14-14. a. This problem, like the preceding problem, illustrates the split coupon bond. The

terms of these bonds are designed to reduce the firm’s cash outflows during the initial years

of the bond’s life.

b. The bond’s price is

c. The current yield is 0%.

d. Even though interest rates have fallen from 14 percent when this bond was issued to 12

14-15. This problem uses a split coupon bond to illustrate acting on expected changes in

interest rates. At 10 percent, the bond’s current price is

14-16. This problem requires the student to realize that when the individual expects the

bond will be retired has an impact on its valuation.

a. If the expected life of the bond is eight years, the

price of the bond is

b. If the life of the bond is thirteen years, its price is

c. If interest rates are 12 percent after eight years, the firm will extend the life of the bond to

take advantage of the lower coupon paid by the bond. Point out that the investor who paid

$875.96 will earn less than the 12 percent yield to maturity as that prices assumes the bond

14-17. a. This problem is another version of the previous problem. If the current interest

rate is 8 percent, than the life of the bond will not be extended and its current price should be

b. At 12 percent, the firm will extend the life of the bond for an additional five years. After

five years have passed, the bond will sell for:

14-18. If interest rates rise to 10 percent, the $70 grows to

If the student uses the interest table for the future value of one dollar, the interest factor is

$2,115.59/$1,000 = 2.11559. The interest factor for 8 percent for ten years is 2.159, which

indicates the return is a little less than 8 percent. In either calculation, the return exceeds the

14-19. This problem requires the student to determine two bonds’ durations to determine

their relative price volatility. The duration (D) of each bond is

Since the duration of bond A is smaller, its price is less volatile.

14-20. The duration for Bond C:

The rankings of the bond’s price volatility from most volatile to least volatile is A, B, C.

The price of bond C is $856

The percentage change (decline) in the price of each bond is

A: -22.6%

B: -21.1%

C: -14.5%

14-21. This problem requires the ranking of bonds based on price volatility as measured by

the duration of each bond. (For simplicity, all bond prices assume annual interest payments.

The usage of semi-annual payments does not affect the rankings.)

a. The prices of each bond:

b. The duration (D) of each bond:

c. The durations suggest that the volatility of the bond is

C, A, E, D, B, and F

d. The prices of the bonds if interest rates rise to 12 percent:

A: $60(3.605) + $1,000(.567) = $783.30

Percentage change in each bond’s price:

A: -11.3%

B: -24.0%

C: -10.2%

D: -20.9%

E: -12.7%

F: -41.9%

Ranking according to actual price volatility is C, A, E, D, B, and F which confirms the

ranking according to the duration calculations.

e. The generalizations are

a. low coupons are associated with longer duration

b. bonds with same coupons but longer terms to maturity

c. the term of a zero coupon bond equals its duration.

14-22. The duration for the bond:

The equation for the change in a bond’s price is

When interest rates rise from 9% to 9.2%, the forecasted change in the bond’s price is

and bond’s forecasted new price will be $1,000 – 12.83 = $987.

The forecasted prices of the bond at each interest rate are

Interest Duration Change in Forecasted

Rate Bond Price Price

9.2 6.995 -$13 $987

9.4 6.995 -26 974

Actual values of the bonds versus the forecasted values:

Interest Value of Forecasted Differential

Rate the Bond Price

9.2 $987 $987 $0

9.4 975 974 -1

The duration accurately predicts the change in the price of the bond for small changes in

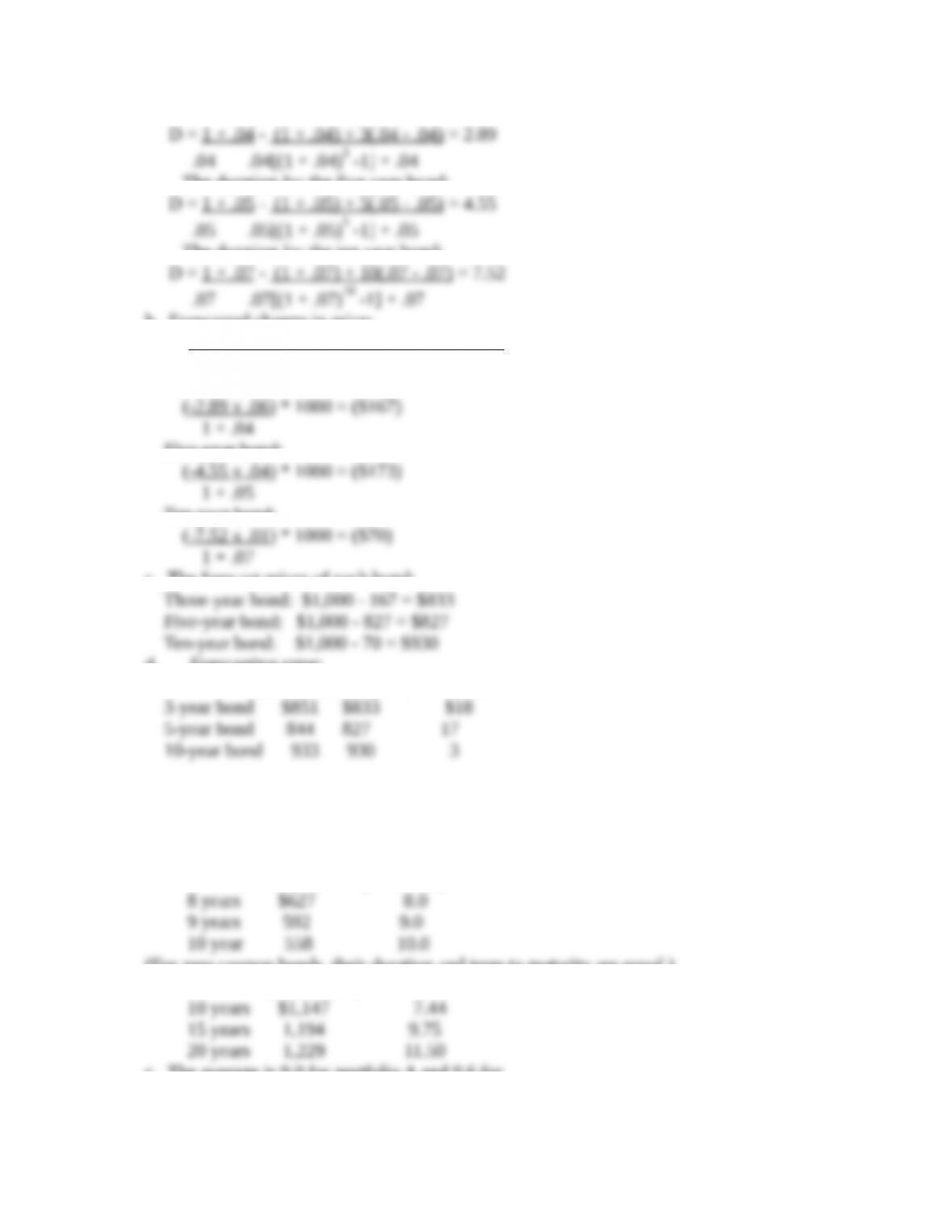

14-23. a. The duration for the three year bond:

The duration for the five year bond:

The duration for the ten year bond:

b. Forecasted change in price:

(-duration x change in the yield to maturity) x 1000

1 + yield to maturity

Three-year bond:

Five-year bond:

Ten-year bond:

c. The forecast prices of each bond:

d. Forecasting error:

Price Forecasted price Difference

Notice that the forecast errors are small for small changes in interest rates.

14-24. a. The longer maturities of the bonds in Portfolio B suggests that it is the riskier of

the two portfolios.

b. Term Bond Price Bond Duration

Portfolio A (zero coupon bonds)

(For zero coupon bonds, their duration and term to maturity are equal.)

Portfolio B (term bonds)

c. The average is 9.0 for portfolio A and 9.6 for

portfolio B. The durations of the two portfolios are almost the same, so B is only marginally

riskier.

d. Portfolio A costs $1,777; portfolio B costs $3,570. After the change in interest rates, the

prices of the bonds are as follows:

Portfolio A (zero coupon bonds)

Portfolio B (term bonds)

Portfolio is now worth $1,276, a decline of 28.2 percent; portfolio B is worth $2,554, a

e. While portfolio B appears to be riskier than a, the difference is marginal once the duration

14-25. This problem raises the question of the return realized by different investors with

different expectations. Investor A expects the bond to be called and would be willing to pay

up to $1,122. Investor B does not expect the bond to be called and will be outstanding until

Both valuations are based on a yield of 6 percent. The price differences are the result of

different termination dates (five years for A and ten years for B).

At 6 percent: $80(7.360) + 1,000(.558) = $1,147, so at a price of $1,122, the return has to be

higher. The determination of the actual return, 6.32 percent, requires the use of a financial

Investor B was willing to pay up to $1,147 but purchased the bond for less. Since the $1,147

price would yield 6 percent if the bond were held to maturity, buying the bond for a lower

14-26. In the previous problems, the valuation of the bond uses the same interest rate to

discount each payment. That procedure is appropriate if the yield curve is flat. This problem

and the material in the appendix to the chapter consider the impact on valuation if the yield

curve is positively sloped and the different rates are used to discount each payment.

a. The price of each bond based on the five-year yield (10%):

b. Price of bond A based on the structure of yields:

Year Payment x Interest Factor = Value

1 $60 0.943 $56.58

Year Payment x Interest Factor = Value

1 $120 0.943 $113.16

2 120 0.873 104.76

c. Based on the valuations in (b), the yields to maturity are

Bond A:

Using a financial calculator, the yield to maturity is

N = 5; PMT = 60; FV = 1000; PV = -857.34; I = ? = 9.74

Bond B:

Using a financial calculator, the yield to maturity is

d. When the structure of yields is used to price the bonds, the yields to maturity are less than

e. If you could purchase a bond for $848.46 and remove the coupons (the interest payments),

you could sell each coupon and the final principal repayment separately. The total value of

each payment sold by itself is worth $857.34. The profit on the transaction is $8.88.

This process illustrates the creation of zero coupon bonds and the possibility of an arbitrage

profit.

Teaching Guides for the Financial Advisor’s Case: High Yield Securities and Relative Risk

Objectives: This problem is concerned with the price volatility of high yield relative to high

quality bonds. Since junk bonds tend to have higher coupons, their prices may be less

volatile than the prices of investment grade bonds. Investment grade bond safety is related to

the probability with which the investor will receive the interest and the principal repayment

but does not necessarily apply to bond’s response to changes in interest rate. Thus, the

investor is high yield securities may fare better than the investor who purchases quality debt

if interest rates rise and drive down the prices of all existing bonds.

To compare the price volatility, the student must compute each bond’s duration.

B-rated Coupon Price Yield to Duration Rank

bonds Maturity

A 10% $900 11.7% 6.58 1

B 15% 1200 12.1 7.33 4

C 0% 487 10.5 7.00 2

D 7% 772 10.8 7.14 3

AAA-rated Coupon Price Yield to Duration Rank

bonds Maturity

E 6.5% $900 8.0% 7.51 2

F 10.5% 1200 8.2 8.74 4

G 0% 587 7.8 7.00 1

H 4.5% 772 7.8 8.04 3

Bond price and percent change in price after the three percent increase in yields:

A $760 -15.6%

B 995 -17.1

C 411 -15.6

D 643 -16.7

E 736 -18.2

F 953 -20.6

G 489 -16.7

H 625 -19.0

Actual price volatility of B-rated bonds: A, C, D, B.

Actual price volatility of AAA-rate bonds: G, E, H, F

The comparisons of price declines:

The comparisons indicate that two bonds have the same term and initially sell for the same

price, the bond with the lower coupon will exhibit more price volatility. In the case of the

zero coupon bonds, the higher priced bond subjects the investor to more interest rate risk.

The obvious implication is that bonds with higher credit ratings may subject the investor to

greater interest rate risk than holders of bonds with lower credit ratings. The lower coupons

increase the bonds’ duration and decrease their price volatility.

Teaching Guides for the Financial Advisor’s Case: Risk Reduction through the Active

Management of a Bond Portfolio

1. Equipment trust certificates are issued in a series and are secured by the equipment they

finance. Since they are secured, there is less default risk.

2. At 8 percent the zero coupon bond should sell for

3. Since the amount needed is $210,000, the investor should acquire 210 zero coupon bonds

4. This question asked how much will the investor have at the end of ten years after

reinvesting the coupon payments at 8 percent.

This amount plus the $97,272 principal produces a terminal amount of $210,000. (Bond B

matures for $97,272 and bond C may be sold for $97,272.) All three portfolios meet the

objective.

5. The three portfolios meet their objective because interest rates have not changed and all

6. If interest rates rise, bond prices decline but the coupons are reinvested at the higher rate.

Bond C has eight years to maturity. Its coupons also earn $124,025 and it would sell for

$86,895.

7. In this question, the reinvestment rate declines to 5 percent. There is no impact on bond A

which matures and pays $210,000.

Bond B also matures and the reinvested coupons grow to $97,881.

(N = 8; I = 5; PMT = 7782; FV = 97,272; PV = -116,134.)

The terminal value is $97,881 + $116,134 = $214,015. Bond C does better than bond B, and

meets the objective. The gain in the value of the bond more than offsets the lost reinvested

interest.

8. The duration of bond A is equal to its term: 8 years. The duration of bond B is 7.3 years.

9. As the previous answers indicate, bonds A and C meet the objective if interest rates rise,

10. Matching the duration of the bond with when the funds are needed offsets interest rate