CHAPTER 17

EXCHANGE RATES

AND MACROECONOMIC POLICY

MASTERY GOALS

The objectives of this chapter are to:

1. Describe what a foreign exchange market is.

2. Explain what an exchange rate is, and why it is helpful to define the exchange rate as

“dollars per unit of foreign currency.”

3. Explain why the demand curve for a foreign currency is downward sloping.

4. List the variables that cause the demand curve for a currency to shift, and describe

whether changes in these variables shift the demand curve rightward or leftward.

5. Explain why the supply curve for a foreign currency is upward sloping.

6. List the variables that cause the supply curve for a currency to shift, and describe whether

changes in these variables cause the supply curve to shift rightward or leftward.

7. Describe how floating exchange rates are determined, using the concepts of excess

supply and excess demand.

8. Define the terms currency appreciation and currency depreciation.

9. Describe how hot-money movements lead to exchange rate changes over the very

short run.

10. Describe how economic fluctuations lead to exchange rate changes over the short run.

11. Use the purchasing power parity (PPP) theory to describe long-run exchange rate

adjustments, and explain why adjustment to purchasing power parity is less than

complete.

12. Discuss why the currency of a country with a higher inflation rate will depreciate against

the currency of a country whose inflation rate is lower.

13. Explain why a country’s central bank might intervene in foreign exchange markets to

influence floating exchange rates under a “managed float.”

14. Describe how a country achieves a fixed exchange rate, and the problems created when

the exchange rate is fixed above the equilibrium rate for a long period.

15. Describe the concept of moral hazard and use this concept to explain why intervention by

the International Monetary Fund (IMF) to help countries recover from foreign currency

crises is controversial.

16. Explain how changes in exchange rates affect equilibrium GDP.

17. Explain why monetary policy effectiveness is enhanced by exchange rate changes.

18. Explain how a net financial inflow can lead to a trade deficit.

THE CHAPTER IN A NUTSHELL

This chapter examines the markets where Americans exchange dollars for other currencies, and

expands the text’s analysis of the macroeconomy to include trading with other nations. It

explores the relationship between foreign exchange markets and our economy, and the effects of

monetary policy in an open economy.

One country’s currency is traded for that of another in a foreign exchange market. The exchange

rate is the rate at which one currency is traded for another. So that we can think of the exchange

rate as the price (in dollars) of foreign currency, this chapter always defines the exchange rate as

“dollars per unit of foreign currency.”

This chapter develops a model of supply and demand for British pounds, under the assumption

that American households and businesses are the only buyers of pounds, and British households

and businesses are the only sellers of pounds. The demand curve for British pounds is downward

sloping because as the exchange rate falls British goods and services are less expensive to

American buyers. The lower the price of the pound, the more British goods Americans will buy,

and the more pounds they will need to make their purchases. This demand curve will shift in

response to changes in U.S. real GDP, the U.S. price level relative to the British price level,

Americans’ tastes for British goods, relative interest rates in the United States, and expectations

about future exchange rates.

The supply curve for British pounds is upward sloping because as the exchange rate rises the

British will get more dollars for each pound traded. This makes U.S. goods less expensive to

British buyers. As they buy more American goods, they will need to supply more pounds in order

to get dollars. The variables that will shift the supply curve include real GDP in Britain, the U.S.

price level relative to the British price level, British tastes for U.S. goods, relative interest rates in

the United States, and expectations about changes in the interest rate.

A floating exchange rate is freely determined by the forces of supply and demand, without

government intervention to change it or keep it from changing. When the exchange rate floats,

equilibrium occurs at the price where the quantity of foreign currency (pounds) demanded equals

the quantity supplied.

An increase in the demand for pounds or a decrease in the supply of pounds leads to an

appreciation of the pound (and a depreciation of the dollar). A decrease in the demand for pounds

or an increase in the supply of pounds leads to a depreciation of the pound (and an appreciation

of the dollar).

There are three types of exchange rate movements: very short-run changes, short-run changes,

and long-run trends.

Decisions by banks and other large financial institutions to move billions of dollars from one

country to another are responsible for exchange rate changes in the very short run. These

decisions to move “hot money” are made in split seconds in response to changes in relative

interest rates and expectations of future exchange rates.

Economic fluctuations are the main cause of short-run exchange rate changes. Generally, a

country whose GDP rises relatively rapidly will experience a depreciation of its currency, and

vice versa.

In the long run, according to the purchasing power parity (PPP) theory, an exchange rate will

adjust until the average price of goods is roughly the same in both countries. The existence of

non-tradable goods, high transportation costs, and artificial trade barriers all limit such perfect

price adjustment. An important implication of PPP theory is that the currency of a country with a

higher inflation rate will depreciate against the currency of a country whose inflation rate is

lower.

Governments sometimes intervene in foreign exchange markets involving their currency. They

may choose to intervene in foreign exchange markets when high exchange rates are harming

export-oriented industries, when falling exchange rates are leading to a general rise in domestic

prices, and when volatile exchange rates are making trading arrangements risky. Under a

managed float, a country’s central bank buys its own currency to prevent a depreciation, and sells

its own currency to prevent an appreciation. A more extreme form of intervention is a fixed

exchange rate, in which a government declares a particular value for its exchange rate with

another country and then, through its central bank, commits itself to intervene anytime the

equilibrium exchange rate differs from the fixed rate.

A foreign currency crisis is a loss of faith that a country can prevent a drop in its exchange rate,

and leads to a rapid depletion of its foreign currency. Thailand’s financial crisis of 1997-1998 is

explained using the concept of a foreign currency crisis. The International Monetary Fund (IMF)

resolved this crisis—an organization formed in large part to help nations avoid such foreign

currency crises and help them recover when crises occur. Such a rescue is controversial,

however, since it creates a moral hazard problem. Moral hazard occurs when a decision maker

expects to be rescued in the event of an unfavorable outcome, and then changes their behavior so

that the unfavorable outcome is more likely. The problem of moral hazard helps explain the

IMF’s response to Argentina’s foreign currency crisis of 2001-2002.

Exchange rates can have important effects on the macroeconomy—largely through their effect on

net exports. A dollar depreciation causes net exports to rise and leads to an increase in real GDP

in the short run. A dollar appreciation does just the opposite. When we include the impact on

exchange rates and net exports, we find that monetary policy has a stronger effect on the

economy than initially described.

A country’s trade deficit measures the extent to which its imports exceed its exports. When

exports exceed imports, a nation has a trade surplus.

The United States has a trade deficit with the rest of the world since the early 1980s because of a

massive capital inflow that arose in the early 1980s and has grown larger since. A rise in U.S.

interest rates relative to interest rates abroad, coupled with America’s lead in exploiting the

Internet, led to this net financial inflow. The net financial inflow has contributed to an

appreciation of the dollar. This appreciation causes exports to fall and imports to rise, leading to

an increase in the trade deficit.

DEFINITIONS

Foreign exchange market: The market in which one country’s currency is traded for

another country’s.

Exchange rate: The amount of one country’s currency that is traded for one unit of another

country’s currency.

Demand curve for foreign currency: A curve indicating the quantity of a specific foreign

currency that Americans will want to buy, during a given period, at each different exchange rate.

Supply curve for foreign currency: A curve indicating the quantity of a specific foreign

currency that will be supplied, during a given period, at each different exchange rate.

Floating exchange rate: An exchange rate that is freely determined by the forces of supply

and demand.

Appreciation: An increase in the price of a currency in a floating-rate system.

Depreciation: A decrease in the price of a currency in a floating-rate system.

Purchasing Power Parity (PPP) theory: The idea that the exchange rate will adjust in the

long run so that the average price of goods in two countries will be roughly the same.

Managed “oat: A policy of frequent central bank intervention to move the exchange rate.

Fixed exchange rate: A government-declared exchange rate maintained by central bank

intervention in the foreign exchange market.

Devaluation: A change in the value of a currency from a higher fixed value to a lower fixed

value.

Foreign currency crisis: a loss of faith that a country can prevent a drop in its exchange

rate, leading to a rapid depletion of its foreign currency (e.g. dollar) reserves.

Trade deficit: The excess of a nation’s imports over its exports during a given period.

Trade surplus: The excess of a nation’s exports over its imports during a given period.

Net financial in”ow: An inflow of funds equal to a nation’s trade deficit.

TEACHING TIPS

1. Visit http://www.xe.com for up to the minute exchange rates.

2. Warn students that a lot of confusion about exchange rates results from a failure to

understand what is being sold in currency exchange transactions. Explain that currency

markets operate exactly like the markets for, say, oranges. Remind them that they learned

how to graph demand and supply curves for goods like oranges in Chapter 3. Ask them to

take a minute to draw the market for oranges and label the axes. At this point in the

course, they will be able to do this fairly effortlessly. Ask them which currency they are

using to measure the price per orange. They will, of course, assume that the price is stated

in U.S. dollars (assuming that your class is held in the U.S.). This assumption comes very

naturally to students, and once they understand that they are making this assumption,

they can apply it to the market for currency markets. At this point, show students the

following graphs and explain that this is how they should always think of currency

markets.

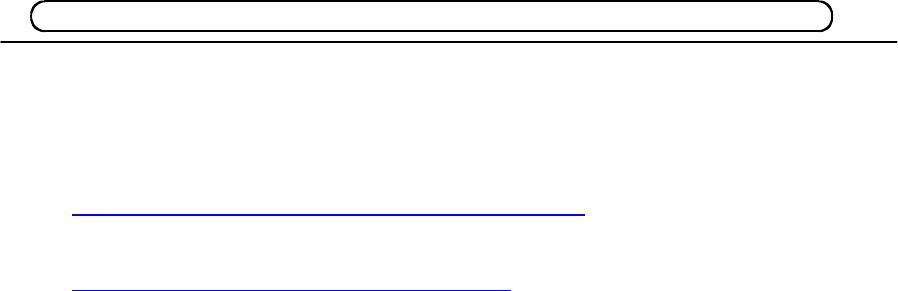

Price per

British Pound

(measured in

U.S. dollars)

Quantity of

British Pounds

Demanded

D

£

S

£

Price per

British Pound

(measured in

U.S. dollars)

Quantity of

British Pounds

Supplied

3. For a real-world example of how hot money can affect exchange rates and economies, see

David Roman, “Asian Countries to Tackle Fund Inflows Cautiously,” The Wall Street

Journal, November 25, 2009.

4. Motivate the discussion on managed float by talking about the Plaza Accord of 1985 and

the Louvre Accord of 1987. In both instances, the finance ministers of the five major

industrialized countries [the Group of Five (G5): France, Germany, Japan, the United

Kingdom, and the United States] decided to actively manage exchange rates. In 1985 a

strong U.S. dollar had contributed to a large U.S. trade deficit, and was undermining the

competitiveness of American corporations in the world market. In response to growing

American sentiment for protectionist policies, the G5 met at the Plaza Hotel in New York

and agreed to manipulate exchange rates to lower the value of the dollar. By 1987, the

dollar had depreciated to such an extent that the G5 met again (at the Louvre Museum in

Paris) and agreed to take steps to prevent its further decline.

5. Some students have a difficult time understanding why currencies don’t all have the same

value, that is, why 1 dollar ≠ 1 peso ≠ 1 baht, etc. Explain to them that each currency was

developed in a different time and place, just like pounds and kilograms were developed in

different locales. But all currencies are used to express prices, just like pounds and

kilograms are used to express weights. A measurement in one currency can be converted

to a measurement in a different currency, just like a measurement in kilograms can be

converted to a measurement in kilograms.

DISCUSSION STARTERS

1. The Mexican peso crisis of 1994–95 is useful for classroom discussion, because it

involves examples of many of the exchange rate concepts discussed in Chapter 29.

Students can read about this crisis in the January/February 1996 issue of the Atlanta Fed’s

Economic Review (available online at

http://www.frbatlanta.org/filelegacydocs/Espin811.pdf ).

2. Use the New York Fed’s foreign exchange operations news Web site at

http://www.ny.frb.org/markets/foreignex.html as the basis for a discussion of current

developments in foreign exchange markets.