Marshall School of Business

University of Southern California

A203-11-TN

Rev. 9-15-04

Olympic Car Wash

Teaching Note

How large should the bonus pool be for the Aalst location?

One possible solution

Flex the budget based on number of hours of good weather.

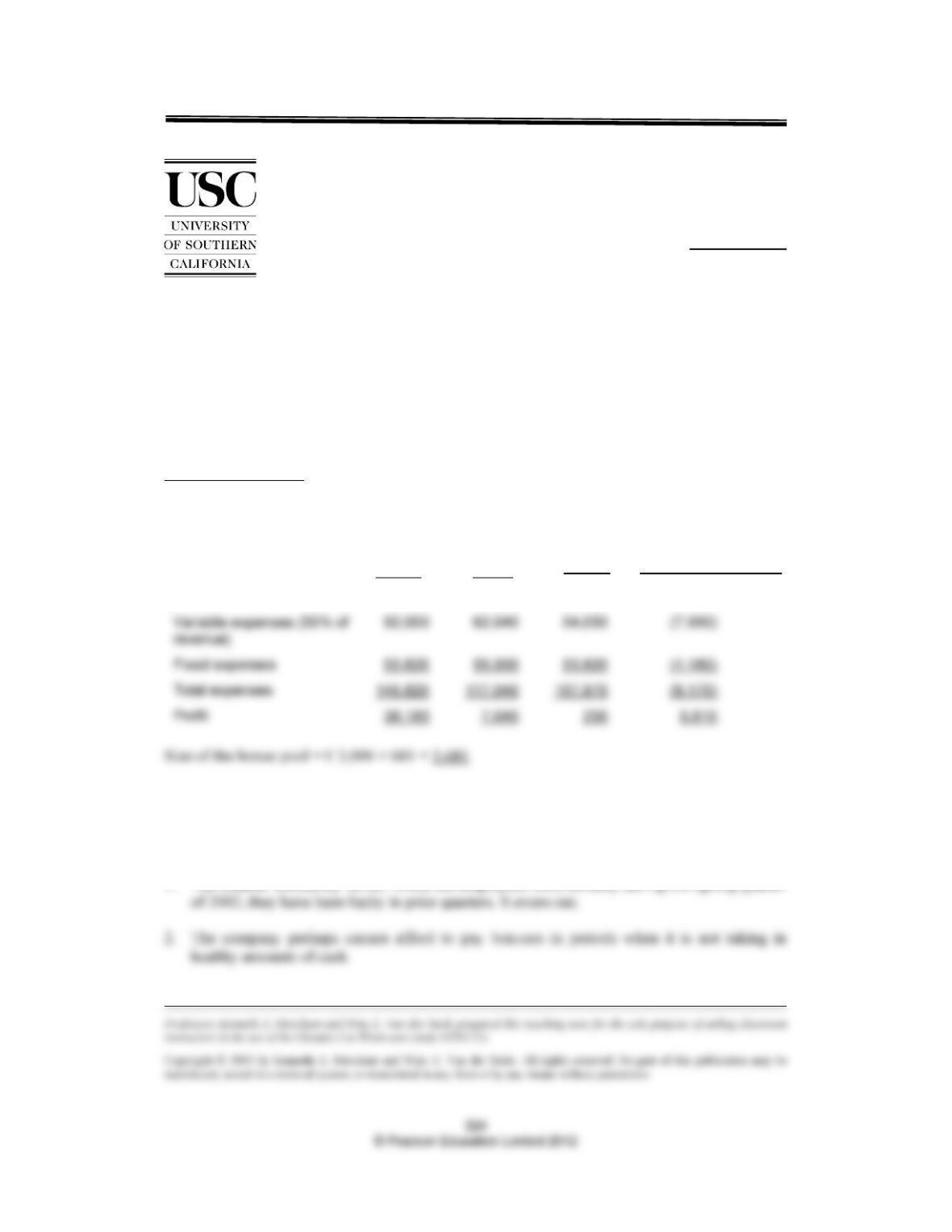

Budget

Actual

Flexible

Budget

Controllable Variance

(Actual – Flex Budget)

Revenue 184,000 124,080 108,100 15,980

While this solution is simple and straightforward, it is far from the only possible solution to this

case. Students might well be asked to judge whether zero is a possible correct answer to this

case. It is. Jacques Van Raemdonck might as well conclude that no adjustments should be made

for the uncontrollable effects of weather for any of the following reasons:

1. The weather constantly varies. While the employees were unlucky during the Spring quarter

325

3. The costs of making these adjustments exceed the benefits of making them. In order to

make these adjustments, someone has to keep track of periods of rain that will deter

customers from getting their cars washed. Some difficult judgments might be required. For

example, how much rain warrants an adjustment? More than a drizzle? A duration more

than a brief shower? Is just the threat of rain a justifiable cause for an adjustment? Is it not

possible that customers will just defer their car wash until a good weather period, resulting

is no (or little) actual loss of business? And if an adjustment seems warranted, someone has

to sit down and do the calculations.

Note that regardless of the reasons, this approach of not adjusting for this weather factor, or any

other uncontrollable factor, forces employees to share some risk with the owners of the

Figure A

Graphical Representation of a Variance Analysis

Factor Budget (1) (2) (3) (4) Actual

Hours of good weather P A A A A A

Vehicles/hr. P P A A A A

Revenue/vehicle P P P A A A

Figure A shows that the budget is based on planned assumptions about each of the factors that

affect performance. This is shown with the letter P. The actuals are calculated based on the

actual levels for each of those factors, here designated with the letter A. The effect of each of the

factors on performance can be calculated by changing the factor from P to A, or A to P. The

difference between the budget and column (1) can be called the weather variance. The

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

326

the numbers that would result if the actuals were adjusted first for the effects of the misforecast

hours of bad weather.41

Budget

Actual

Adjusted

Actual42

Controllable Variance

(Adjusted Actual Budget)

Revenue 184,000 124,080 211,200 27,200