Marshall School of Business

University of Southern California

Statoil

Teaching Note

Purpose of Case

This case describes the innovative, even radical, management systems of a company that

combines the major elements of Beyond Budgeting and Balanced Scorecards into an approach

called Ambition-to-Action. The Ambition-to-Action approach involves the replacement of a

unitary budgeting process with three processes that separate the major purposes of budgeting:

planning, resource allocation, and performance evaluation. It also involves the use of key-

Possible Background Reading

Direct students to the Beyond Budgeting Roundtable website (www.bbrt.org). Have them click

on the Beyond Budgeting tab on the left panel and read the material in that section, titled

About Beyond Budgeting.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

316

Suggested Assignment Questions

1. Statoil managers claim that their company no longer prepares a budget. What do they mean

by that claim?

2. Why did Statoil decide to abandon budgeting?

3. Describe the new processes that Statoil implemented to replace the budget. What are its

strengths and weaknesses?

Suggested Discussion Questions and Analysis

1. What purposes are served by the annual budgeting process used by most companies?

Students will provide a variety of answers, but most of them can be organized into the

2. Statoil managers were displeased with the traditional budgeting process that the

company formerly used. Why?

a. Conservatism. If the forecasts are used as performance targets and, hence, as the bases

for performance evaluations (as is the case in most companies), they naturally become

conservatively biased.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

317

3. What are the major differences between a traditional budgeting process and the

Statoil Ambition-to-Action process?

a. Statoil separates the three functions of budgeting: forecasting, target setting and

resource allocation.

i. Forecasts compensate for the lack of agility; they are updated as needednot on

annual cycles. In terms that Bjarte often uses, Supertankers need forecasts. Speed

boats not so much.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

318

iii. It was normal for units to identify 1020 KPIs. (The range was 525.) Bjarte thinks

that 2025 is too many, but he is quick to point out that the perfect KPI does not

exist.

c. Where they can, Statoil managers use KPIs that describe relative performance, ideally

relative to an external benchmark (e.g., the performance of competitors or like inside

units), or at least relating outputs to inputs (e.g., cost per barrel). The reasons:

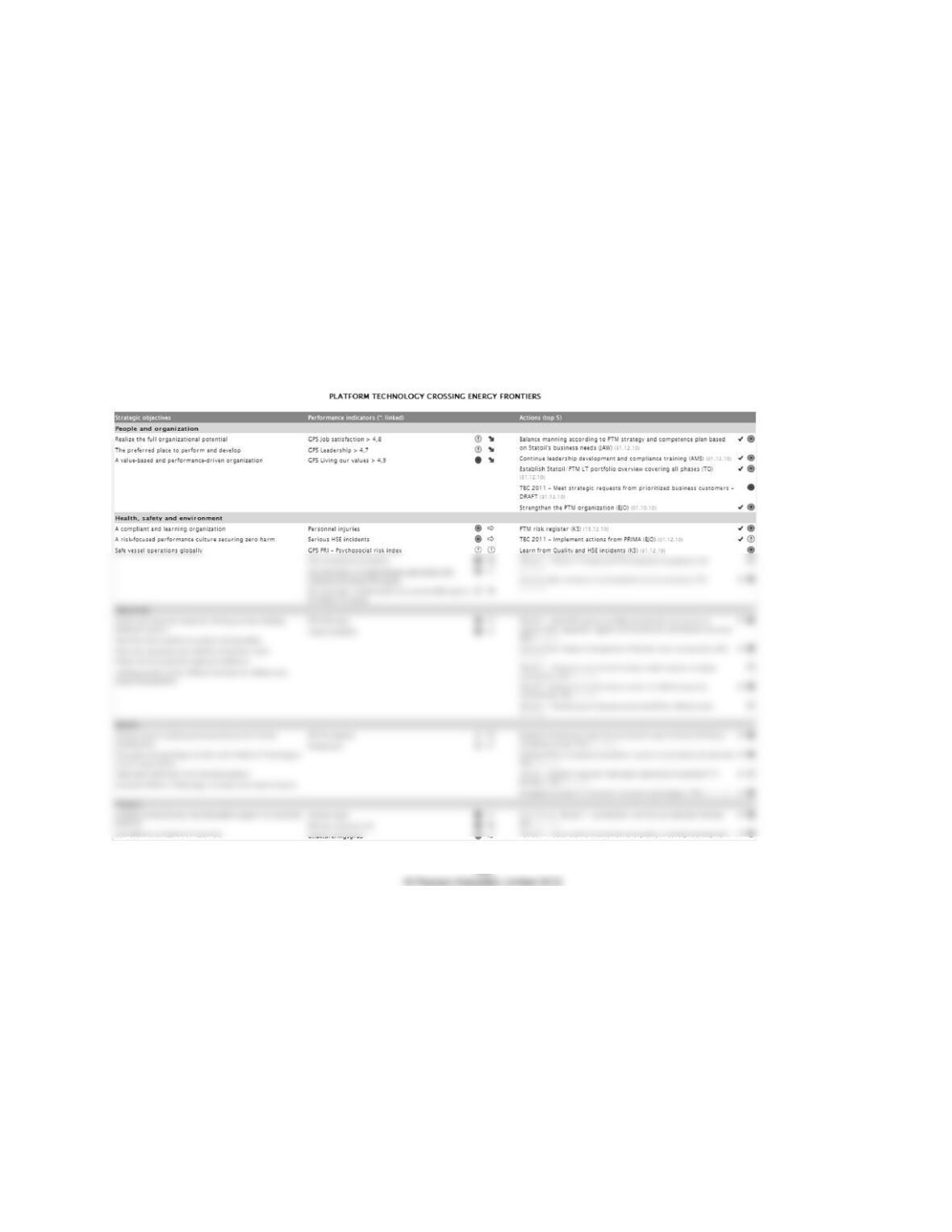

d. Statoil uses Ambition-to-Action documents that provide a direct link between strategic

objectives, the KPIs that can be used to monitor performance, and the actions necessary

to affect the KPIs and, hence, to implement the intended strategy.

Issues for Discussion

1. In January 2011, Bjarte Bogsnes estimated that if every manager within Statoil used the

process, upward of 2,000 Ambition-to-Action documents would be generated and

maintained. But at the time of the case, there were only 1,100 such documents in existence,

meaning that many managers were not participating. Is this a problem? (All of the upper-

2. The KPIs did not cascade from the top to the bottom of the organization. Instead, the

scorecard targets were said to be translated from one organization level to another. Only a

few targets (e.g., oil produced) could be consolidated. The KPIs could be, and were,

changed from period to period, perhaps hindering comparisons over time. Could this/should

this be tightened up?

3. The managers chose their own targets. No level of performance was imposed on them.

Statoil managers thought that the use of relative performance KPIs caused them to set more

ambitious targets for themselves because no one wants to be a laggard. If this

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

319

assumption/belief is correct, should all companies allow managers to set their own

performance targets, or does this work only with relative performance targets?

4. The performance evaluations are holistic but quite subjective. Statoil managers think that

evaluations can be made only with the advantage of hindsight. But subjectivity creates its

own problems, such as evaluation bias. Is the high use of subjectivity evidence of an

immature, or if not that, an overly complex, performance measurement/evaluation system?

Also, how convincing is Elder Saetres claim that it takes a few years for employees to

understand how it works, but then it can be very credible?

One conclusion to leave with the students is that the Statoil system is directly related to the

companys managers beliefs about people, which affects their philosophy of management (see

Pedagogy

This is a complex case. The teaching of it works better if students have a basic understanding of

the traditional annual budgeting process used by the vast majority of organizations world-wide.

Then contrasts can be drawn between traditional systems and this Beyond Budgeting system.

The Balanced Scorecard aspect of the Statoil system seems quite loose, as the measures do not

cascade automatically from the top to the bottom of the organization. But that is by design. This

is an aspect of the system that is left up to the wisdom of the managers.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

322

Exhibit TN-A

Reasons to Budget

Strategy implementation:

Operationalizing/translating strategy

Communication and coordination:

Operational planning:

Annual resource allocation and financial planning (e.g., estimates of spending by

Performance evaluation:

Establishing results accountability and providing motivation through budget targets

And also:

Authorization or permission to spend

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

323

Exhibit TN-B

Beliefs about People: Theory X v. Y

Theory X

Employees are inherently lazy, unambitious, averse to taking responsibility, and valuing

security above all else.

Theory Y

Employees as being self-directed if they are committed to organizational objectives and

accepting of responsibility.

Statoil managers beliefs:

CEO Helge Lund:

One of the main principles in our Ambition-to-Action concept is that Statoil consists of

mature, professional, and able people who both can and want to accept responsibility.

Bjarte Bogsnes:

We believe that perhaps 90% of our employees have Theory Y traits. We are not naïve.