CHAPTER TWELVE

DECISION MAKING UNDER UNCERTAINTY

OBJECTIVES

1. To review the notions of uncertainty, probability, and expected value.

(Uncertainty Probability and Expected Value)

2. To show how to draw decision trees and average them back. (Decision Trees)

3. To explore sequential decisions. (Sequential Decisions)

4. To introduce the concept of risk aversion. (Risk Aversion)

5. To show how the manager can use the (more general) criterion of expected

utility. (Expected Utility)

TEACHING SUGGESTIONS

I. Introduction and Motivation

A. Business Risks.

An easy way to introduce this topic is to ask students to prepare to answer the

discussion question at the end of Chapter 12. The discussion can begin with the

case of Olestra, Procter & Gamble’s miracle no-fat substitute and then move on to

a categorization of business risks in general. (The class usually comes up with a list

of risk categories like the one on the next page.)

Business Risks

I. Macro risks:

• GNP growth: boom or recession; how this affects firm’s future sales.

• Inflation: effect on input and output prices and wage demands

• Interest rates: given future movements in interest rates, when is the best time

to borrow to meet the firm’s investment needs?

• Exchange rate changes: important for overseas sale and production

II. Micro Risks

• Predicting demand: for a new product, the impact of advertising

• Predicting costs: R&D cost, cost of building a new facility, day-to-day

operating costs, changes in input costs and/or availability.

III. Competitive Uncertainty

• Will new competitors enter the market?

• Will current competitors cut prices, increase output, raise advertising, and so

on?

• Will ours be the winning bid for a valuable procurement contract?

• Will a competitor sue for patent infringement? If so, at what terms might the

competitor be willing to settle? Should the firm fight the suit in court?

IV. Government/political uncertainty.

• Regulation: will it be imposed and at what cost? Tax treatment?

• International relations and political risks

V. Scientific (or Natural) Uncertainty

• Will the firm’s well strike oil?

• Are we winning or losing the war on cancer?

• Will the firm’s scientific approach lead to a successful R&D outcome?

• Natural disasters, war, acts of God, the weather, global warming.

B. Guinea Pig Questions

1. $500,000, Take it or leave it?

a. In 1975, a 22-year women sued a New York hospital and two doctors for

administering too much oxygen following her birth (two months premature).

The woman grew up nearly totally blind. The case went to trial, and while

the jury was deliberating its verdict, the hospital’s lawyers offered a

settlement of $165,000. Would you advise her to accept this settlement?

b. In 1976, the parents of a seven-year old boy sued a Maryland hospital for

$3.5 million in a similar case. Born two weeks premature, the boy was

blinded shortly after birth allegedly because too much oxygen was given.

Again, the case went to trial, and during jury deliberations, the family

received a settlement offer of $500,000. Would you advise them to accept?

2. Escalating Investments in R&D An electronics firm can initiate an important

R&D program by making a $3 million investment. There is a 1/5 chance that

the program will meet with immediate success (i.e. within the year) earning the

firm a return of $10 million (for a net profit of $7 million). If success does not

come, the firm can invest another $3 million and raise its success chances to

1/4. If this second stage fails, the firm can invest again, and so on, up to a total

of five investments. The investment cost for each stage is $3 million, the

ultimate return from a successful completion of the program (sooner or later) is

$10 million, and the chances of success are 1/5, 1/4, 1/3, 1/2, and 1 for the

investments. As the manager in charge of this decision, would you make the

initial $3 million investment and if so, at what stage (if any) would you stop?

3. Which Cab Did It? Two taxi companies, Blue Cab Co. and Green Cab Co.,

serve a city. Blue cabs make up 85% of all taxies. A witness to a hit-and-run

accident at twilight believes he saw a green cab leave the scene. The witness is

found to be 80% accurate in distinguishing green and blue cabs (under twilight

conditions). What are the chances that a green cab did it? (This question relies

on probability revisions taken up in Chapter Thirteen.)

4. Monday Morning Quarterbacking. In the 1984 Orange Bowl game,

Nebraska trailed Miami by 14 points in the second half. Nebraska scored a

touchdown and kicked the extra point to close the gap to seven points. Then, in

the closing seconds of the game, Nebraska scored a dramatic touchdown to

draw within one point. If it successfully kicked the extra point, the game would

end in a tie. If it attempted a two-point conversion, it would win or lose the

game depending on whether or not the attempt succeeded. Nebraska attempted

to pass for the two-point conversion. The pass failed, and Nebraska lost the

game and the mythical national championship of college football.

Analyze Nebraska’s decisions to attempt the one-point and two-point

conversions after its first and second touchdowns in the second half. In your

analysis, assume that (1) kicking a one-point conversion is a certainty; (2) a

two-point conversion has a .5 chance of succeeding; and (3) Nebraska is

indifferent between a tie and a 50-50 chance of winning or losing. What is

Nebraska’s optimal strategy?

C. Guinea Pig Questions, Discussed

1. In either instance, your decision to accept or reject the settlement depends on

your assessment of the expected monetary award (net of legal fees) in court. You

would be wise to question your lawyers closely about the strength of the case,

the chances of various court outcomes (including appeals), and the possible

monetary awards. In each instance, the

plaintiff accepted the settlement. After accepting $165,000, the woman learned

that the jury would have awarded her $900,000. In the family’s case, the jury

would have awarded them nothing. This is a good example to show the

difference between good and bad decisions versus good and bad outcomes.

2. See the discussion and decision tree in Chapter 13, pp. 559-561.

3. Most students believe that the chances are 60% or greater that the green cab did

it. Many think that chance is 80% (reflecting the witness’s degree of accuracy).

The correct answer is 12/29 or about 41%. To see this, suppose that cabs of one

company are no more prone to such behavior than the cabs of the other. If we

imagine 100 such accidents, 85 would involve blue cabs and 15 green cabs. The

green cab accidents would generate (.8)(15) = 12 correct green sightings. The 85

blue cab accidents would generate (.2)(85) = 17 incorrect green sightings. Thus,

of 29 green sightings, 12 are actually caused by green cabs.

4. Consider two of Nebraska’ possible strategies: (1) kicking after each touchdown

secures a tie; (2) kicking now and trying the two-point conversion after the

second touchdown offers a 50/50 chance of winning (if the conversion

succeeds) or losing (if the conversion fails). According to the coach’s stated

preferences, Nebraska is indifferent between these two options. However, there

is a third and better option: (3) attempting the two-point conversion now. If it

succeeds, kick the point after the second touchdown (for a one-point win). If it

fails, go for two points after the second touchdown (in the hopes of salvaging a

tie). This strategy offers a 50 percent chance of a win (whenever the first

conversion succeeds), a 25 percent chance of a tie (the first attempt fails, the

second succeeds), and only a 25 percent chance of a loss (if both attempts fail).

This strategy “dominates” the second strategy, i.e., it provides a lower chance of

a loss and the same chance of a win.

II. Teaching the “Nuts and Bolts”

A. The basic oil drilling problem implies the simplest possible decision tree: one

safe action, one risky action with only two possible outcomes. It is a good

vehicle for talking about: a) probabilities (that they are subjective and subject

to revision, i.e. not etched in stone) and b) the meaning of expected value.

Check station 2 extends the example to a sequential decision.

B. Developing an anti-clotting drug is a more complicated sequential decision.

We usually present a streamlined discussion which includes:

a) comparing the expected profits of each separate method;

b) drawing the decision tree for simultaneous development (reminding students

of the product rule for independent probabilities and that the company will

only commercialize the more profitable method, not both);

c) showing via a decision tree that an optimal sequential decision is to try the

riskier R&D method first.

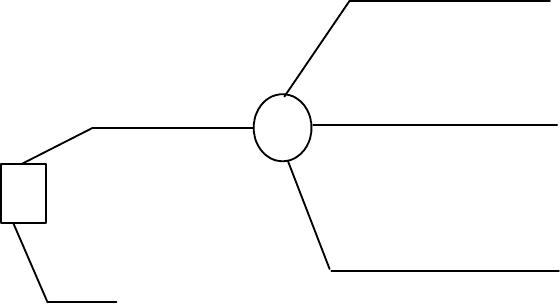

C. Launching a new product Here is an alternative extended example that can

be used in class to cover the “nuts and bolts” of Chapters Twelve and Thirteen.

A firm faces the decision as to whether to launch a new product. The decision

tree is:

$0

Not

5.92 $10 million

moderate economy

.40

-$22 million

recession

.24

$20 million

booming economy

.36

Launch

The firm’s business economists think the most likely outcome is moderate

growth (a 40 percent chance). If moderate growth does not materialize, they

see a booming economy as more likely than a recession by odds of 3 to 2.

Note: If you wish, you can supply a complete economic explanation for the

launch payoffs. Here is one possible example:

The firm’s fixed cost is $30 million and its MC is $2/unit.

Demand is:

P = 12 – .5Q in a boom economy (so that Q* = 10 and P* = 7),

P = 11 – .5Q in a moderate economy, (so that Q* = 9 and P* = 6.5)

P = 6 – .5Q in a recession (so that Q* = 4 and P* = 4).

Here Q is in millions of units. The respective profits are $20 million, $10.5

million, and -$22 million, close to the round numbers above. As the decision tree

shows, the best course of action for a risk-neutral firm is to launch the product.

To carry out the analysis if management is risk averse, let utility values be:

U(20) = 100, U(-20) = 0, U(10) = 90, and U(0) = 70.

It follows that:

E(Ulaunch) = (.36)(100) + (.4)(90) + (.24)(0) = 72,

which is just slightly better than the utility of not launching, U(0) = 70.

D. Suggested Problems

Problems 4, 6, 8, 10, 13

E. Risk Aversion and Expected Utility. Here is an important topic that in some

respects is hard to handle. The presentation in the text takes the middle road –

by discussing risk aversion in general terms and then showing how a manager

can quantify his attitude toward risk by assessing utility values.

i) For an instructor who wants to devote minimal time to this topic, we

suggest omitting the section in the text on Expected Utility. The instructor

can stress the consequences of risk aversion (the demand for insurance, the

tradeoff between risk and return, the evaluation of safety risks) and note

that risk aversion implies declining marginal utility.

ii) An instructor who wants to do more on this topic might look more closely

at the assumptions underlying expected utility and discuss actual choices

under uncertainty (which often violate the expected utility axioms).