Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 172

Copyright © 2019 by Pearson Education, Inc. All rights reserved.

commitment by the central bank; if conditions suddenly change where a change in the policy

stance may be warranted, then holding to the commitment could be destabilizing. On the

other hand, not strictly maintaining the commitment could then be viewed as reneging on a

promise, and the central bank could lose significant credibility.

19.

In which economic conditions would a central bank want to use a “forward-guidance”

strategy? Based on your previous answer, can we easily measure the effects of such a

strategy?

20.

How do the monetary policy tools of the European System of Central Banks compare to the

monetary policy tools of the Fed? Does the ECB have a discount lending facility? Does the

ECB pay banks an interest rate on their deposits?

In general the set of monetary policy tools available to the ECB is quite similar to the one at

21. What is the main rationale behind paying negative interest rates to banks for keeping their

deposits at central banks in Sweden, Switzerland, and Japan? What could happen to these

economies if banks decide to loan their excess reserves, but no good investment

opportunities exist?

22. In early 2016 as the Bank of Japan began to push policy interest rates negative, there was a

sharp increase in sales for home in Japan. Why might this be, and what does it mean for the

effectiveness of negative interest rate policy?

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 173

Copyright © 2019 by Pearson Education, Inc. All rights reserved.

banking system available for lending. Second, the intended effect of negative interest rates is

to penalize saving in the form of deposits, and thereby encourage consumption and

borrowing, which can help stimulate the economy. However, if depositors are simply pulling

their deposits and instead holding them as cash in safes, it does not increase spending and

create the intended stimulus.

ANSWERS TO APPLIED PROBLEMS

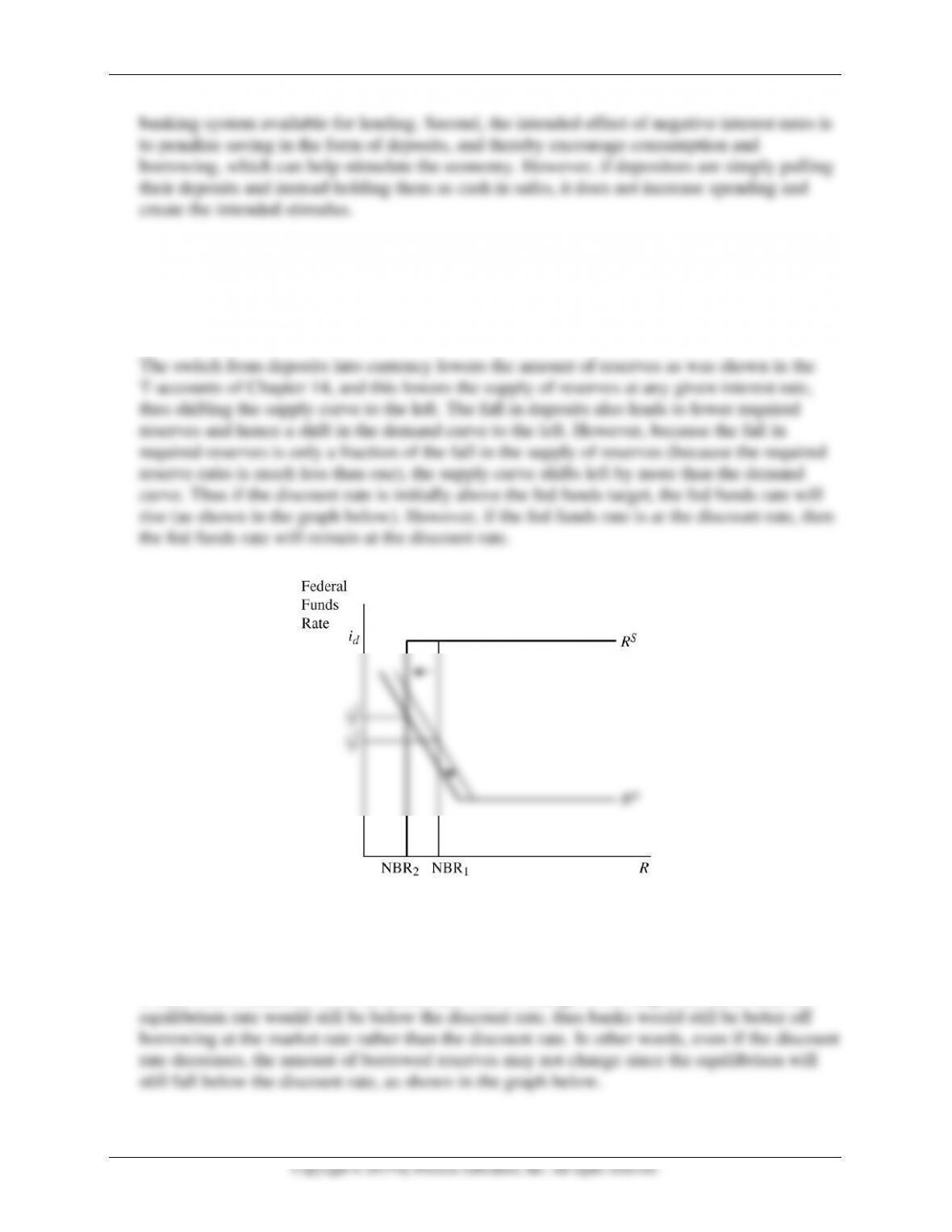

23. If a switch occurs from deposits into currency, what happens to the federal funds rate? Use

the supply and demand analysis of the market for reserves to explain your answer.

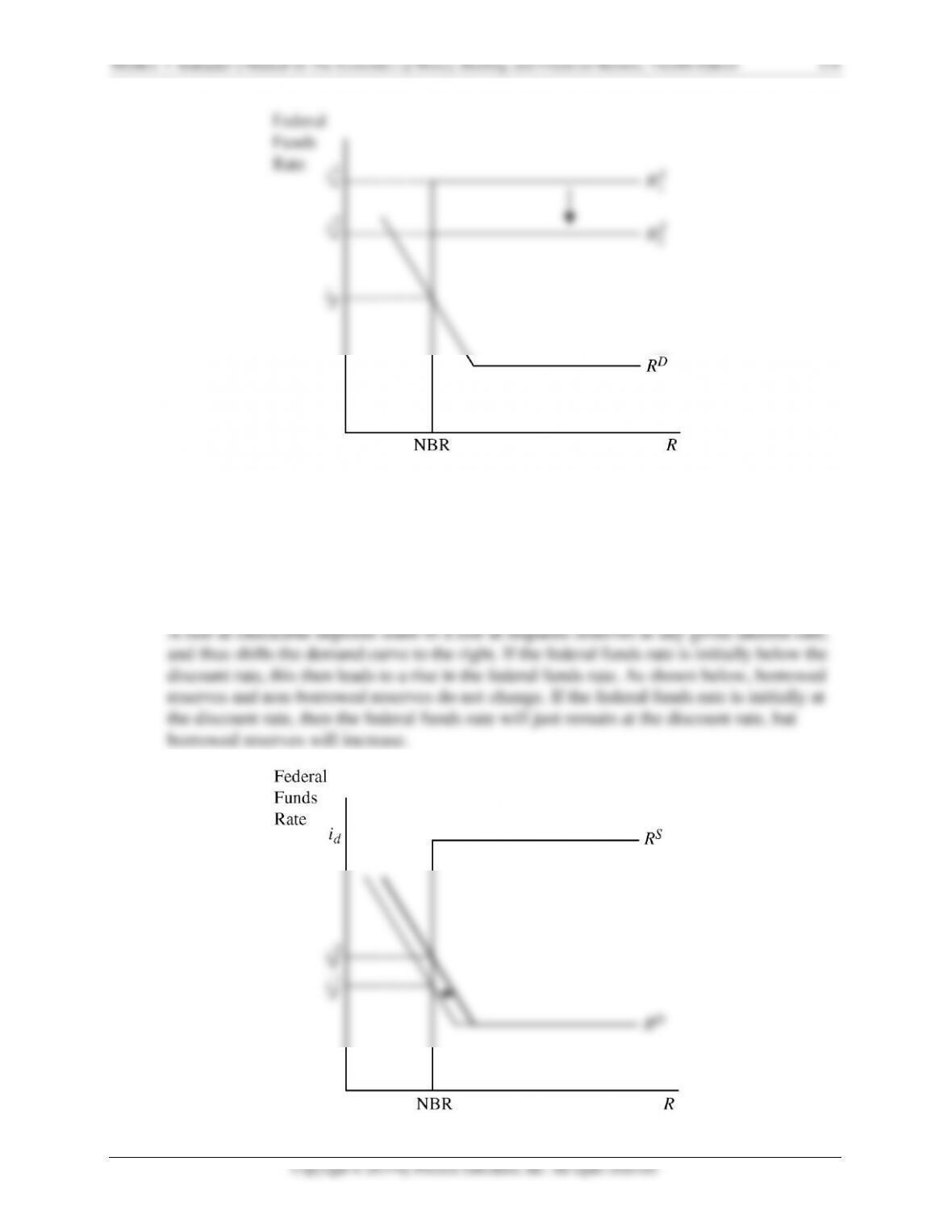

24. Why is it that a decrease in the discount rate does not normally lead to an increase in

borrowed reserves? Use the supply and demand analysis of the market for reserves to explain.

In most cases, the discount rate is set far enough above the fed funds target rate such that, even

if there was a reduction in the discount rate with no change in the target fed funds rate, the

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 175

b. Banks expect an unusually large increase in withdrawals from checking deposit accounts

in the future.

c. The Fed raises the target federal funds rate.

d. The Fed raises the interest rate on reserves above the current equilibrium federal funds

rate.

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 176

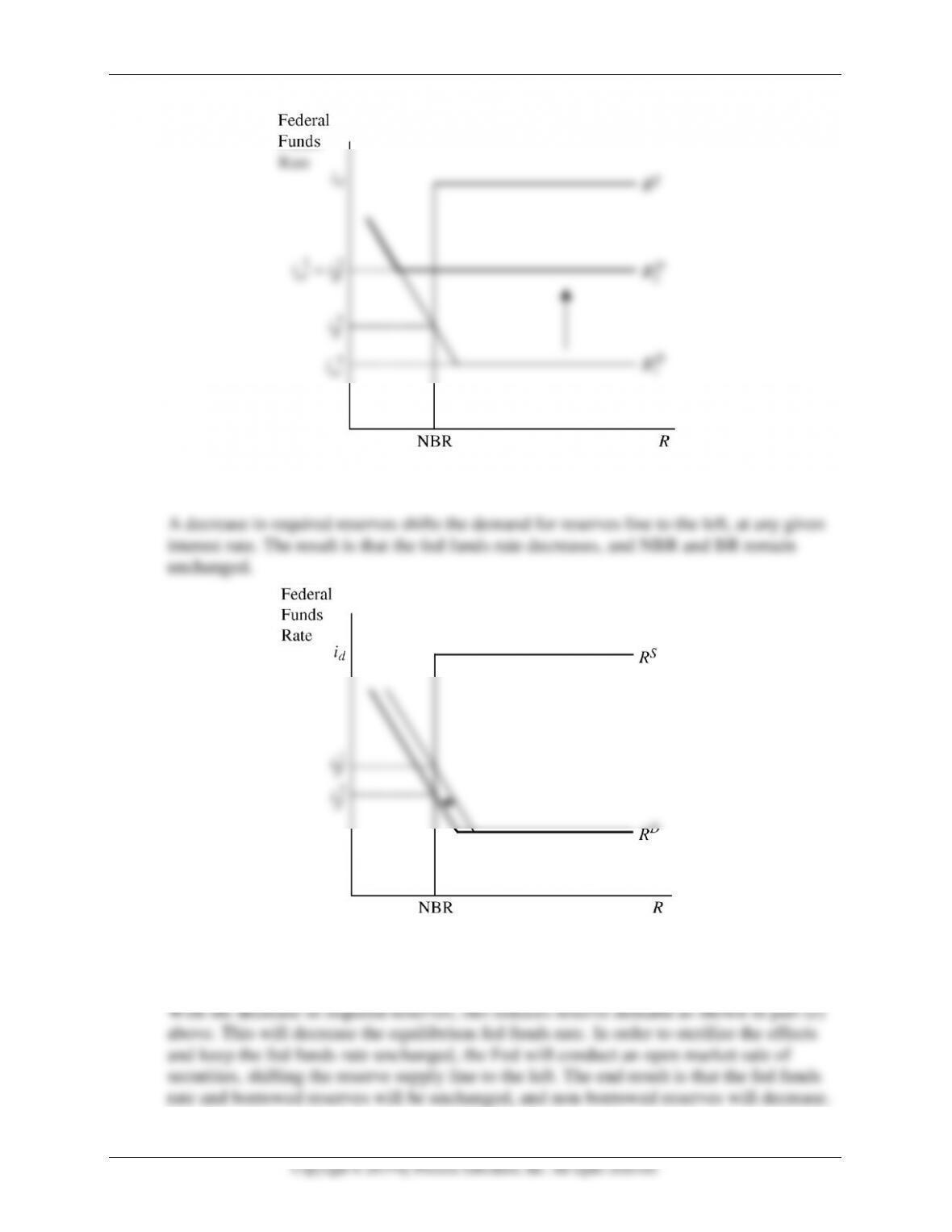

e. The Fed reduces reserve requirements.

f. The Fed reduces reserve requirements and then offsets this action by conducting an open

market sale of securities.

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 177

ANSWERS TO DATA ANALYSIS PROBLEMS

1. Go to the St. Louis Federal Reserve FRED database, and find data on nonborrowed reserves

(NONBORRES) and the federal funds rate (FEDFUNDS).

a. Calculate the percent change in nonborrowed reserves and the percentage point change

in the federal funds rate for the most recent month of data available and for the same

month a year earlier.

b. Is your answer to part (a) consistent with what you expect from the market for reserves?

Why or why not?

2. In December 2008, the Fed switched from a point federal funds target to a range target

(and it’s possible that it will switch back to a point target in the future). Go to the St. Louis

Federal Reserve FRED database, and find data on the federal funds targets/ ranges

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 178

(DFEDTAR, DFEDTARU, DFEDTARL) and the effective federal funds rate (DFF).

Download into a spreadsheet the data from the beginning of 2006 through the most current

data available.

a. What is the current federal funds target/range, and how does it compare to the effective

federal funds rate?

b. When was the last time the Fed missed its target or was outside the target range? By how

much did it miss?

c. For each daily observation, calculate the “miss” by taking the absolute value of the

difference between the effective federal funds rate and the target (use the abs(.) function).

For the periods in which the rate was a range, calculate the absolute value of the “miss”

as the amount by which the effective federal funds rate was above or below the range.

What was the average daily miss between the beginning of 2006 and the end of 2007?

What was the average daily miss between the beginning of 2008 and December 15,

2008? What is the average daily miss for the period from December 16, 2008, to the most

current date available? Since 2006, what was the largest single daily miss? Comment on

the Fed’s ability to control the federal funds rate during these three periods.

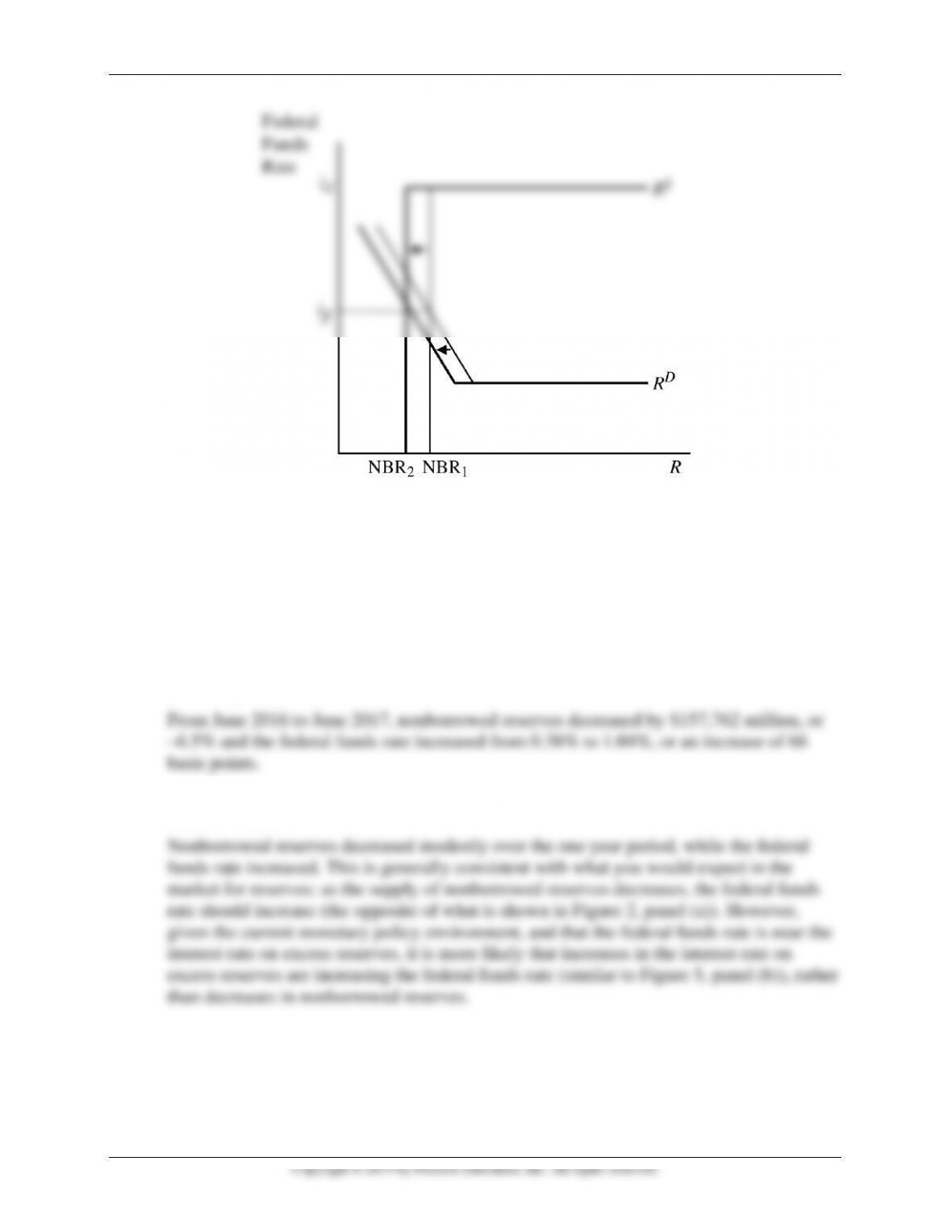

From the beginning of 2006 to the end of 2007, the average daily miss was 0.05, or 5

basis points. From the beginning of 2008 to December 15, 2008, the average daily miss