3-16. This problem has two things growing simultaneously: population and per capita

expenditures. The town’s budget depends on the total population and the per capita

expenditure.

Population

Per capital expenditures

Budget

(This problem should give every homeowner, who pays property tax, something to

contemplate!)

3-17. This problem asks the student to understand the impact of spreading the mortgage

payments over a longer time period with a higher interest rate.

The first step is to determine the amount borrowed, which is $300,000 ($350,000 – 50,000).

With an interest rate of 8 percent and a 20 year time period, the amount of the annual

payment is

With an interest rate of 9 percent and a 25-year time period, the amount of the annual

payment is

9.823 is the interest factor for the present value of an annuity at 9 percent for 25 years.

Using a calculator, the answer is N = 25; I = 9; PV = 300,000; FV = 0, and PMT = ? =

30542.

3-18. This problem illustrates a typical situation facing the elderly. Aunt Kitty sells her

home, enters a retirement community, and needs to know how long her funds will last.

The framework of the problem is essentially the same as the mortgage in the previous

problem. In terms of a mortgage, the wording might be as follows. Suppose your mortgage

3.650 is the interest factor for the present value of an annuity at 6 percent for X years.

Locating this interest factor in the table indicates that the number of years is approximately

4.

Using a calculator, the answer is

3-19. This problem reverses the previous problem by asking will the individual be able to

withdraw $18,234 a year for 10 years if he earns 8 percent and starts with $107,500. To

answer the question, determine how much can be withdrawn. (This is also the reverse of the

mortgage in problem #17 except the payments are received and not made.)

With an interest rate of 8 percent and a 10-year time period, the amount of the annual

payment is

The widower will not be able to withdraw $18,234 a year for the next ten years. If he wants

to withdraw that much, he will have to earn a larger rate. (This is a repeat of the previous

problem except the rate is the unknown and the time period is known.)

Using a calculator, the answer is

N = 10; PV = 107,500; FV = 0, PMT = -18,234, and

I = ? = 10.97.

3-20. This problem has two parts; the first requires determining the future value of the

$26,000. That value is

Since the $26,000 grows to $44,668, you will have to accumulate an additional $55,332 in

order to have $100,000 at the end of the eight years. If the annual contributions are made at

the end of each year, the required amount is

10.259 is the interest factor for the future value of an annuity of $1 at 7 percent for eight

years.

Using the financial calculator, the answer is as follows:

3-21. This problem illustrates distributions (withdrawals) from retirement accounts. It is

similar to problem 19 except the payments are taken out at the beginning of the year and not

at the end of the year.

a. With an interest rate of 8 percent and a 20-year time period, the amount of the annual

withdrawal is

b. If 1/20 is withdrawn, the amount is $16,250. This leaves $308,750 which at 8 percent

grows to $333,450. The account increases in value.

3-22. The first part of the problem requires determining the future value of $60,000. At 5

percent for eighteen years, that amount is

3-23. This question boils down to: which alternative requires lower payments: $30,000 at 6

percent over four years or $28,000 at 8 percent over four years. The cash outflow required

by the $30,000 loan is

The cash outflow required by the $28,000 loan is

Take the $28,000 loan at 8 percent; the loan payments over the four years are smaller.

3-24. While this problem combines material in Chapters 2 and 3, it also serves as an

introduction to Chapter 10, which covers returns.

a. Using interest tables, the return is

b. If you buy the stock on margin of 60 percent, you invest $30 and borrow $20 which

grows to $70 minus the $20 borrowed (i.e., $50). Using interest tables, the return is

c. One method to prove the return is not 10 percent is to show that present value of the

payments is not equal to $30. At 10 percent the present value of the payments is

3-25. The first step is to determine the amount needed. That value is

The final sum is $14,901 short of the needed amount. She will have to invest each year an

amount necessary to obtain $14,901 so that she will have the necessary $267,300. That

amount is

3-26. At 5 percent: 72/5 = 14.4 years

Using interest tables to verify the number of years does not work since the tables will only

generate approximations. The student needs use a financial calculator. At 5 percent:

PV = 1; FV = 2; PMT = 0; I = 5; N = ? = 14.2

The Rule of 72 does provide reasonable approximations of how long it takes for a sum to

double.

3-27. The purpose of these problems is to encourage the use of computer programs or

financial calculators to solve time value of money problems. I use these only after I believe

that the students have had sufficient exposure to the concepts of time value and can set up

the problems and solve them.

Teaching Guides for Financial Advisor’s Investment Case: Funding a Pension Plan

This case places solving time value problems in the context of estimating future pension

benefits and funding those benefits. To make the case manageable, the estimates are limited

to two individuals.

1. Estimated salaries:

Estimated pensions:

Barber: If Ms. Barber retires at age 65, she will

2. The cost of each annuity to fund each pensions:

3. This question implicitly assumes that the firm has not put aside any funds to fund the

pension. Since the pension plan was recently adopted, the assumption is reasonable. (You

could recast the problem in terms of determining the possible cost of adopting particular

terms of a pension plan.)

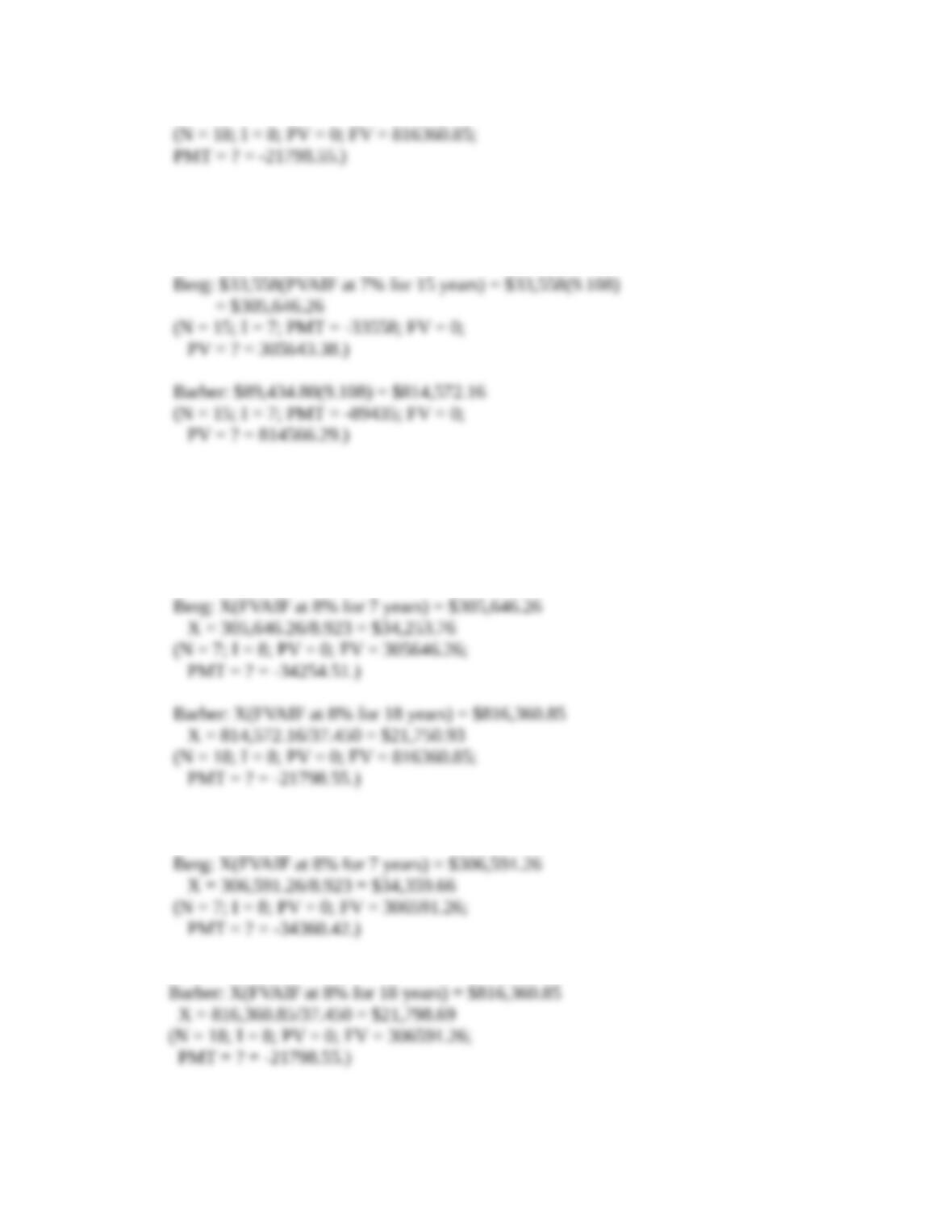

Berg: X(FVAIF at 8% for 7 years) = $270,477.48

4. Forecasting pension benefits and their current costs is exceedingly difficult, as the three

additional situations illustrate. Small changes in the assumptions can have a magnified

impact on benefits and their costs.

a. Increasing life expectancy to twenty years increases the amounts required to fund the

pensions:

The annual cost (amount invested) to have the money to fund the pensions:

b. Reducing the rate the insurance company pays on the annuity contracts will increase the

amount the firm will have to invest each year to cover the pensions:

The firm will now have to accumulate $305,646.26 and $814,572.16 instead of $270,477.48

and $720,844.49 to fund the two fifteen year pensions. (The costs would be even larger for

the twenty-year pensions.) The annual cost of this larger amount necessary to fund the

pension plans is

The annual cost (amount invested) to have the money to fund the pensions:

The increase in the annual payments to the pension plan is

c. If Ms. Barber retires early at age 62, this will reduce the estimate of her pension because

(1) her final salary will be lower and (2) the number of years worked is less.

Notice that Ms. Barber will have worked only 18 years, which requires a reduction in the

pension since she will have worked less than the required twenty-five years to obtain a full

pension.

Notice that the terms of the pension plan state that pension payments begin at age 65 and

that there is no provision for payments for early retirement. Since the pension starts 18 years

from now and not after 15 years when Ms. Barber retires, the firm has 18 years to

accumulate the required amount to fund the pension.