Key West Fisheries

Teaching Note

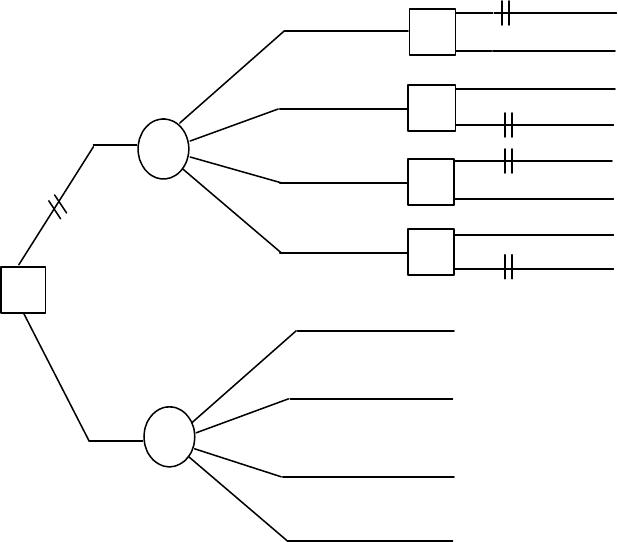

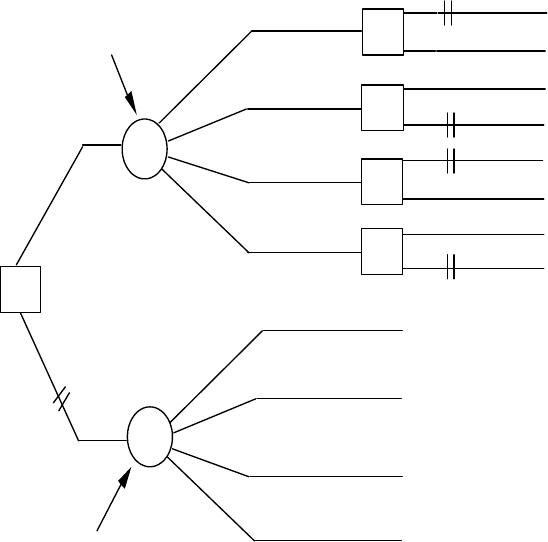

A decision tree describing Harry Morgan’s basic problem is shown below. If

Morgan rejects the contract, his monetary position at the end of the year

depends on the price of tuna and the size of his catch. The expected value of

this option is $49,500 after averaging over the four equally likely outcomes.

If Morgan accepts the contract, he locks in a fixed price for 150,000 pounds

of his catch, but the profit from his domestic sales is still uncertain. Thus, he

faces the same chance branches as in the reject decision. After learning about

the type of season(s) and the going price of tuna, he decides how to ship the

fish. Thus, there is a decision square at the end of each of the four chance

branches. He is free to make different shipping decisions in different types of

seasons.1 (This decision is simple since it is made after all uncertainty has

been resolved.)

The decision tree shows that his most profitable shipping decision depends

on the price of tuna. If the going price is $.80 or $1.00 (when the Pacific

catch is small), hiring the freighter is the more profitable option. If the going

price is $.50 or $.70 (when the Pacific catch is large), using his own boat

more profitable. There is an easy intuitive explanation for this result. When

domestic prices are high, the opportunity cost of using his own boat exceeds

the explicit cost of hiring the freighter. Accordingly the freighter is the better

option. Conversely, when domestic prices are low, doing it yourself costs

little and is the better option.

Comparing the expected values of the alternatives, we see that a risk-neutral

decision maker should reject the contract.

11 We have not shown one possible shipping option: transporting half the

catch by freighter and half by one’s own boat. The value of this option

always lies midway between the values of shipping all by freighter and all

by own boat. Thus, it is always worse than one of the “all or none”

alternatives and can be eliminated from consideration.

John Wiley & Sons

12-=

Freighter

Freighter

Freighter

Freighter

Boat

Boat

Boat

Boat

24

40

69

55

12

22

39

25

42.5

49.5

$.50

.25

$.80

.25

$.70

.25

$1.0 0

.25

0

90

18

90

Reject

Accept

40

69

22

39

$.50

.25

$.80

.25

$.70

.25

$1.0 0

.25

49.5

The following questions are typical vehicles for leading a class discussion of

this decision:

1. What are Morgan’s options? What are the associated risks? If he

accepts the contract, does he face an additional decision?

2. How does one use the answers above to draw the outline of Morgan’s

decision tree? At what point in the tree does the shipping decision occur?

(This last question is important since many students incorrectly put the

shipping decision “up front” – the same time the contract is signed.)

3. What are the monetary values to be listed at the branch tips?

4. Where should Morgan begin solving the tree? (This is another

important question. The analysis of any tree should begin with the last

decision — that is, the tree should be solved from right to left. Students

who forget this point are inclined to begin with the first decision.)

John Wiley & Sons

12-=

Additional Questions:

1. The option to postpone effectively gives Morgan perfect information

about price and catch before having to make the contract decision. The

appropriate decision tree is shown below. From the tree, we see that if the

domestic price is $.80 or $1.00 (when the Pacific catch is small), Morgan

should reject the contract. If the domestic price is $.50 or $.70 (when the

Pacific catch is large), Morgan should accept the contract and use his own

boat. The overall expected value is $60,500. Therefore, the expected value

afforded by this additional information is 60,500 – 49,500 = $11,000.

Freighter

Boat

Reject

Freighter

Boat

Reject

Freighter

Boat

Reject

Freighter

Boat

Reject

40

90

22

40

$.50

.25

$.80

.25

$.70

.25

$1.0 0

.25

60 .5

Delay

signing

24

40

0

69

55

90

12

18

39

25

90

22

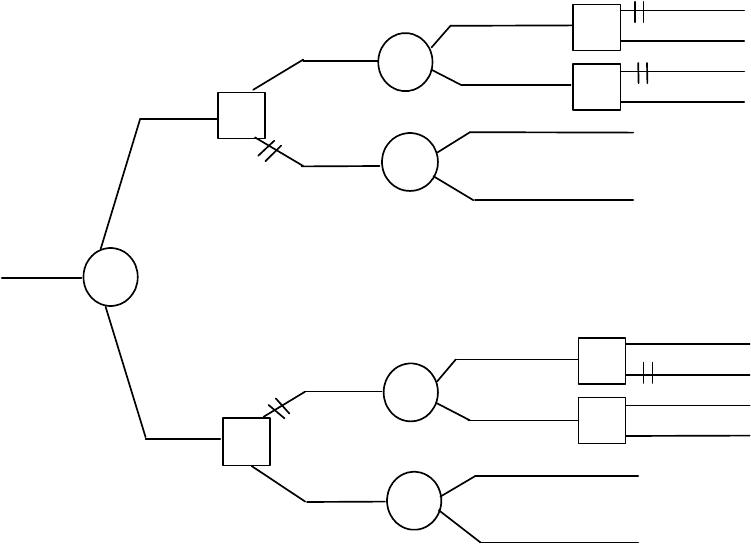

2. The decision tree below shows the situation when Morgan can acquire

perfect information about the Pacific catch (from a marine biologist)

before making his contract decision. Knowing that the Pacific catch is

large, Morgan should accept the contract and use his own boat. Knowing

that it is small, he should reject the contract. The expected value is

$60,500. This is exactly the same expected value as in question 1. After a

little reflection this should be no surprise. It happens that Morgan’s best

course of action depends only the Pacific season (and the resulting prices).

John Wiley & Sons

12-=

Knowing the Atlantic outcome as well (as in additional question 1) makes

no difference. Since the same decisions are made in either case, Morgan

obtains the same expected value.

31

Freighter

9

Atlantic Large

0

18

.5

Atlantic Small

.5

31

Reject

Accept

60.5

Marine

Biologist

.5

Pacific

Large

Pacific

90

.5

Small

54

90

Accept

Reject

22

24

40

Boat

40

Freighter

Boat

12

22

.5

.5

Atlantic Large

Atl. Small

39

69

69

Boat

55

Freighter

Boat

39

25

.5

.5

Atlantic Large

Atl. Small

Freighter

Atlantic Large

90

90

.5

Atlantic Small

.5

31

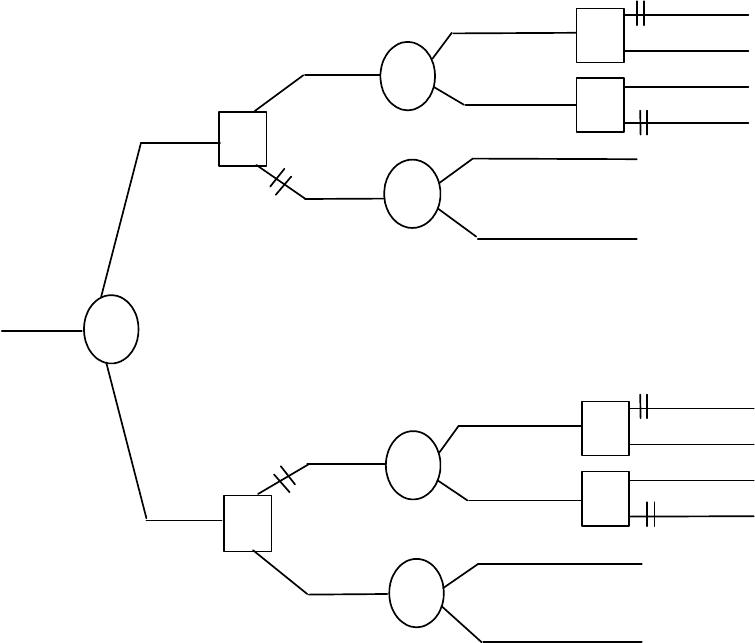

Extra Point. For different amounts of information, Morgan’s expected

values are:

— — $49,500

Atl — $54,250

— Pac $60,500

Atl Pac $60,500

Knowing the Pacific outcome, Morgan obtains no additional benefit from

also knowing the Atlantic. But what if Morgan does not know the Pacific

outcome? In this case, would information on the Atlantic outcome be of

any value? The answer is yes. As the tree below shows, Morgan’s

expected value is $54,250 (which is greater than $49,500).

John Wiley & Sons

12-=

31

Freighter

54.5

45

0

.5

.5

54.5

Reject

Accept

54.25

Marine

Biologist

.5

Atlantic

Large

Atlantic

.5

Small

Accept

Reject

24

40

Boat

40

Freighter

Boat

.5

.5

69

Boat

55

Freighter

Boat

39

25

.5

.5

Freighter

90

.5

.5

Pacific Large

Pac. Small

69

69

55

90

Pacific Large

Pacific Small

54

54

30.5

Pacific Large

Pac. Small

Pacific Large

Pacific Small

22

39

18

This demonstrates an important point explored in Chapter Thirteen. The

value of additional information depends in part on the amount of

information a manager starts with.

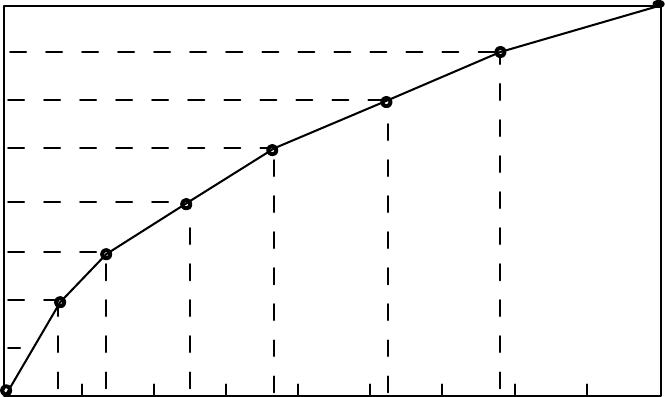

3. Set U(0) = 0 and U(90) = 100. Then, Morgan’s certainty equivalents

for the 50-50 gambles establish the following utility values:

U(24) = 50, U(52) = 75, U(6) = 25, U(69) = 87.5, U(35) = 62.5,

U(13) = 37.5.

In the graph below, we have drawn free hand a smooth utility curve going

through these points. Then, we have reproduced the original decision tree

with utility values at the end points (as read roughly from the graph).

John Wiley & Sons

12-=

The decision tree shows that accepting the contract delivers the higher

expected utility. For the risk-averse Morgan, this is the better course of

action. By reading from vertical axis to horizontal axis on the graph, we

find the certainty equivalent of accepting the contract to be about $40,000.

(Because rejecting the contract is very risky, its certainty equivalent is

lower than the CE of accepting the contract, even though its expected

value is higher.)

Utility 10 0

010 20 30 40 50 60 70 80 90

75

50

25

0

Wealth ($ Thousands)

John Wiley & Sons

12-=

Freighter

Freighter

Freighter

Freighter

Boat

Boat

Boat

Boat

24 (50 )

40 (67)

69 (87.5)

55 (77)

12 (36)

22 (48)

39 (66)

25 (51)

67.1

61

$.50

.25

$.80

.25

$.70

.25

$1.0 0

.25

0 (0 )

90 (10 0 )

18 (44)

90 (10 0 )

Reject

Accept

67

87.5

48

66

$.50

.25

$.80

.25

$.70

.25

$1.0 0

.25

CE = $40 K

CE = $34 K

IV. Quips and Quotes

I was expecting this but not so soon. (Written on a Tombstone in Boot Hill)

You can get more with a kind word and a gun than you can get with a kind

word. (Gangster Al Capone on the virtues of diversification)

If at first you don’t succeed, try, try again. Then stop. No use being a damn

fool about it. (W.C. Fields)

If you start to take Vienna, take Vienna. (Napoleon Bonaparte)

What men really want is not knowledge but certainty.

If Hell is paved with good intentions, it is largely because of the impossibility

of foreseeing consequences. (Aldous Huxley)

John Wiley & Sons

12-=

So far indeed are men in business from knowing the conditions on which

future prices and profits depend that they are often ignorant after the event of

the causes of their past profit and losses. (Thomas Leslie)

They couldn’t hit an elephant from this dis-. . . (The dying words of Civil

War General, John Sedgewick)

Ready, fire, aim. (A confused sequential decision?)

A man jumps from a skyscraper. As he passes the 20th floor, “So far, I don’t

see any problems.”

What do you do when you see a banker jumping out the window? Follow

him. There must be money to be made down there.

The contempt of risk and the presumptuous hope of success are in no period

of life more active than at the age at which young people choose their

professions. (Adam Smith)

John Wiley & Sons

12-=