Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 268

Chapter 24

ANSWERS TO QUESTIONS

1. What does the Lucas critique state about the limitations of our current understanding of the

way in which the economy works?

2. “The Lucas critique by itself casts doubt on the ability of discretionary stabilization policy to

be beneficial.” Is this statement true, false, or uncertain? Explain your answer.

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 273

Announcements about the inflation targets and potential punishments for central bank

officials are crucial for inflation targeting. It is very important for the public to be able to

check whether the target has been reached or not. When central bank officials know that the

18. In recent years, central banks have dramatically increased the amount of communication

with market participants and the public, and at the same time in many of these countries,

average inflation has declined and become less volatile. Is this coincidence, or is there a

connection? Explain.

19. What are the purposes of inflation targeting, and how does this monetary policy strategy

achieve them?

20. How can the establishment of an exchange-rate target bring credibility to a country with a

poor record of inflation stabilization?

Tying its domestic currency to another country’s currency is an easy way for a country with a

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 275

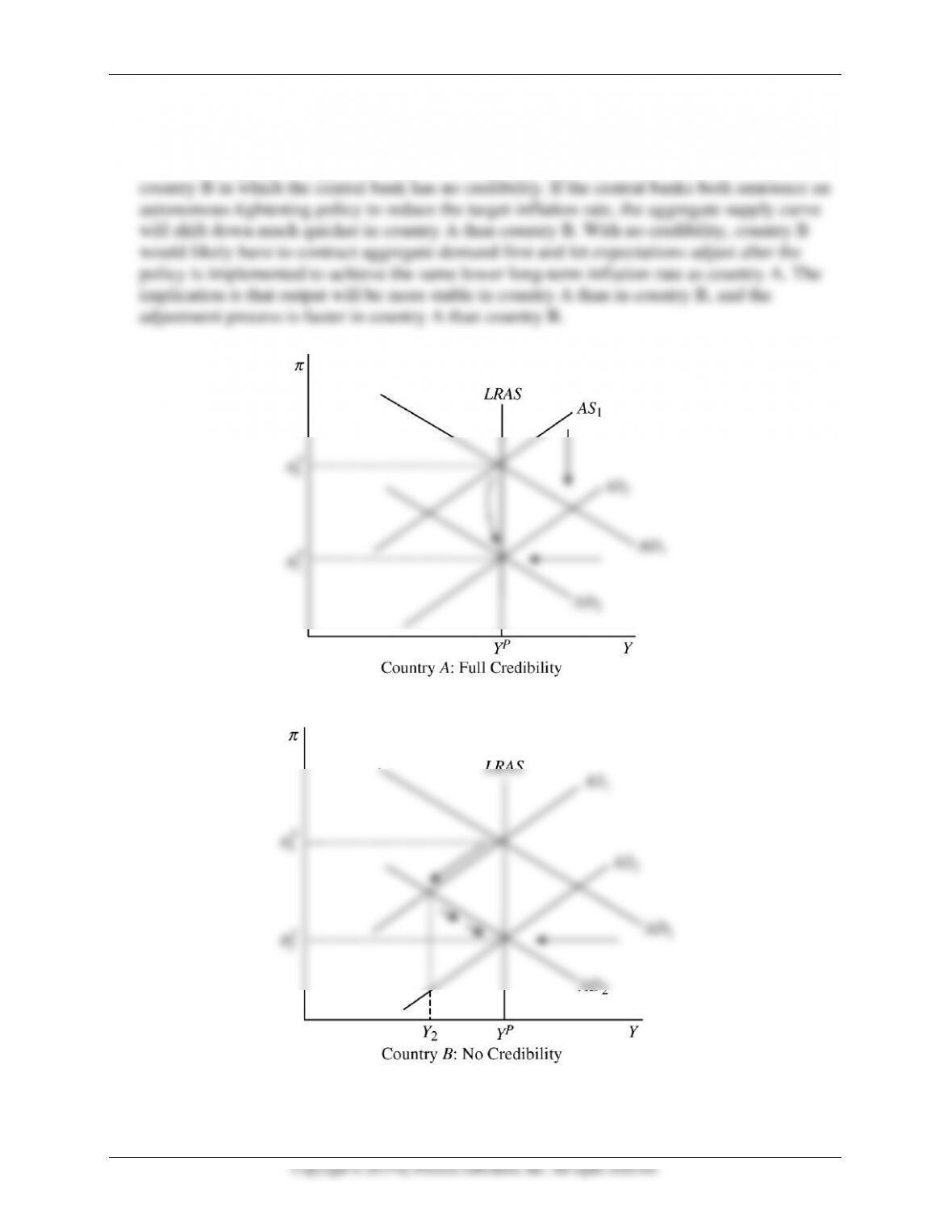

In country A, the public is more likely to believe announcements about future policy

changes, and therefore adjust inflation expectations in anticipation of changes in future policy.

As a result, aggregate supply will adjust more quickly to policy announcements compared to

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 277

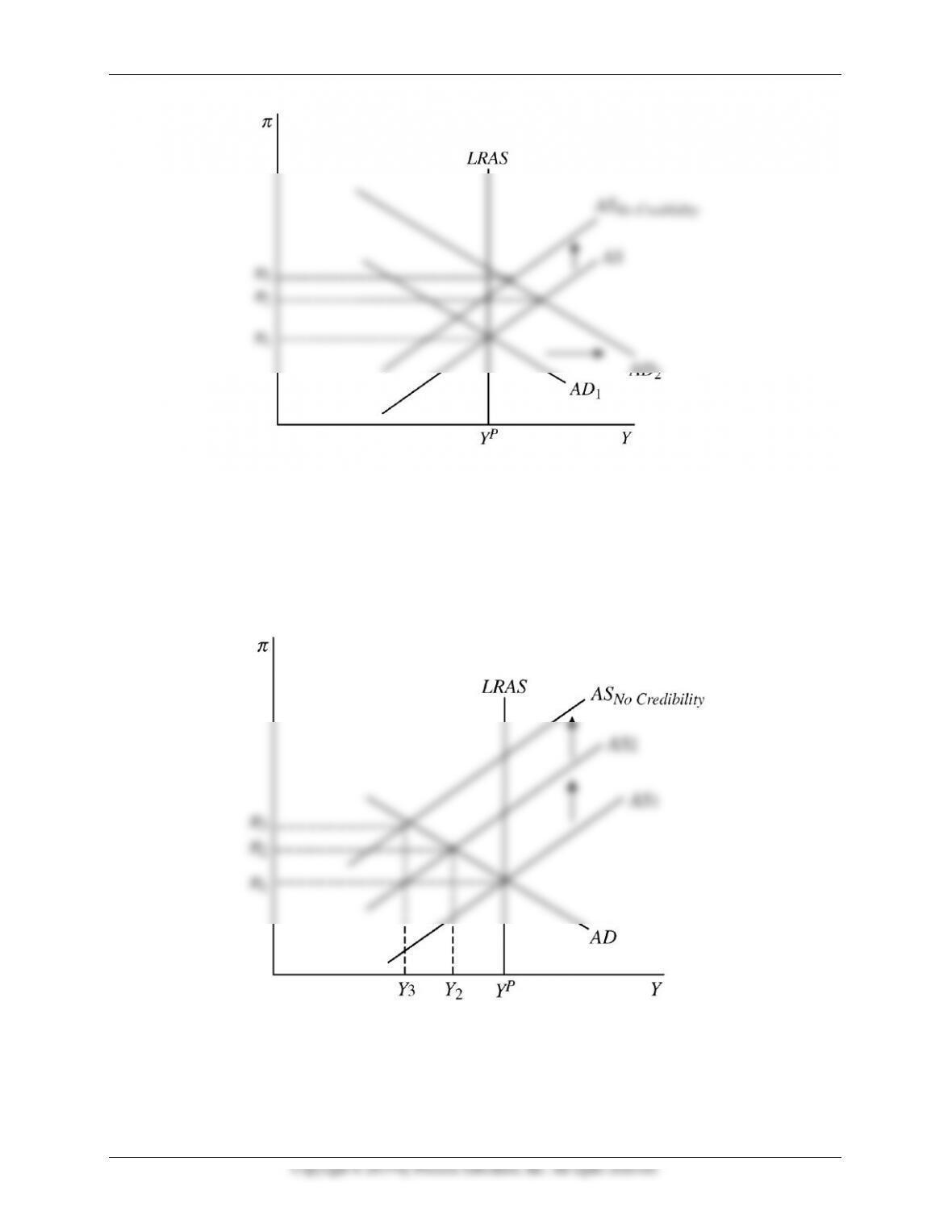

The outcome is similar when a negative aggregate supply shock occurs. Inflation increases

and output falls as the short-run aggregate supply curve shifts upward, but with a credible

nominal anchor, expected inflation does not increase. As a result, no further upward shifts of

the short-run aggregate supply curve occur and the increase in inflation and decrease in output

are not as great as they otherwise would be. Thus the credible nominal anchor brings about

better outcomes for both inflation and output when a negative supply shock occurs, as shown

in the graph below.

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 278

ANSWERS TO DATA ANALYSIS PROBLEMS

1. Go to the St. Louis Federal Reserve FRED database and find data on the personal

consumption expenditure price index (PCECTPI). Convert the units setting to “Percent

Change from Year Ago,” and download the data. Beginning in January 2012, the Fed

formally announced a 2% inflation goal over the “longer-term.”

a. Calculate the average inflation rate over the last four and the last eight quarters of data

available. How does it compare to the 2% inflation goal?

b. What, if anything, does your answer to part (a) imply about Federal Reserve credibility?

2. Go to the St. Louis Federal Reserve FRED database and find data on the core PCE price

index (PCEPILFE) and the spot price of a barrel of oil (WTISPLC). For both variables,

convert the units setting to “Percent Change from Year Ago,” and download the data from

1960 to the most recent available data.

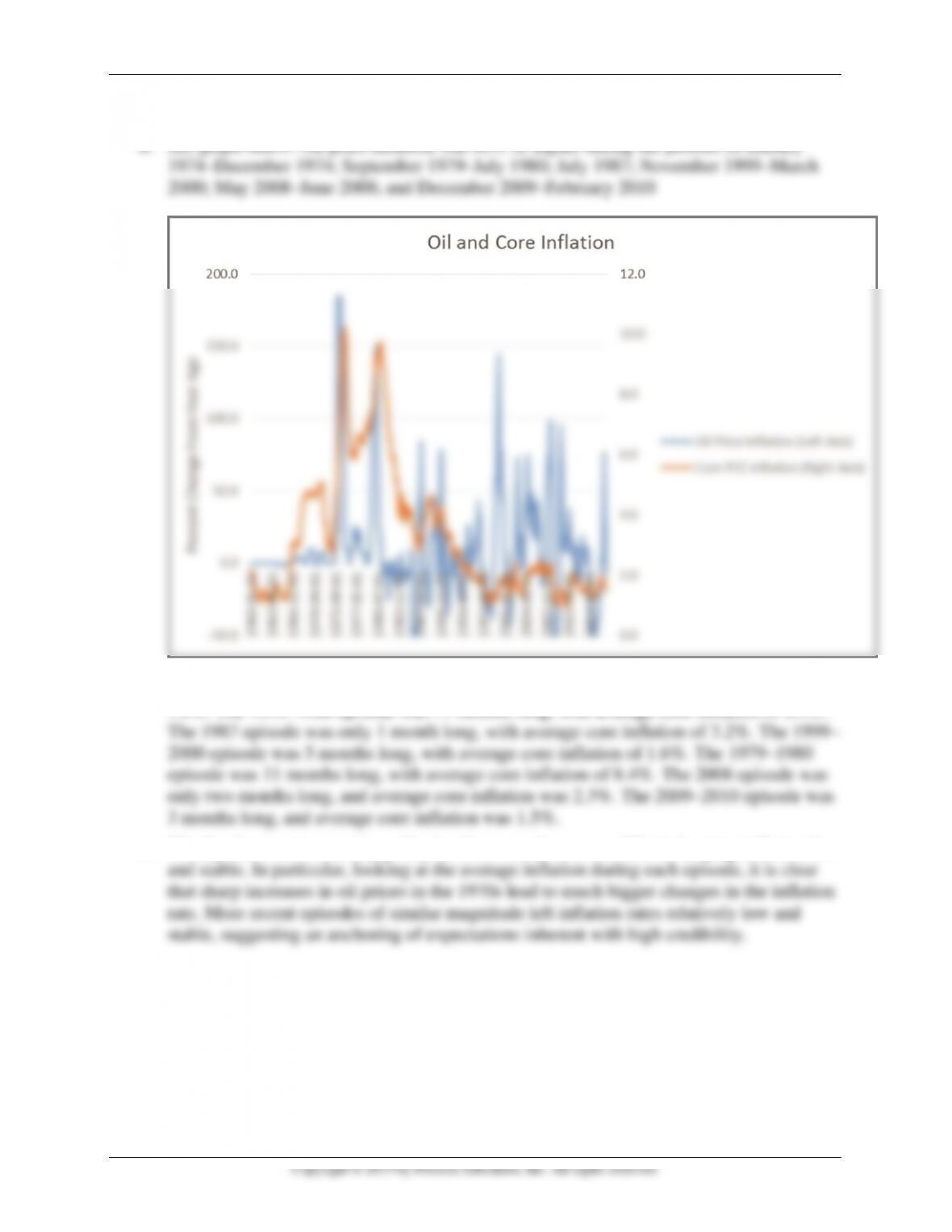

a. Identify periods in which oil price inflation is 80% or higher.

b. In the periods identified in part (a), how many months was oil price inflation 80% or

higher? What was the average core inflation rate during each of those episodes?

c. Based on your answers to parts (a) and (b) above, what can you conclude about the

credibility of more recent monetary policy compared to its credibility in the earlier

periods?

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 279

a. See graph below. Oil price inflation was 80% or higher during the periods of January

b. For the 1974 episode, it lasted 12 months, and average inflation during that time was

7.9%. The 1979–1980 episode was 11 months long, with average core inflation of 8.4%.

c. Clearly, the recent monetary policy has been much more credible in keeping inflation low