Harvard Business School 5-190-199

May 17, 1990

HCC Industries, Inc.

Teaching Note

Purpose of Case

The HCC Industries case was written to motivate a discussion of the relationships between

budget targets, performance evaluation procedures, and incentives in decentralized

organizations. The situation described in the case is dramatic because the company made a

significant shift in its philosophies about budgets and incentives.

Until 1987, HCCs operating units budgets contained stretch performance targets because

corporate managers believed aggressive targets would motivate the operating managers to perform

at their highest possible levels. In planning for fiscal year 1988, however, the corporate managers

The case describes the companys management systems before and after the change and the

first-quarter experiences with the new systems. The description at the end of the case suggests

that the change was not totally successful: None of the operating units achieved all of its MPS

targets, and organizational tension had increased significantly. This outcome leaves students to

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

227

Suggested Assignment Questions

2. Should HCC managers have expected that the MPS target-setting philosophy would be

equally effective in all four operating divisions described?

3. What, if anything, could have been done to improve the implementation of the new

philosophy?

Question 1MPS vs. Stretch Targets

HCC corporate managers primary stated motivation for changing their budgeting philosophy

was their desire to improve the predictability of corporate planning and financial reporting.

They thought they could improve corporate planning without compromising motivation.

Motivation was to be intact because the new system was designed to give division managers a

challenging target to shoot for, as well as an MPS, and no upside limits on bonus potentials.

But if planning was the sole reason for change, corporate managers could have merely factored

down the consolidation of the divisions plans. In other words, they could have taken a

negative reserve to protect against the consequences of some divisions not achieving their

plans.

Since the negative-reserve alternative is so obvious, there must be something else going on. I

think corporate managers had two other major concerns. First, they were disturbed that some

division managers were adding overhead in periods when they are not achieving their targets

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

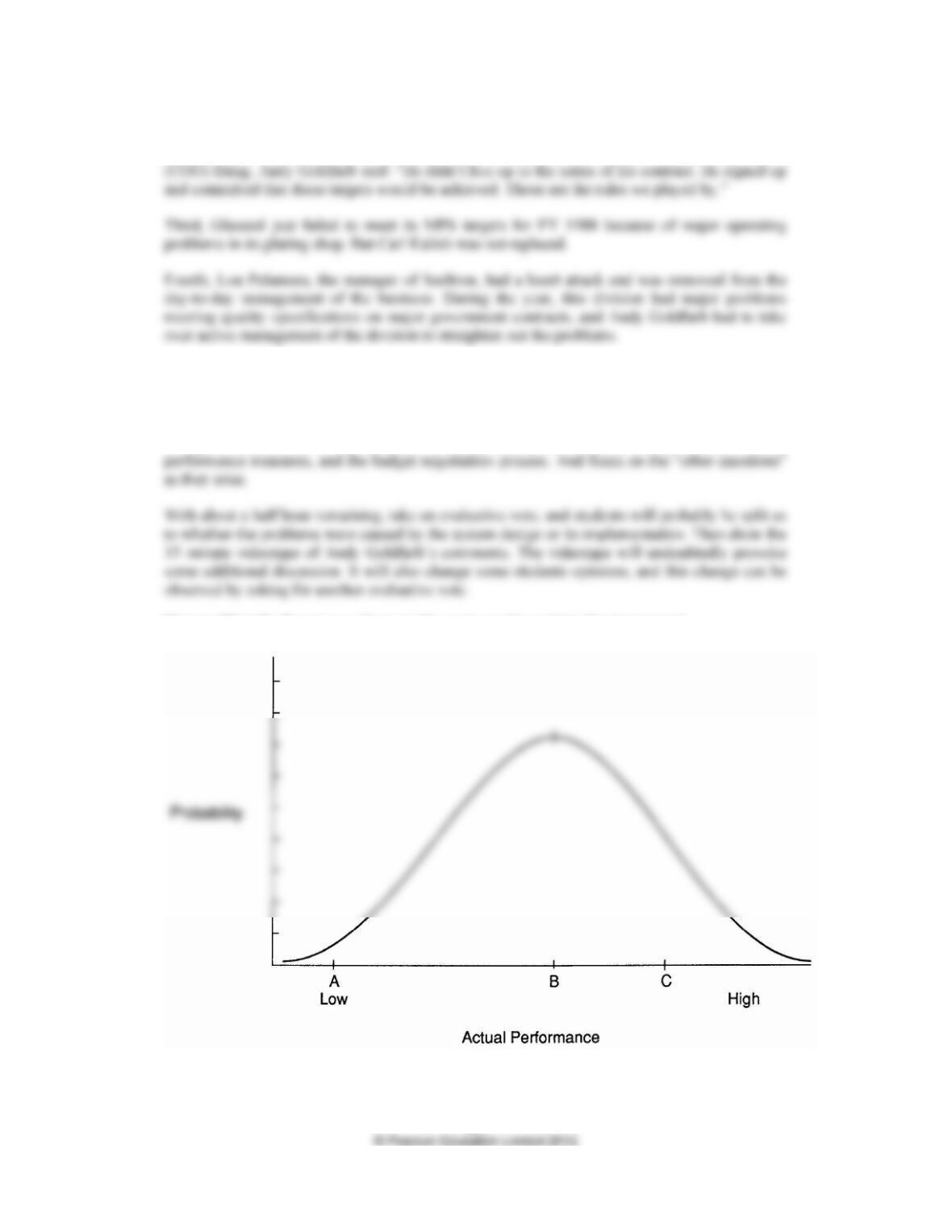

The idea of less-than-100% achievability is illustrated in Figure TN-1. Expectations of actual

performance are shown to be roughly symmetrical around a point B which can be labeled a

In class it can be noted that the stretch targets even in HCCs old system are far below point C

on Figure TN-1, the 2540% achievability level that some textbooks conclude provides the

optimal motivation.22 Mike Pelta in Hermetic Seal said he used to feel he had an 8595% chance

of achieving his targets (p. 8), but he also bragged that he had never missed a budget in his 33

years of being a manager. Carl Kalish in Glasseal felt the old probability was 90%. Thus even

the old stretch targets were more highly achievable then best-guess targets. The question that

can be raised in class is: Was/is motivation being compromised by these excessively easy

targets?

The second cause of early failure of the new system seems to be that the operating managers

expected value of bonuses has declined sharply. Now they must exceed their MPS targets to

It might be useful to put students in Al Bergers role to consider how they would treat

uncontrollable influences. Would they provide forgiveness? (Doing so makes the corporation

1. Would they override the terms of the contract and provide some incentive compensation? If

so, how much? (Estimate and forgive the full amount, or merely a token bonus?)

3. If forgiveness is to be given for events like this, how specific should the promises of

Question 2Any Differences Across Divisions?

While the divisions are in many ways quite similar, they have a few differences that perhaps

should lead to special budgeting/evaluation/reward differences.

a. Hermetic Seal is run by Mike Pelta. Mike is a powerful person in the corporation because he

was a cofounder and is a major stockholder. Mike is also somewhat unique in that his

b. Sealtron presents two unique considerations. First, the division missed its targets in 1987

and its personnel received no bonuses or salary increases. Lou Palamara (division manager)

argues that this may cause employee retention problems. Should this type of employee

retention issue have an effect on budgeting/evaluation/reward decisions? (Yes.)

Second, corporate managers regard Lou Palamara as a poor manager. They feel that in 1987

c. Hermetite is also unique in two ways. First, it is in a turnaround situation, so planning

uncertainty is high. As Alan Wong (division manager) says in the case (p. 12), nobody

knows what to expect. How do you set budget targets in such an environment?

Second, Alan Wong seems to be an inveterate optimist. (Alan is not totally unique; I met

Question 3Implementation

Other Questions that Might Be Raised in Class

1. Why do managers not play it straight in setting budget targets?

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

230

2. A unique feature of HCCs new system is that corporate managers allow the division

managers to decide what their share of the division bonus pool should be (p. 7). Is

this a wise idea?

3. Why are bonus levels set where they are? Why 2025% of base salary and not 10% or

100%?

4. Why is there no upper cap on bonus possibilities?

There is little good data on how many companies cap bonus potentials, but most seem to. (In my

study of 12 firms,23 nine firms used such caps.) Thus, HCCs practice seems unusual. The firms

5. Because of the significant penalties of not achieving the MPS targets, is there a

danger that managers will attempt to carry profits across years?

Subsequent Events

Many significant events took place shortly after those described in the case. First, Mike Pelta,

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

231

Second, failures to meet the MPS targets caused both the chief operating officer to be fired (in

March 1988) and one division (Hermetite) to be divested (in June 1988). About the Al Bergers

Pedagogy

I suggest using an unstructured approach in teaching the case. Go right to the evaluation of the

change. At some time it may be useful to clarify facts, such as about the key success factors,

Figure TN-1 Performance Expectations in an Uncertain Environment