Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

278 Brooks ◼ Financial Management: Core Concepts, 4e

30. Changing risk level. Ms. Chambers wants to change the expected return of her portfolio.

Currently, she has all her money in U.S. Treasury Bills with a return of 3%. She can switch

some of her money into a risky portfolio with an expected return of 15%. What percentage

of her wealth will she need to invest in the risky portfolio to get an expected return of 5%?

Of 7%? Of 9%? Of 11%? Of 13%? Of 15%? Is there a pattern here?

ANSWER

The weight in the risk-free asset is 1 – w, and the weight in the risky portfolio is w and the total

of the two reflects 1 or 100% of his wealth.

Thus 1/6 (16.67%) of the wealth is invested in the risky portfolio and 5/6 in the risk-free asset.

Thus 1/3 (33.33%) of the wealth is invested in the risky portfolio and 2/3 in the risk-free asset.

Thus 1/2 (50.0%) of the wealth is invested in the risky portfolio and 1/2 in the risk-free asset.

Chapter 8 ◼ Risk and Return 279

Thus 2/3 (66.67%) of the wealth is invested in the risky portfolio and 1/3 in the risk-free asset.

Thus 5/6 (83.33%) of the wealth is invested in the risky portfolio and 1/6 in the risk-free asset.

Thus all (100%) of the wealth is invested in the risky portfolio and none in the risk-free asset.

The pattern is linear in the change in expected return and the percent invested in the risky

portfolio.

31. Reward-to-risk ratio. The Royal Seattle Investment Club has $100,000 to invest in the equity

market. Frasier advocates investing the funds in KSEA Radio with a beta of 1.3 and an

expected return of 16%. Niles advocates investing the funds in Northwest Medical with a

beta of 1.1 and an expected return of 14%. The club is split 50/50 on the two stocks. You are

the deciding vote, and you cannot pick a split of $50,000 for each stock. Before you vote,

you look up the current risk-free rate (the one-year U.S. Treasury bill with a yield of 3.75%).

Which stock do you select?

ANSWER

Chapter 8 ◼ Risk and Return 283

Solutions to Advanced Problems for Spreadsheet Application

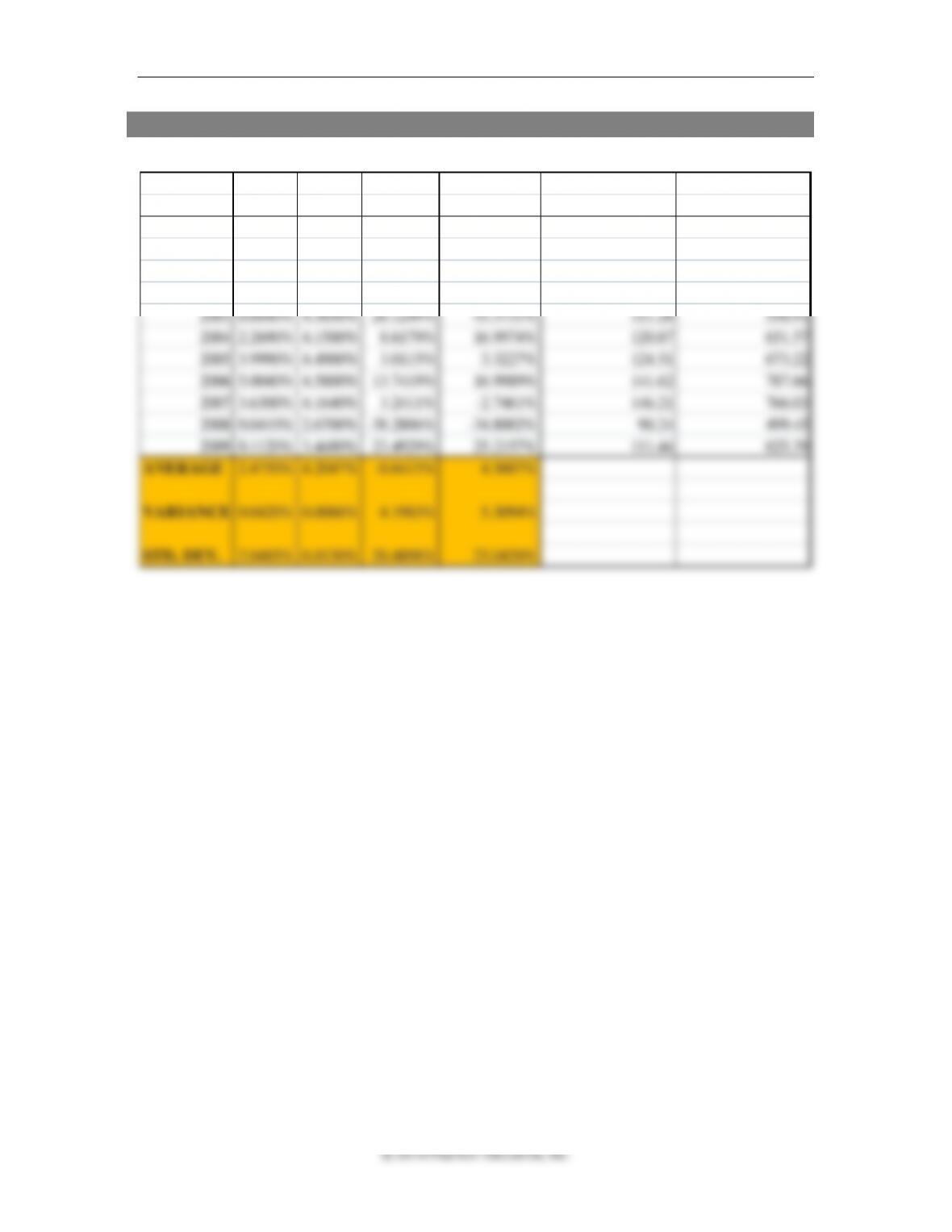

1. Returns and variances in the period 2000-2009

T-Bill T-Note S&P 500 Russe ll 2000 S&P 500 Russe ll 2000

Year Re turn Re turn Re turn Re turn End of Ye ar Price End of Ye ar Price

1999 146.88 504.75

2000 5.8640% 5.8650% -10.6822% -4.2041% 131.19 483.53

2001 1.7400% 4.2200% -12.8745% 1.0279% 114.3 488.5

2002 1.2070% 4.0950% -22.8084% -21.5783% 88.23 383.09

2003 0.8840% 4.3650% 26.1249% 45.3731% 111.28 556.91

2004 2.2690% 4.1500% 8.6179% 16.9974% 120.87 651.57

2005 3.9990% 4.4900% 3.0115% 3.3227% 124.51 673.22

2006 5.0040% 4.5800% 13.7419% 16.9989% 141.62 787.66

2007 3.6300% 4.1640% 3.2411% -2.7461% 146.21 766.03

2008 0.0410% 2.6700% -38.2806% -34.8002% 90.24 499.45

2009 0.1120% 3.4480% 23.4929% 25.2157% 111.44 625.39

AVERAGE 2.4750% 4.2047% -0.6415% 4.5607%

VARIANCE 0.0420% 0.0066% 4.1983% 5.3094%

STD. DEV. 2.0485% 0.8130% 20.4898% 23.0420%

Chapter 8 ◼ Risk and Return 285

© 2016 Pearson Education, Inc.

Given the purpose of the portfolio, to fund annual grants, it is convenient to think in terms

of a one-year holding period return, which includes both distributions and capital gains or

losses. If the portfolio gains $100,000, the dollar HPR is $130,000, the percentage HPR is

($30,000 + $100,000)/$1,000,000 = 13%.

286 Brooks ◼ Financial Management: Core Concepts, 4e

© 2018 Pearson Education, Inc.

If it loses $100,000, the dollar HPR is (–$100,000 + $30,000) = $(70,000), the percentage HPR

is:

$(70,000)/$1,000,000 = –7%.

With a one-year holding period, HPR, APR, and EAR are all the same.

The amount of the grants will be either $1,130,000 × 0.05 = $56,500, leaving $1,073,500 or

$930,000 × 0.05 = $46,500, leaving $883,500.

To illustrate how to compute annualized returns (EAR) over a longer period, we can look at

how Lawrence did on his investment in Google.

2. How can we assess the risk of an individual stock?

In financial terms, an investment is risky if the outcome is uncertain and some possible

outcomes are unfavorable. We can understand this better by looking at some examples.

a. Kraska will first address this question by looking at recent returns on Amazon.com and

on Coca-Cola. Compute the mean and standard deviation for each and explain what

they mean. He has collected the following data:

Year

AMAZON

COKE

2007

134.77%

33.35%

2006

–16.31%

26.35%

2005

6.46%

2.24%

2004

–15.83%

13.93%

2003

178.56%

21.94%

The average return is the sum of the returns shown above divided by 5.

Chapter 8 ◼ Risk and Return 287

It is obvious that the average return on Amazon.com has been much higher, but that

288 Brooks ◼ Financial Management: Core Concepts, 4e

b. Kraska will also suggest that is good to assess risk by looking forward to how we

expect stocks to react to a particular set of circumstances or states of nature. Use the

following set of assumptions for the coming year to compute the expected rate of

return and standard deviation for Amazon.com, Coca-Cola, and a portfolio with equal

dollar amounts invested in Amazon.com and Coca-Cola. Explain briefly what they

mean.

Amazon.com

Coca-Cola

50/50

Portfolio

State of

Economy

Probability of

State

Conditional

Return

Conditional

Return

Conditional

Return

Recession

30.00%

–25.00%

5.00%

–10.00%

Average

50.00%

30.00%

12.00%

21.00%

Boom

20.00%

50.00%

20.00%

32.50%

Amazon.com

Coca-Cola

Portfolio

The mean and standard deviation can be interpreted in the same way as for the sample data

in question a. Note that in this exercise both the probabilities and the returns are somewhat

3. What kinds of investments are safe and earn a high rate of return?

Chapter 8 ◼ Risk and Return 289

© 2016 Pearson Education, Inc.

Kraska responds that unfortunately there is no such thing. If there were, everyone would

want to buy it, demand would drive the price up, and returns would soon drop to expected

rates.

4. Google seems to be a great company. Why did Lawrence require the town to sell the

Google stocks and reinvest the money in a diversified portfolio?

Lawrence was reluctant to sell Google because taxes on his profits would have reduced the

Chapter 8 ◼ Risk and Return 291

© 2016 Pearson Education, Inc.

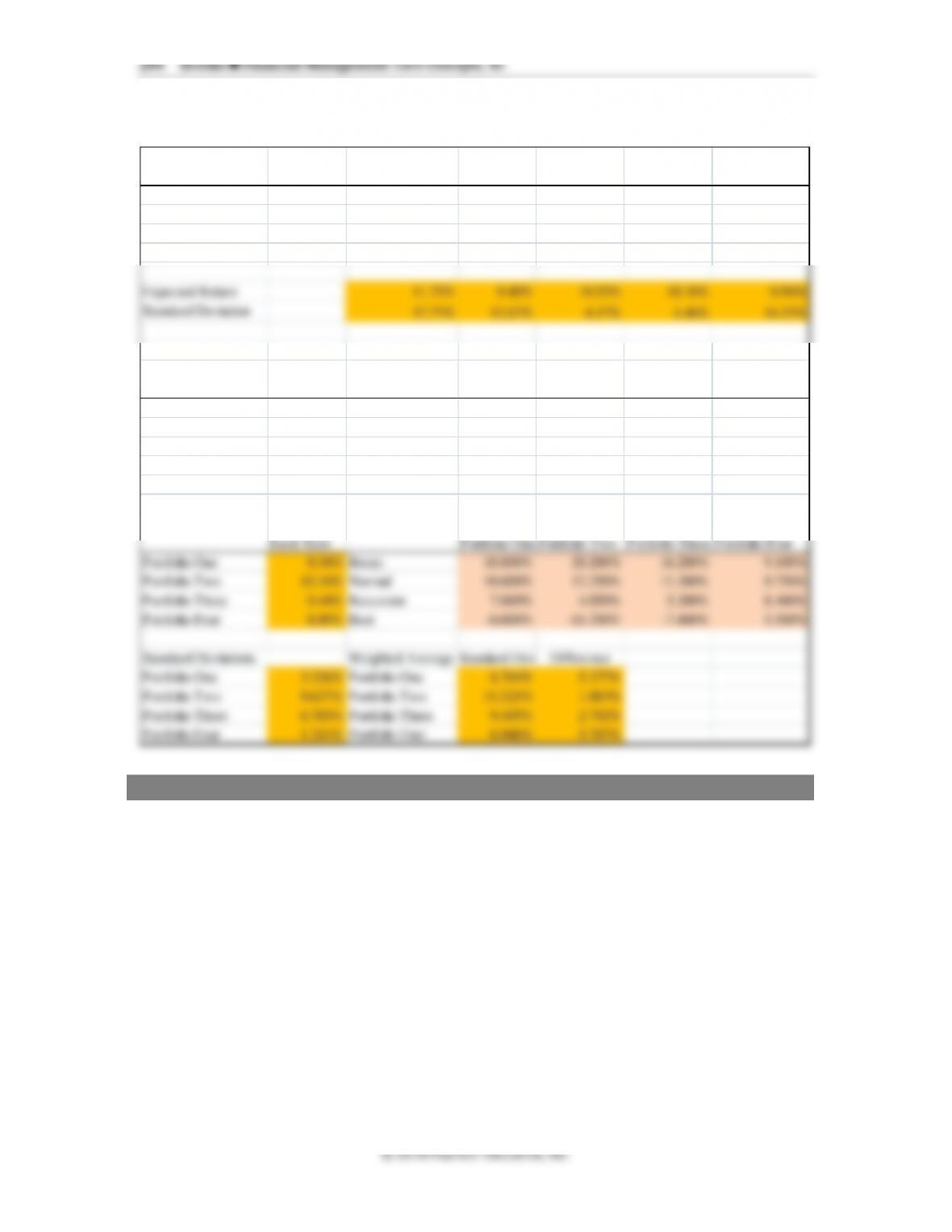

The beta of a portfolio is just the weighted average of the betas of the stocks in the

portfolio, so

Stock

Weight

Beta

Weight × Beta

Amazon.com

20/105

3.02

0.58

Coca-Cola

50/105

0.62

0.30

Merck Pharmaceuticals

35/105

1.11

0.37

Portfolio beta

1.24

Kraska would attempt to keep the portfolio beta close to 1.

Additional Problems with Solutions

1. Comparing HPRs, APRs and EARs. Two years ago, Jim bought 100 shares of IBM stock at $50

per share and just sold them for $65 per share after receiving dividends worth $3 per share

over the two-year holding period. Mary, bought 5 ounces of gold at $800 per ounce, three

months ago and just sold it for $1,000 per ounce. Calculate each investor’s HPR, APR, and

EAR and comment on your findings.

ANSWER (Slides 8-61 to 8-63)

Jim’s holding period (n) = 2 years

Chapter 8 ◼ Risk and Return 293

© 2016 Pearson Education, Inc.

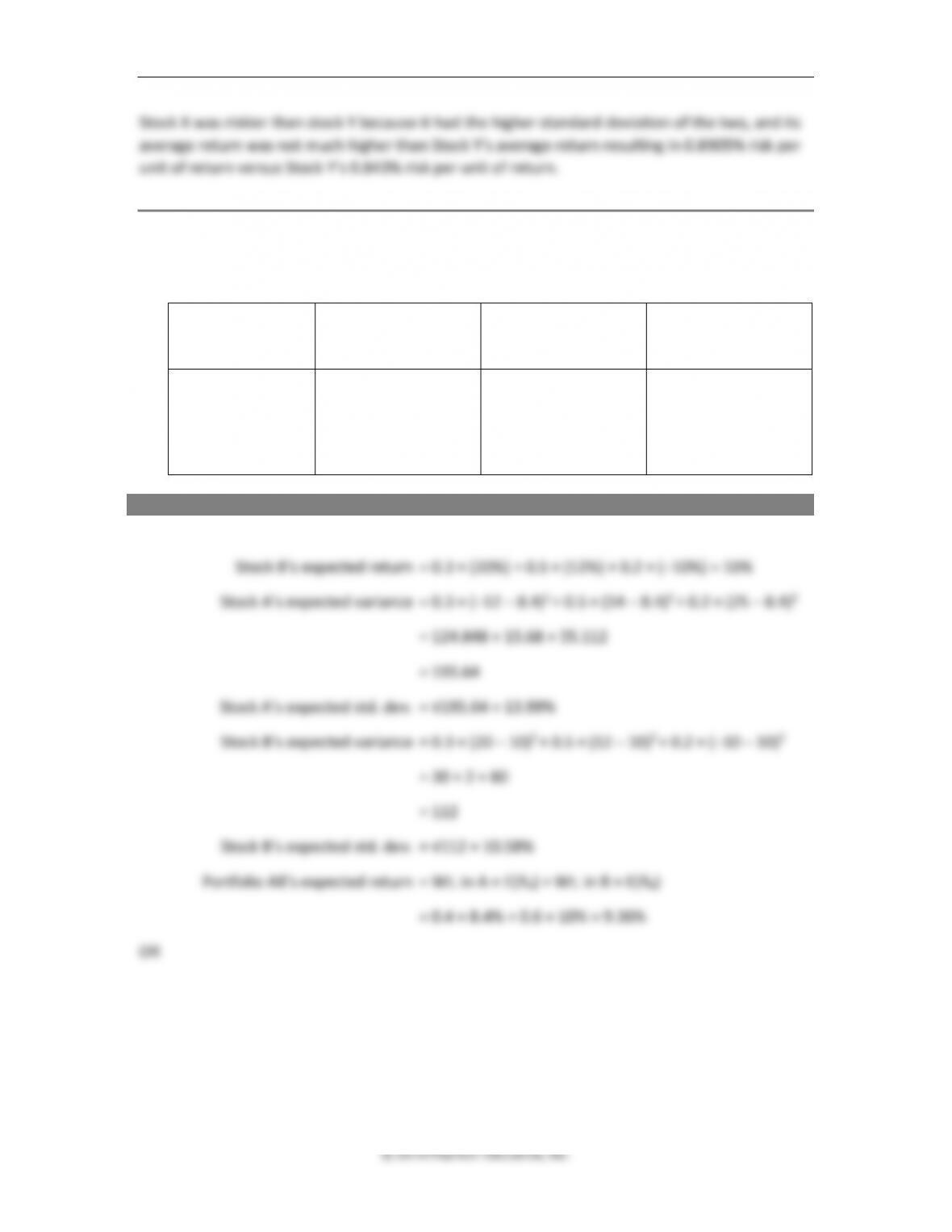

Stock X was riskier than stock Y because it had the higher standard deviation of the two, and its

average return was not much higher than Stock Y’s average return resulting in 0.8905% risk per

unit of return versus Stock Y’s 0.843% risk per unit of return.

3. Calculating ex-ante risk and return measures. Using the probability distribution shown

below, calculate the expected risk and return estimates of each stock and of a portfolio

comprised of 40% of stock A and 60% of stock B.

State of Economy

Probability of State

occurring

Stock A's Conditional

return

Stock B's Conditional

return

Recession

0.3

–12%

20%

Normal

0.5

14%

12%

Boom

0.2

25%

–10%

ANSWER (Slides 8-67 to 8-69)

Stock A’s expected return = 0.3 × (–12%) + 0.5 × (14%) + 0.2 × (25%) = 8.4%

294 Brooks ◼ Financial Management: Core Concepts, 4e

© 2018 Pearson Education, Inc.

We can calculate the portfolio’s conditional returns and then compute the expected return and

standard deviation/variance.

Portfolio AB’s recession return = 0.4 × (–12) + 0.6 × (20) = 7.2%

Portfolio AB’s normal return = 0.4 × (14) + 0.6 × (12) = 12.8%

Portfolio AB’s boom return = 0.4 × (25) + 0.6 × (–10) = 4%

Portfolio AB’s expected return = 0.3 × 7.2 + 0.5 × 12.8 + 0.2 × 4 = 9.36%

Portfolio AB’s expected variance = 0.3 × (7.2 – 9.36)2 + 0.5 × (12.8 – 9.36)2 + 0.2

× (4 – 9.36)2

= 1.39968 + 5.9168 + 5.74592

= 13.0624

Portfolio AB’s expected std. dev. = √13.0624 = 3.61%

4. Calculate a portfolio’s expected rate of return using the CAPM. Annie is curious to know

what her portfolio’s CAPM-based expected rate of return should be. After doing some

research she figures out the market values and betas of each of her five stocks (shown

below) and is told by her consultant that the risk-free rate is 3% and the market risk

premium is 8%. Help Annie calculate her portfolio’s expected rate of return.

ANSWER (Slides 8-70 to 8-72)

Stock Value Weight Beta

Chapter 8 ◼ Risk and Return 295

© 2016 Pearson Education, Inc.

Next, using the CAPM equation and rf = 3%, E(rm – rf) = 8%; calculate the portfolio’s expected

rate.

E(rp) = 3% + 8% × (0.692) = 8.54%

5. Applying the CAPM to determine market attractiveness.

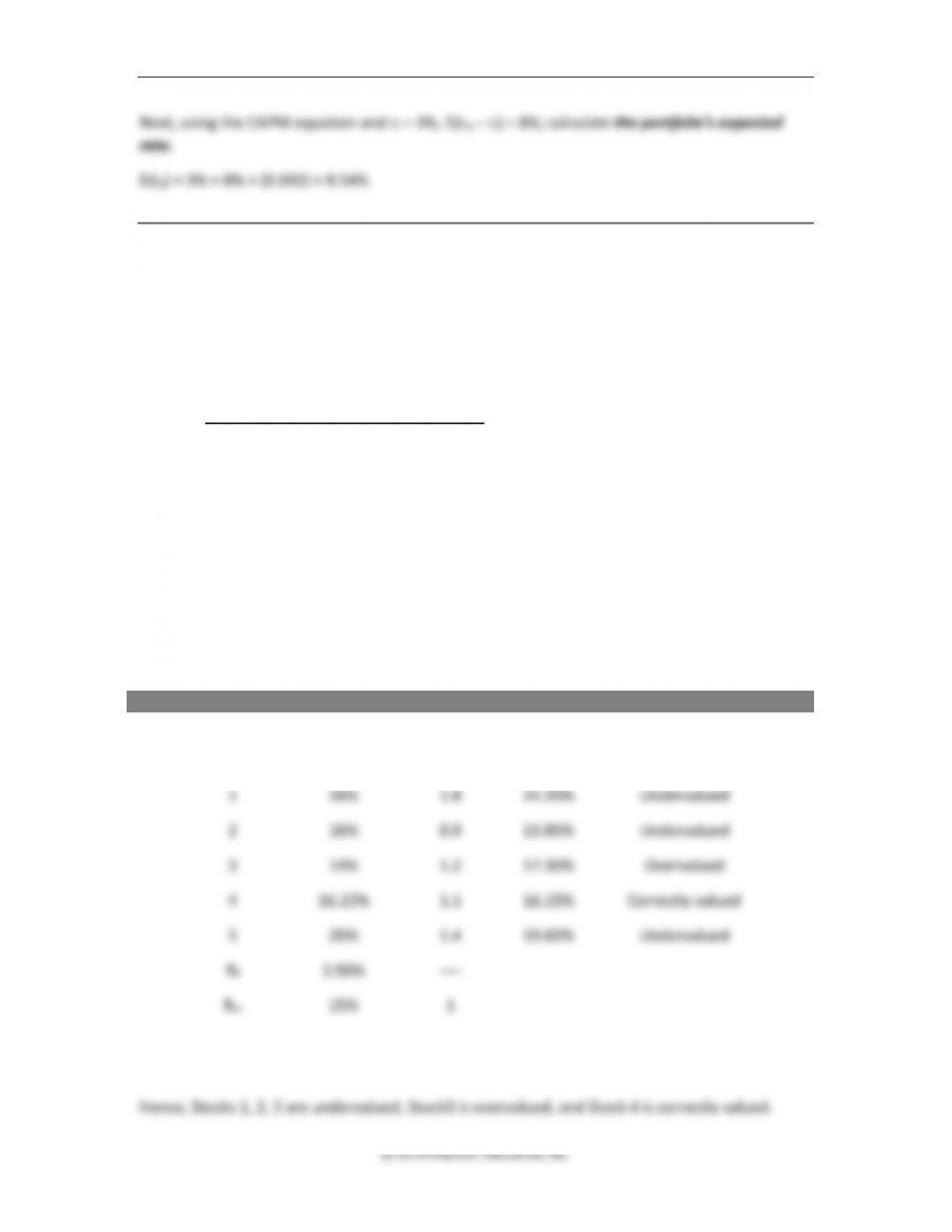

a. Annie is curious to know whether the following five stocks are appropriately valued in

the market. Accordingly, she creates a table (shown below) listing the betas of each

stock along with their ex-ante expected return values that have been calculated using a

probability distribution. She also lists the current risk-free rate and the expected rate of

return on the broad market index. Help her out and state your steps.

Stock Expected Return Beta

1 26.00% 1.8

2 16.00% 0.9

3 14.00% 1.2

4 16.15% 1.1

5 20.00% 1.4

Rf 3.50% ----

Rm 15.00% 1.0

ANSWER (a) (Slides 8-73 to 8-76)

Step 1. Using the CAPM equation, calculate the risk-based return of each stock.

Stock

Expected Return

Beta

CAPM E(Ri)

Comment

1

26%

1.8

24.20%

Undervalued

2

16%

0.9

13.85%

Undervalued

3

14%

1.2

17.30%

Overvalued

4

16.15%

1.1

16.15%

Correctly valued

5

20%

1.4

19.60%

Undervalued

Rf

3.50%

----

Rm

15%

1

Step 2. If CAPM-based E(R) is less than the ex-ante return listed, the stock is undervalued, i.e., it

is expected to earn a higher rate than it should, based on its beta.

296 Brooks ◼ Financial Management: Core Concepts, 4e

b. If Annie wants to form a two-stock portfolio of the most undervalued stocks with a beta

of 1.3, how much will she have to weight each of the stocks by?

ANSWER (b)

Based on the results in (a), stocks 1 and 2 are most undervalued and would be chosen by Annie

to form the two-stock portfolio with a beta = 1.3.