Chapter 5 ◼ Interest Rates 135

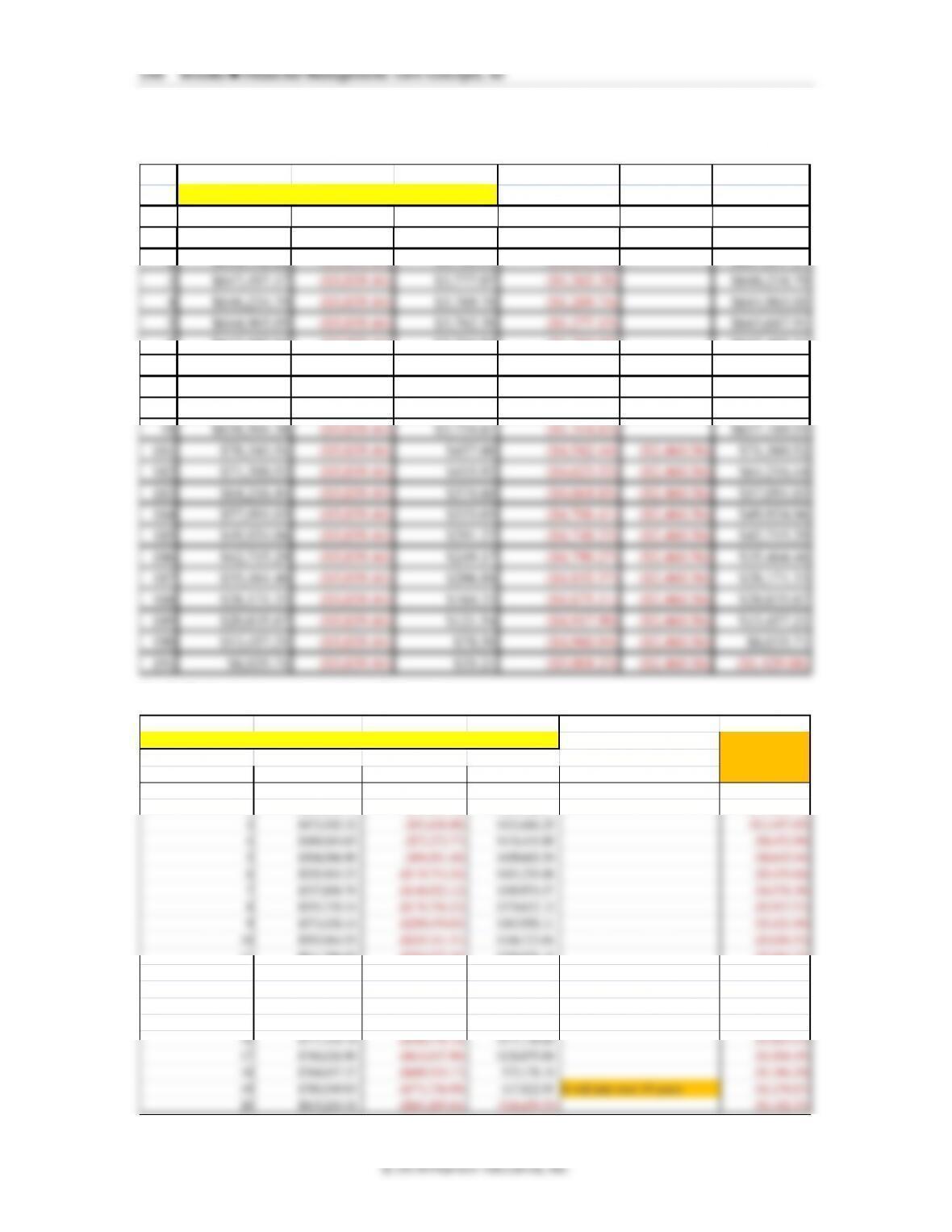

13. Inflation, nominal interest rates, and real rates. Given the following information,

estimate the nominal rate with the approximate nominal interest rate equation and the

true nominal interest rate equation for each set of real and inflation rates.

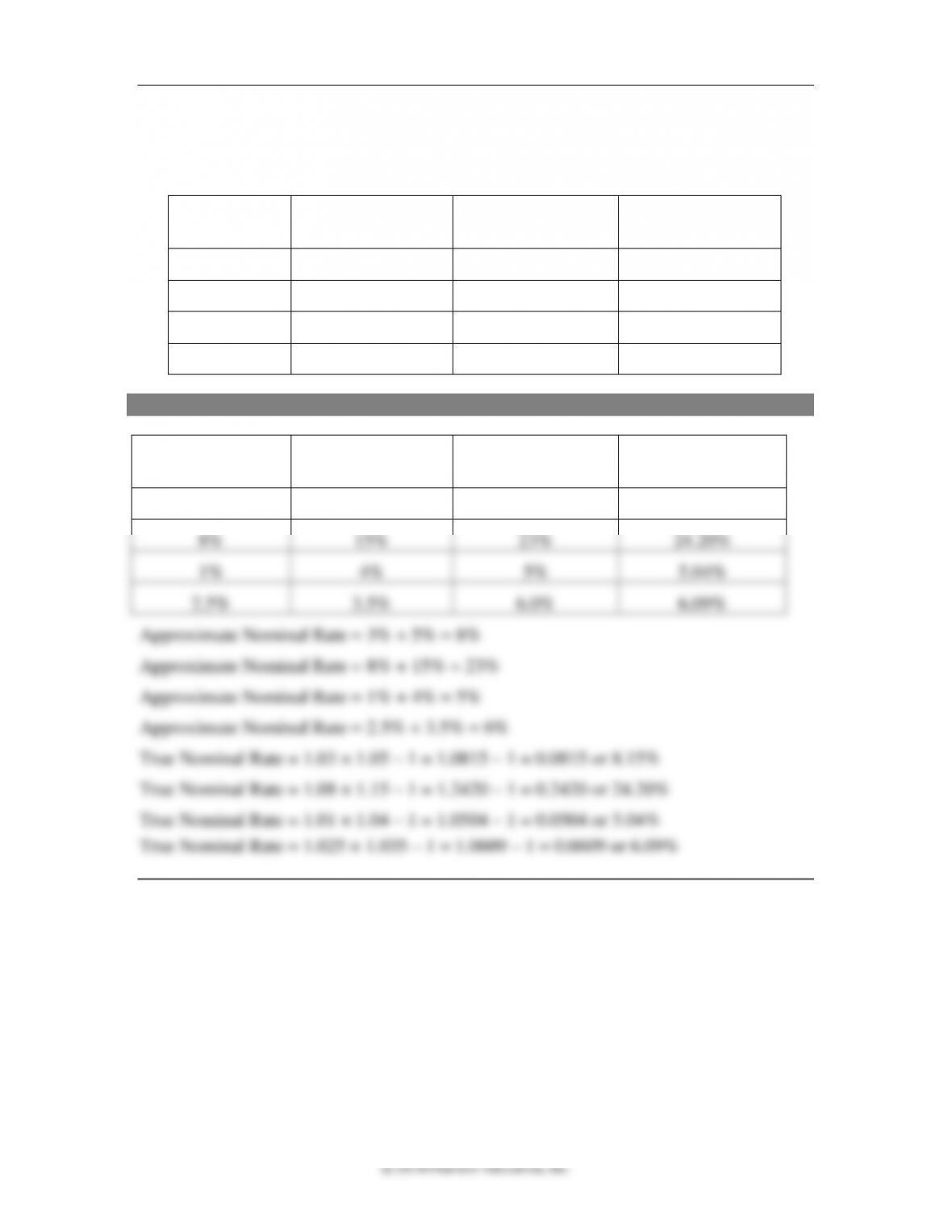

Real Rate

Inflation Rate

Approximate

Nominal Rate

True Nominal Rate

3%

5%

8%

15%

1%

4%

2.5%

3.5%

ANSWER

Real Rate

Inflation Rate

Approximate

Nominal Rate

True Nominal Rate

3%

5%

8%

8.15%

8%

15%

23%

24.20%

1%

4%

5%

5.04%

2.5%

3.5%

6.0%

6.09%

Chapter 5 ◼ Interest Rates 137

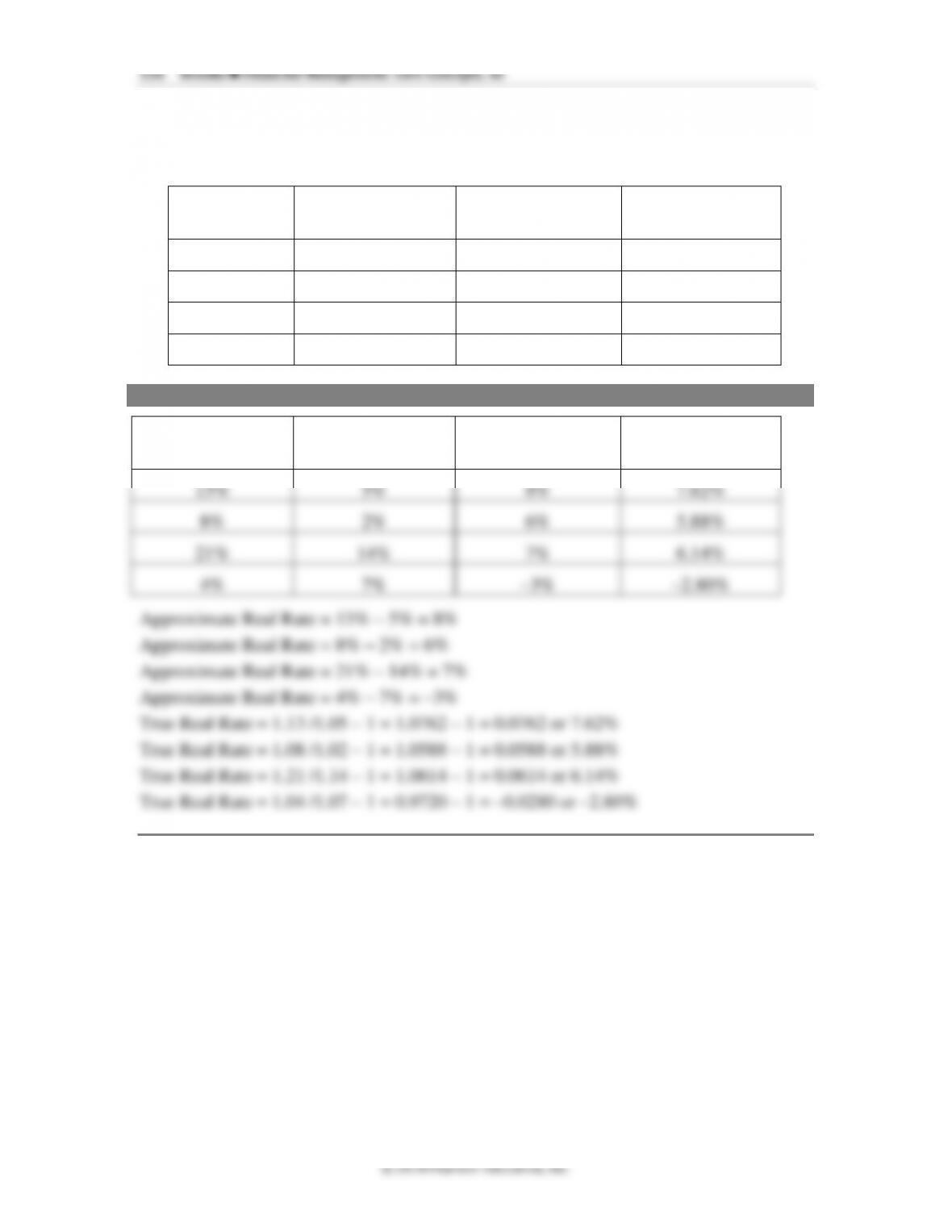

15. Inflation, nominal interest rates, and real rates. Given the information below,

estimate the inflation rate with the approximation formula and the true inflation with

the Fisher Effect formula.

Nominal Rate

Real Rate

Approximate

Inflation

True Inflation

11%

5%

8%

2%

21%

14%

5.5%

1.25%

ANSWER

Nominal Rate

Real Rate

Approximate

Inflation

True Inflation

11%

5%

6%

5.71%

8%

2%

6%

5.88%

21%

14%

7%

6.14%

5.5%

1.25%

4.25%

4.20%

142 Brooks ◼ Financial Management: Core Concepts, 4e

© 2018 Pearson Education, Inc.

Periodic Rate = 0.0816/4 = 0.0204

EAR = 1.02044 – 1 = 8.41%.

Bank Four has the lowest EAR and all else equal, Michael should take the quarterly

payment choice.

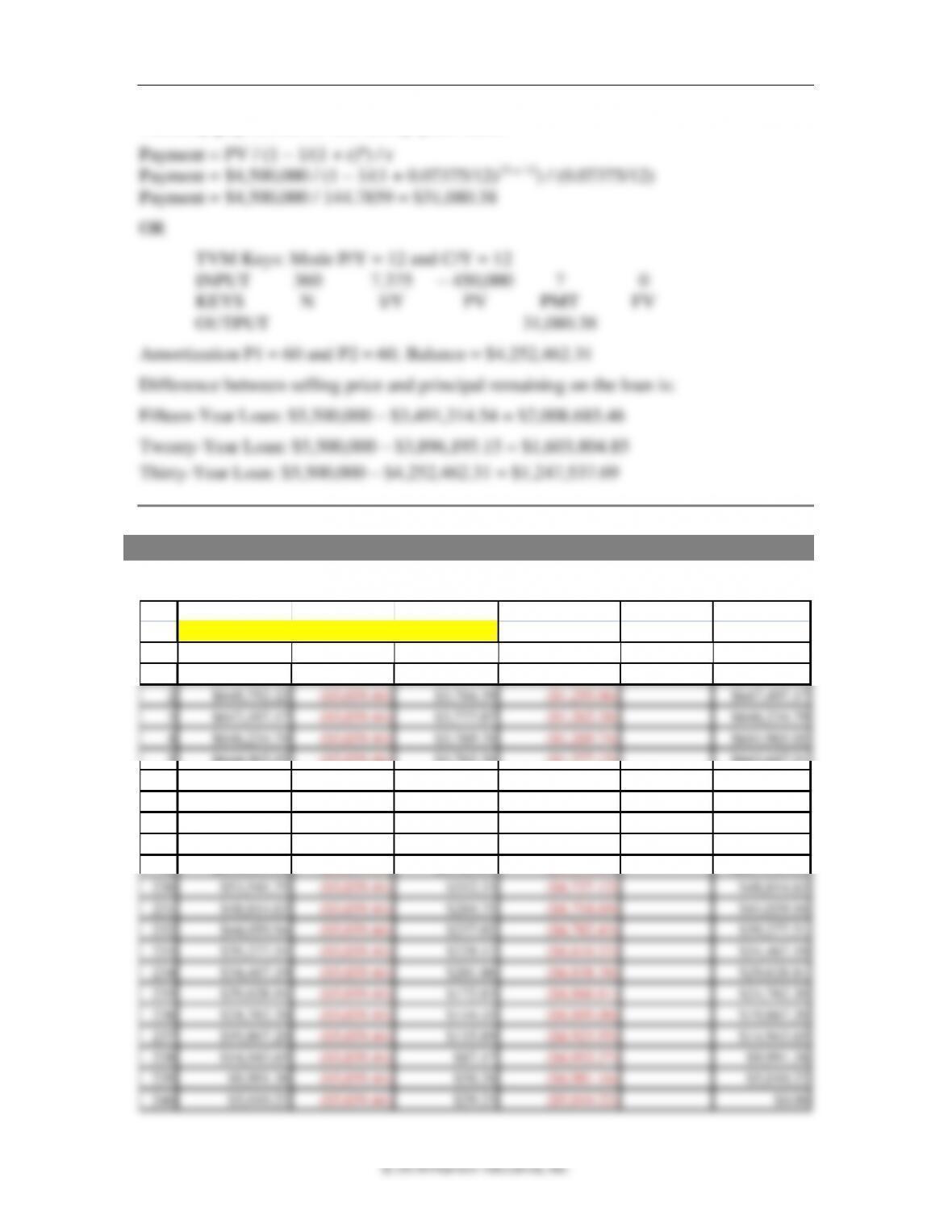

30. Challenge question II. Tyler wants to buy a beach house as part of his investment

portfolio. After searching the coast for a nice home, he finds a house with a great

view and a hefty price of $4,500,000. Tyler will need to borrow the whole amount

from the bank to pay for this house. Mortgage rates are based on the length of the

loan, and a local bank is advertising fifteen-year loans with monthly payments at

7.125%, twenty-year loans with monthly payments at 7.25%, and thirty-year loans

with monthly payments at 7.375%. What is the monthly payment of principal and

interest for each loan? Tyler believes the property will be worth $5,500,000 in five

years. Ignoring taxes and real estate commissions, if Tyler sells the house after five

years, what will be the difference in the selling price and the remaining principal on

the loan for each of the three loans?

ANSWER

Monthly payments for the fifteen-year loan:

OR

Monthly payments for the twenty-year loan:

Payment = PV / (1 – 1/(1 + r)n) / r

Chapter 5 ◼ Interest Rates 143

Monthly payments for the thirty-year loan:

Solutions to Advanced Problems for Spreadsheet Application

1. a. Monthly amortization schedule:

Loan Amount Interes Rate Years for Loan

$650,000.00 7.00% 20

Mnth Beginning Balance Annual Payment Interest Expense Principal Reduction Extra Principal Ending Balance

1$650,000.00 ($5,039.44) $3,791.67 ($1,247.78) $648,752.22

2$648,752.22 ($5,039.44) $3,784.39 ($1,255.06) $647,497.17

3$647,497.17 ($5,039.44) $3,777.07 ($1,262.38) $646,234.79

4$646,234.79 ($5,039.44) $3,769.70 ($1,269.74) $644,965.05

5$644,965.05 ($5,039.44) $3,762.30 ($1,277.15) $643,687.91

6$643,687.91 ($5,039.44) $3,754.85 ($1,284.60) $642,403.31

7$642,403.31 ($5,039.44) $3,747.35 ($1,292.09) $641,111.22

8$641,111.22 ($5,039.44) $3,739.82 ($1,299.63) $639,811.59

9$639,811.59 ($5,039.44) $3,732.23 ($1,307.21) $638,504.38

10 $638,504.38 ($5,039.44) $3,724.61 ($1,314.83) $637,189.55

230 $53,541.75 ($5,039.44) $312.33 ($4,727.12) $48,814.63

231 $48,814.63 ($5,039.44) $284.75 ($4,754.69) $44,059.94

232 $44,059.94 ($5,039.44) $257.02 ($4,782.43) $39,277.51

233 $39,277.51 ($5,039.44) $229.12 ($4,810.32) $34,467.19

234 $34,467.19 ($5,039.44) $201.06 ($4,838.38) $29,628.81

235 $29,628.81 ($5,039.44) $172.83 ($4,866.61) $24,762.20

236 $24,762.20 ($5,039.44) $144.45 ($4,895.00) $19,867.20

237 $19,867.20 ($5,039.44) $115.89 ($4,923.55) $14,943.65

238 $14,943.65 ($5,039.44) $87.17 ($4,952.27) $9,991.38

239 $9,991.38 ($5,039.44) $58.28 ($4,981.16) $5,010.22

240 $5,010.22 ($5,039.44) $29.23 ($5,010.22) $0.00

Chapter 5 ◼ Interest Rates 145

Solutions to Mini-Case

Sweetening the Deal: Povero Construction Company

This case demonstrates the importance of the appropriate use of interest rate terms in the

structuring and marketing of real estate and loan offerings.

1. Povero believes that interest rates are a major factor in the real estate market.

What are the implications of rising, falling, and steady interest rates for future

real estate prices?

In general, rising yield curves indicate that inflation and interest rates will be higher

2. If the risk-free interest rate is 3.86% and the inflation rate is 2.2%, what is the

real rate of interest? Compute the rate with and without the Fisher effect.

3. Interest on a conventional thirty-year fixed-rate mortgage at the time of the case

was 4.75%. At that rate, what is the monthly payment on a $290,000 mortgage?

What is the monthly payment on a $261,000 mortgage?

For the $290,000 mortgage:

For the $261,000 mortgage:

Chapter 5 ◼ Interest Rates 147

Additional Problems with Solutions

1. The First Federal Bank has advertised one of its loan offerings as follows:

“We will lend you $100,000 for up to five years at an APR of 9.5% (interest

compounded monthly).” If you borrow $100,000 for one year and pay it off in one

lump sum at the end of the year, how much interest will you have paid and what is the

bank’s APY?

ANSWER (Slides 5-27 to 5-28)

2. If First Federal offers to structure the 9.5%, $100,000, one-year loan on a monthly

payment basis, calculate your monthly payment and the amount of interest paid at the

end of the year. What is your EAR?

ANSWER (Slides 5-29 to 5-30)

Calculate monthly payment:

N

i/y

PV

PMT

FV

12

9.5/12

100,000

–8,768.35

0