220 Brooks ◼ Financial Management: Core Concepts, 4e

20. Dividend growth rate: Using Yahoo! Finance, update the dividends of Intel for only the last

six years. Find the arithmetic growth rate and the geometric growth rate of the dividends.

(Note: we used 2005–10 for this solution)

ANSWER

Year

Dividend

Change (percent)

2010

$0.632

$0.632 – $0.56 = $0.072 ($0.072/$0.56 = 12.86%)

2009

$0.56

$0.56 – $0.546 = $0.014 ($0.014/$0.546 = 2.56%)

2008

$0.546

$0.546 – $0.452 = $0.094 ($0.094/$0.452 = 20.80%)

2007

$0.452

$0.452 – $0.40 = $0.052 ($0.052 / $0.40 = 13.00%)

2006

$0.40

$0.40 – $0.32 = $0.08 ($0.08 / $0.32 = 25.00%)

2005

$0.32

21. Rate of return. Using the answer to Problem 17 on Coca-Cola’s growth rates and the current

trading price, determine the current required rate of return for the company.

$65.22

22. Rate of return. Using the answer to Problem 18 on the Johnson & Johnson growth rates and

the current trading price, determine the current required rate of return for the company.

ANSWER

Chapter 7 ◼ Stocks and Stock Valuation 221

© 2018 Pearson Education, Inc.

Johnson and Johnson’s

( )

$2.11 1 0.13.04 0.1304

$62.82

r+

=+

= 0.1684 or 16.84%

23. Rate of return. Using the answer to Problem 19 on the Walmart growth rates and the

current trading price, determine the current required rate of return for the company.

ANSWER

$54.56

24. Rate of return. Using the answer to Problem 20 on Intel’s growth rates and the current

trading price, determine the current required rate of return for the company.

ANSWER

25. Stock price. Given the growth rates for Coca-Cola, Johnson & Johnson, Walmart, and Intel

from the dividend history in Problems 21 through 24, what price would you predict for each

stock if they all had a required return of 18%? Why are Walmart and Intel prices

troublesome?

ANSWER

$2.11 1 0.1304 $48.09

( )

$1.76 1 0.1044 $25.71

0.18 0.1768

−

222 Brooks ◼ Financial Management: Core Concepts, 4e

© 2018 Pearson Education, Inc.

Intel,

( )

$0.632 1 0.1458 $21.18

0.18 0.1458

P+

==

−

Walmart’s predicted price is unrealistically high since the required rate is so close to the growth

rate. Intel’s price on the other hand seems okay.

26. Rate of return. Assume that Exxon-Mobil’s price dropped to $30 overnight. Given the

dividend growth rate of Exxon-Mobil of 5.07% and the last annual dividend of $1.28, what is

the implied required rate of return necessary to justify the new lower market price of

$30.00?

27. Stock price. Peterson Packaging Incorporated does not currently pay dividends. The

company will start with a $0.50 dividend at the end of year three and grow it by 10% for

each of the next six years until it nearly reaches $1.00. After six years of growth, it will fix its

dividend at $1.00 forever. If you want a 15% return on this stock, what should you pay

today, given this future dividend stream?

ANSWER

Chapter 7 ◼ Stocks and Stock Valuation 223

© 2018 Pearson Education, Inc.

( )

3

2

1

Price 1 1

n

g

Div

r g r

+

= −

−+

( )

7

2

$0.50 1 0.10

Price 1

0.15 0.10 1 0.15

+

= −

−+

Price2 = $10.00 × (0.2674) = $2.674

The price at the end of period 2 is a future value. Now we must discount this future value at 15%

for its present value:

( )

1n

FV

PV

r

=+

Price0 =

( )

2

$2.674 $2.674 $2.02

1.3225

1 0.15

PV = = =

+

The final dividend pattern is a perpetuity and we can use equation 7.1 here:

10

9

Price Dividend

r

=

9

$1.00

Price $6.67

0.15

==

And again, we must discount this future value at 15% for its present value:

( )

09

$6.67

Price $1.90

1 0.15

==

+

Finally, adding the three pieces we get:

Price of Stock = $0.00 + $2.02 + $1.90 = $3.92

Although we now have a way of pricing stocks through discounting dividends, we must realize

that dividends are not a promised future cash flow. In fact, firms can increase, reduce, or even

suspend cash dividends. And even though past dividends may be a good predictor of future

dividends, the timing and amount of dividends can and do vary across time for a company. The

dividend models are really expected dividend models, and if we were to write these models

correctly we would use an expectations operator with the dividends, E(Div0) and E(Div1) instead

of Div0 and Div1.

224 Brooks ◼ Financial Management: Core Concepts, 4e

Solutions to Advanced Problems for Spreadsheet Applications

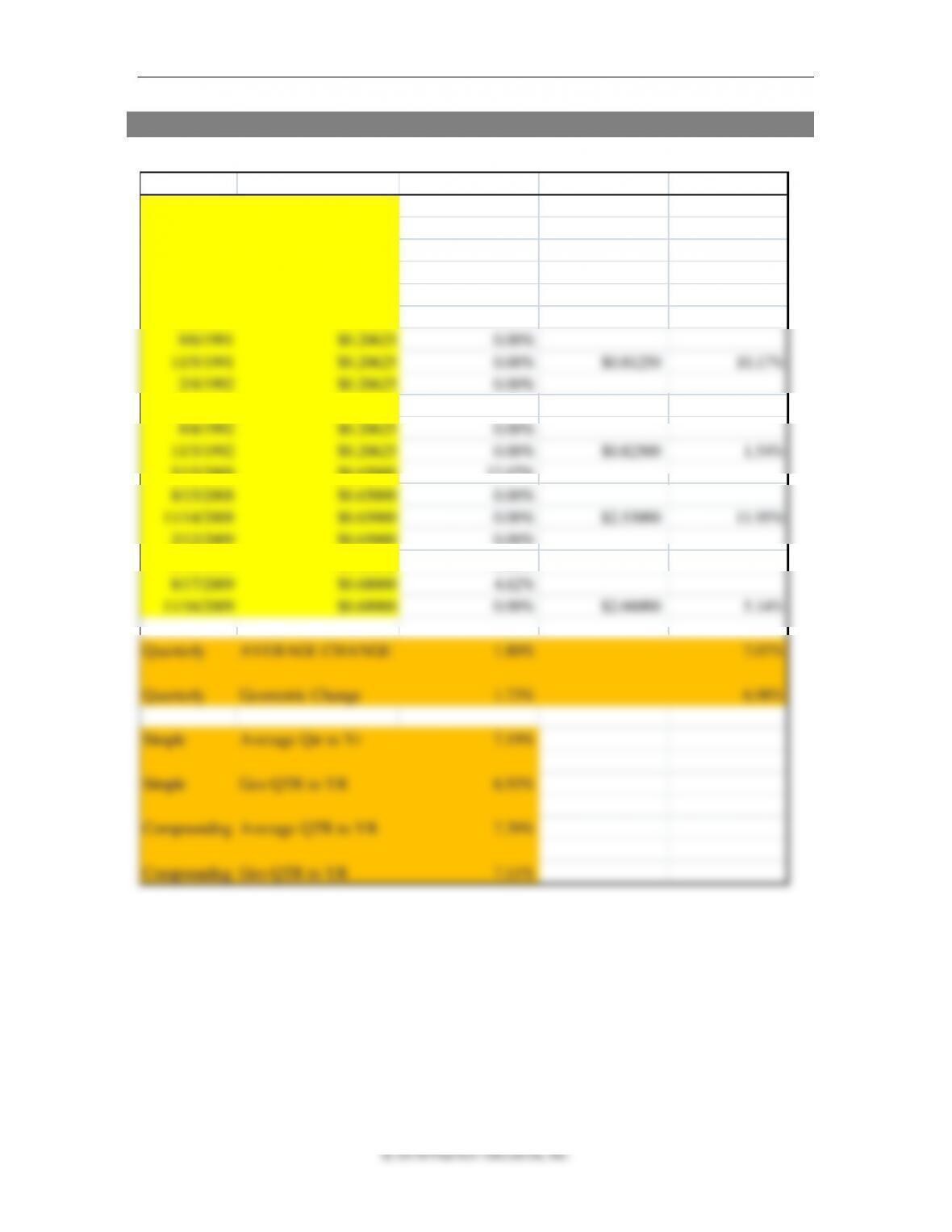

1. Dividend history and dividend growth rates

Date Dividend Quarterly Change Annual Dividend Annual Change

2/7/1990 $0.17500

5/1/1990 $0.17500 0.00%

7/31/1990 $0.19375 10.71%

11/6/1990 $0.19375 0.00% $0.73750

2/5/1991 $0.19375 0.00%

4/30/1991 $0.20625 6.45%

8/6/1991 $0.20625 0.00%

11/5/1991 $0.20625 0.00% $0.81250 10.17%

2/4/1992 $0.20625 0.00%

5/5/1992 $0.20625 0.00%

8/4/1992 $0.20625 0.00%

11/3/1992 $0.20625 0.00% $0.82500 1.54%

5/15/2008 $0.65000 12.07%

8/15/2008 $0.65000 0.00%

11/14/2008 $0.65000 0.00% $2.53000 11.95%

2/12/2009 $0.65000 0.00%

5/15/2009 $0.65000 0.00%

8/17/2009 $0.68000 4.62%

11/16/2009 $0.68000 0.00% $2.66000 5.14%

Quarterly AVERAGE CHANGE 1.80% 7.07%

Quarterly Geometric Change 1.73% 6.98%

Simple Average Qtr to Yr 7.19%

Simple Geo QTR to YR 6.93%

Compounding Average QTR to YR 7.39%

Compounding Geo QTR to YR 7.11%

Chapter 7 ◼ Stocks and Stock Valuation 225

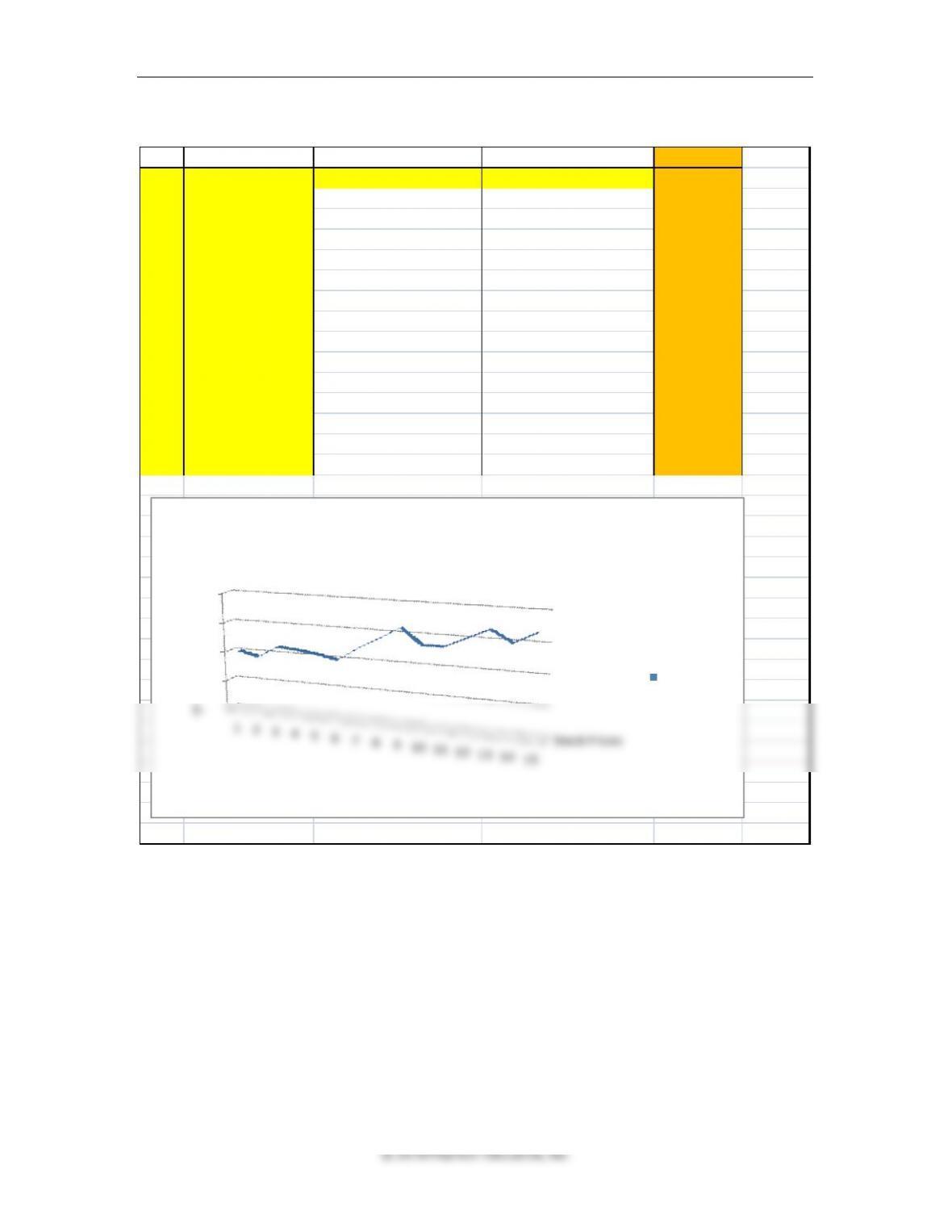

2. Changing stock price year by year.

Year Required Return Most recent Dividend Dividend Growth Rate Stock Price

1 11.20% 2.80$ 4.00% 40.44$

2 12.15% 2.80$ 4.00% 37.16$

3 10.98% 2.80$ 4.00% 45.12$

4 11.45% 2.80$ 4.00% 43.97$

5 12.06% 2.80$ 4.00% 42.27$

6 12.98% 2.80$ 4.00% 39.45$

7 11.55% 2.80$ 4.00% 48.80$

8 10.83% 2.80$ 4.00% 56.11$

9 10.22% 2.80$ 4.00% 64.07$

10 11.73% 2.80$ 4.00% 53.62$

11 11.98% 2.80$ 4.00% 54.02$

12 11.42% 2.80$ 4.00% 60.42$

13 10.96% 2.80$ 4.00% 66.99$

14 12.15% 2.80$ 4.00% 59.49$

15 11.55% 2.80$ 4.00% 66.79$

Stock Prices

$–

$20.00

$40.00

$60.00

$80.00

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Stock Prices

Stock Prices

226 Brooks ◼ Financial Management: Core Concepts, 4e

Solutions to Mini-Case

Lawrence’s Legacy: Part 1

This case requires students to think in a critical and applied way about the nature of common

stock investments, primary and secondary markets, the implications of EMH, stock valuation

models, and the limitations of stock valuation models.

1. Why do you think Lawrence specified to invest money in stocks rather than bonds or

certificates of deposit?

This question can be the stimulus for a broad ranging discussion of the nature of common

stock.

Lawrence wants the memorial trust fund to provide meaningful grants in perpetuity.

2. How will the trust obtain the cash to make the grants if the dividends do not amount to

5% of the portfolio’s value?

Unless stocks are specifically purchased for high dividend yields rather than growth, it is

3. What is the difference between common stock and preferred stock?

Preferred stock usually pays a fixed dividend. As a result, the price moves more closely with

4. How do we know if we are paying a fair price for the stock that we purchase?

Chapter 7 ◼ Stocks and Stock Valuation 227

© 2018 Pearson Education, Inc.

every day. The price we pay will be very close to the price paid by the buyer just before or

after us. Many stock purchases and sales take place between large institutional investors

managed by people with advanced degrees in finance or economics, and whose only job is

to know everything there is to know about the companies they invest in. If these investors

agree to pay a particular price, and equally sophisticated investors agree to sell at the same

price, then the price must reflect all the information it is legally possible to have. These

conditions describe what is known as the semi-strong form of the efficient market

hypothesis, which implies that no investor has an unfair advantage over any other investor.

5. For what are we actually paying when we buy a share of stock?

Kraska intends to use the following examples to answer this question.

a. ABC Inc. preferred stock pays a constant dividend of $5.00 per year. Assume that

investors require a 9% rate of return.

b. DEF, Inc. common stock that recently paid s a dividend of $1.50. The estimated growth

rate of dividends is 6% per year and the required rate of return is 11%.

c. GBH, Inc. pays no dividend and reinvests all of its earnings into rapid growth, but it is

expected to begin paying dividends in five years. The first dividend will be $5.00;

dividends will grow at 5% per year; the required rate of return throughout the period

is 15%.

To the extent that our assumptions are correct, in four years the next dividend will be

6. Why do stock prices change so quickly and by so much?

Notice that the formulas we used depend on forecasts of variables that in themselves

depend on many other forecasts, most of which are very difficult to predict. Future

dividends depend on future earnings, which depend on future costs, future sales volume,

228 Brooks ◼ Financial Management: Core Concepts, 4e

© 2018 Pearson Education, Inc.

and future prices. Future sales depend on competition, changes in technology, geopolitical

events, and so on. The discount rate or required rate of return depends on future inflation,

interest rates, and perceptions of how risky the company is. These estimates all change with

every piece of news, and frankly sometimes with the mood of investors. Realistically, the

market is always looking for the correct price of a stock and never quite finding it, but the

large volume of sales, rapid flow of information, insider trading laws, and the self-interest of

investors assure that we are all trading on the same information. Paradoxically, this is true

whether or not we even have the information because the price is presumably determined

by those who do have it. This is another illustration of the efficient market hypothesis.

Chapter 7 ◼ Stocks and Stock Valuation 229

Additional Problems with Solutions

1. Pricing constant growth stock, with finite horizon. The Crescent Corporation just paid a

dividend of $2.00 per share and is expected to continue paying the same amount each year

for the next four years. If you have a required rate of return of 13%, plan to hold the stock

for four years, and are confident that it will sell for $30 at the end of four years, how much

should you offer to buy it at today?

ANSWER (Slides 7-49 to 7-50)

2. Constant growth rate, infinite horizon (with growth rate estimated from past history.

Using the historical dividend information provided below to calculate the constant growth

rate, and a required rate of return of 18%, estimate the price of Nigel Enterprises’ common

stock.

Nigel Enterprises’ Annual Dividends

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

$0.35

$0.45

$0.51

$0.65

$0.75

$0.88

$0.99

$1.10

$1.13

$1.30

ANSWER (Slides 7-51 to 7-53)

First, estimate the historical average growth rate of dividends by using the following equation:

1

n

FV

0.35

© 2018 Pearson Education, Inc.

3. Pricing common stock with multiple dividend patterns. The Wonder Products Company is

expanding fast and therefore will not pay any dividends for the next three years. After that,

starting at the end of Year 4, it will pay a dividend of $0.75 per share to its common

shareholders and increase it by 12% each year until it pays $1.50 at the end of Year 10. After

that it will pay $1.50 per year forever. If an investor wants to earn 15% per year on this

investment, how much should he pay for the stock?

ANSWER (Slides 7-54 to 7-56)

First lay out the dividends on a time line.