Chapter 8 ◼ Risk and Return 239

© 2016 Pearson Education, Inc.

Unsystematic risk is firm-specific risk, while systematic risk is risk that varies with changes in

the economy. You can avoid unsystematic risk by diversification. You cannot avoid

systematic risk.

240 Brooks ◼ Financial Management: Core Concepts, 4e

12. What is beta in the finance world? What is standard deviation in the finance world? What

type of risk does each measure? What assumption do you make about the stock when you

use beta as a measure of its risk?

Prepping for Exams

1. a.

10. b.

Problems

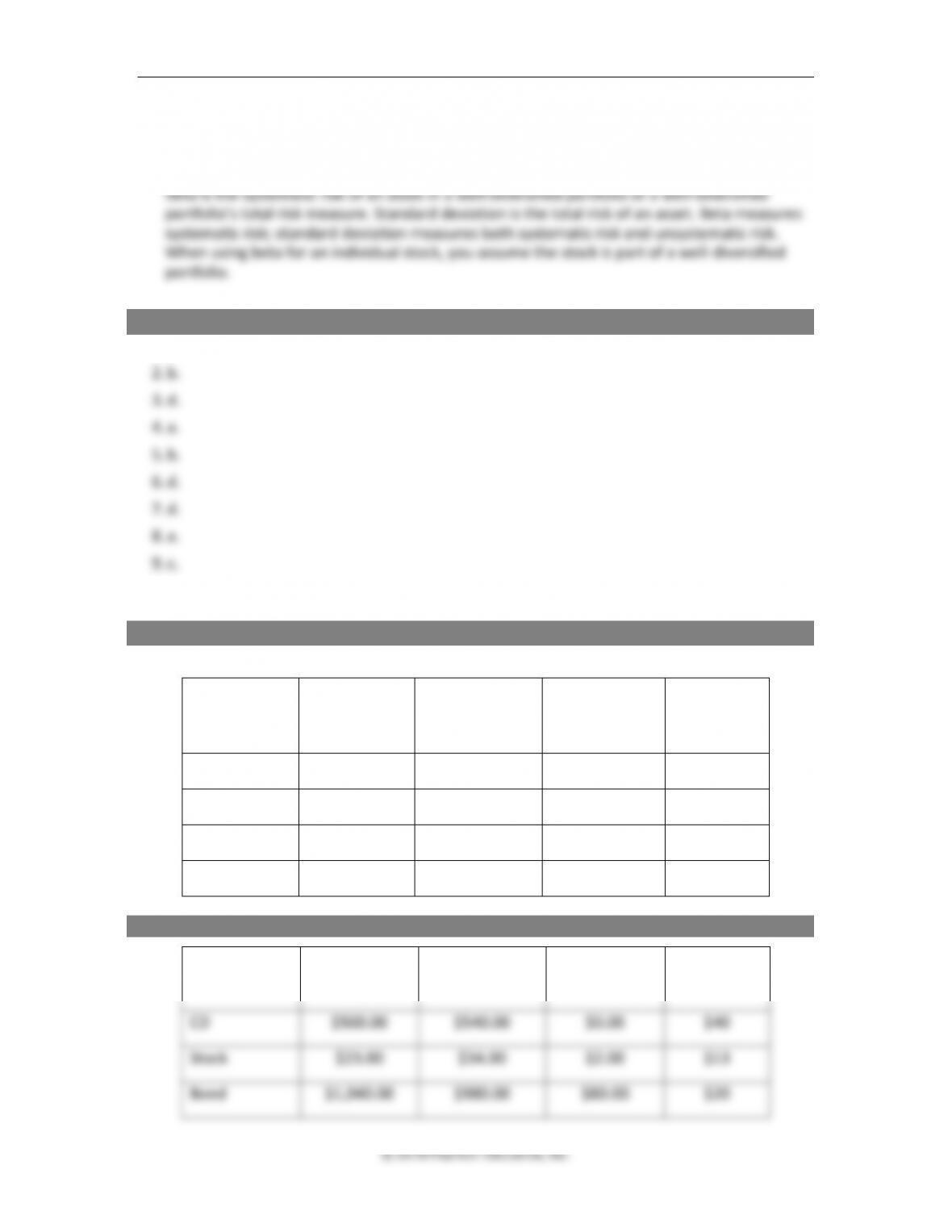

1. Profits. What are the profits on the following investments?

Investment

Original Cost

or Invested $

Selling Price of

Investment

Distributions

Received $

Dollar Profit

CD

$500.00

$540.00

$0.00

Stock

$23.00

$34.00

$2.00

Bond

$1,040.00

$980.00

$80.00

Bike

$400.00

$220.00

$0.00

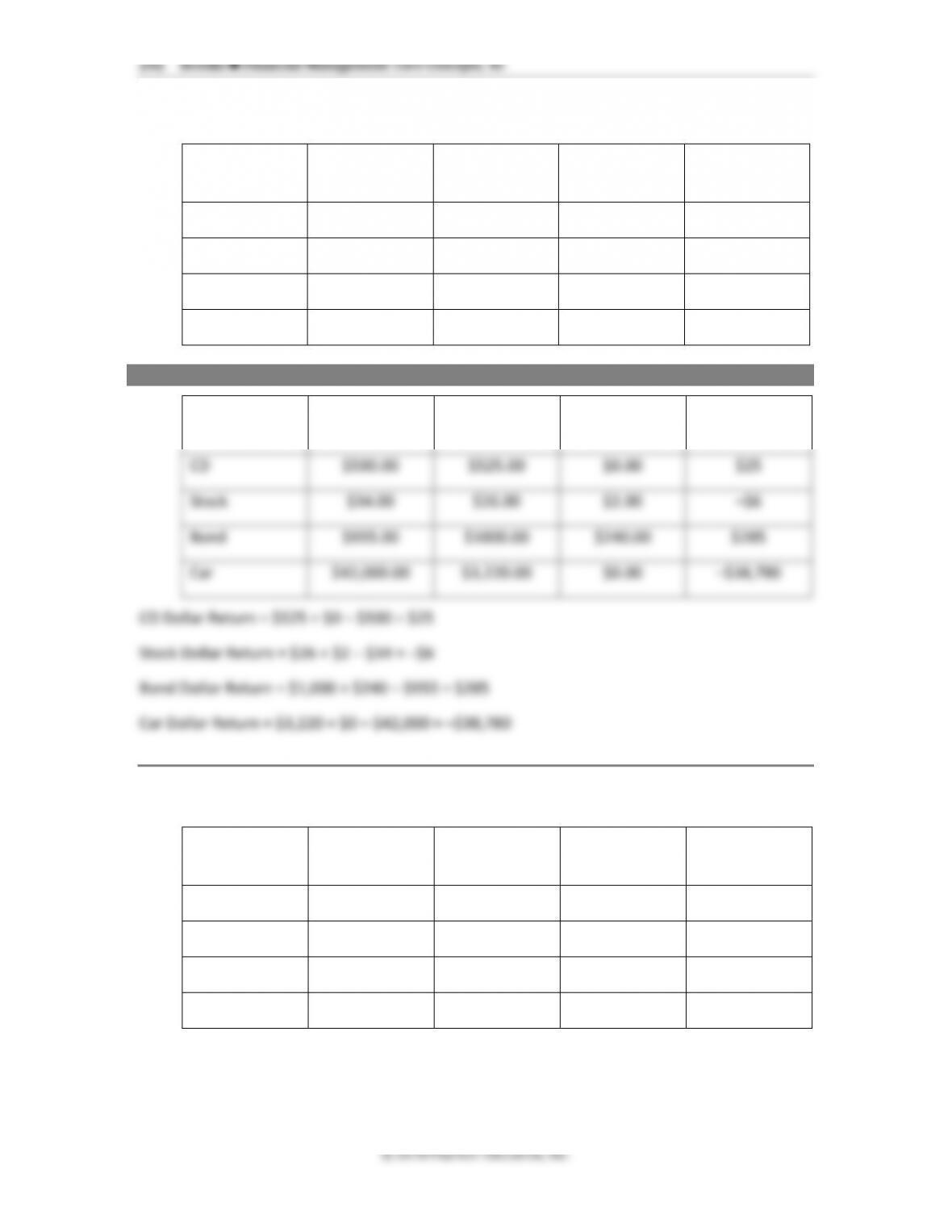

ANSWER

Investment

Original Cost

or Invested $

Selling Price of

Investment

Distributions

Received $

Dollar Profit

CD

$500.00

$540.00

$0.00

$40

Stock

$23.00

$34.00

$2.00

$13

Bond

$1,040.00

$980.00

$80.00

$20

Chapter 8 ◼ Risk and Return 241

© 2016 Pearson Education, Inc.

Bike

$400.00

$220.00

$0.00

–$180

CD Dollar Return = $540 + $0 – $500 = $40

Stock Dollar Return = $34 + $2 – $23 = $13

Bond Dollar Return = $980 + $80 – $1,040 = $20

Bike Dollar Return = $220 + $0 – $400 = –$180

Chapter 8 ◼ Risk and Return 243

ANSWER

Investment

Original Cost or

Invested $

Selling Price of

Investment

Distributions

Received $

Percent Return

CD

$500.00

$540.00

$0.00

8.00%

Stock

$23.00

$34.00

$2.00

56.52%

Bond

$1,040.00

$980.00

$80.00

1.92%

Bike

$400.00

$220.00

$0.00

–45.00%

CD Percent Return = ($540 + $0 – $500) / $500 = 0.0500 or 8.00%

Stock Percent Return = ($34 + $2 – $23) / $23 = 0.565217 or 56.52%

Bond Percent Return = ($980 + $80 – $1040) / $1040 = 0.01923 or 1.92%

Bike Percent Return = ($220 + $0 – $400) / $400 = –0.45 or –45%

Chapter 8 ◼ Risk and Return 245

© 2016 Pearson Education, Inc.

PV= –35; FV = 180; N = 5; PMT = 0; I = 38.75%

6. Holding Period and Annual (Investment) Returns. Bohenick Classic Automobiles restores

and rebuilds old classic cars. The company purchased and restored a classic 1957

Thunderbird convertible six years ago for $8,500. Today at auction, the car sold for $50,000.

What are the holding period return and the annual return on this investment?

ANSWER

7. Comparison of returns. Looking back at Problems 5 and 6, which investment had the higher

holding period return? Which had the higher annual return?

ANSWER

8. Comparison of returns. WG Investors are looking at three different investment

opportunities. Investment one is a five-year investment with a cost of $125 and a promised

payout of $250 at maturity. Investment two is a seven-year investment with a cost of $125

and a promised payout of $350. Investment three is a ten-year investment with a cost of

$125 and a promised payout of $550. WG Investors can only take on one of the three

investments. Assuming all three investment opportunities have the same level of risk,

calculate the annual return for each investment, and select the best investment choice.

246 Brooks ◼ Financial Management: Core Concepts, 4e

ANSWER

Holding Period Return for Investment One = ($250 – $125) / $125 = 1.00 or 100.00%

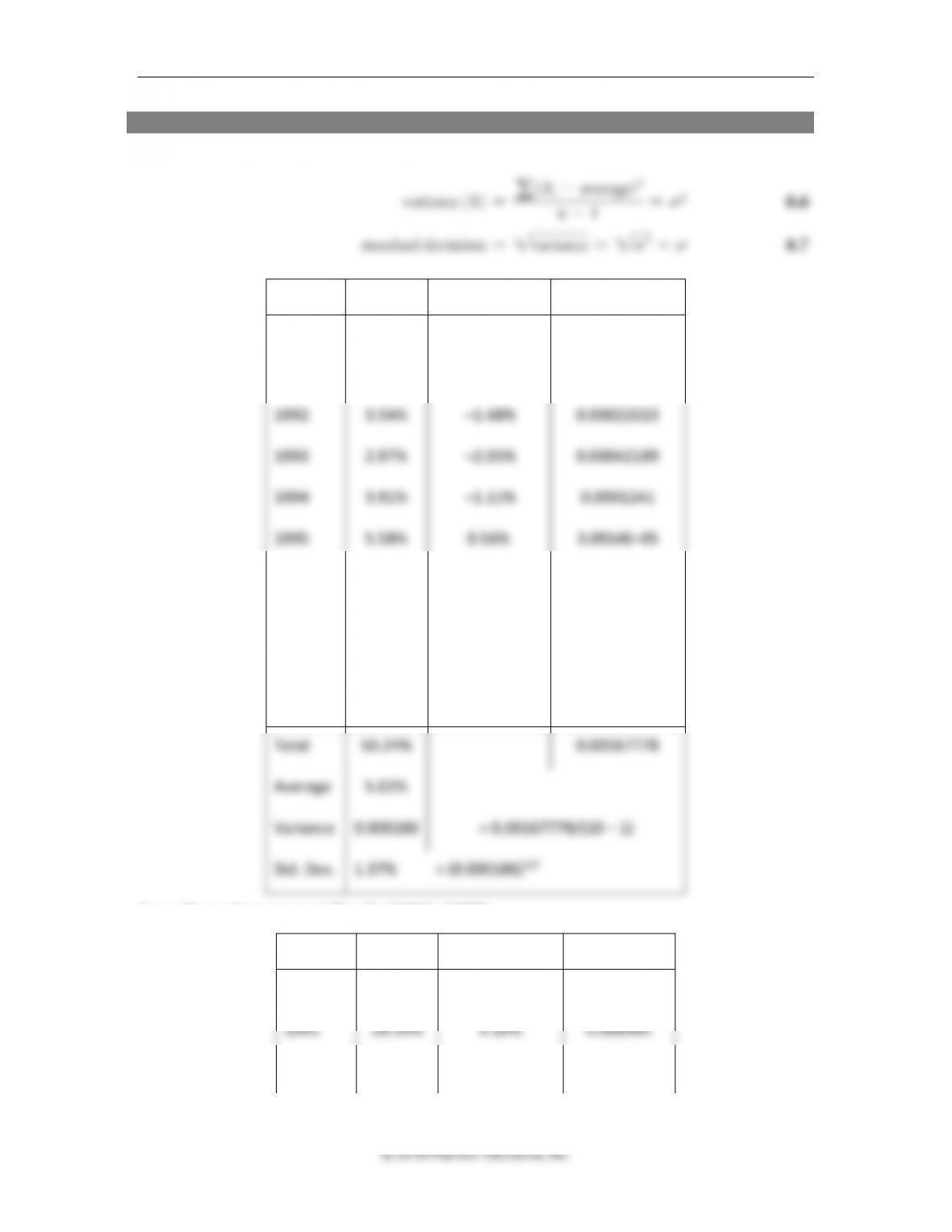

9. Historical returns. Calculate the average return of U.S. Treasury bills, long-term government

bonds, and large company stocks for 1990 to 1999 from Table 8.1. Which had the highest

and which had the lowest return?

ANSWER

248 Brooks ◼ Financial Management: Core Concepts, 4e

ANSWER

U.S. Treasury Bills (1990–1999)

Year

Return

(R – Average)

(R – Average)2

1990

7.86%

2.84%

0.00080429

1991

5.65%

0.63%

3.9188E–05

1992

3.54%

–1.48%

0.00022023

1993

2.97%

–2.05%

0.00042189

1994

3.91%

–1.11%

0.0001241

1995

5.58%

0.56%

3.0914E–05

1996

5.50%

0.48%

2.2658E–05

1997

5.32%

0.30%

8.7616E–06

1998

5.11%

0.09%

7.396E–07

1999

4.80%

–0.22%

5.0176E–06

Total

50.24%

0.00167778

Average

5.02%

Variance

0.000186

= 0.00167778/(10 – 1)

Std. Dev.

1.37%

= (0.000186)1/2

Long-Term Government Bonds (1990–1999)

Year

Return

(R – Mean)

(R – Mean)2

1990

7.13%

–2.10%

0.000442

1991

18.39%

9.16%

0.008385

1992

7.79%

–1.44%

0.000208

Chapter 8 ◼ Risk and Return 249

1993

15.48%

6.25%

0.003903

1994

–7.18%

–16.41%

0.026939

1995

31.67%

22.44%

0.050342

1996

–0.81%

–10.04%

0.010086

1997

15.08%

5.85%

0.003419

1998

13.52%

4.29%

0.001838

1999

–8.74%

–17.97%

0.032303

Total

92.33%

0.137864

Mean

9.23%

Variance

0.015318

= 0.137864/(10 – 1)

Std. Dev.

12.38%

= (0.015318)1/2

U.S. Large Company Stocks

Year

Return

(R – Mean)

(R – Mean)2

1990

–3.20%

–22.19%

0.04924

1991

30.66%

11.67%

0.013619

1992

7.71%

–11.28%

0.012724

1993

9.87%

–9.12%

0.008317

1994

1.29%

–17.70%

0.031329

1995

37.71%

18.72%

0.035044

1996

23.07%

4.08%

0.001665

1997

33.17%

14.18%

0.020107

1998

28.58%

9.59%

0.009197

1999

21.04%

2.05%

0.00042

Total

189.90%

0.181662

Chapter 8 ◼ Risk and Return 251

© 2016 Pearson Education, Inc.

Year

T-Bills

L-T Gov. Bonds

Large Stocks

Small Co. Stocks

Std.Dev

0.74%

4.59%

19.99%

29.46%

Standard Deviation for U.S. Treasury bill for 1950s: 0.74%; Variance = 0.000055

Standard Deviation for U.S. Long-Term Government Bonds for 1950s: 4.59%

Standard Deviation for U.S. Small Company Stocks for 1950s: 29.46%

252 Brooks ◼ Financial Management: Core Concepts, 4e

1960s

Year

T-Bills

L-T Gov. Bonds

Large Stocks

Small Co. Stocks

1960

2.66%

13.78%

0.19%

–5.16%

1961

2.13%

0.19%

27.63%

30.48%

1962

2.72%

6.81%

–8.79%

–16.41%

1963

3.12%

–0.49%

22.63%

12.20%

1964

3.54%

4.51%

16.67%

18.75%

1965

3.94%

–0.27%

12.50%

37.67%

1966

4.77%

3.70%

–10.25%

–8.08%

1967

4.24%

–7.41%

24.11%

103.39%

1968

5.24%

–1.20%

11.00%

50.61%

1969

6.59%

–6.52%

–8.33%

–32.27%

Average

3.90%

1.31%

8.74%

19.12%

Var

0.000186

0.003915

0.021117

0.153854

Std.Dev

1.36%

6.26%

14.53%

39.22%

1970s

Year

T-Bills

L-T Gov. Bonds

Large Stocks

Small Co. Stocks

1970

6.50%

12.69%

4.10%

–16.54%

1971

4.34%

17.47%

14.17%

18.44%

1972

3.81%

5.55%

19.14%

–0.62%

1973

6.91%

1.40%

–14.75%

–40.54%

1974

7.93%

5.53%

–26.40%

–29.74%

Chapter 8 ◼ Risk and Return 253

1975

5.80%

8.50%

37.26%

69.54%

1976

5.06%

11.07%

23.98%

54.81%

1977

5.10%

0.90%

–7.26%

22.02%

1978

7.15%

–4.16%

6.50%

22.29%

1979

10.45%

9.02%

18.77%

43.99%

Average

6.31%

6.80%

7.55%

14.37%

Var

0.000381

0.0040207

0.037099

0.131502

Std.Dev

1.95%

6.34%

19.26%

36.26%

254 Brooks ◼ Financial Management: Core Concepts, 4e

1980s

Year

T-Bills

L-T Gov. Bonds

Large Stocks

Small Co. Stocks

1980

11.57%

13.17%

32.48%

35.34%

1981

14.95%

3.61%

–4.98%

7.79%

1982

10.71%

6.52%

22.09%

27.44%

1983

8.85%

–0.53%

22.37%

34.49%

1984

10.02%

15.29%

6.46%

–14.02%

1985

7.83%

32.68%

32.00%

28.21%

1986

6.18%

23.96%

18.40%

3.40%

1987

5.50%

–2.65%

5.34%

–13.95%

1988

6.44%

8.40%

16.86%

21.72%

1989

8.32%

19.49%

31.34%

8.37%

Average

9.04%

11.99%

18.24%

13.88%

Var

0.0008

0.0124889

0.016021

0.034069

Std.Dev

2.88%

11.18%

12.66%

18.46%

13. Treasury rates. Find the thirteen-week Treasury bill rates for the years 2000 to 2017 shown

in the table below. What was the average from 2000 to 2017? What was the standard

deviation of this sample of auction rates? How does it compare with the data presented in

Table 8.1?

ANSWER:

Year

T-Bill rate

(R – Avg)

(R – Avg)2

2000

5.32%

3.44%

0.001186037

2001

6.60%

4.72%

0.002231513

Chapter 8 ◼ Risk and Return 255

2002

2.15%

0.27%

7.50151E-06

2003

1.35%

–0.53%

2.76793E-05

2004

0.98%

–0.90%

8.03015E-05

2005

2.20%

0.32%

1.04904E-05

2006

4.12%

2.24%

0.000503504

2007

5.09%

3.21%

0.001032908

2008

3.53%

1.65%

0.000273535

2009

0.81%

–1.07%

0.000113659

2010

0.24%

–1.64%

0.000267686

2011

0.20%

–1.68%

0.000280935

2012

0.07%

–1.81%

0.000326204

2013

0.12%

–1.76%

0.000308393

2014

0.09%

–1.79%

0.000319019

2015

0.07%

–1.81%

0.000326204

2016

0.29%

–1.59%

0.000251575

2017

0.54%

–1.34%

0.000178519

Total

33.77%

Sum of (R – Avg)2

➔0.007725663

Average

1.88%

Variance

0.00045

0.000454451

S.Dev

2.13%

0.021317851

14. Internet exercise. Find the Standard & Poor’s 500 annual returns for 2000 to the present. Go

to Yahoo! Finance (www.finance.yahoo.com), and in the “Get Quotes” search field, enter

SPY (the ticker symbol for the Standard & Poor’s 500 electronically traded fund). Select

historical prices and find the year-end prices for the fund and all dividends from 2000

through the end of the most recent year. Find each year’s return (remember to add in the

dividend distributions for the year). What was the average annual return? What was the

standard deviation? How does it compare with the data presented in Table 8.1?

256 Brooks ◼ Financial Management: Core Concepts, 4e

ANSWER

Note: We used data for the period 1999–2010

Year End Price of SPY (1999–2010) and annual Dividends and annual Return

Price Dividends (annual) Return

1999 146.88

2000 131.19 1.454 – 9.69%

2004 120.87 2.197 10.59%

2005 124.51 2.149 4.79%

2006 141.62 2.446 15.71%

2007 146.21 2.701 5.15%

The early years of the start of this decade had negative returns for three consecutive years, and

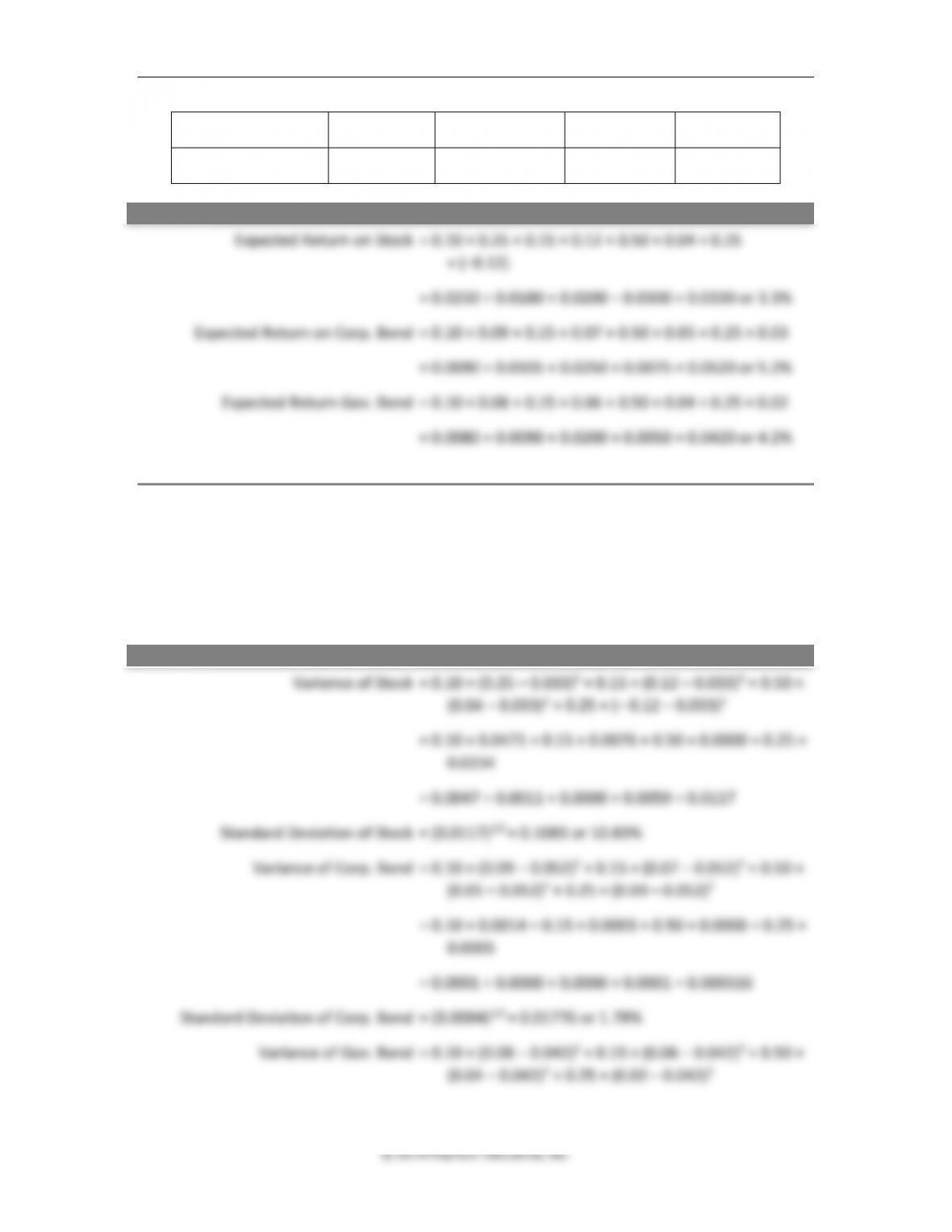

15. Expected return. Hull Consultants, a famous think tank in the Midwest, has provided

probability estimates for the four potential economic states for the coming year. The

probability of a boom economy is 10%, the probability of a stable growth economy is 15%,

the probability of a stagnant economy is 50%, and the probability of a recession is 25%.

Estimate the expected returns on the following individual investments for the coming year.

INVESTMENT

Forecasted Returns for Each Economy

Boom

Stable Growth

Stagnant

Recession

Stock

25%

12%

4%

–12%

Chapter 8 ◼ Risk and Return 257

Corporate Bond

9%

7%

5%

3%

Government Bond

8%

6%

4%

2%

ANSWER

16. Variance and standard deviation (expected). Using the data from Problem 15, calculate the

variance and standard deviation of the three investments, stock, corporate bond, and

government bond. If the estimates for both the probabilities of the economy and the

returns in each state of the economy are correct, which investment would you choose,

considering both risk and return? Why?

ANSWER

258 Brooks ◼ Financial Management: Core Concepts, 4e

© 2018 Pearson Education, Inc.

= 0.10 × 0.0014 + 0.15 × 0.0003 + 0.50 × 0.0000 + 0.25 ×

0.0005

= 0.0001 + 0.0000 + 0.0000 + 0.0001 = 0.000316

Standard Deviation of Gov. Bond = (0.000316)1/2 = 0.01776 or 1.78%