473

This note was prepared by Professor Robert S. Kaplan for the sole purpose of aiding classroom instructors in the use of Boston

L

yric Opera, HBS No. 101-111. It provides analysis and questions that are intended to present alternative approaches to

deepening students comprehension of business issues and energizing classroom discussion. HBS cases are developed solely as the

basis for class discussion. Cases are not intended to serve as endorsements, sources of primary data, or illustrations of effective o

r

ineffective management.

5-102-074

APRIL 8, 2002

Boston Lyric Opera

TEACHING NOTE

Pedagogical Objective

The Boston Lyric Opera case, the first documented application of the Balanced Scorecard to

an arts organization, was written to illustrate the application of the Balanced Scorecard to a

nonprofit organization, especially one whose performance some people believe can not be

quantified and measured. The case provides the history of the arts organization and describes its

The case includes the BLO strategy map and asks students to suggest and debate the measures

for the scorecards strategic objectives, particularly its customer perspective. Once the class sees

that plausible measures can be created for BLOs strategic objectives, it can discuss the benefits

and challenges the BLO faces from use of the scorecard. Students can also discuss the

implementation approach used by the BLO, and the management system that the general

director is using to imbed the scorecard philosophy into the organization.

The case was first taught in executive programs on managing and governing nonprofit

organizations, and in a second-year MBA elective on social enterprises. We have also used it

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

Reading

A great deal of reading is available for preparatory reading. The challenge is choosing from

among the many options to keep the students reading load manageable. For historical purposes,

one could use the original article that introduced the Balanced Scorecard concept:

Kaplan, R.S., and D.P. Norton, The Balanced Scorecard: Measures that Drive Performance,

Harvard Business Review (January-February 1992): 7179, HBR 92105.

This article, however, does not describe the explicit link of the BSC to strategy and use of

strategy maps. One could supplement this original article with a later article that does describe

the role of strategy and use of strategy maps:

Kaplan, R.S., and D.P. Norton, Having Trouble with Your Strategy? Then Map It, Harvard

Business Review (September-October 2000): 167176, HBR 00509.

I recommend, however, using the following article:

Kaplan, R.S., and D.P. Norton, Transforming the Balanced Scorecard from Performance

Measurement to Strategic Management: Part I, Accounting Horizons (March 2001):

87104.

This article provides a historical context for why the Balanced Scorecard became more

important in the 1990s (growth of intangible assets), discusses each of the four BSC

In the interests of full disclosure, I note an explicit article on applying the BSC to nonprofit

organizations:

Kaplan, R.S., Strategic Performance Measurement and Management in Nonprofit

Organizations, Nonprofit Management and Leadership (Spring 2001): 353370.

This paper describes several nonprofit examples and some specific issues and challenges that

arise when implementing the BSC in nonprofit organizations. Unfortunately, the journals

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

475

Assignment Questions

1. The Boston Lyric Opera working group has selected eight customer objectives for its three

strategic themes (see bulleted items on pages 57 of the case, also summarized in the

Customer row of Exhibit 5):

Develop loyal and generous supporters

What measures should the project team select for these eight objectives?

2. What changes were required to adapt the Balanced Scorecard to a nonprofit organization?

3. What are the benefits from developing the Balanced Scorecard at BLO? What challenges

and barriers must Del Sesto and Dahling-Sullivan overcome to capture these benefits?

5. Is Janice Del Sesto using the Balanced Scorecard as a performance measurement system or

a management system?

6. Comment on the process that the BLO used to develop the BSC. What was critical for the

success of the project?

Opportunities for Class Discussion

Instructors should get to class early so they can organize the front board with headings from the

Customer objectives in the strategy map of Exhibit 5 in the case (see Exhibit TN-2).

Before launching the case discussion, if this is the first class on the Balanced Scorecard for

students (or executives), I start by showing a representative diagram of a Balanced Scorecard

that includes a portion of a strategy map and columns for objectives, measures, targets, and

initiatives. See Exhibit TN-1 for an example of a strategy map for a revenue growth theme

using product innovation.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

476

Initiatives are the action plans that help the organization achieve its stretch targets.

Many organizations get the measurement process backward. They view strategy as an action

Question 1: Can the BLO objectives be measured? What measures would you

suggest Sue Dahling-Sullivan select for the eight customer

objectives across the three strategic themes?

Turn to the students for suggestions of measures for the eight customer objectives. The first

theme, to develop and nurture loyal and generous donors, is straightforward and generally

generates lots of good responses. The challenge is to cut off the discussion early enough so time

remains for the other customer perspectives, and for a more general discussion on the scorecard

process. I recommend allocating about 20-25 minutes for this process.

Based on teaching the case several times, I prepared a listsee Exhibit TN-3of

representative measures for each of the eight customer objectives. You can challenge students

Question 2: What changes had to be made to adapt the Balanced Scorecard,

originally developed for businesses, to nonprofit organizations?

The changes required are relatively modest. The mission and customer objectives are placed at

the top of the strategy map and the financial objectives become a driver (or a constraint) but not

the ultimate performance measure for a nonprofit (or public sector) organization. Basically,

Question 3: What benefits does the BLO get from developing a BSC?

Students can identify several benefits from the case and background readings. Among these are:

The objectives and goals of the organization become transparent to everyone. Management,

board and the staff now have a better basis for managing tradeoffs and handling

disagreements.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

477

The strategy map provides focus for management discussions. Note how Jan del Sesto puts

the three high-level strategic themes on the white board before every staff meeting,

signaling to all that discussions should remain focused on ideas that help the opera company

succeed in its three strategic themes.

The clear statement of objectives gives senior managers of the BLO the ability to say no

to foundation and board member initiatives that require significant management and

The BSC provides a more objective basis for making resource allocation decisions for how

limited resourcesmoney and peopleshould be assigned to departments and initiatives.

Even with an arts organization, the BSC approach helps to set parameters for making the

difficult judgments and tradeoffs on the artistic productions (the Balanced Repertory

Scorecard). The general director (Del Sesto) has an explicit basis for productive

discussions with Stephen Lord and Leon Major about achieving a good balance between

popular, familiar operas and new, original, and nontraditional productions that allow

exciting young talent to be trained and featured. She can balance the needs of her different

constituencies.

The staff, for the first time, has a clear idea about how the organization measures success.

All employees understand how they fit in and can contribute. Two vignettes in the case

The BSC process engages the board and senior management in tough, but productive

discussions about objectives and strategy. The process helped to persuade a strong board

member, the founder of Opera New England (ONE), to voluntarily cutback on the scope of

this outreach program because she saw the benefits from focusing resources in the

immediate Boston area. Such an agreement would have been difficult if not impossible to

achieve if this edict came down from Jan del Sesto or the BLO board chairman. But because

the board member participated actively in setting the strategy and objectives, she bought

into the more focused, somewhat scaled-down, mission for ONE.

Many nonprofits struggle to engage their boards in active discussions, beyond issues of

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

478

revise plans and budgets in light of much lower revenue and donation projections. But these

What challenges does the BLO have to overcome for the BSC to be effective?

Students generally note that a BSC project, especially for a nonprofit, seems to require

significant time and resources. Are the benefits worth the cost? This is a good issue to let the

class debate. The project did run for about four months but the work, of course, was not

Some of the measures can be costly and difficult to obtain. Conducting focus groups with opera

experts, and conducting surveys of donors, opera attendees, board members, and employees is

expensive. The organization must decide that the benefits they obtain from the measures exceed

this cost. Also difficult is setting targets, particularly when you are first in the industry to be

using such a measure-based approach.

The BLO experienced a backlash from a board member who felt that an arts organization cannot

479

Question 4: Is the BSC too controlling? Are BLO departmental managers, artistic

leaders, and employees empowered or suffocated by the BSC?

Whether the system is controlling or empowering clearly depends on how it is used by senior

management. A command and control manager can certainly use the BSC to set detailed

performance targets for each department or employee. Jan del Sesto, on the other hand, a true

One can draw the following diagram to illustrate the key issue involved in the control vs.

empowerment debate:

Standard cost systems and budgets control inputs and the processhow much can be spent and

the efficiency of the process (cost, quality, and time). This works well when the production

process is well defined and senior executives want employees to follow standard operating

procedures.

In contrast, the BSC sets targets, sometimes stretch targets, for outputs and outcomes.

Employees for the first time understand what their organization is trying to accomplish and how

they can make a difference. Senior managers should encourage departments and employees to

be creative and find new and better ways to accomplish organizational objectives. Employees

One can have an interesting discussion about whether the staff should have been engaged at the

outset in developing the BSC, or is it better to have the board and senior management develop

the scorecard and then communicate it out to middle managers and staff. In the case, Sherif

Nada (board chairman) contrasted the BLO approach with his experience at Citizen Schools

This discussion should lead naturally to the next question.

480

Question 5: Is Janice Del Sesto using the BSC as a performance measurement

system or a management system?

Janice (like executives in other successful BSC organizations) uses the scorecard interactively.

The BSC helps her communicate objectives and stimulate dialogue and discussion about mission

Question 6: Comment on the process used by the BLO to develop the BSC.

1. CEO Leadership. Strong leadership at the top of the organization is the most important

ingredient for any successful BSC project. Janice Del Sesto is an outstanding leader for the

2. Internal Project Leader. Sue Dahling-Sullivan, deputy director, was already an experienced

3. Board Leadership and Support. Ken Freed, head of the BLO planning committee and

Sherif Nada, chairman of the BLO board, were enthusiastic participants and supporters

4. Experienced and Capable Consultant/Coach. Ellen Kaplan had five years of experience

helping nonprofit organizations articulate their strategies and translate them into strategy

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

481

Question: Why is such an extended process, with board members, the CEO,

and artistic and management staff required to produce the strategy

map? Why not have Sue Dahling-Sullivan and Ellen Kaplan get

together for a day or two and craft the strategy map and BSC for the

BLO?

Arguably, Dahling-Sullivan understands well the mission and strategy of the BLO, and Kaplan

has the skills to work with Dahling-Sullivan to translate these into well-crafted strategic

objectives and cause-and-effect relationships. Why then take up the time of all the other

constituents?

The most successful BSC projects have both an analytic component and an emotional component.

Dahling-Sullivan and Kaplan can do the analytic component but they can not, by themselves,

Postscript

When Sue Dahling-Sullivan attended a class in December 2001, she brought a summary of the

initiatives currently underway based on the BLO Balanced Scorecard. Exhibit TN-5 is the

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

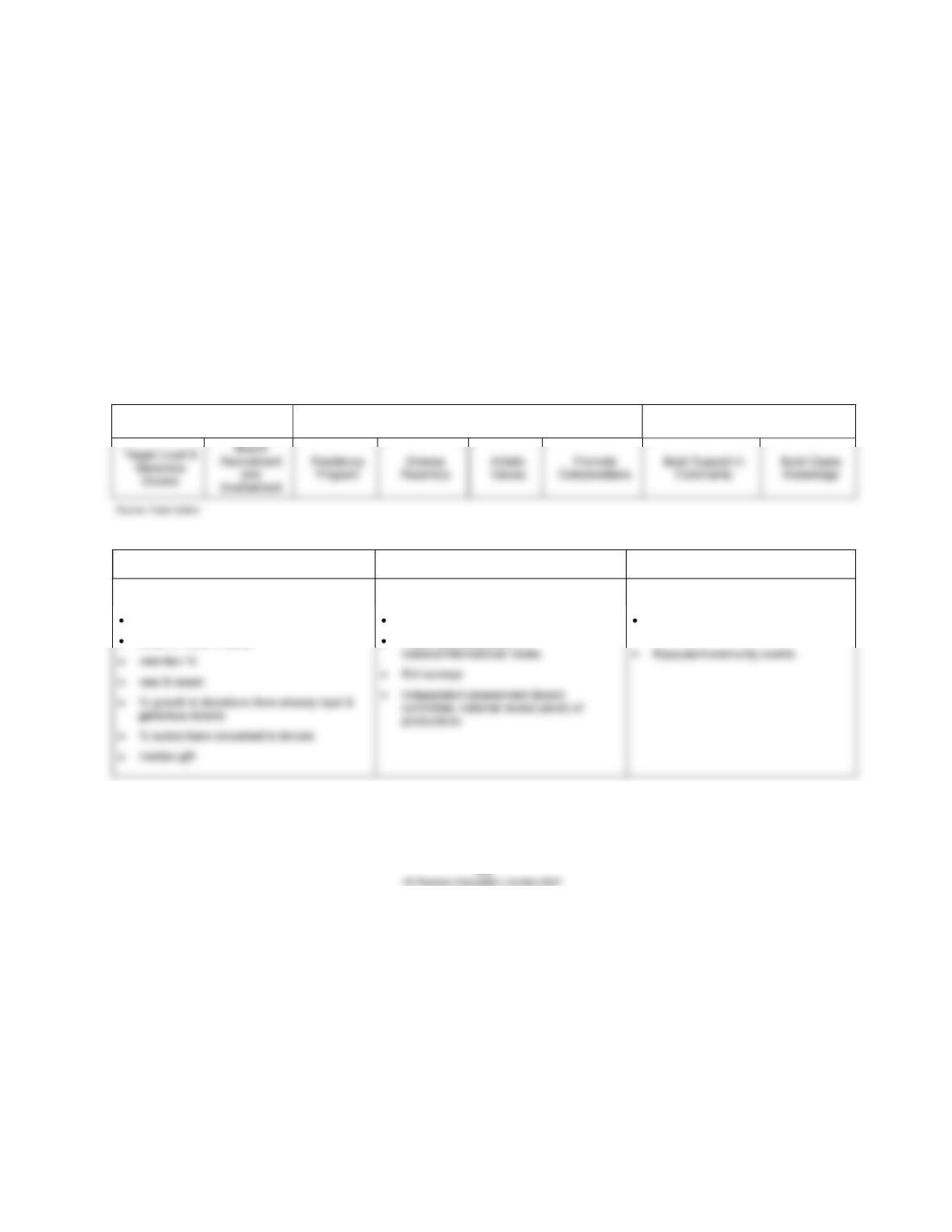

Exhibit TN-1 Example of Strategy Map and Balanced Scorecard

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

Exhibit TN-2 Front Board Plan for Customer Measures

Loyal and Generous

Supporters/Subscribers National/International Opera Scene Enhance Opera in Boston

Community

Exhibit TN-3 Potential Measures for BLO Customer Perspective

Loyal & Generous Supporters National/International Opera Scene Boston Community

1. TARGET LOYAL & GENEROUS DONORS 2. ARTISTIC REPUTATION 3. BUILD COMMUNITY SUPPORT

# new donors > $5,000

share of donors wallet

Peer review ratings

Press notices/awards in

Awareness survey in Boston

community

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

BOARD RECRUITMENT AND INVOLVEMENT

Strategic gap coverage

% board members involved in recruiting or

fundraising

2. SUCCESSFUL RESIDENCY PROGRAM

# BLO young artists with subsequent

appearances in national/international

productions

3. BUILD KNOWLEDGE ABOUT

OPERA IN BOSTON COMMUNITY

# people exposed to educational

programs (in person, Web)

PRODUCE A DIVERSE REPERTORY

# contemporary/nontraditional operas

# nontraditional productions

PROMOTE COLLABORATIONS

# prestigious partnerships

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

Exhibit TN-4 Boston Lyric Opera Strategic Measures

Strategy Map Theme Objective Department Target and Measure

Customer/Community Build community support Marketing TBD X% name recognition in community survey by x yr.

Customer/Community Build community support Marketing/Education TBD X # of community-oriented activities in which BLO takes

a major role.

Customer/Opera

Build artistic reputation for

high standards Marketing

50% of press references acknowledge a BLO

standards/style in 3 years.

Customer/Opera

Build artistic reputation for

high standards Marketing 75% annual subscription renewal.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

Customer/Opera

Launch unique

comprehensive residency

program

Artistic 50% of debut artists engaged within 3 years at Level I or

equivalent opera companies.

Customer/Supporters Focus on board involvement

and recruitment Development 10% new board members (directors and overseers) each

year that fill specific needs.

Customer/Supporters Focus on board involvement

and recruitment Development 75% board participation in fundraising activities annually.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

Int. Business Process #1 Enhance customer

relationships within key

groups through streamlined

process; increased one-on-

All/Executive One outstanding employee award given per production.

Int. Business Process #1 Enhance customer

relationships within key

groups through streamlined

process; increased one-on-

one contact; improved board

Development Gift Acknowledgements sent 2 working days after gift/pledge

received.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

Int. Business Process #2 Increase Brand Awareness

with launch of

comprehensive PR

campaign; developing new

programs/products

Marketing/

Development

50% of all new programs/events are repeated in subsequent

seasons.

Int. Business Process #3 Insure operational excellence

through contracting best

talent; developing innovation

Artistic 75% of first-choice talent is contracted each season.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

Learning & Growth #3 Integrate organizational

alignment to strategic goals

with a communications plan

and milestone evaluation

dates/plan.

All/Executive 80% of each years targets successfully achieved.

Learning & Growth #3 Integrate organizational

alignment to strategic goals

All/Executive 100% awareness level of strategic goals by board, staff, and

volunteers.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

Exhibit TN-5 FY2002 Balanced Scorecard Initiatives

Boston Lyric Opera Balanced Scorecard

Case Study Follow-up December, 2001

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

491

Exhibit TN-6 Summary of BLO FY2002 Strategic Initiatives

Customer:

Major community initiative launched: Outdoor Performance on Boston Common in

September 2002.

Artistic Planning and reprogramming discussions: Stephen Lord/Music Director, Now

how will these repertoire changes fit into the Balanced Scorecard and our goals?

Internal Business Processes:

Internal software program developed by junior staff to capture donor data (Harmonic

Convergence).

New strategic education plan implemented: On-line learning initiative; Opera Insights

program: community previews programs launched to support outdoor production;

Learning and Growth:

Internal teaching teams/skills training program (peer to peer) developed.

Financial:

Contingency planning underwayBSC helps to guide trade-offs.