CHAPTER 11

THE SHORT-RUN MACRO MODEL

MASTERY GOALS

The objectives of this chapter are to:

1. Explain the usefulness of the short-run macro model.

2. List the four components of aggregate expenditure included in the simple macro model of

this chapter.

3. List the determinants of consumption spending and describe their effects on consumption

spending.

4. Describe a consumption function in terms of autonomous consumption and the marginal

propensity to consume.

5. Show how changes in taxes and in autonomous consumption changes affect the

consumption-income line.

6. Explain why inventory investment is not included in aggregate expenditure.

7. Define government spending.

8. Define net exports.

9. Explain why investment, government spending, and net exports are assumed to be

determined by forces outside the short-run macro model.

10. Use a 45 translator line, together with the aggregate expenditure line, to show inventory

changes and to find the short-run equilibrium output level.

11. Explain why short-run equilibrium output is not necessarily full-employment output.

12. Use the multiplier to show how a change in spending affects equilibrium output in an

economy.

13. Give examples of automatic stabilizers/destabilizers and explain how they

reduce/increase the impact of changes in spending.

14. Discuss the size of multiplier in the real-world.

15. Use the short-run macro model of the chapter to explain the causes of the 2008–09

recession.

THE CHAPTER IN A NUTSHELL

The main purpose in building the short-run macro model is to explain fluctuations in real GDP

that the long-run, classical model cannot explain. The short-run macro model focuses on the role

of spending in explaining economic fluctuations. It explains how shocks that initially affect one

sector of the economy quickly influence other sectors, causing changes in total output and

employment. In this chapter, spending is the only force that determines how much output the

economy will produce.

The short-run macro model focuses on spending in markets for currently produced U.S. goods

and services—that is, spending on things that are included in U.S. GDP. Spending has four

components: (real) consumption spending, (real) investment spending, (real) government

purchases, and (real) net exports.

Consumption is positively related to real disposable income, real wealth, and expectations of

future income, and is negatively related to the interest rate.

The consumption function illustrates the relationship between consumption and disposable

income. Changes in disposable income lead to movements along the consumption function. The

slope of the consumption function is equal to the marginal propensity to consume, that is, the

amount by which consumption spending changes when disposable income rises by one dollar.

The vertical intercept represents autonomous consumption spending, the combined impact on

consumption spending of everything other than disposable income. Changes in wealth, the

interest rate, or expectations of future income lead to a change in autonomous consumption

spending. These changes are shown graphically as a shift of the consumption schedule.

The consumption-income line shows the relationship between real consumption spending and

real income, rather than real disposable income. When the government collects a fixed amount of

taxes from households, the consumption-income line shifts downward by the amount of the tax

times the MPC. The slope of the consumption-income line, however, is unaffected by taxes, and

is equal to the MPC.

A change in income causes consumption spending to change and leads to a movement along the

consumption-income line, while consumption spending changes that occur for any other reason

will cause the consumption-income line to shift. These other changes work by changing

autonomous consumption or taxes.

In the short-run macro model, (planned) investment spending includes plant and equipment

purchases by business firms, and new home construction. Inventory investment is treated as

unintentional and undesired, and is therefore excluded from the definition. Government

purchases include all of the goods and services that government agencies buy during the year.

Net exports equal exports minus imports. Export spending measures production sold to

foreigners, while import spending measures our spending on foreign output. Thus, to accurately

measure domestic output, we must add U.S. exports and subtract U.S. imports. These two

adjustments can be made together by simply including net exports as the foreign sector’s

contribution to total spending. Investment spending, government purchases, and net exports are

all treated as given values, determined by forces outside of this model.

Aggregate expenditure (AE) is the sum of spending by households, businesses, the government,

and the foreign sector on final goods and services. Since the relationship between income and

spending is circular, when income increases, aggregate expenditure will rise by the MPC times

the change in income.

When aggregate expenditure is less than GDP, output will decline in the future. Similarly, when

aggregate expenditure is greater than GDP, output will tend to rise in the future. Therefore, in the

short run, equilibrium GDP is the level of output where output and aggregate expenditure are

equal.

Output minus aggregate expenditures equals the change in inventories during any period. When

output equals aggregate expenditures, then inventory changes will equal zero, so another way to

find the equilibrium GDP in the economy is to find the output level where inventory changes are

equal to zero.

Graphically, equilibrium GDP is found at the intersection of the aggregate expenditure line and

the 45 line. At any output level where the aggregate expenditure line lies below the 45 line,

aggregate expenditure is less than GDP and inventory accumulation will cause firms to reduce

output in the future. At any output level where the aggregate expenditure line lies above the 45

line, aggregate expenditure is greater than GDP and inventory depletion will cause firms to

increase output in the future.

Operating at equilibrium does not guarantee full employment. If aggregate spending is too high

or too low, the aggregate expenditure line will cross the 45 line at some output level other than

full employment output, and the economy will remain at a short-run equilibrium where full

employment is not achieved.

Changes in spending—in investment, government purchases, or autonomous consumption—lead

to a multiplier effect on GDP, where the initial shock sets off a chain reaction, leading to

successive rounds of changes in spending and income. The expenditure multiplier is the number

by which the initial spending change is multiplied to get the change in equilibrium GDP. The

formula for the expenditure multiplier is 1/(1 – MPC).

Automatic stabilizers reduce the size of the multiplier, and therefore reduce the impact of

spending changes. They work by shrinking the additional spending that occurs in each round of

the multiplier. Some real-world automatic stabilizers are changes in taxes, transfer payments,

interest rates, imports, and forward-looking behavior. Perhaps the most important automatic

stabilizer of all is the passage of time—in the long run our multipliers have a value of zero. After

any change in spending, output will eventually return to full employment, so the change in

equilibrium GDP will be zero.

Automatic destabilizers increase the size of multiplier, and therefore increase the impact of

spending changes. They work by increasing the additional spending that occurs in each round of

the multiplier. Some real-world automatic destabilizers are asset prices and wealth, and

investment spending.

In the real world, the multiplier is impacted by both automatic stabilizers and automatic

destabilizers so coming a real value can be difficult. Economists generally agree that the current

number is smaller than it was during the Great Depression and most put the actual value in the

neighborhood of 1.5. In the long run, however, the value of the multiplier is zero.

The recession of 2008-09 was caused by a spike in oil prices and the collapse of the housing

bubble, as discussed in chapter 4. After the declines in spending fueled by the first two events,

the U.S. economy was hit by a third event: a serious financial crisis. All of these events caused

a significant decline in investment and consumption spending. Over time, as the multiplier

process took place, the decrease in spending brought down both GDP and employment.

There are two appendices to this chapter. The first explains how to use algebraic equations to

find equilibrium GDP, while the second explains the special case of the tax multiplier.

Short-run macro model: A macroeconomic model that explains how changes in spending

can affect real GDP in the short run.

Consumption function: A positively sloped relationship between real consumption

spending and real disposable income.

Autonomous consumption spending: The part of consumption spending that is

independent of income; also the vertical intercept of the consumption function.

Marginal propensity to consume: The amount by which consumption spending rises

when disposable income rises by one dollar.

Consumption-income line: A line showing aggregate consumption spending at each level

of income or GDP.

Aggregate expenditure (AE): The sum of spending by households, business firms, the

government, and foreigners on final goods and services produced in the United States.

Equilibrium GDP: In the short run, the level of output at which output and aggregate

expenditure are equal.

Expenditure multiplier: The amount by which equilibrium real GDP changes as a result of

a one-dollar change in autonomous consumption, investment spending, government purchases,

or net exports.

Automatic stabilizer: A feature of the economy that reduces the size of the expenditure

multiplier and diminishes the impact of spending changes on real GDP.

Automatic destabilizer: A feature of the economy that increases the size of the expenditure

multiplier and enlarges the impact of spending changes on real GDP.

1. Stress that, in the model of this chapter, firms want to keep output equal to sales, so that

inventory stocks won’t change. Thus, changes in inventories signal producers to increase

or decrease production. Explain that firms have optimal inventory levels. If actual

inventory falls below the optimal level, then firms risk not having merchandise on hand

to meet unpredictable peaks in demand. If actual inventory rises above the optimal level,

then firms incur excessive storage costs.

2. It is important to stress that investment spending (IP) is one of the spending aggregates

while actual investment (I) is a component of GDP. This means that while aggregate

expenditure is equal to the sum of C + IP + G NX, GDP is equal to the sum of C + I + G

NX. Emphasize to students that there is only one term that is different in these two

equations. Explain that, since this is the case, the only way that aggregate expenditures

can equal GDP is if IP is equal to I. This will help students see that in equilibrium,

investment spending and actual investment are equal.

DISCUSSION STARTERS

1. Have students look at the current state of the economy. (Refer to

hp://research.stlouisfed.org/fred/data/gdp/gdppot for potential real GDP !gures to

compare with actual real GDP numbers from www.bea.doc.gov/bea/dn/nipaweb ,

“Selected NIPA tables, table 1.2.” Refer to www.bls.gov for the unemployment rate and

changes in the CPI.) Discuss whether the economy appears to be at full employment. Do

they !nd con/icting evidence?

2. To emphasize the difference between the short-run macro model and the long-run

classical model, ask students how automobile manufacturers initially respond to an

overstock of cars. Some students may say that they offer rebates; point out that this

typically happens in slow markets but is not the first response. The first response is to lay

off workers until the glut disappears (they close the plant or reduce the number of shifts

for two weeks, or however long they deem necessary). Notice that the manufacturers do

not respond by cutting wages and car prices. Explain that this unemployment is predicted

by the short-run macro model, but is not predicted by the long-run classical model.

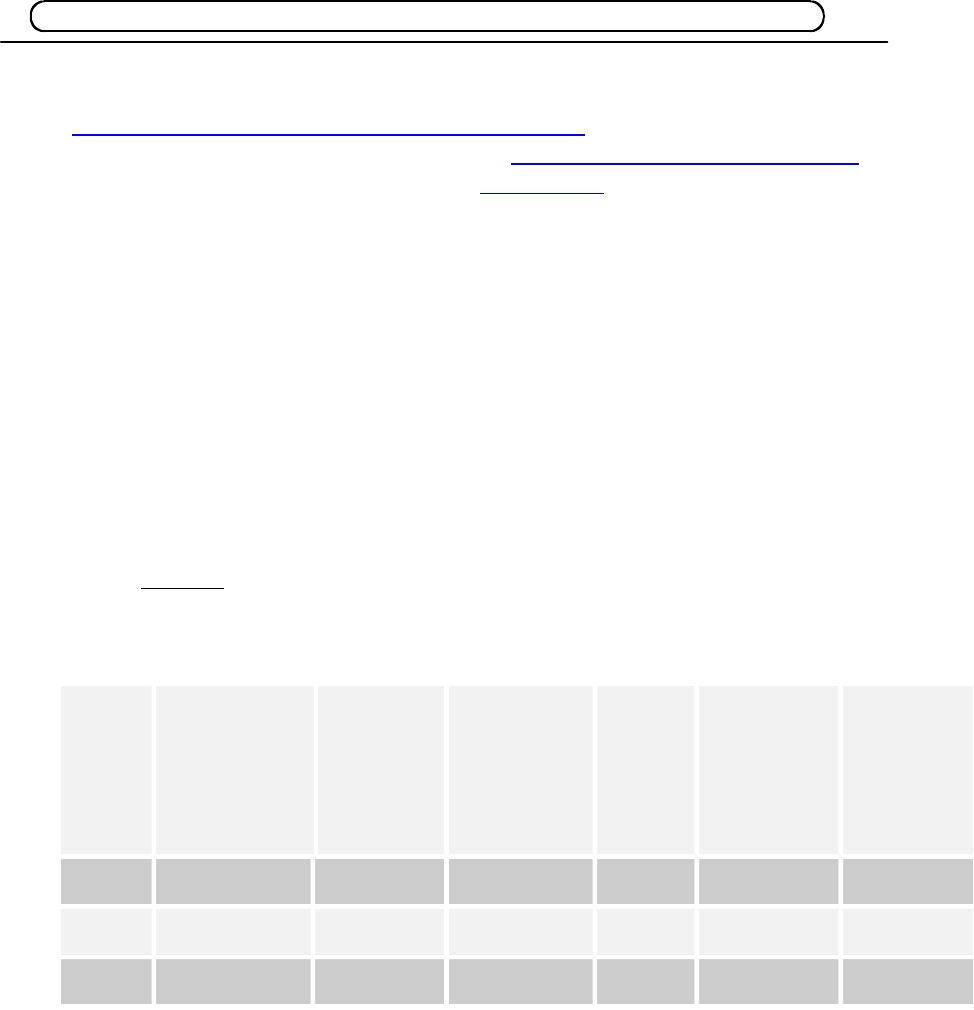

3. Recall the results from Table 4 in the chapter: when investment spending was equal to

$800 billion, the equilibrium GDP was $8,000 billion. Examine the effect of a $400

billion decrease in planned investment by reworking columns 3, 6, and 7 of the table, and

using the results to find the new equilibrium level of GDP. Check your results by using

the multiplier.

Answer:

(1)

Incom

e or

GDP

(2)

Consumptio

n Spending

(3)

Investme

nt

Spending

(4)

Governme

nt

Spending

(5)

Net

Export

s

(6)

Aggregate

Expenditur

e

(7)

Change

in

Inventori

es

4,000 3,200 400 1000 600 5,200 –1,200

5,000 3,800 400 1000 600 5,800 –800

6,000 4,400 400 1000 600 6,400 –400

7,00

0

5,000 400 1000 600 7,000 0

8,000 5,600 400 1000 600 7,600 400

9,000 6,200 400 1000 600 8,200 800

10,00

0

6,800 400 1000 600 8,800 1200

11,00

0

7,400 400 1000 600 9,400 1600

12,00

0

8,000 400 1000 600 10,000 2000

GDP = multiplier aggregate expenditure

GDP = 2.5 –$400 = –$1,000

The new equilibrium GDP = the original equilibrium GDP level + GDP

The new equilibrium GDP = $8,000 + –$1,000 = $7,000

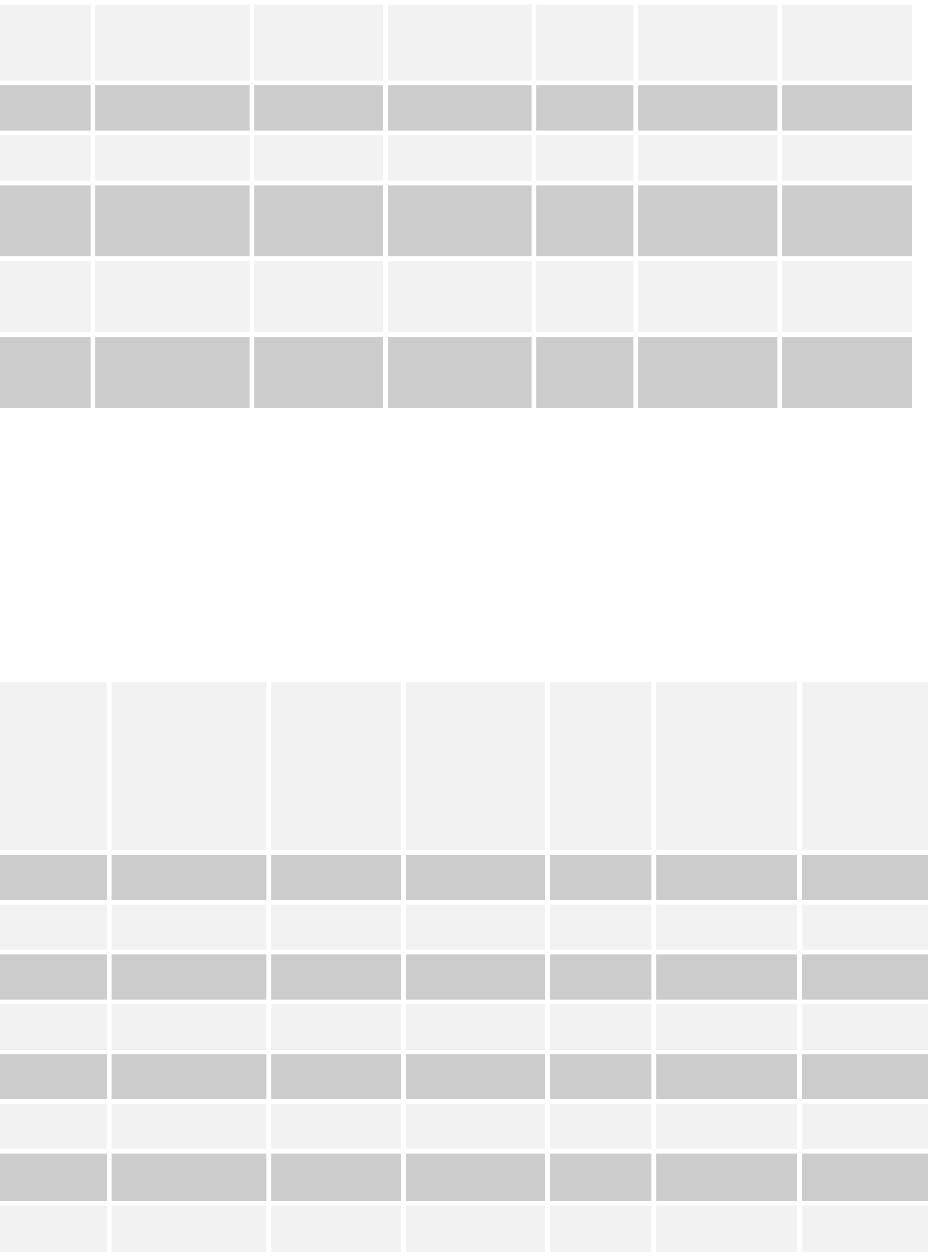

5. Once again, use Table 4 to explore a change in spending—this time, an $800 billion

increase in government spending—by reworking columns 4, 5, and 6. Find the new

equilibrium GDP, and check your results by using the multiplier.

Answer:

(1)

Income

or GDP

(2)

Consumptio

n Spending

(3)

Investme

nt

Spending

(4)

Governme

nt

Spending

(5)

Net

Exports

(6)

Aggregate

Expenditur

e

(7)

Change

in

Inventori

es

4,000 3,200 800 1,800 600 6,400 –2,400

5,000 3,800 800 1,800 600 7,000 –2,000

6,000 4,400 800 1,800 600 7,600 –1,600

7,000 5,000 800 1,800 600 8,200 –1,200

8,000 5,600 800 1,800 600 8,800 –800

9,000 6,200 800 1,800 600 9,400 – 400

10,000 6,800 800 1,800 600 10,000 0

11,000 7,400 800 1,800 600 10,600 400

12,000 8,000 800 1,800 600 11,200 800

GDP = multiplier X aggregate expenditure

GDP = 2.5 $800 = $2,000

The new equilibrium GDP = the original equilibrium GDP level + GDP

The new equilibrium GDP = $8,000 + $2,000 = $10,000