Making Automobile

and Housing Decisions

Chapter 5

How Will This Affect Me?

A home is typically the largest single investment you’ll ever make, and a car is usually the

second largest. The decisions to buy and finance these assets are important, personal, and

complicated. This chapter presents frameworks for deciding when to buy a first home, how to

discuss in class the critical thinking questions and assign as homework problems 2 and 3.

Learning Goals

LG1 Design a plan to research and select a new or used automobile.

A useful exercise is to go to Carmax or other site and compare the cost of owning a car where:

LG2 Decide whether to buy or lease a car.

LG3 Identify housing alternatives, assess the rental option, and perform a rent-or-buy analysis.

The Worksheet 5.2 gives a format for making this decision. It is an important decision. I knew a

couple of school teachers in Milwaukee that never purchased a home. They rented their entire

LG4 Evaluate the benefits and costs of homeownership and estimate how much you can afford

to pay for a home.

LG5 Describe the home-buying process.

LG6 Choose mortgage financing that meets your needs.

Financial Facts or Fantasies?

These may be used as “teasers” to get the students on the right page with you. Also, they may be

used as quizzes after you covered the material or as “pre–test questions” to get their attention.

The closing costs on a home are rather insignificant and seldom amount to more than a few

hundred dollars.

Fantasy: Closing costs – most of which must be paid by the buyer – on home purchases can

amount to several thousand dollars and often total an amount equal to 50 percent or more of the

down payment.

In an adjustable-rate mortgage, payment will change periodically, along with prevailing interest

Financial Facts or Fantasies?

These may be used as a quiz or as a pre-test to get the students interested.

1. True False For most people, an automobile will be their second largest purchase.

2. True False The most popular form of single-family housing is the condominium.

3. True False The closing costs on a home are rather insignificant and seldom amount to

more than a few hundred dollars.

4. True False The amount of money you earn has a lot to do with the amount of money

you can borrow.

5. True False In an adjustable-rate mortgage, payment will change periodically, along

with prevailing interest rates.

6. True False Mortgage insurance guarantees the lender that the loan will be paid off in

the event of the borrower’s death.

YOU CAN DO IT NOW

The “You Can Do It Now” cases may be assigned to the students as short cases or problems.

They will help make the topic more real or relevant to the students. In most cases, it will only

take about ten minutes to do, that is, until the student starts looking around at the web site. But

they will learn by doing so.

What’s Your Car Worth?

YOU CAN DO IT NOW

Rent vs. Buy a Home?

YOU CAN DO IT NOW

Current Mortgage Rates

Financial Impact of Personal Choices

Read and think about the choices being made. Do you agree or not? Ask the students to discuss

the choices being made.

Clara Wants to Buy a House but Doesn’t Want a Roommate Now

Additional comments:

How’s Your Local Housing Market?

What’s the best source of information about available housing in your community? The answer

is a well-informed professional real estate agent whose business is helping buyers find and

negotiate the purchase of the most suitable property at the best price. However, there’s another

Teaching suggestions:

Perhaps you could help the student by identifying neighborhoods or areas of the city based upon

your knowledge of the locality. In addition, most large real estate agency have web pages that

Financial Planning Exercises

1. Planning a new car purchase: Anna Davis has just graduated from college and needs to

buy a car to commute to work. She estimates that she can afford to pay about $450 per

month for a loan or lease and has about $2,000 in savings to use for a down payment.

Develop a plan to guide her through her first car-buying experience, including researching

car type, deciding whether to buy a new or used car, negotiating the price and terms, and

financing the transaction.

Exhibit 5.1 lists the steps in buying a new car.

• Research which car best meets your needs and determine how much you can afford to

spend on it. Choose the best way to pay for your new car—cash, financing, or lease. Ask

2. Lease vs purchase car decision: Use Worksheet 5.1. Ben Halls is trying to decide whether

to lease or purchase a new car costing $18,000. If he leases, he’ll have to pay a $600 security

deposit and monthly payments of $450 over the 36-month term of the closed-end lease. Ben

could earn 1% on the amount of any down payment or security deposit. On the other

hand, if he buys the car then he’ll have to make a $2,400 down payment and will finance

the balance with a 36-month loan with a 4% interest rate; he’ll also have to pay a 6 percent

sales tax ($1,080) on the purchase price, and he expects the car to have a residual value of

$6,500 at the end of 3 years. Ben can earn 4 percent interest on his savings.

Use the automobile lease versus purchase analysis form in Worksheet 5.1 to find the total

cost of both the lease and the purchase and then recommend the best strategy for Ben.

Name Date

Item Amount

1

$

$

600.00

2 3

336

4 $ 450.00

5 $ 16,200.00

6 0.010

estimated end-of–term charges

Purchase price

Down payment

Item 6)

Payment/refund for market value adjustment

at end of lease ($0 for closed-end leases) and/or

Opportunity cost of initial payment (Item 1 × Item 2 ×

13 $ 1,080.00

14 15600.00 $ 460.57

36 months, 4.00 %)

15 $ 16,580.67

16 $ 72.00

17 $ 6,500.00

If the value of Item 9 is less than the value of Item 18, leasing is preferred; otherwise the

purchase alternative is preferred.

Total payments over term of lease (Item 3 × Item 4)

AUTOMOBILE LEASE VERSUS PURCHASE ANALYSIS*

Description

Initial payment:

LEASE

Ben Halls

a. Down payment (capital

cost reduction):

b. Security deposit:

Term of lease and loan (years)*

Term of lease and loan (months) (Item 2 × 12)

Monthly lease payment

600.00

Estimated value of car at end of loan

Monthly loan payment (Terms:

Opportunity cost of down payment (Item 2 ×

Item 6 × Item 11)

Total payments over term of loan (Item 3 × Item 14)

November 15, 2018

Sales tax (Item 10 × Item 12)

Interest rate earned on savings (in decimal form)

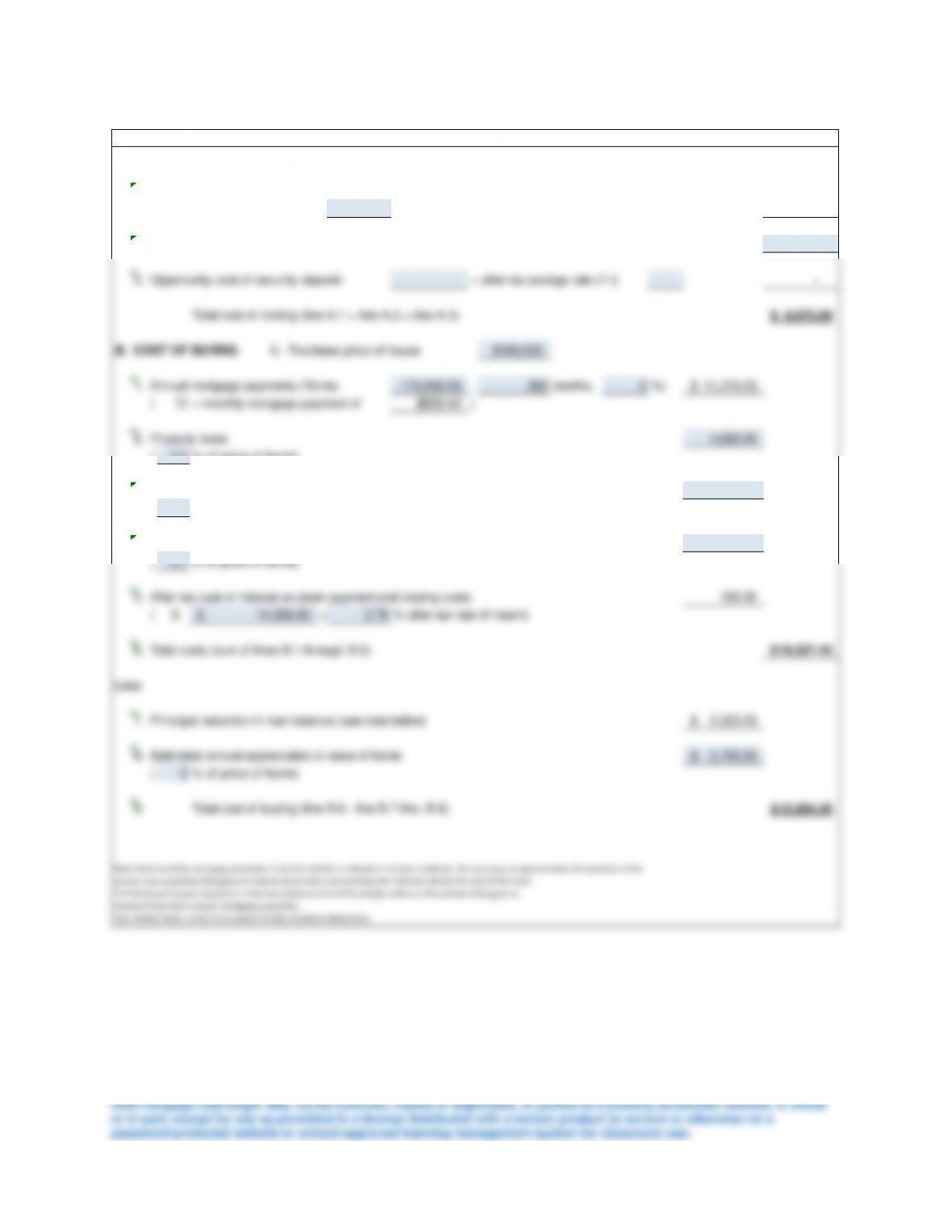

3. Rent versus buy home. Use Worksheet 5.2. Emma Sanchez is currently renting an

apartment for $725 per month and paying $275 annually for renter’s insurance. She just

found a small townhouse she can buy for $185,000. She has enough cash for a $10,000 down

payment and $4,000 in closing costs. Her bank is offering 30-year mortgages at 5 percent

per year. Emma estimates the following costs as a percentage of the home’s price: property

taxes, 2.5 percent; homeowner’s insurance, 0.5 percent; and maintenance, 0.7 percent. She

is in the 22 percent tax bracket and does not plan to itemize deductions on her taxes.

Emma estimates that the value of the home will appreciate 2 percent per year. Using

Worksheet 5.2, calculate the cost of each alternative and recommend the least costly

option—rent or buy—for Emma.

Note since Emma will not itemize, there are no tax advantages to mortgage interest or property

taxes. Given the increase in the standard deduction enacted by the 2017 tax act, 90% of

taxpayers are expected to elect the standard deduction and not itemize deductions.

Problem 5.3

A.

1.

(12 $ 725.00 ) 8,700.00$

2. 275.00

3. × after-tax savings rate (1-t) –

Total cost of renting (line A.1 + line A.2 + line A.3) 8,975.00

$

B. 0. Purchase price of house $185,000

1. 175,000.00 , 360 months, 5 %) 11,273.25$

(12 $939.44 )

2. 4,625.00

( 2.5

3. 925.00

( 0.5

4. 1,295.00

( 0.7

Total costs (sum of lines B.1 through B.5)

% after-tax rate of return)

Less:

8. 3,700.00$

( 2

9. 12,004.20$

% of price of home)

Homeowner’s insurance

RENT-OR-BUY ANALYSIS

× monthly rental rate of

COST OF RENTING

Annual rental costs

Renter’s insurance

Property taxes

Opportunity cost of security deposit:

COST OF BUYING

Annual mortgage payments (Terms:

× monthly mortgage payment of

% of price of home)

Maintenance

% of price of home)

% of price of home)

Total cost of buying (line B.6 – line B.7 line -B.8)

Estimated annual appreciation in value of home

4. Maximum affordable mortgage payment. Using the maximum ratios for a conventional

mortgage, how big a monthly payment could the Ross family afford if their gross (before-

tax) monthly income amounted to $3,500?

Would it make any difference if they were already making monthly installment loan

payments totaling $750 on two car loans?

5. Changes in mortgage principal and interest over time. Explain how the composition of the

principal and interest components of a fixed-rate mortgage change over the life of the

mortgage. What are the implications of this change?

6. Calculating required down payment on home purchase. How much would you have to put

down on a house with an appraised value of $105,000 and the lender required an 80

percent loan-to-value ratio?

7. Calculating monthly mortgage payments. Find the monthly mortgage payments on the

following mortgage loans using either your calculator or the table in Exhibit 5.6:

a. $90,000 at 6.5 percent for 30 years

b. $125,000 at 5.5 percent for 20 years

c. $97,500 at 5 percent for 15 years

8. Estimating closing costs on home purchase. How much might a home buyer expect to pay

in closing costs on a $220,000 house with a 10 percent down payment? How much would

the home buyer have to pay at the time of closing, taking into account closing costs, down

payment, and a loan fee of 3 points?

9. Using a real estate broker. Describe the ways in which a real estate broker represents

buyers versus sellers. What’s a typical real estate commission?

10. Adding to monthly mortgage payments. What are the pros and cons of adding $100 a

month to your fixed-rate mortgage payment?

11. Refinancing a mortgage.

Use Worksheet 5.4. Daisy Tran purchased a condominium ten

years ago for $300,000, paying $1,439 per month on her $240,000, 6 percent, 30-year

mortgage. The current loan balance is $200,857. Recently, Daisy has been considering

refinancing her condo. She expects to remain in the condo for at least four more years and

has found a lender that will make a 4 percent, 20-year, $200,857 loan, requiring monthly

payments of $1,217. Although there is no prepayment penalty on her current mortgage,

Daisy will have to pay $1,500 in closing costs on the new mortgage. She is in the 22 percent

tax bracket. Based on this information, use the mortgage refinancing analysis form in

Worksheet 5.4 to determine whether Daisy should refinance her mortgage under the

specified terms.

From the worksheet below, it will take 8.7 months to breakeven on the refinancing. Since she

plans to stay in the home for another 4 years, it will be to her advantage to refinance the

mortgage

Name Date September 6, 2018

Item Amount

1 240,000.00 , 6.00

%,

30 years) 1,439.00$

2 200,857.00 , 4.00

%,

20 years) 1,217.00$

3222.00$

422 %) 49.00$

5173.00$

6

$

1,500

1,500.00$

7 8.7

b. Total closing costs (after-tax)

Current monthly payment (Terms:

c. Total refinancing costs (Item 6a + Item 6b)

Months to break even (Item 6c ÷ Item 5)

New monthly payment (Terms:

Monthly savings, pretax (Item 1 – Item 2)

Tax on monthly savings [Item 3 × tax

Monthly savings, after-tax (Item 3 – Item 4)

Costs to refinance:

a. Prepayment penalty

Description

MORTGAGE REFINANCING ANALYSIS

Daisy Tran

Test Yourself – Legacy questions for your use

5-1 Briefly discuss how each of these purchase considerations would affect your choice of a

car:

a. Affordability

b. Operating costs

c. Gas, diesel, hybrid, or electric?

d. New, used, or “nearly new”?

e. Size, body style, and features

f. Reliability and warranty protection

5-2 Describe the purchase transaction process, including shopping, negotiating price, and

closing the deal on a car.

Shopping is all about finding the best car for you. Exhibit 5.2 lists some steps to take. The key

5-3 What are the advantages and disadvantages of leasing a car?

5-4 Given your personal financial circumstances, if you were buying a car today, would you

probably pay cash, lease, or finance it, and why? Which factors are most important to you

in making this decision?