P

rofessors Kenneth A. Merchant and Wim A. Van der Stede wrote this teaching note as an aid to instructors using the Houston

F

earless 76, Inc. case.

Marshall School of Business

University of Southern California

Houston Fearless 76, Inc.

Teaching Note

Purpose of Case

This case describes a sales incentive system based on a traditional commission payout and a

proposal for change. The proposal raises a number of issues regarding performance

Suggested Assignment Questions

1. Why are Houston Fearless 76, Inc. (HF76) managers unhappy with the companys existing

sales incentive plan? Are weaknesses in this plan a major cause of the companys

performance problems?

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

107

Case Analysis

What does HF76 want from its salespeople?

Before getting into a discussion of the old and new sales incentive plans, it is useful to have the

students clarify the companys markets and to identify the behaviors that HF76 managers would

ideally like from their salespeople. HF76 is organized into four business units: HF International,

Extek, Mekel, and Pollution Control Systems.

a. HF International (photo processing)

Mature market

b. Extek (micrographics)

Mature market

c. Mekel (scanners)

More high tech, more growth potential

d. Pollution control systems

Only one sale to date

What does HF76 want its salespeople to do?

Provide good service to existing customers. This is particularly important in the mature

markets.

What should be the goals of the sales incentive system?

Motivation (stimulate effort)

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

108

What are the key elements of the existing sales incentive plan?

What are the problems currently being faced?

Dealers and sales reps do not share customer lists.

Salespeople are not developing new customers. Most of them merely respond to inquiries.

Sales people are spread all over the country. The VP-Sales is in Atlanta. The organization is

hard to control/monitor.

The sales people have not received performance evaluations recently, or raises.

What are the key elements of the proposed incentive plan?

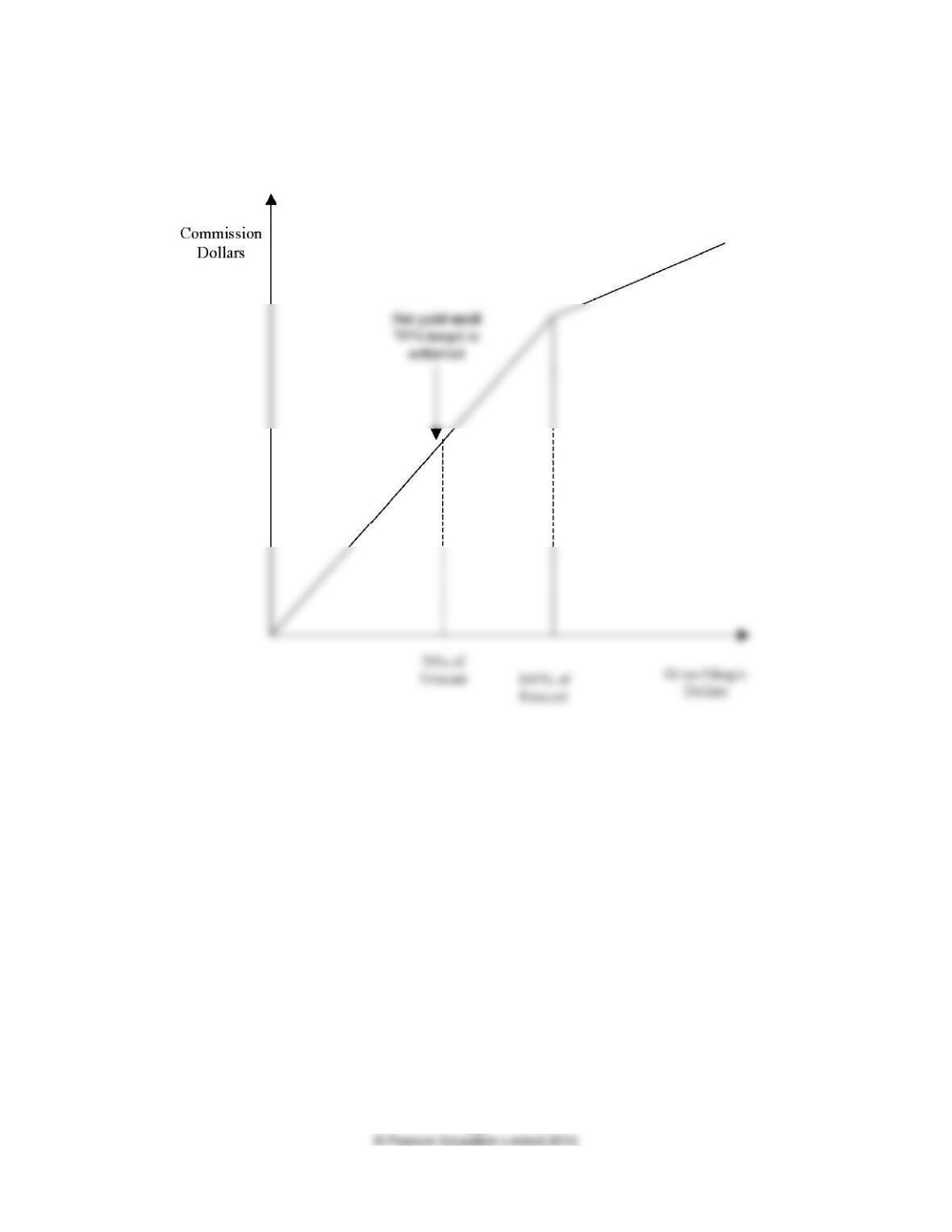

See Figure TN-1.

It is useful to clarify the shape of the performance/reward function. The slope of the payout

function in the existing system was 24% of sales. The slope of the function in the proposed

These slopes can be illustrated with a hypothetical example. Here is one that can be used:

Assume a high margin sale = 30% GM

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

109

Under the old plan

Commission on the one sale = $2,000

Under the new plan

At 70% of plan ($1.12M in sales): Company GM = $336,000

Salesman commission = 0

Evaluation

Students should be asked to evaluate the plan and to provide recommendations for

improvement. There are a lot of issues that can be discussed. Students will raise most of the

obvious measurement and calibration issues. A good student report on this case is appended to

this teaching note.

Here are some other questions that can be posed if they do not come up naturally:

How should HF76 provide incentives to sell products that are sold at a negative gross

margin? HF76 had a number of these products, which managers wanted to keep selling for

customer access and service reasons. This is a difficult issue that HF76 managers had not

solved. Any number of approaches could have been used, such as guaranteeing the sales

force a minimum gross margin percentage on each sale.

Other, perhaps more peripheral, questions that can be posed, time allowing:

Should anything have been done with the incentives for the sales assistants?

This aspect of the plan does not seem to have any motivational value. On the other hand, it

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

110

Should HF76s managers have been satisfied with measuring and providing rewards for

profits on sales down only to the gross margin line, rather than down to a bottom-line

product profit figure?

The sales people do not control much below the gross margin line (only their selling

What the Company Did

The company presented the proposed plan to the sales force and met with unanimous and strong

objections. The top managers decided that the change was too radical, so they backed off on

their plan to make the change. Instead they modified their old plan. They left the old

commission plan in place, but they added three extra rewards. One was an extra bonus of 5% of

salary if total year-end sales were within plus or minus 10% of the sales forecast. The second

Pedagogy

This case contains a lot of issues that can be discussed. Thus the instructor will have to provide

some structure to the discussion to ensure coverage of the issues deemed most important. The

discussion above presents one possible structure. If that structure is used, the class timing could

be approximately as follows:

2. The existing incentive plan 5 ”

4. The proposed incentive plan 15 ”

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

Figure TN-1

Key Features of the Existing and Proposed Sales Incentive Plans

Existing Plan Proposed Plan

Who is included in the plan? Salespeople Salespeople

Form of payment? Cash Cash

Frequency of payment? Monthly Annual award, but monthly

advances at 80% rate

Measures and weighting? Sales (100%)

Product gross margins (83%)

P

rofessors Kenneth

A

. Merchant and Wim A. Van der Stede wrote this teaching note as an aid to instructors using the Houston

F

earless 76, Inc. case.

Marshall School of Business

University of Southern California

A201-02

Houston Fearless 76, Inc. (A): Aftermath

On November 25, 2000, James Lee proposed the new plan in the annual sales meeting. All

salespeople voted against the plan, particularly the idea of replacing the sales-based commission

plan with a profit-based bonus plan. Here are some quotes from salespeople:

I understand that firms need to generate profitable sales and cash inflow. However, why

should we salespeople be held accountable for profitability? If the product is

unprofitable, that was caused by top managements pricing decision, or their decision to

keep the product offering.

..

Historically, HF76 has not had a good cost accounting system that could track

accurately the costs incurred to make a specific product. How can I trust that the profit

number is correct for the products I have sold?

..

We all understand that, from an operations perspective, more accurate forecasts are

always preferred. But given the nature of capital products, accurate forecasts are

difficult even if you work with customers closely. You know sales are going to happen

However, the new compensation plan provided extra rewards, on top of the existing

commission structure, in the following ways. First, salespeople could earn 5% of their salary if

total year-end sales were within plus or minus 10% of sales forecast. Second, salespeople would

earn an extra 3% of salary if they achieved each of the goals in a set of MBO targets negotiated

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

113

About the new plan, James Lee explained:

This is the first step in moving our sales force to even think about other objectives beyond

sales. HF76 has always had the culture to make sales, even if it meant selling at a loss. This

However, James also realized that his attempt to revamp the sales incentive system based on his

original idea was largely unsuccessful. He reflected:

The fate of the new plan is not totally unexpected, although it is disappointing. I noticed that

the sales personnel were against the new plan from the very beginning of our meeting.

There are some good reasons for their opposition. For example, moving toward a profit-

based incentive system would require a relatively accurate cost system, and we do not have

J

ames Lee, an Executive MBA graduate, and Professor Larry Greiner wrote this case as a basis for class discussion rather than to

illustrate either effective or ineffective handling of an administrative situation.

Marshall School of Business

University of Southern California

A202-01

Houston Fearless 76, Inc. (B)

In January, 2002, M.S. Lee, President/CEO of Houston Fearless76, Inc. (HF76), expressed some

optimism about the changes that had occurred in the company:

We used to have overly optimistic sales forecasts, but now I feel they are more realistic.

accomplished.

On August 13, 2001, HF76 and Fuji Photo Film USA, Inc. (Fujifilm) announced that HF76

obtained an exclusive distribution agreement for Fujifilms micrographics products for the US

and Canadian markets. Ken Kopald, then Vice-President and General Manager of Fujifilm

USAs document products division also announced that he will be leaving Fujifilm after 29

lists from Fujifilm and HF76.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

115

Ken Kopald built from scratch his sales and service organization at Fujifilm USA, which grew

The plan is relatively simple but communicates much more than just a base salary and

flat rate commission. Also, our former Fujifilm sales staff was already used to a similar

plan at Fujifilm. And, we can shape direction by boosting commissions for the more

profitable products such as scanners and duplicators. We also weighted the

Company Performance

As of late January, financial statements for 2001 were not available from the Accounting

Department. Sales performance for recent years and projections through 2003 are provided in

Exhibit 1.

Growth Challenges

The number of sales transactions has increased tenfold and several departments have

experienced growing pains. Before ASI, HF76 would process 510 orders per day for spare

parts or custom-built equipment. Now, HF76 is receiving 4070 orders per day for film and

photochemicals our customers typically want the next day. M.S. Lee remarked, We have

changed from a manufacturing company to a distribution company overnight. Several other

areas need to change, too.

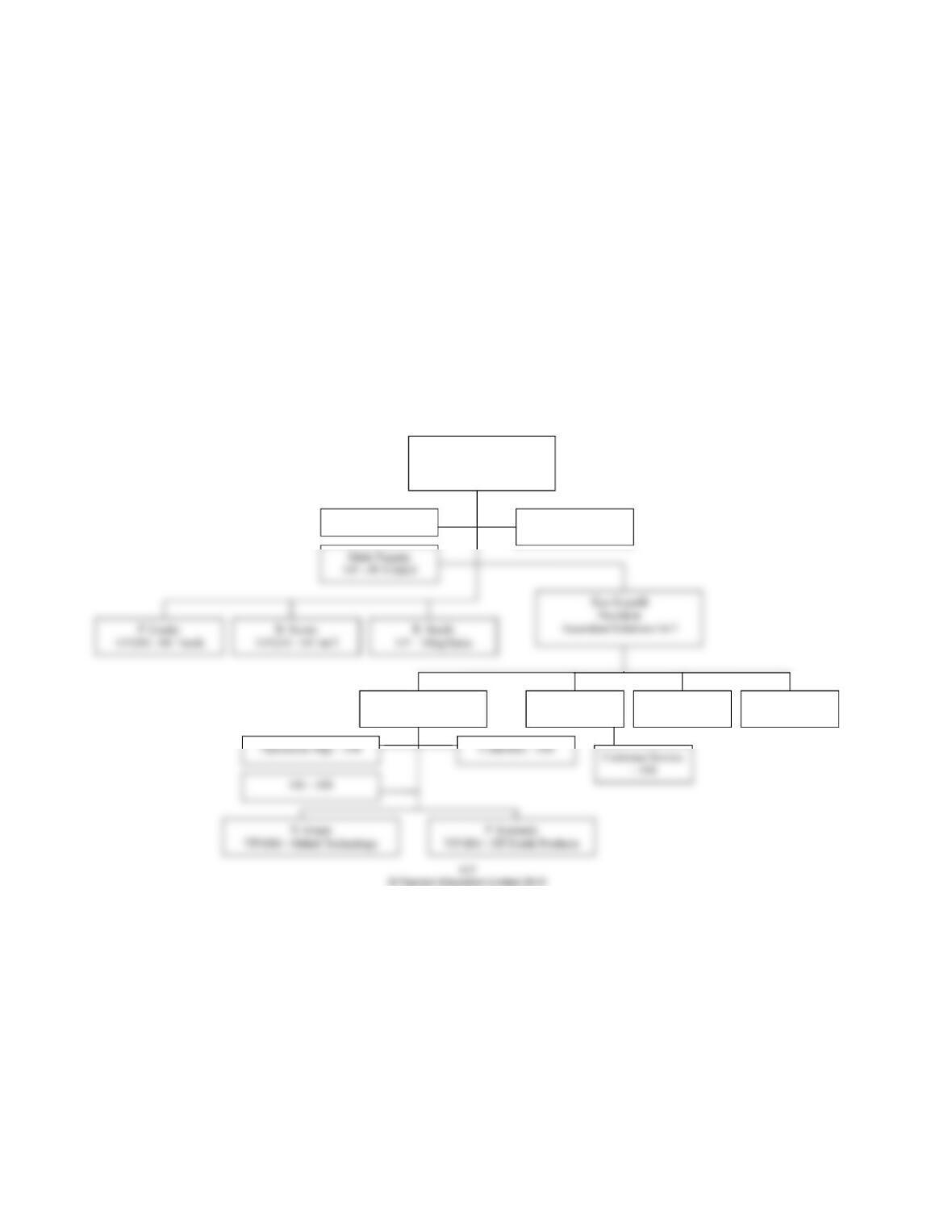

A New Organization

A new organization (Exhibit 2) was being contemplated by M.S. Lee. We have all this good

Exhibit 1

Houston Fearless 76, Inc.

Sales History

2000 2001 2002 2003

(Actual) % (Estimated) % (Forecast) % (Forecast) %

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

Exhibit 2

Proposed Reorganization – 2002

Houston Fearless 76, Inc.

M.S. Lee

Chairman/CEO

HF76

Corp HR/Security S. McLaren

CFO

J. Lee

VP Operations – ASI

VP Marketing –

ASI

Regional Field

Sales – ASI

Tech Support –

ASI

P

rofessors Kenneth A. Merchant and Wim A. Van der Stede prepared this teaching note addendum as an aid to instructors using the

H

ouston Fearless 76, Inc. case.

Marshall School of Business

University of Southern California

Houston Fearless 76, Inc.

Teaching Note

Addendum: Student Exam Assignment and Report

Below is one relatively representative example of a student analysis of the Houston Fearless 76,

Exam Rules

1. Next weeks midterm exam will be take-home. It will consist of a case similar to the cases

2. The exam can be done individually or in groups of up to three people. Groups will have to

monitor and manage themselves. All members of the group will receive the same grade on

3. Case reports (individual or one per group of three students maximum) must be e-mailed to

4. I will not answer any questions regarding the exam to avoid (perceptions of) unfair

5. Please make a comprehensive analysis to support your answers to the assignment questions,

6. If you cannot comply with the exam deadline or any other exam rule spelled out above, you

need to contact me as soon as possible, but certainly before I post the exam. I will maintain

a tough stance toward exceptions, such as a request for an extension of the exam deadline,

for the following reasons:

a) This is a take-home, open-book, open-note, open-everything exam.

b) You have two days (48 hours) to complete the exam.

Assignment Questions

Case Background

The Houston Fearless 76, Inc. (HF76) case study discusses a proposal for change in a sales

incentive program. The new program is interesting for a number of reasons, including a

proposed shift toward rewarding the generation of profits (actually gross margins), rather than

just sales, and a truth-inducing forecast incentive feature.

Case Questions

[Q1 = 30 points / Q2 = 30 points / Q3 = 30 points / Q4 = 10 points]

1. Evaluate the old incentive plan as well as the new incentive plan being contemplated. Are

there any significant impediments to the successful implementation of the new incentive

plan? Which?

2. Should HF76s managers have been satisfied with measuring and rewarding profits on sales

down only to the gross margin line, rather than down to a bottom-line product profit

figure? (More generally, discuss the issues associated with incentives placed on sales, gross

3. What modifications would you make to the proposed new plan, if any? Formulate specific

4. Would you make any changes to the system providing bonuses to sales assistants? Which?

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

120

Student Report

Current Situation

Houston Fearless 76 (HF76) manufactures and sells products for several different markets, in-

cluding photo processing, micrographics and motion picture processing, scanner products, and

most recently, pollution control systems. The company has products in varying stages of the life

cycle. M.S. Lee intends to increase sales and profitability in each market through strategies

based on its corresponding life-cycle stage.

HF76 is currently experiencing several problems. Sales of its products have slowed. Although

this trend is in part due to market conditions, M.S. Lee believes the company is not doing

enough to develop new markets, to expand [its] existing markets, or to develop synergies among

[its] markets. In addition, the companys managers believe that HF76s performance is

lacking behind that of its major competitors on all dimensions. HF76 is also encountering

production-planning problems, which are linked to problems in forecast accuracy. Production

M.S. Lee believes that many of the companys troubles are related to the present sales force in-

centive system. This system provides a base salary of $40,000 to $60,000 and a commission as a

percentage of sales on products shipped within a salespersons assigned territory. The

Proposed Incentive Plan

HF76s new incentive plan is an attempt to re-align the sales forces goals to address problems

that HF76 is encountering. M.S. Lee had previously communicated to the sales force which

products were the most profitable; however, this communication has had no impact on

behavior. The new system is designed to translate that message into financial terms. In an effort

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

121

The proposed system presents several problems. The change from commissions based on sales

to commissions based on gross margins has several inconsistencies. First, the percentage of

gross margin paid ranges from 1012% on high margin sales to 3035% on low margin sales.

This range in percentage paid seems to negate the effect it is supposed to create. In order to

induce salespeople to sell higher margin products, the rate paid on those margins should be

constant. On the other hand, if the plan is structured in this way out of fairness, in that different

The system also does not solve the forecasting problem. The 70% floor now encourages

sandbagging as opposed to optimistic forecasting. The increase in commission rate paid beyond

100% has the same effect. It seems that while there is some disincentive over the sale of the

marginal unit that pushes a salesman over the 110% threshold, that disincentive is more than

compensated for by the increase in commission rate paid for sales in that range. The plan will

induce salespersons to provide artificially low forecasts, and their subsequent compensation will

be well beyond what was intended. Absent a more effective forecasting approach, this new

compensation system will not be effective in alleviating the forecasting problems of the past.

There are also problems with MBO targets. The advantages to these targets are that they can be

tailor-made by M.S. Lee to address specific concerns that he has about his sales force. The

major impediment is the lack of communicability of the MBO targets. Salespeople often

prefer clearly defined compensation plans; incentives such as the percentage of sales are easy to

understand.

Sales vs. Gross Margins vs. Net Profits

The new compensation plan pays commissions on gross margins instead of net profits or sales.

This results in salespeople being measured by sales and also production cost. Many organization

measure salespeople performance as revenue centers and measure performance based on sales.

Sales personnel are responsible for making the sales and not for production. However, HF76 is

different since it is selling low volume and expensive capital equipment. Production is often

tailored to a specific sale that a salesperson makes. Therefore, it is important for salespeople to

consider production issues when making a sale.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

122

margin measures require a good communication flow between sales and production so that

production schedules will be efficient. However, it is important that production managers are

held accountable for production costs (i.e., by making them cost center managers). The

Recommendations

On the basis of the above discussion of the HF76 proposed compensation plan, we recommend

that changes be made to the plan in order to improve its effectiveness. The following paragraphs

discuss the changes that should help the compensation plan align the objectives of the company

with the actions of the employees. However, we recognize that these changes do not provide a

panacea to solving all compensation plan problems.

As mentioned, the proposed new plan does not jive with managements objective to increase

sales of high margin products. These margin percentages should be adjusted as previously

described. This does not, however, solve the issue of how to deal with low or negative margin

products. These products are important not for the profits they generate today but the potential

We have also determined that the 5% bonus is not significant enough to be effective in

encouraging accurate sales forecasting. However, we do not recommend an increase in such a

bonus as we disagree with it in principle. Since management wants accurate sales forecast but

does not want to deter sales growth, the forecast-accuracy bonus should be eliminated. We do

not recommend a direct penalty (loss of bonus) for sales beyond a target measure. Such a

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

123

sandbagging, it does not reward them. Also, even though the decrease in payout percentage

beyond the 100% mark may encourage myopic behavior, such as sales postponement, it will do

so to a lesser degree than would a flat cap on commissions. This structure is our best

compromise for balancing goals that are sometimes in conflict.

We also recommend that management become more involved in the forecasting process. In

general, forecasting (which provides the basis for budgeting) should remain a bottom-up

process. The salespeople should be required to fully explain and document their forecasts. They

Sales Assistants

The final aspect of the new compensation plan that needs to be modified is the bonuses for sales

assistants. Sales assistants provide administrative support for the sales people. Although they

provide value to the company, sales assistants are not directly responsible for sales, gross

margins, or even corporate performance. There is no link between the bonus and the

performance of sales assistants. The case provides an example of a sales assistant, Eva Colton,

who received a bonus. She neither expected nor understood why she received the bonus. This

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

124

Exhibit 1

Recommended Compensation Structure