Marshall School of Business

University of Southern California

Axeon N.V.

Teaching Note

Purpose of Case

The Axeon N.V. case was written to illustrate the effects of a management control system and

the supporting management processes on one specific, major decision in a decentralized,

multinational corporation. The situation, which is real, but disguised, illustrates the real world

application of many management accounting concepts, including incremental cost analysis,

capital budgeting, sensitivity analysis, and transfer pricing. But perhaps more importantly, the

case is about managing the cost/benefit trade-offs that are inherent in a decentralized firm. The

Suggested Assignment Questions

1. Is construction of the new factory in the UK in the best interest of Axeon N.V.?

2. Ignoring your answer to question 1, if the plant were not built and AR-42 was shipped from

the Netherlands to the UK, what transfer price would be appropriate?

3. What should Mr. van Leuven do?

P

rofessors Kenneth A. Merchant, Wim A. Van der Stede, and research assistant Xiaoling (Clara) Chen wrote this teaching note as

an aid for instructors using the Axeon N.V. case.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

131

Case Analysis

A. Product Sourcing Alternatives

Despite the existence of many relevant data in the case, the answer to the first assignment

question is not an easy one. There are two alternatives for producing AR-42: UK and

Netherlands.

The best place to start is with the discounted cash flow analysis, a summary of which is

presented in Exhibit 2 of the case. Case Exhibits 3 to 5 provide back-up detail. The analysis is

Was there anything wrong with this initial analysis? The analysis looks sophisticated, and most

students will instantly empathize with Mr. Wallingford. However, criticisms can be made of his

analysis:

1. The end-of-project recovery value of equipment and working capital is a surrogate for the

cash flows after the end of 7 years. It is likely that this is biased downward. Why would all

sales and profits stop after that date? Is there no learning that has come from this project?

Does the project have no option value?

2. Wallingford might well have presented some sensitivity analyses, reflecting more

3. Most importantly, although he appears to be taking a corporate perspective and, hence,

comes across as an appealing character with whom most MBA students will identify,

Wallingford is really parochial. He did not consider the investment opportunity using a

corporate-focused perspective. Wallingford is indignant about Axeon managers rejection of

his idea, but he is not as innocent as he portrays himself. The main defect in his analysis

So we see in the case that the Dutch managers argue that producing the AR-42 in the

Netherlands is an even better alternative than that proposed by Mr. Wallingford. Some of their

arguments question some of the numbers in the Hollandsworth analysis. The Axeon director of

sales (Mr. De Rijcke) questioned the sales forecasts. But who understands the UK market better,

the local general manager or the functional specialist in a foreign country?

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

analysis. The analysis of the variable costs (as shown in Exhibit 6 of the case) is misleading. As

shown in Exhibit-TN 1, an average variable cost of 1860 on the full 1000 tons of production

Next the instructor can turn to the discounted cash flow comparisons. Exhibit-TN 2 shows an

analysis of the Netherlands proposal. The revised analysis still favors the Netherlands proposal,

mainly due to the much greater initial investments for the UK proposal.

UK Proposal Netherlands Proposal

Net present value @ 8% 916,000 £1,288,790

Internal rate of return 20% 26%

In addition, taking into account the higher risks involved in the UK startup relative to the

Netherlands expansion, the UK hurdle rate should be higher, which makes the Netherlands

alternative even more attractive.

On the other hand, sensitivity analyses would show that the UK managers could face significant

sales shortfalls and manufacturing problems and still have a project with a positive net present

value. In terms of that criterion, or even the Axeon 12% hurdle rate criterion, perhaps the impact

of the startup complications are not as significant as the Axeon functional managers believe

them to be.

Further, the irrelevance of the fixed costs in the Netherlands proposal makes sense only if the

Netherlands has, and will always have, excess capacity for producing AR-42. In other words,

Other issues such as nationalism and perceived autonomy are also important. Axeon N.V. is

increasingly embracing a philosophy of decentralization. Therefore, even if the UK proposal is

not optimal, forcing manufacturing of AR-42 in the Netherlands will undercut the perceived

decentralization in the company. Another consideration is the nationalistic sentiments of the

English. This is suggested by the requirement of a majority of local directors for the

Hollandsworth board and the threatened resignation of Mr. Nobel. An increase in duties on AR–

42 is likely if the UK viewed Axeon as exploiting the UK market from the Netherlands.

B. Why Did Mr. van Leuven Behave as He Did?

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

133

C. The Transfer Pricing Issue

If the AR-42 for the UK is sourced from the UK, then the analysis is complete. However, if AR-

42 is supplied from the Netherlands to the UK, then a transfer price must be established. There

are a number of transfer pricing possibilities:

2. Cost, or cost plus a mark-up. Cost can be defined anywhere from incremental variable

3. A two-book system. This would involve crediting the Netherlands at market price but

charging the UK only the variable cost. This would make both divisions happy, presumably,

but it would lead to a double counting of profits and require a corporate elimination.

In many decentralized companies, managers would allow the division managers to negotiate a

fair transfer price. But in this case, because of the friction already generated between personnel

in the UK and the Netherlands, negotiation may not be possible. So, here, Mr. van Leuven

probably has to choose a transfer pricing method and a means of implementing his decision.

The total contribution per ton of AR-42 is as follows (using figures from year two and the

following):

Selling price £3,700

Each transfer pricing method allocates this contribution between the UK and the Netherlands.

What transfer pricing/profit sharing arrangement is best? There is no correct solution. Transfer

prices provide one way of shaping managerial behavior. If centralized production is deemed to

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

134

D. Fit Between Strategy, Organization Structure, and Control Systems

At this point in the class discussion, it is useful for the instructor to ask the following question:

What is Axeons corporate strategy? Can you tell from the case what the key success factors are

for Axeon?

The case does not provide much information about Axeons critical success factors. What is

most critical for Axeonidentifying new applications and markets or producing at low cost?

Should the companys critical success factor(s) affect decisions about organization structure and

management control systems? Clearly yes. This observation can lead naturally into a discussion

1. Market sensitivity is enhanced with increased decentralization. Also, a decentralized

2. Economies of scale decrease with increased levels of decentralization. This is because a

decentralized organization loses the cost savings from shared management overhead and

larger, more efficient plants.

In summary, Axeon is facing two sets of pressures:

Centralization Strategy Decentralization Strategy

Key success factor Low cost New product applications

Key function Production Marketing

Responsibility Centers:

To some extent, Axeons control system is a compromise between full decentralization, which

would use highly autonomous local investment centers, and full centralization, which would

have the local organizations be only marketing outposts, revenue centers.

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

135

E. What Should Mr. van Leuven Do?

There is no correct solution here; there are only pros and cons. The options are to source in the

UK, source in the Netherlands, or delay. Delay means possibly source in the UK after the

viability of the market has been demonstrated. Asking students to vote as to their preference will

reveal significant differences in opinion. This vote, if one is taken, should come very late in the

class.

While it appears that the economics of this decision favor the Netherlands, our own take is that

the decision in this case should probably favor the UK. If a decentralized organization structure

What Happened?

In the real world situation, the Hollandsworth project was rejected. The transfer price was set at

£3700, so the full cost to Hollandsworth (including shipping and duty) was £3900. Initially,

Hollandsworth managers tried to sell AR-42 at a price of £4500 per ton, but the volume sold

was miniscule. Eight months later, they lowered the price to £4200. The annualized rate of sales

went to 150 tons, and Hollandsworth managers thought that the potential was there for annual

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

136

Student Takeaways

Students can learn a lot from this case. They can practice their technical skills, such as those

required to do net present value analyses, and they can apply their transfer pricing theories to a

Pedagogy

Many students see this case as difficult. Sound amount of floundering with the numbers is

useful, but if the floundering continues, instructors should be prepared to step in and help clarify

the analysis. That understanding is essential before moving on to the more qualitative aspects of

the case. Suggestd timing in a 75-minute class is as follows:

40 min. The plant investment decision

15 min. Transfer pricing alternatives and behavioral effects

Exhibit TN-1

Relevant cost analysis

Calculation of incremental variable cost per ton of manufacturing AR-42 in the

Netherlands for shipment to the UK:

Projected average variable cost in the Netherlands at 1000 tons 1,860

Projected total variable cost in the Netherlands at 1000 tons 1,860,000

Revised variable cost per ton (Different from Exhibit 6):

Incremental manufacturing variable cost 1,800

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

137

Exhibit TN-2

Discounted cash flow analysis Netherlands proposal

(Figures in rows (2)(4) in ; row (1) and rows (6)(9) in 000)

Year 0 1 2 3 4 5 6 7

(1) Working capital 120 20 20 160

(3) Incremental cost per ton 2,000 2,000 2,000 2,000 2,000 2,000 2,000

(2) (3)

(6) Total contribution

400 510 680 680 680 680 680

(7) Promotion costs 260 150 100 100 100 100 100

(6) (7)

Net present value at 8% 1,288,790

Merchant & Van der Stede, Management Control Systems, 3rd edition, Instructors Manual

138

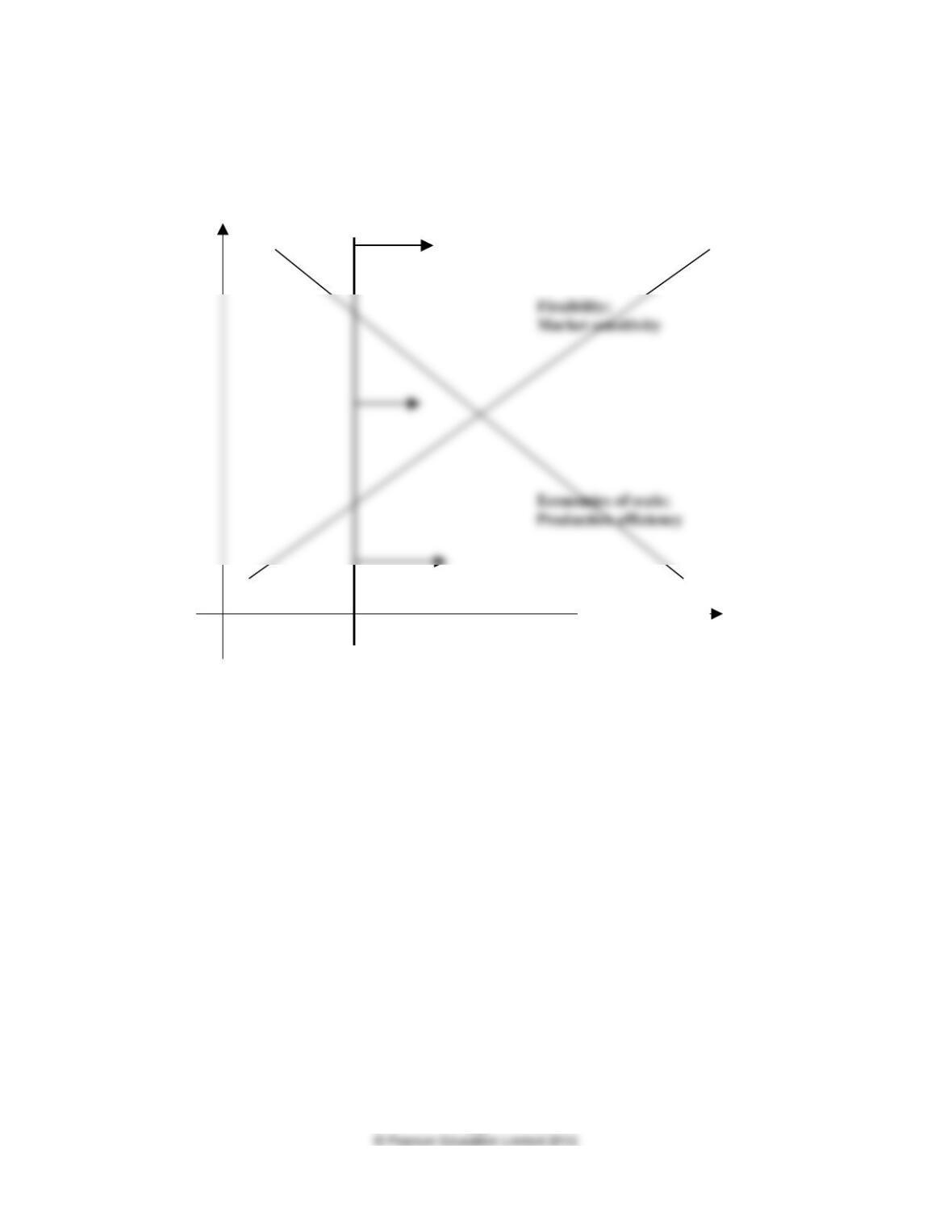

Exhibit TN-2

Flexibility and Efficiency as a Function of the Level of Decentralization

Axeon

Decentralization