi wireless local networks, mobile plat–

forms enabling computing anywhere and anytime would be impossible. By 2013 there will be 143

Mobile Commerce

Up until the introduction of the Apple iPhone smartphone in 2007, and the development of iTunes

store where millions of iPod and iPhone users could download songs, mobile e-commerce in

the United States was more of a dream than a reality. In Asia and northern Europe (particularly

Finland and Sweden) mobile payment systems were developed for cell phones in 2000, but there

Chapter 1 Learning Track 3 6

continued

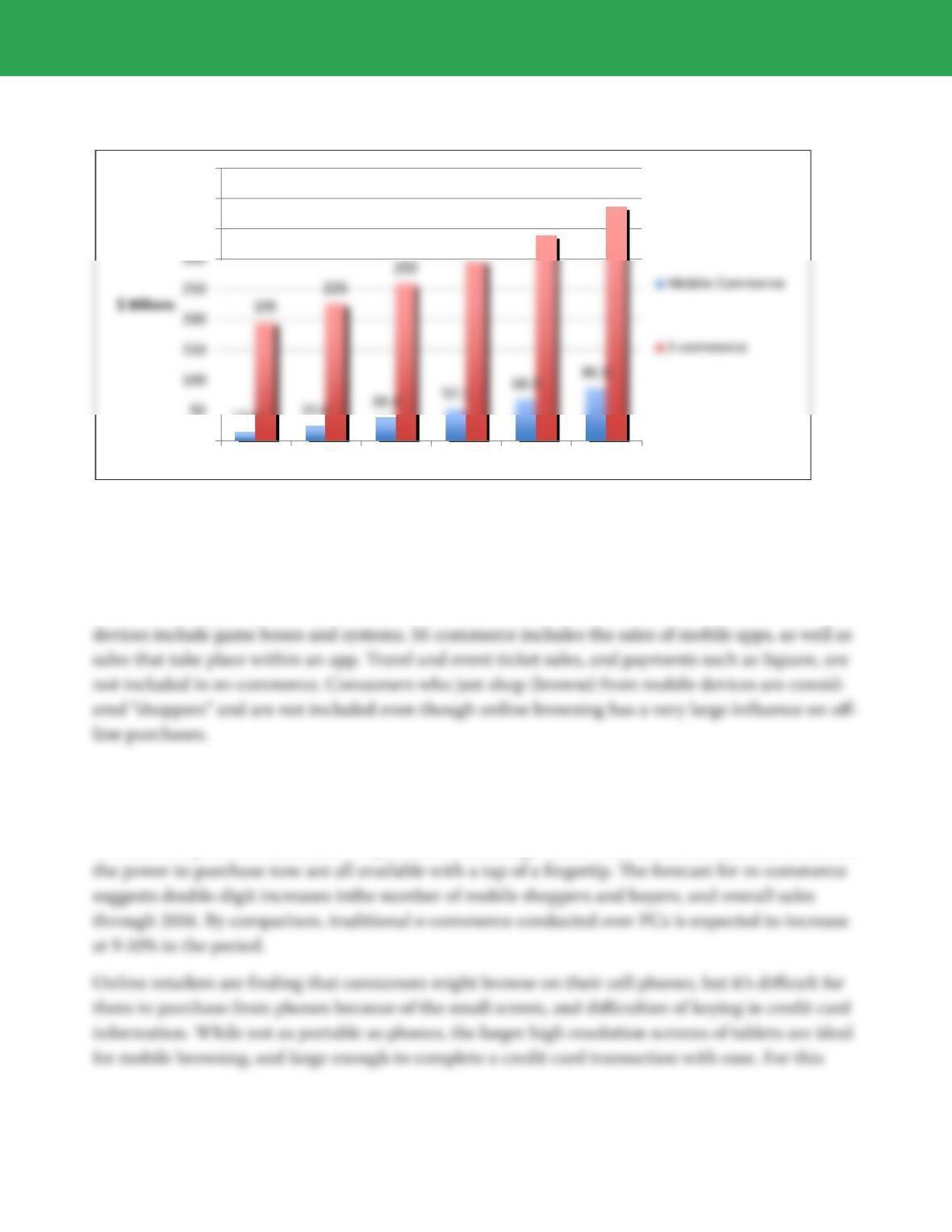

FIGURE 1.4 M-commerce and E-commerce, 2011-2016

13.6 24.6 38.4 52.1 68.3 86.9

296

338

385

0

350

400

450

2011 2012 2013 2014 2015 2016

Source: eMarketer, 2013

It is important to understand what is meant by “m-commerce” and “e-commerce” sales.

E-commerce and m-commerce sales include the buying of physical goods and services using

a browser or app on a mobile phone, tablet, e-reader, or other handheld device. Other kinds of

Mobile commerce is growing so rapidly in part because it gives consumers the ability to access

information now, buy it now, and pay for it now. Because mobile phones are usually always on, and

usually attached to the consumer, they provide to access instant coupons, deals, and ash sales, all

of which are powerful motivators to purchase something. Product information, deals and sales, and

Chapter 1 Learning Track 3 7

continued

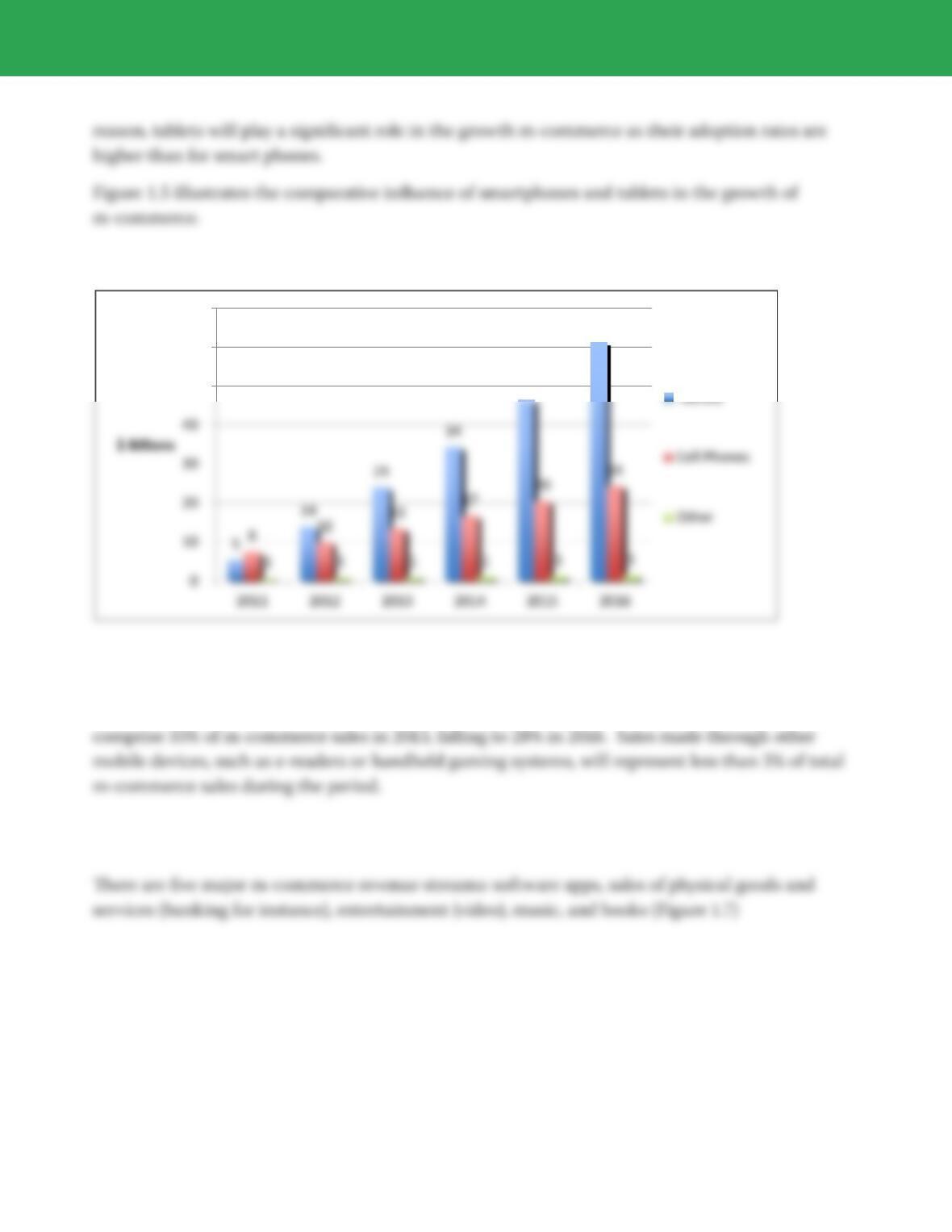

FIGURE 1.5 M-commerce Sales by Device

46

61

50

60

70

Retail purchases made through tablets are expected to comprise 70% of m-commerce sales in

2016, up from 62% in 2013. Smartphone sales are expected to grow at double-digit rates and

M-Commerce: Where’s the Money?

Chapter 1 Learning Track 3 8

continued

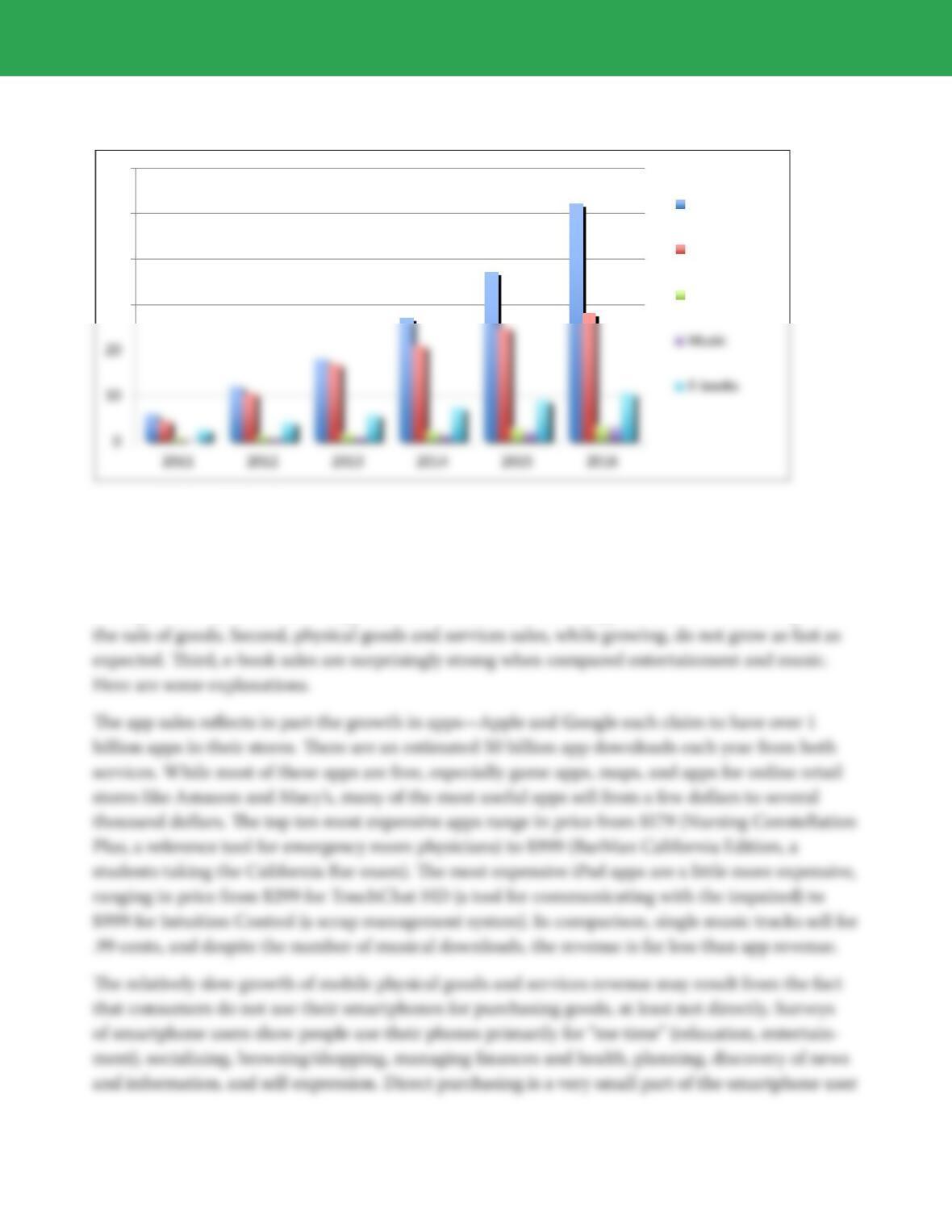

FIGURE 1.7 Sources of M-commerce Revenues

30

40

50

60

Apps

Goods

Entertainment

Sources: eMarketer, 2013; author estimates

ere are several surprises in Figure 1.7. e sales of apps on both Apple and Android devices is

larger than sales of goods in 2013, and is expected to grow faster than all other mobile revenues

through 2016. By 2016, sales of apps and sales of services within apps is almost twice as large as

Chapter 1 Learning Track 3 9

continued

mobile time. ere’s also the “fat finger” problem: purchasing on a 3.5” square screen is dicult,

mistakes are common, and clicking on tiny mobile ads is just no fun and often is just a mistake as

the user is trying to accomplish something else. While direct phone sales are very small, browsing

Figure 1.8 illustrates how consumers actually use their smartphones as indicated by the kinds of

apps they are downloading.

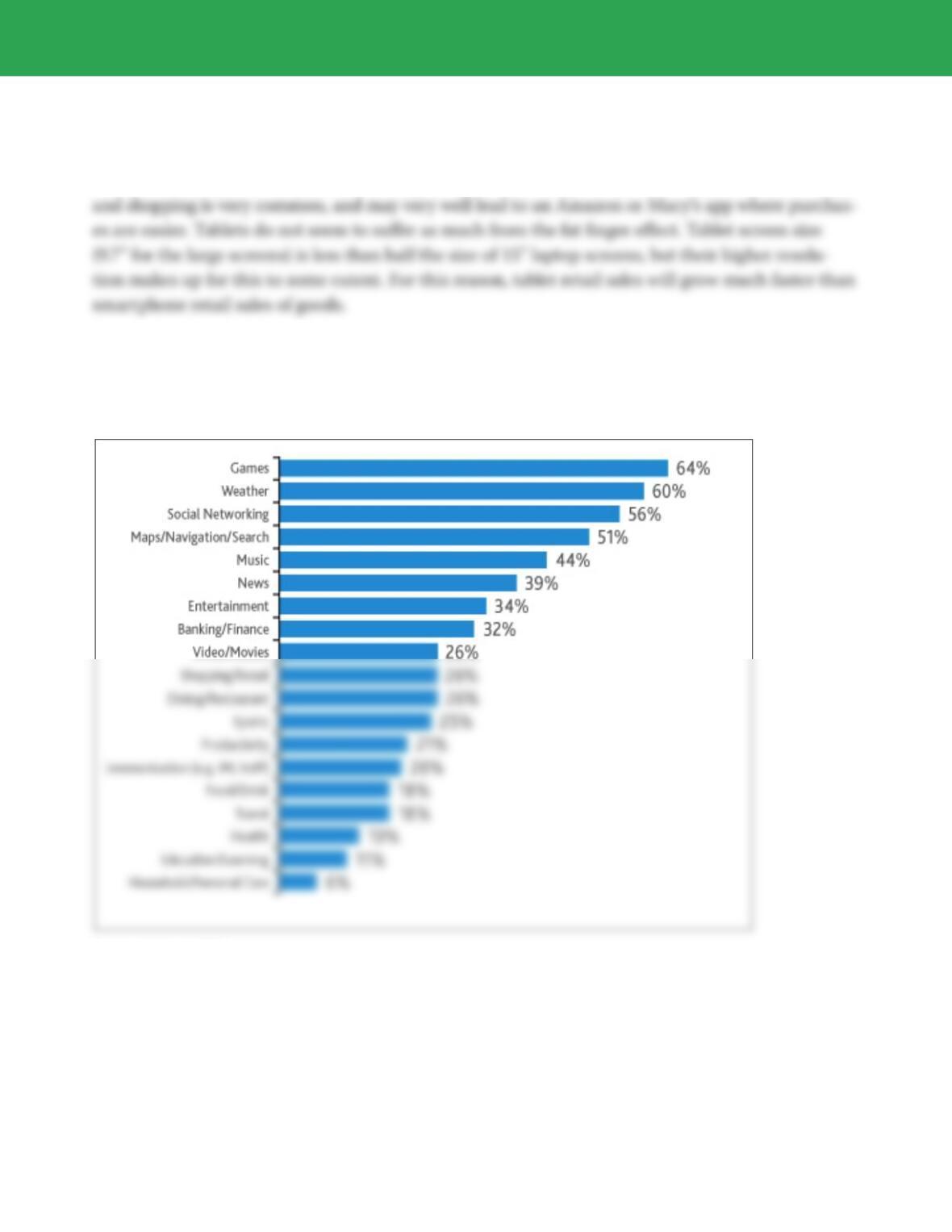

FIGURE 1.8 The Apps Consumers Use

Source: Nielsen, 2011

Purchasing goods and services, as opposed to informing and socializing activties, is not high on

the list of apps that are downloaded. Only 26% of smartphone users download shopping/retail

apps, and actual purchasing is not that common (as opposed to shopping).

Chapter 1 Learning Track 3 10

A final surprise in Figure 1.7 concerns the strength of mobile eBook sales which are expected to

grow faster than entertainment revenues (TV and video). In part this is due to the extraordinary

success of the Amazon Kindle devices which are both low in cost, and adequate for browsing the

Web (Kindle Fire). Small smartphone screens are adequate for books, and large tablet screens are

The Mobile Platform Transforms Online Advertising

So far we’ve discussed how the mobile platform is changing e-commerce in terms of sales of goods

and services. e mobile platform is also having a powerful impact on the marketing and advertis-

ing industry. Marketers have to go where consumers go, and increasingly, this means going mobile.

E-commerce marketers, retailers, and service vendors are discovering that smartphones repre–

sent a new channel for selling and paying for goods and services, the so-called “fourth screen”

(Hollywood movies, television, and personal computers being the first three screens).

Chapter 1 Learning Track 3 11

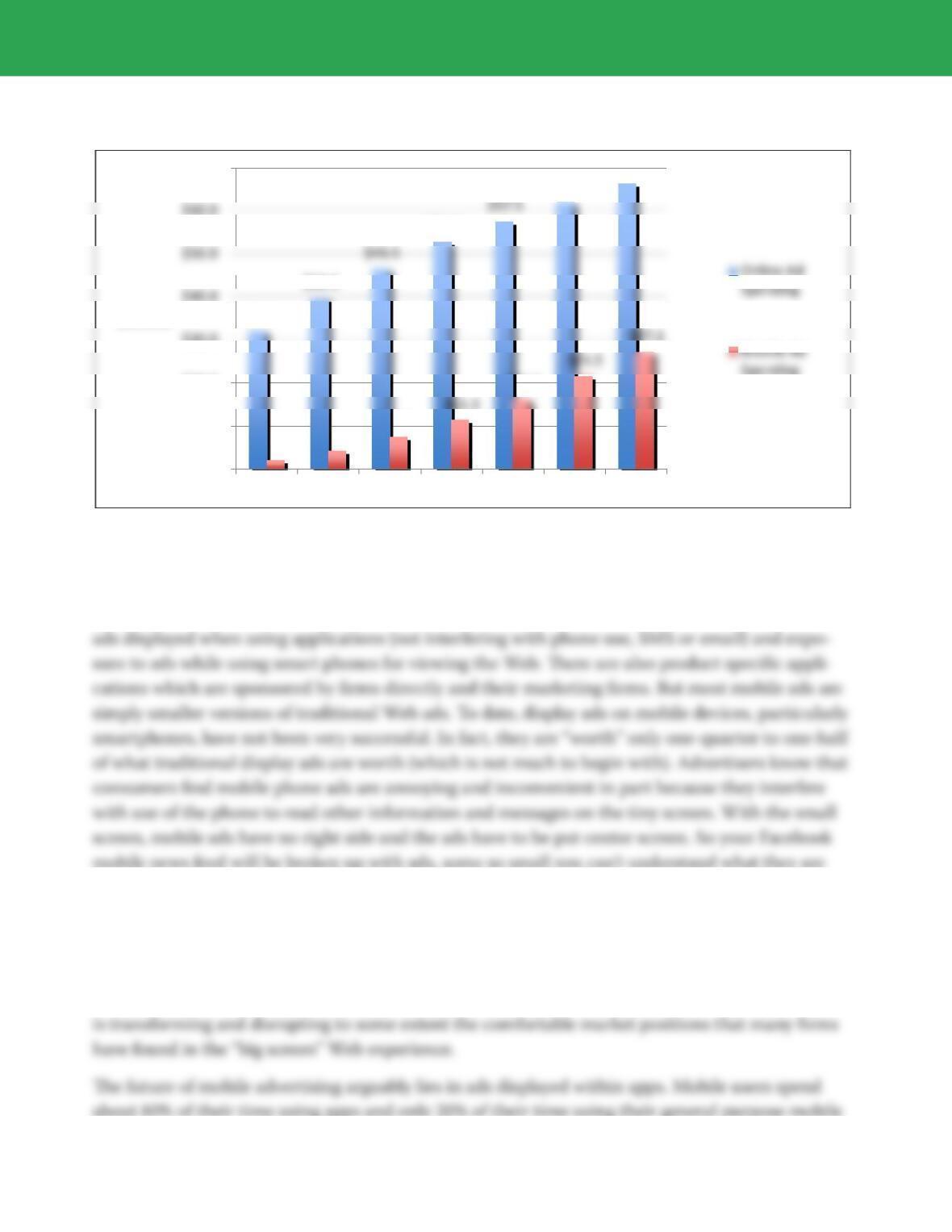

FIGURE 1-5 U.S. Mobile Ad Spending 2011-2017 (millions)

$32.0

$39.5

$52.8

$62.0

$66.3

$2.0 $4.1 $7.3

$16.2

$-

$10.0

$20.0

$30.0

$70.0

2011 2012 2013 2014 2015 2016 2017

$Billions

Mobile Internet advertising is the fastest growing online ad channel.

Source: eMarketer, 2012

Mobile ads come in all the same formats as traditional online Web ads. Examples include banner

selling.

e low value and utility of mobile ads poses a threat to Google, Facebook, and Amazon, and

most other online marketing and advertising firms. As users turn away from their traditional large

screen Web screens, and switch to mobile devices, ad revenues decline because the ads just don’t

work as well driving customers to shop and purchase products. Once again, the mobile platform

Chapter 1 Learning Track 3 12

browsers. e biggest revenue generating apps for advertising will be games and entertainment

(art 42% of user time, it’s the largest time segment for mobile users), social networks (mostly

Facebook, 32% of mobile user time), utilities (maps, text, photo sites), discovery and shopping

(Yelp, TripAdvisor, Instagram), and brands (like Amazon, Nike, Coke, and scores of others). In-app