Chapter 14

Time Series Analysis and Forecasting

Learning Objectives

1. Be able to construct a time series plot and identify the underlying pattern in the data.

2. Understand how to measure forecast accuracy.

3. Be able to use smoothing techniques such as moving averages and exponential smoothing to forecast a

time series with a horizontal pattern.

4. Know how simple linear regression can be used to forecast a time series with a linear trend.

5. Be able to develop a quadratic trend equation and an exponential trend equation to forecast a time

series with a curvilinear or nonlinear trend.

6. Know how to develop forecasts for a time series that has a seasonal pattern.

7. Know how time series decomposition can be used to separate or decompose a time series into season,

trend, and irregular components.

8. Be able to deseasonalize a time series.

9. Know the definition of the following terms:

time series

mean squared error

time series plot

mean absolute percentage error

horizontal pattern

moving average

stationary time series

weighted moving average

trend pattern

smoothing constant

seasonal pattern

time series decomposition

cyclical pattern

additive model

mean absolute error

multiplicative model

Solutions:

1. The following table shows the calculations for parts (a), (b), and (c).

Week

Time Series

Value

Forecast

Forecast

Error

Absolute

Value of

Forecast

Error

Squared

Forecast

Error

Percentage

Error

Absolute Value

of Percentage

Error

1

18

2

13

18

-5

5

25

-38.46

38.46

3

16

13

3

3

9

18.75

18.75

4

11

16

-5

5

25

-45.45

45.45

5

17

11

6

6

36

35.29

35.29

6

14

17

-3

3

9

-21.43

21.43

Totals

22

104

-51.30

159.38

a. MAE = 22/5 = 4.4

b. MSE = 104/5 = 20.8

2. The following table shows the calculations for parts (a), (b), and (c).

Week

Time Series

Value

Forecast

Forecast

Error

Absolute

Value of

Forecast

Error

Squared

Forecast

Error

Percentage

Error

Absolute Value

of Percentage

Error

1

18

2

13

18.00

-5.00

5.00

25.00

-38.46

38.46

3

16

15.50

0.50

0.50

0.25

3.13

3.13

4

11

15.67

-4.67

4.67

21.81

-42.45

42.45

5

17

14.50

2.50

2.50

6.25

14.71

14.71

6

14

15.00

-1.00

1.00

1.00

-7.14

7.14

Totals

13.67

54.31

-70.21

105.86

a. MAE = 13.67/5 = 2.73

b. MSE = 54.31/5 = 10.86

3. The following table shows the measures of forecast error for both methods.

Exercise 1

Exercise 2

MAE

4.40

2.73

MSE

20.80

10.86

MAPE

31.88

21.18

4. a.

Month

Time Series

Value

Forecast

Forecast

Error

Squared

Forecast

Error

1

24

2

13

24

–11

121

3

20

13

7

49

4

12

20

-8

64

5

19

12

7

49

6

23

19

4

16

7

15

23

-8

64

Total

363

Forecast for month 8 = 15

b.

Week

Time Series

Value

Forecast

Forecast

Error

Squared

Forecast

Error

1

24

2

13

24.00

-11.00

121.00

3

20

18.50

1.50

2.25

4

12

19.00

-7.00

49.00

5

19

17.25

1.75

3.06

6

23

17.60

5.40

29.16

7

15

18.50

-3.50

12.25

Total

216.72

MSE = 216.72/6 = 36.12

c. The average of all the previous values is better because MSE is smaller.

5. a.

The data appear to follow a horizontal pattern.

b. Three-week moving average.

Week

Time Series

Value

Forecast

Forecast

Error

Squared

Forecast

Error

1

18

2

13

3

16

4

11

15.67

-4.67

21.78

5

17

13.33

3.67

13.44

6

14

14.67

-0.67

0.44

Total

35.67

MSE = 35.67/3 = 11.89.

The forecast for week 7 = (11 + 17 + 14) / 3 = 14

c. Smoothing constant = .2

Week

Time Series

Value

Forecast

Forecast

Error

Squared

Forecast

Error

1

18

2

13

18.00

-5.00

25.00

3

16

17.00

-1.00

1.00

4

11

16.80

-5.80

33.64

5

17

15.64

1.36

1.85

6

14

15.91

-1.91

3.66

Total

65.15

MSE = 65.15/5 = 13.03

The forecast for week 7 is .2(14) + (1 – .2)15.91 = 15.53

d. The three-week moving average provides a better forecast since it has a smaller MSE.

e. Smoothing constant = .4

Week

Time Series

Value

Forecast

Forecast

Error

Squared

Forecast

Error

1

18

2

13

18.00

-5.00

25.00

3

16

16.00

0.00

0.00

4

11

16.00

-5.00

25.00

5

17

14.00

3.00

9.00

6

14

15.20

-1.20

1.44

Total

60.44

MSE = 60.44/5 = 12.09

The exponential smoothing forecast using α = .4 provides a better forecast than the exponential

smoothing forecast using α = .2 since it has a smaller MSE.

6. a.

The data appear to follow a horizontal pattern.

Three-week moving average.

Week

Time Series

Value

Forecast

Forecast

Error

Squared

Forecast

Error

1

24

2

13

3

20

4

12

19.00

-7.00

49.00

5

19

15.00

4.00

16.00

6

23

17.00

6.00

36.00

7

15

18.00

-3.00

9.00

Total

110.00

MSE = 110/4 = 27.5.

The forecast for week 8 = (19 + 23 + 15) / 3 = 19

b. Smoothing constant = .2

Week

Time Series

Value

Forecast

Forecast

Error

Squared

Forecast

Error

1

24

2

13

24.00

-11.00

121.00

3

20

21.80

-1.80

3.24

4

12

21.44

-9.44

89.11

5

19

19.55

-0.55

0.30

6

23

19.44

3.56

12.66

7

15

20.15

-5.15

26.56

Total

252.87

MSE = 252.87/6 = 42.15

The forecast for week 8 is .2(15) + (1 – .2)20.15 = 19.12

Week

Time Series

Value

Forecast

Forecast

Error

Squared

Value of

Forecast

Error

1

24

2

13

24.00

-11.00

121.00

3

20

19.60

0.40

0.16

4

12

19.76

-7.76

60.22

5

19

16.66

2.34

5.49

6

23

17.59

5.41

29.23

7

15

19.76

-4.76

22.62

Total

238.72

The exponential smoothing forecast using α = .4 provides a better forecast than the exponential

smoothing forecast using α = .2 since it has a smaller MSE.

7. a.

Week

Time-Series

Value

4-Week

Moving

Average

Forecast

(Error)2

5-Week

Moving

Average

Forecast

(Error)2

1

17

2

21

3

19

4

23

5

18

20.00

4.00

6

16

20.25

18.06

19.60

12.96

7

20

19.00

1.00

19.40

0.36

8

18

19.25

1.56

19.20

1.44

9

22

18.00

16.00

19.00

9.00

10

20

19.00

1.00

18.80

1.44

11

15

20.00

25.00

19.20

17.64

12

22

18.75

10.56

19.00

9.00

Totals

77.18

51.84

b. MSE(4-Week) = 77.18 / 8 = 9.65

8. a.

Week

Time-Series

Value

Weighted Moving

Average Forecast

Forecast

Error

(Error)2

1

17

2

21

3

19

4

23

19.33

3.67

13.47

5

18

21.33

-3.33

11.09

6

16

19.83

-3.83

14.67

7

20

17.83

2.17

4.71

8

18

18.33

-0.33

0.11

9

22

18.33

3.67

13.47

10

20

20.33

-0.33

0.11

11

15

20.33

-5.33

28.41

12

22

17.83

4.17

17.39

Total

103.43

b. MSE = 103.43 / 9 = 11.49

Prefer the unweighted moving average here; it has a smaller MSE.

Week

Time Series

Value

Forecast

Forecast

Error

Absolute

Value of

Forecast

Error

Squared

Forecast

Error

Percentage

Error

Absolute Value

of Percentage

Error

1

17

2

21

17.00

4.00

4.00

16.00

19.05

19.05

3

19

17.40

1.60

1.60

2.56

8.42

8.42

4

23

17.56

5.44

5.44

29.59

23.65

23.65

5

18

18.10

-0.10

0.10

0.01

-0.56

0.56

6

16

18.09

-2.09

2.09

4.37

-13.06

13.06

7

20

17.88

2.12

2.12

4.49

10.60

10.60

8

18

18.10

-0.10

0.10

0.01

-0.56

0.56

9

22

18.09

3.91

3.91

15.29

17.77

17.77

10

20

18.48

1.52

1.52

2.31

7.60

7.60

11

15

18.63

-3.63

3.63

13.18

-24.20

24.20

12

22

18.27

3.73

3.73

13.91

16.95

16.95

Totals

28.24

101.72

65.67

142.42

Week

Time Series

Value

Forecast

Forecast

Error

Absolute

Value of

Forecast

Error

Squared

Forecast

Error

Percentage

Error

Absolute Value

of Percentage

Error

1

17

2

21

17.00

4.00

4.00

16.00

19.05

19.05

3

19

17.80

1.20

1.20

1.44

6.32

6.32

4

23

18.04

4.96

4.96

24.60

21.57

21.57

5

18

19.03

-1.03

1.03

1.06

-5.72

5.72

6

16

18.83

-2.83

2.83

8.01

-17.69

17.69

7

20

18.26

1.74

1.74

3.03

8.70

8.70

8

18

18.61

-0.61

0.61

0.37

-3.39

3.39

9

22

18.49

3.51

3.51

12.32

15.95

15.95

10

20

19.19

0.81

0.81

0.66

4.05

4.05

11

15

19.35

-4.35

4.35

18.92

-29.00

29.00

12

22

18.48

3.52

3.52

12.39

16.00

16.00

Totals

28.56

98.80

35.84

147.44

a. MSE for

= .1 = 101.72/11 = 9.25

MSE for

= .2 = 98.80/11 = 8.98

= .2 provides more accurate forecasts based upon MSE

b. MAE for

= .1 = 28.24/11 = 2.57

MAE for

= .2 = 28.56/11 = 2.60

= .1 provides more accurate forecasts based upon MAE; but, they are very close.

c. MAPE for

= .1 = 142.42/11 = 12.95%

MAPE for

= .2 = 147.44/11 = 13.40%

= .1 provides more accurate forecasts based upon MAPE

10. a. F13 = .2Y12 + .16Y11 + .64(.2Y10 + .8F10) = .2Y12 + .16Y11 + .128Y10 + .512F10

F13 = .2Y12 + .16Y11 + .128Y10 + .512(.2Y9 + .8F9) = .2Y12 + .16Y11 + .128Y10 + .1024Y9 + .4096F9

F13 = .2Y12 + .16Y11 + .128Y10 + .1024Y9 + .4096(.2Y8 + .8F8) = .2Y12 + .16Y11 + .128Y10 + .1024Y9 +

.08192Y8 + .32768F8

b. The more recent data receives the greater weight or importance in determining the forecast. The moving

averages method weights the last n data values equally in determining the forecast.

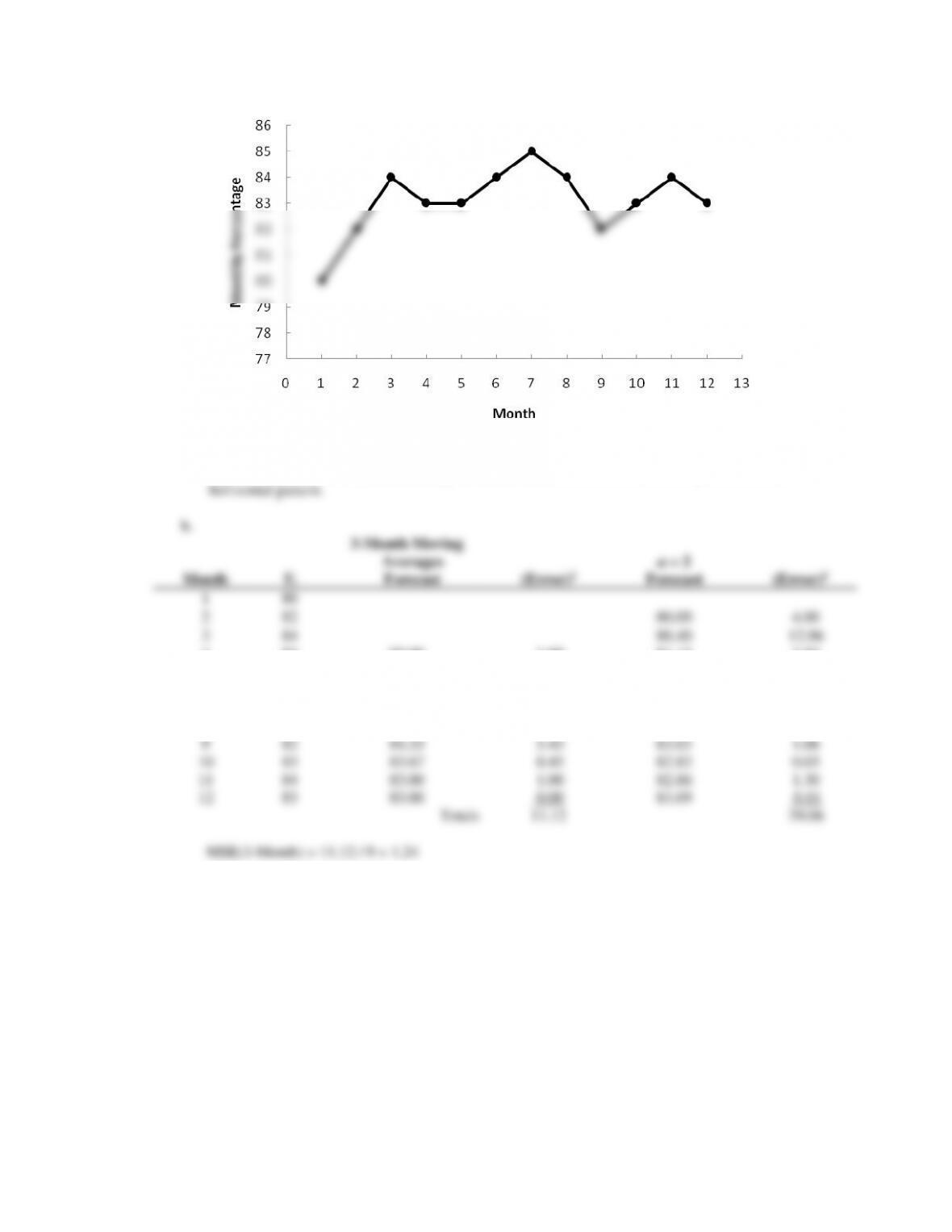

11. a.

The first two time series values may be an indication that the time series has shifted to a new

higher level, as shown by the remainig 10 values. But, overall, the time series plot exhibits a

Month

Time-Series

Value

3-Month Moving

Average Forecast

(Error)2

4-Month Moving

Average Forecast

(Error)2

1

9.5

2

9.3

3

9.4

4

9.6

9.40

0.04

5

9.8

9.43

0.14

9.45

0.12

6

9.7

9.60

0.01

9.53

0.03

7

9.8

9.70

0.01

9.63

0.03

8

10.5

9.77

0.53

9.73

0.59

9

9.9

10.00

0.01

9.95

0.00

10

9.7

10.07

0.14

9.98

0.08

11

9.6

10.03

0.18

9.97

0.14

12

9.6

9.73

0.02

9.92

0.10

Totals

1.08

1.09

MSE(3-Month) = 1.08 / 9 = .12

MSE(4-Month) = 1.09 / 8 = .14

Use 3-Month moving averages.

c. Forecast = (9.7 + 9.6 + 9.6) / 3 = 9.63

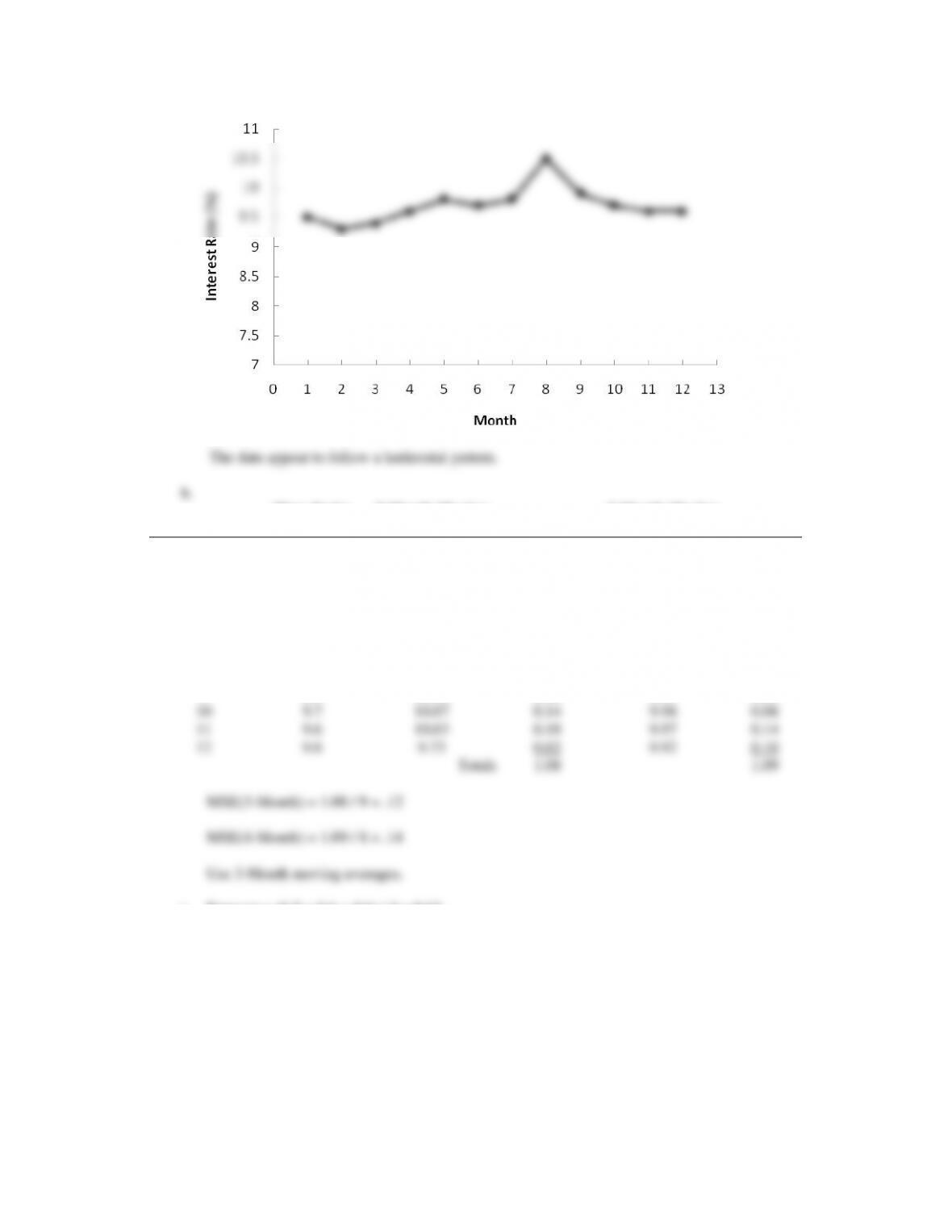

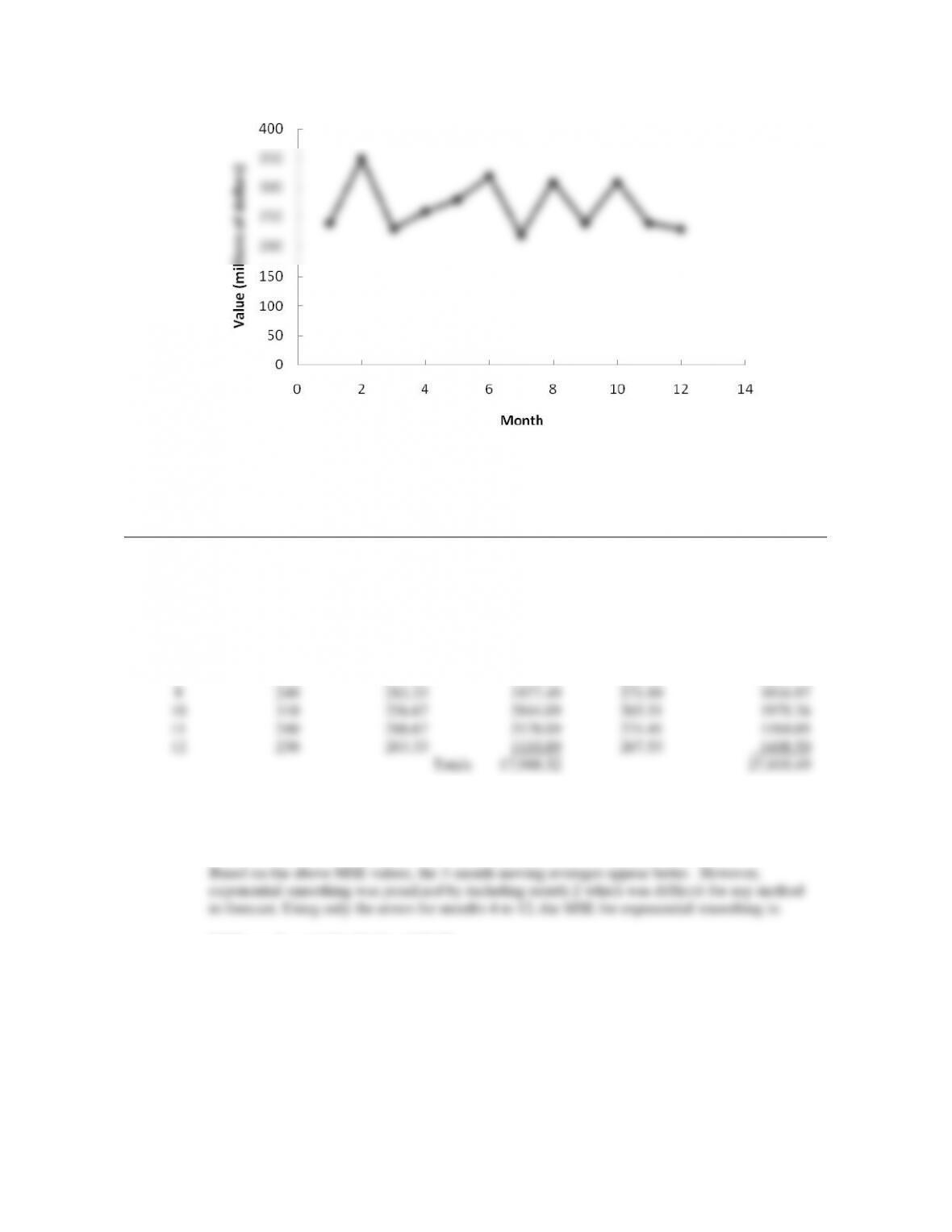

13. a.

The data appear to follow a horizontal pattern.

b.

Month

Time-Series

Value

3-Month Moving

Average Forecast

(Error)2

α = .2

Forecast

(Error)2

1

240

2

350

240.00

12100.00

3

230

262.00

1024.00

4

260

273.33

177.69

255.60

19.36

5

280

280.00

0.00

256.48

553.19

6

320

256.67

4010.69

261.18

3459.79

7

220

286.67

4444.89

272.95

2803.70

8

310

273.33

1344.69

262.36

2269.57

9

240

283.33

1877.49

271.89

1016.97

10

310

256.67

2844.09

265.51

1979.36

11

240

286.67

2178.09

274.41

1184.05

12

230

263.33

1110.89

267.53

1408.50

Totals

17,988.52

27,818.49

MSE(3-Month) = 17,988.52 / 9 = 1998.72

MSE(α = .2) = 27,818.49 / 11 = 2528.95

MSE(α = .2) = 14,694.49 / 9 = 1632.72

Thus, exponential smoothing was better considering months 4 to 12.

c. Using exponential smoothing,

F13 = α Y12 + (1 – α)F12 = .20(230) + .80(267.53) = 260