Using Credit

Chapter 6

How Will This Affect Me?

The ability to borrow funds to buy goods and services is as convenient as it is seductive. It is

important to understand how to get and maintain access to credit via credit cards, debit cards,

lines of credit, and other means. This chapter reviews the common sources of consumer credit

and provides a framework for choosing among them. It also discusses the importance of

developing a good credit history, achieving and maintaining a good credit score, and protecting

against identity theft and credit fraud. The chapter will help you understand the need to use credit

intentionally, in a way that is consistent with your overall financial objectives.

The student needs to understand that the ability to obtain credit is not an invitation to spend

money. The use of credit must be intentional and done for the right reasons. Of special

importance to the students is the section on credit cards and credit scoring, specifically the FICO,

the largest provider of credit scores by far. The FICO scores are a product of Fair Isaac & Co.

LG1 Describe the reasons for using consumer credit, and identify its benefits and problems.

LG2 Develop a plan to establish a strong credit history.

LG3 Distinguish among the different forms of open account credit.

LG4 Apply for, obtain, and manage open forms of credit.

LG5 Choose the right credit cards and recognize their advantages and disadvantages.

LG6 Avoid credit problems, protect yourself against credit card fraud, protect yourself against

identity theft, and understand the personal bankruptcy process.

Financial Facts or Fantasies?

These may be used as “teasers” to get the students on the right page with you. Also, they may be

used as quizzes after you covered the material or as “pre–test questions” to get their attention.

• It’s a good idea to contact your creditors immediately if, for some reason, you can’t make

payments as agreed.

Fact: Let the lenders know and they’ll often give you a credit

extension. This is one of the smartest things you can do to build a sound

credit history. However, except for those occasional tight spots, it’s

important to make credit payments on time consistently!

• When you apply for credit, most lenders will contact a credit bureau and let them decide

whether or not you should receive the credit.

Fantasy: Credit bureaus collect information and maintain credit files

about individual borrowers. However, they do not make the credit

decision. That’s done by the merchant or financial institution considering

extending the credit.

Financial facts or Fantasies as True/False Questions

1. True False One of the benefits of using credit is that it allows you to purchase

expensive goods and services while spreading the payment for them

overtime.

2. True False It’s a good idea to contact your creditors immediately if, for some reason,

you can’t make payments as agreed.

3. True False Excluding mortgage payments, most families will have little or no credit

problems so long as they limit their monthly credit payments to 25 to 30

percent their monthly take-home pay.

4. True False When you apply for credit, most lenders will contact a credit bureau and

let them decide whether or not you should receive the credit.

5. True False Credit card issuers are required by truth-in-lending laws to use the average

daily balance in your account when computing the amount of finance

charges you’ll have to pay.

6. True False You use a check rather than a credit card to obtain funds from an

unsecured personal line of credit.

YOU CAN DO IT NOW

The “You Can Do It Now” cases may be assigned to the students as short cases or problems.

They will help make the topic more real or relevant to the students. In most cases, it will only

take about ten minutes to do, that is, until the student starts looking around at the web site. But

they will learn by doing so.

Is Your Credit Card a Good Deal?

YOU CAN DO IT NOW

How Does Your Credit Report Look?

Financial Impact of Personal Choices

Carter Has Had It and Files for Bankruptcy

Applying Personal Finance

How’s Your Credit?

Financial Planning Exercises

1. Establish a credit history. After graduating from college last fall, Holly Baker took a job

as a consumer credit analyst at a local bank. From her work reviewing credit applications,

she realizes that she should begin establishing her own credit history. Describe for Holly

several steps that she could take to begin building a strong credit record. Does the fact that

she took out a student loan for her college education help or hurt her credit record?

Here are some things you can do to build a strong credit history:

2. Evaluating debt burden. Ted Phillips has a monthly take-home pay of $1,685; he makes

payments of $410 a month on his outstanding consumer credit (excluding the mortgage on

his home). How would you characterize Isaac’s debt burden? What if his take-home pay

were $850 a month and he had monthly credit payments of $150?

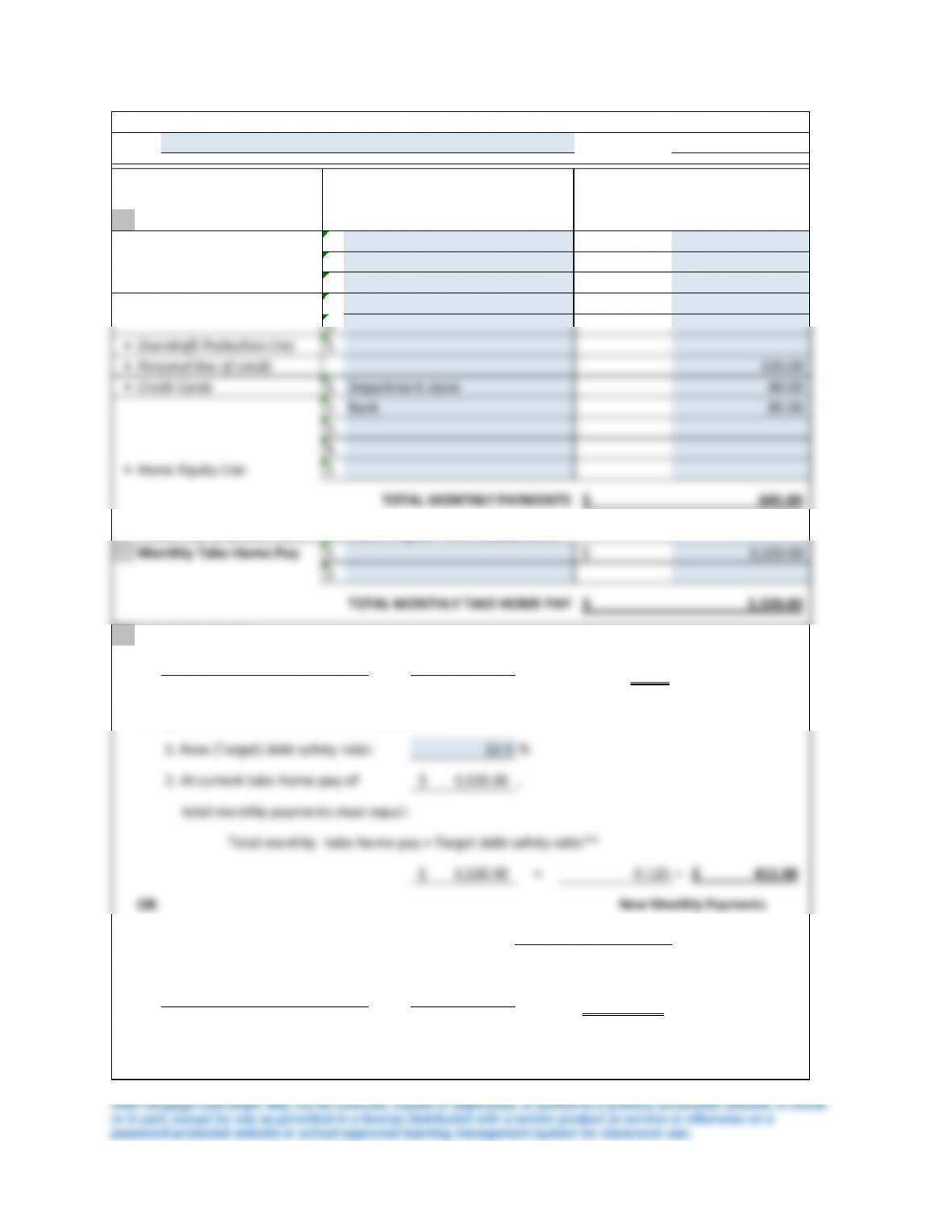

3. Evaluating debt safety ratio. Use Worksheet 6.1. Chloe Young is evaluating her debt

safety ratio. Her monthly take- home pay is $3,320. Each month, she pays $380 for an auto

loan, $120 on a personal line of credit, $60 on a department store charge card, and $85 on

her bank credit card. Complete Worksheet 6.1 by listing Chloe’s outstanding debts, and

then calculate her debt safety ratio. Given her current take-home pay, what is the

maximum amount of monthly debt payments that Chloe can have if she wants her debt

safety ratio to be 12.5 percent? Given her current monthly debt payment load, what would

Chloe’s take-home pay have to be if she wanted a 12.5 percent debt safety ratio?

Dated

•1. $

2.

3.

•1.

2.

•1.

•

•1.

2.

3.

4.

•1.

*Note: List only those loans that require regular monthly payments.

Changes needed to reach a new debt safety ratio

12.5 %

3,320.00$ ,

Total monthly

3,320.00$ ×=415.00

$

total take-home pay must equal:

Bank

Home Equity Line

120.00

60.00

85.00

Education loans

Type of Loan*

Name

Lender

Current

Monthly (or Min.)

Payment

380.00

MONTHLY CONSUMER LOAN PAYMENTS & DEBT SAFETY RATIO

September 7, 2018

Chloe Young

**Note: Enter debt safety ratio as a decimal (e.g., 15%=0.15).

take-home pay × Target debt safety ratio**

0.125

Required take-home pay

1. New (Target) debt safety ratio:

2. At current take-home pay of

total monthly payments must equal:

Auto and Personal loans

Personal line of credit

Credit Cards

Department store

Overdraft Protection Line

4. Comparing credit and debit cards. Samuel Ramirez is trying to decide whether to apply

for a credit card or a debit card. He has $8,500 in a savings account at the bank and spends

his money frugally. What advice would you have for Samuel? Describe the benefits and

drawbacks of each type of card.

If Samuel is willing to keep good records of use, a debit card provides the desired convenience

without the possibility of high interest on balances. However, if he does not keep good records,

use of a debit card may result in overdraft of the related bank account, typically a checking

5. Home equity lines. Kai and Ivy Harris have a home with an appraised value of $180,000

and a mortgage balance of only $90,000. Given that an S&L is willing to lend money at a

loan to-value ratio of 75 percent, how big a home equity credit line can Kai and Ivy obtain?

How much, if any, of this line would qualify as tax deductible interest if their house

originally cost $200,000?

6. Using overdraft protection line. Grace Wang has an overdraft protection line. Assume

that her October 2020 statement showed a latest (new) balance of $862. If the line had a

minimum monthly payment requirement of 5 percent of the latest balance (rounded to the

nearest $5 figure), then what would be the minimum amount that she’d have to pay on her

overdraft protection line?

7. Choosing between credit cards. Gabriel Clark recently graduated from college and is

evaluating two credit cards. Card A has an annual fee of $75 and an interest rate of 9

percent. Card B has no annual fee and an interest rate of 16 percent. Assuming that

Gabriel intends to carry no balance and pay off his charges in full each month, which card

represents the better deal? If Gabriel expected to carry a significant balance from one

month to the next, which card would be better? Explain.

8. Calculating credit card interest. Ruby Wilson, a student at State College, has a balance of

$380 on her retail charge card; if the store levies a finance charge of 21 percent per year,

how much monthly interest will be added to Ruby’s account?

9. Balance transfer credit cards. Zoe Robinson has several credit cards, on which she is

carrying a total current balance of $14,500. She is considering transferring this balance to a

new card issued by a local bank. The bank advertises that, for a 2 percent fee, she can

transfer her balance to a card that charges a 0 percent interest rate on transferred balances

for the first nine months. Calculate the fee that Zoe would pay to transfer the balance, and

describe the benefits and drawbacks of balance transfer cards.

Zoe has a fairly large balance of $14,500 on her credit cards. If her current cards charge her 12%

10. Credit card liability. Luna was reviewing her credit card statement and noticed several

charges that didn’t look familiar to her. Lina is unsure whether she should “make some

noise,” or simply pay the bill in full and forget about the unfamiliar charges. If some of

these charges aren’t hers, is she still liable for the full amount? Is she liable for any part of

these charges—even if they’re fraudulent?

11. Protecting against credit card fraud. Liam O’Sullivan takes pride in managing his

finances carefully with great attention to detail. He recently received a phone call in which

he was asked to confirm his credit card account number and social security number. Wyatt

was pleased he had the information handy and appreciated the caller’s thoroughness. He

gladly provided the information. What advice would you give Liam concerning his

response?

12. How to Improve FICO Score. Caleb Stewart had a FICO score of 620 when he learned

that his neighbor, Bert Collins, has a FICO score of 750. While shopping for a new

mortgage, Caleb learns that a new mortgage will cost him about 1/2 percent higher than

the rate available to Bert. Advise Caleb how he could possibly increase his FICO score.

13. Protecting Against Identity Theft. Sienna Flores lives in a neighborhood where three of

her friends have had their identities stolen in the last six months. She’s worried it will

happen to her. Explain what Sienna should keep in mind to protect herself from identity

theft.