108 Brooks ◼ Financial Management: Core Concepts, 4e

32. Challenge problem. Each holiday season, Michael received a U.S. savings bond from

his grandmother. Michael eventually received twelve savings bonds. The bonds vary in

their rates of interest and their face value. Assume that today is December 31, 2011.

What is the value of this portfolio of U.S. savings bonds? On what dates does each of

the individual bonds reach their face value or maturity date (note that the price is half

the face value)? Estimate to the nearest month and year for each bond. Note: the bonds

continue earning interest past their maturity dates.

Issue Date

Price

Face Value

Interest Rate

Maturity Date

12/31/1990

$50

$100

6.0%

12/31/1991

$50

$100

6.0%

12/31/1992

$25

$50

5.0%

12/31/1993

$25

$50

4.0%

12/31/1994

$25

$50

4.0%

12/31/1995

$50

$100

5.0%

12/31/1996

$25

$50

5.0%

12/31/1997

$25

$50

4.0%

12/31/1998

$25

$50

4.0%

12/31/1999

$50

$100

4.0%

12/31/2000

$25

$50

4.0%

12/31/2001

$25

$50

3.0%

TOTAL

$400

ANSWER

Chapter 4 ◼ The Time Value of Money (Part 2) 109

© 2018 Pearson Education, Inc.

FV#11 (11 years) = $25 × 1.042011–2000 = $25 × 1.5395 = $ 38.49

FV#12 (10 years) = $25 × 1.032011–2001 = $25 × 1.3439 = $ 33.59

TOTAL VALUE $885.42

Maturity Dates of Each Bond: n is the length of time between the issue date and the

maturity date.

N#12 = ln (2 /1) / ln (1.03) = 0.6931/0.0296 = 23.45 years or 23 years and 5 months

110 Brooks ◼ Financial Management: Core Concepts, 4e

Solutions to Advanced Problems for Spreadsheet Application

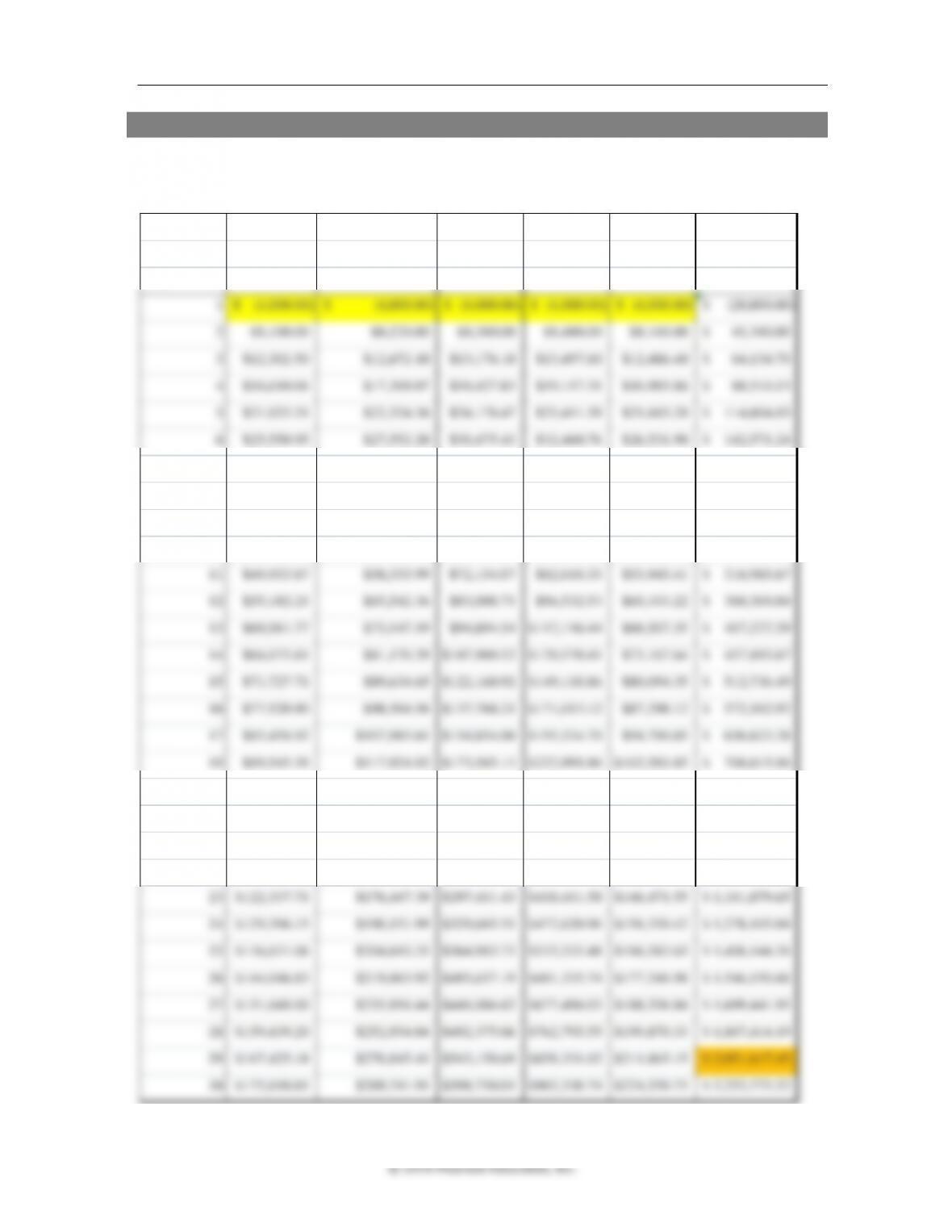

1. Future value with an annuity.

a. They will have accumulated $2,000,000 after approximately twenty-nine years.

Money market G overnment Bonds Large Cap Small Cap Real Estate Portfolio

G rowth rate 2.5% 5.5% 9.5% 12.0% 4.0%

Year

1 (4,000.00)$ (4,000.00)$ (4,000.00)$ (4,000.00)$ (4,000.00)$ (20,000.00)$

2 $8,100.00 $8,220.00 $8,380.00 $8,480.00 $8,160.00 41,340.00$

3 $12,302.50 $12,672.10 $13,176.10 $13,497.60 $12,486.40 64,134.70$

4 $16,610.06 $17,369.07 $18,427.83 $19,117.31 $16,985.86 88,510.13$

5 $21,025.31 $22,324.36 $24,178.47 $25,411.39 $21,665.29 114,604.83$

11 $49,933.87 $58,333.99 $72,154.07 $82,618.33 $53,945.41 316,985.67$

12 $55,182.21 $65,542.36 $83,008.71 $96,532.53 $60,103.22 360,369.04$

13 $60,561.77 $73,147.19 $94,894.54 $112,116.44 $66,507.35 407,227.29$

14 $66,075.81 $81,170.29 $107,909.52 $129,570.41 $73,167.64 457,893.67$

15 $71,727.71 $89,634.65 $122,160.92 $149,118.86 $80,094.35 512,736.49$

23 $122,337.71 $176,447.39 $297,411.43 $418,411.58 $146,471.55 1,161,079.65$

24 $129,396.15 $190,151.99 $329,665.51 $472,620.96 $156,330.42 1,278,165.04$

25 $136,631.06 $204,610.35 $364,983.73 $533,335.48 $166,583.63 1,406,144.26$

26 $144,046.83 $219,863.92 $403,657.19 $601,335.74 $177,246.98 1,546,150.66$

27 $151,648.00 $235,956.44 $446,004.62 $677,496.03 $188,336.86 1,699,441.95$

Chapter 4 ◼ The Time Value of Money (Part 2) 111

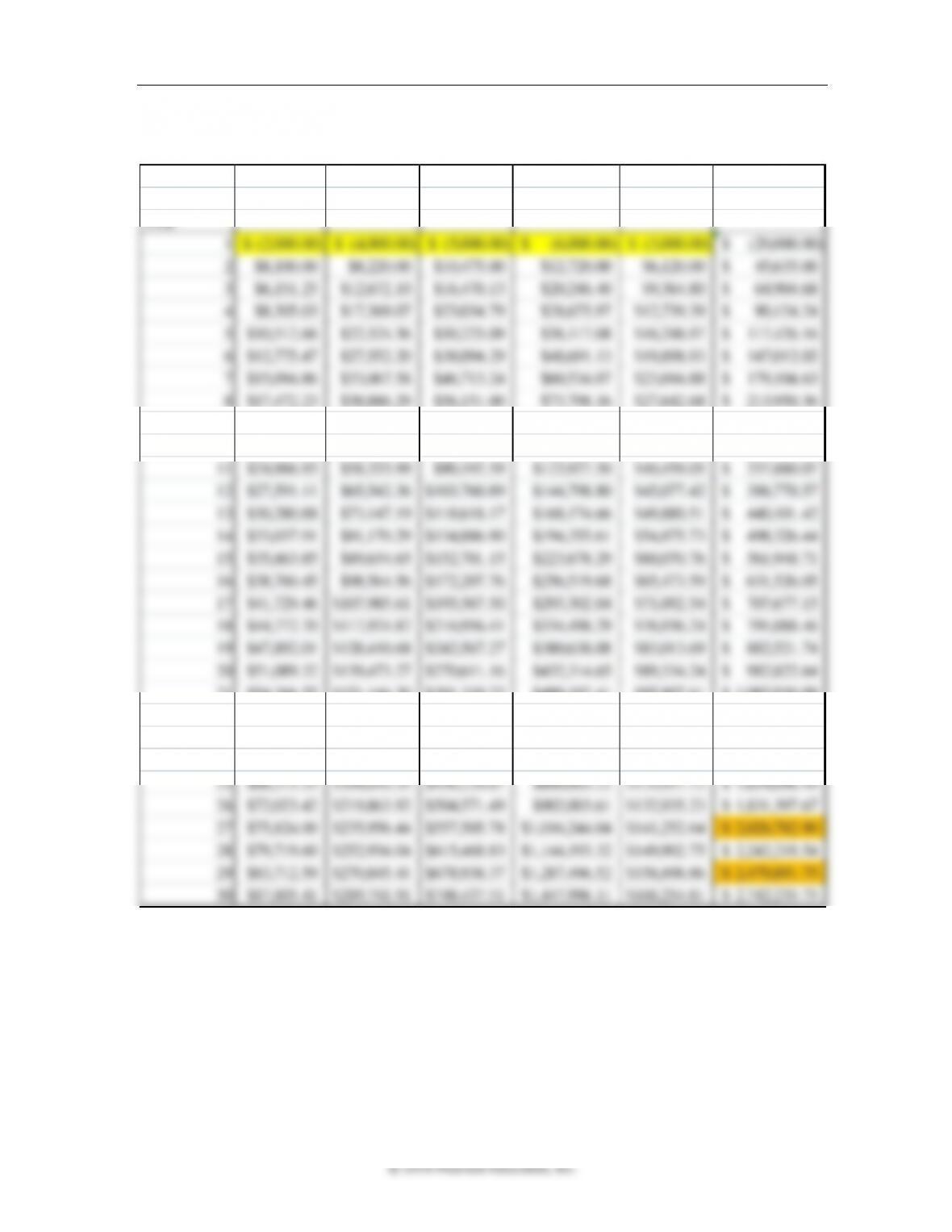

b. They will be able to retire two years earlier. If they retire after twenty-nine years, they

will have saved $428,274.30 more than the amount saved in Part (a)

Money Mkt. Gvt. Bonds Large Cap Small Cap Real Estate Portfolio

Growth Rate 2.5% 5.5% 9.5% 12.0% 4.0%

Year

1 (2,000.00)$ (4,000.00)$ (5,000.00)$ (6,000.00)$ (3,000.00)$ (20,000.00)$

2 $8,100.00 $8,220.00 $10,475.00 $12,720.00 $6,120.00 45,635.00$

3 $6,151.25 $12,672.10 $16,470.13 $20,246.40 $9,364.80 64,904.68$

4 $8,305.03 $17,369.07 $23,034.79 $28,675.97 $12,739.39 90,124.24$

5 $10,512.66 $22,324.36 $30,223.09 $38,117.08 $16,248.97 117,426.16$

6 $12,775.47 $27,552.20 $38,094.29 $48,691.13 $19,898.93 147,012.02$

7 $15,094.86 $33,067.58 $46,713.24 $60,534.07 $23,694.88 179,104.63$

8 $17,472.23 $38,886.29 $56,151.00 $73,798.16 $27,642.68 213,950.36$

9 $19,909.04 $45,025.04 $66,485.35 $88,653.94 $31,748.39 251,821.74$

10 $22,406.76 $51,501.42 $77,801.45 $105,292.41 $36,018.32 293,020.36$

11 $24,966.93 $58,333.99 $90,192.59 $123,927.50 $40,459.05 337,880.07$

12 $27,591.11 $65,542.36 $103,760.89 $144,798.80 $45,077.42 386,770.57$

13 $30,280.88 $73,147.19 $118,618.17 $168,174.66 $49,880.51 440,101.42$

14 $33,037.91 $81,170.29 $134,886.90 $194,355.61 $54,875.73 498,326.44$

15 $35,863.85 $89,634.65 $152,701.15 $223,678.29 $60,070.76 561,948.71$

23 $61,168.85 $176,447.39 $371,764.28 $627,617.36 $109,853.67 1,346,851.55$

24 $64,698.08 $190,151.99 $412,081.89 $708,931.45 $117,247.81 1,493,111.22$

25 $68,315.53 $204,610.35 $456,229.67 $800,003.22 $124,937.72 1,654,096.49$

Chapter 4 ◼ The Time Value of Money (Part 2) 113

Solutions to Mini-Case

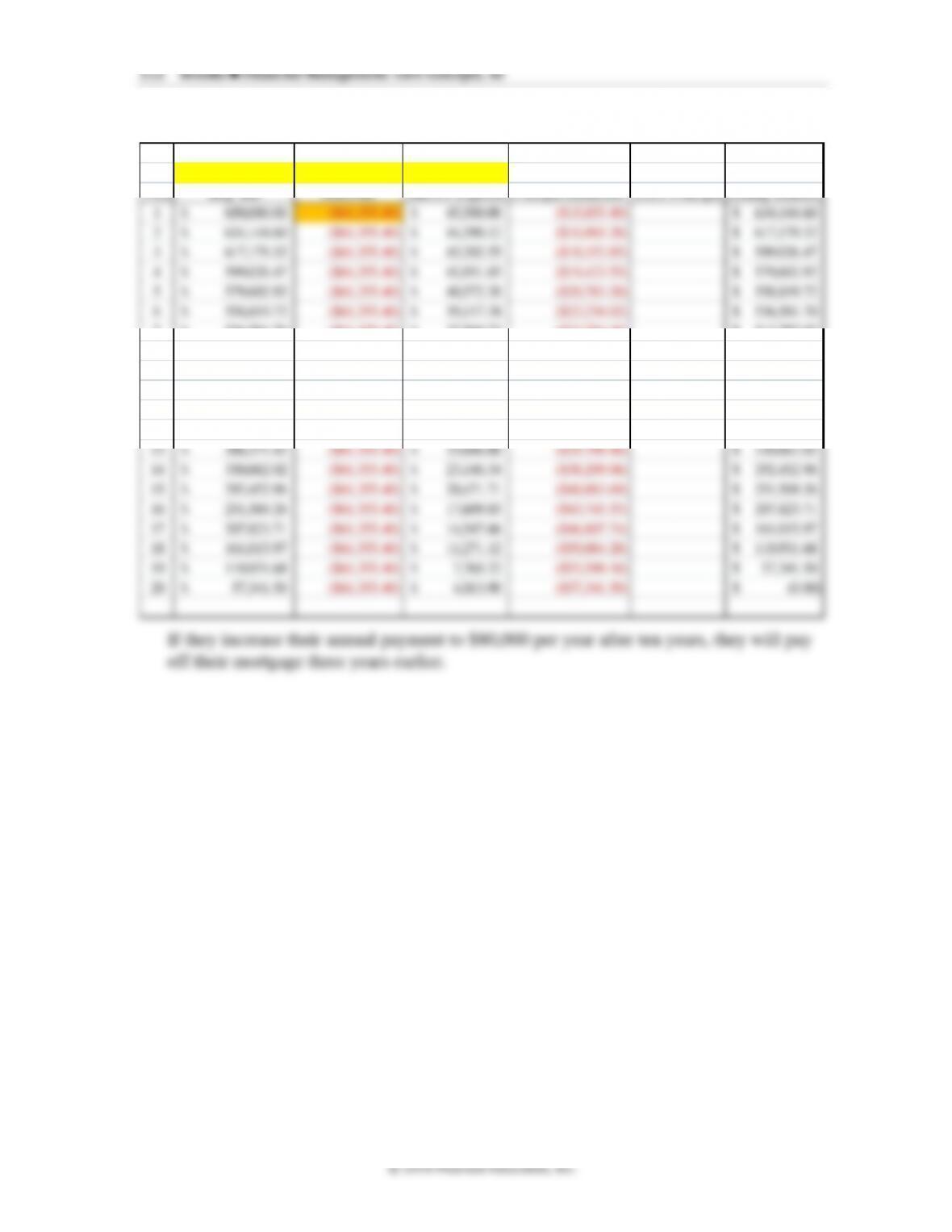

Fitchminster Injection Molding, Inc.: Rose Climbs High

This case illustrates the important role that present and future values of annuities play in

business decisions, and emphasizes the structuring of loan payments as an important

practical application of time value of money computations.

1. Rose could probably borrow the money to purchase the shares outright because

the shares would serve as collateral and dividends would cover a good part of the

loan payments. The interest rate is 7%, and the loan will be amortized with a

series of equal payments. What are the annual payments if the bank amortizes the

Loan Amount Interest Rate Years for Loan

650,000.00$ 7.00% 20

Year Beginning Balance Annual Payment Interest Expense Principal Reduction Extra Principal Ending Balance

1 650,000.00$ ($61,355.40) 45,500.00$ ($15,855.40) 634,144.60$

2 634,144.60$ ($61,355.40) 44,390.12$ ($16,965.28) 617,179.32$

3 617,179.32$ ($61,355.40) 43,202.55$ ($18,152.85) 599,026.47$

4 599,026.47$ ($61,355.40) 41,931.85$ ($19,423.55) 579,602.92$

5 579,602.92$ ($61,355.40) 40,572.20$ ($20,783.20) 558,819.72$

6 558,819.72$ ($61,355.40) 39,117.38$ ($22,238.02) 536,581.70$

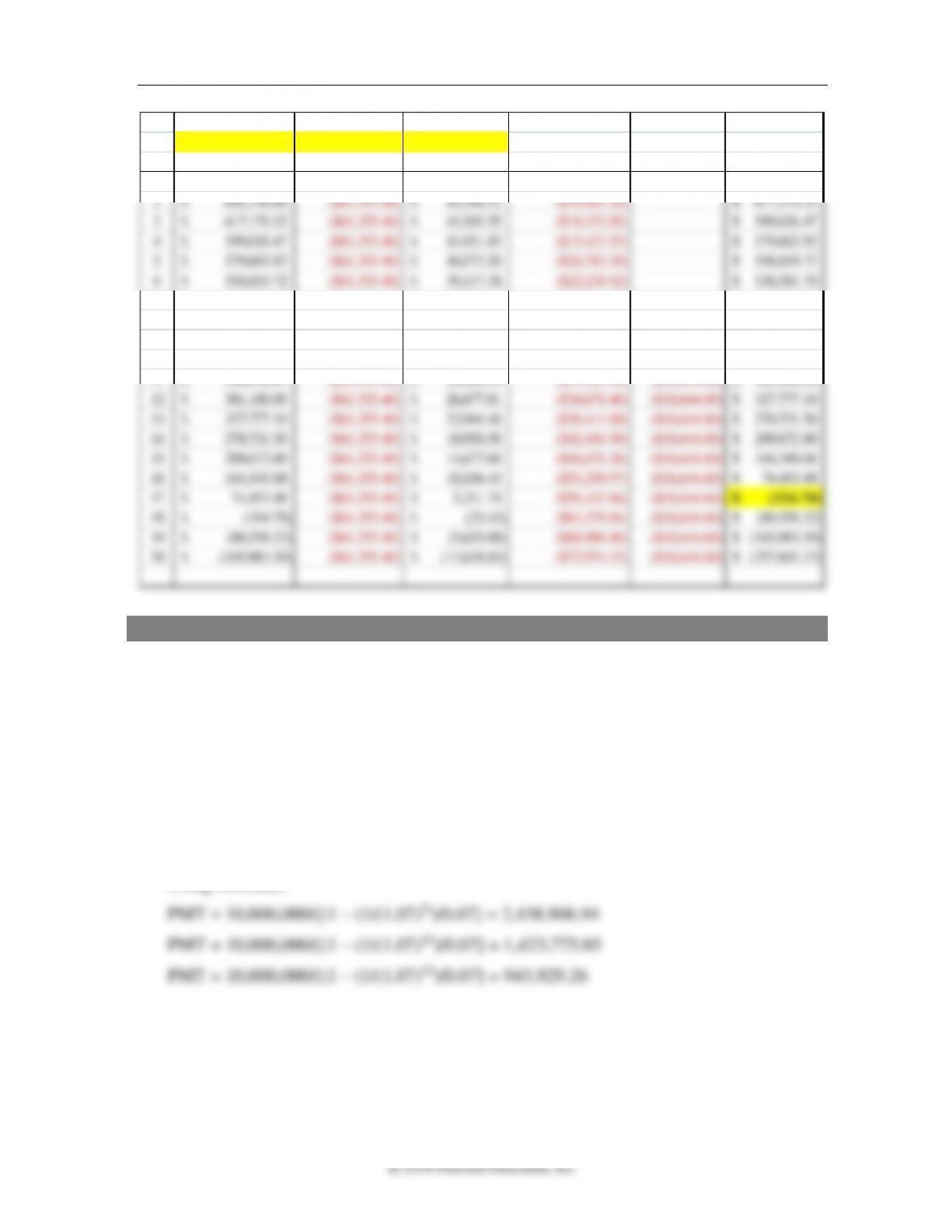

7 536,581.70$ ($61,355.40) 37,560.72$ ($23,794.68) 512,787.02$

8 512,787.02$ ($61,355.40) 35,895.09$ ($25,460.31) 487,326.71$

9 487,326.71$ ($61,355.40) 34,112.87$ ($27,242.53) 460,084.18$

10 460,084.18$ ($61,355.40) 32,205.89$ ($29,149.51) 430,934.67$

11 430,934.67$ ($61,355.40) 30,165.43$ ($31,189.98) ($18,644.60) 381,100.09$

12 381,100.09$ ($61,355.40) 26,677.01$ ($34,678.40) ($18,644.60) 327,777.10$

13 327,777.10$ ($61,355.40) 22,944.40$ ($38,411.00) ($18,644.60) 270,721.50$

14 270,721.50$ ($61,355.40) 18,950.50$ ($42,404.90) ($18,644.60) 209,672.00$

15 209,672.00$ ($61,355.40) 14,677.04$ ($46,678.36) ($18,644.60) 144,349.04$

16 144,349.04$ ($61,355.40) 10,104.43$ ($51,250.97) ($18,644.60) 74,453.48$

17 74,453.48$ ($61,355.40) 5,211.74$ ($56,143.66) ($18,644.60) (334.78)$

18 (334.78)$ ($61,355.40) (23.43)$ ($61,378.84) ($18,644.60) (80,358.22)$

19 (80,358.22)$ ($61,355.40) (5,625.08)$ ($66,980.48) ($18,644.60) (165,983.29)$

20 (165,983.29)$ ($61,355.40) (11,618.83)$ ($72,974.23) ($18,644.60) (257,602.12)$

114 Brooks ◼ Financial Management: Core Concepts, 4e

Calculator Solution

N

i/y

PV

PMT

FV

5

7

10,000,000

–2,438,906.94

0

10

7

10,000,000

–1,423,775.03

0

20

7

10,000,000

–943,929.26

0

2. Repeat Question 1, but assume that Rose makes payments at the beginning of each

year.

3. Complete the amortization schedule below for a $10,000,000 loan at 7% with five

equal end-of-year payments.

Year

Beginning

Principal

Annual

Payment

Interest

Expense

Principal

Reduction

Remaining

Principal

1

$10,000,000.00

$2,438,906.94

$ 700,000.00

$1,738,906.94

$ 8,261,093.06

2

$ 8,261,093.06

$2,438,906.94

$ 578,276.51

$1,860,630.43

$ 6,400,462.63

3

$ 6,400,462.63

$2,438,906.94

$ 448,032.38

$1,990,874.56

$ 4,409,588.06

4

$ 4,409,588.06

$2,438,906.94

$ 308,671.16

$2,130,235.78

$ 2,279,352.28

5

$ 2,279,352.28

$2,438,906.94

$ 159,554.66

$2,279,352.28

$

4. Sam has offered to finance the purchase with a ten-year, interest-only loan. How

much is Rose’s annual payment? Describe the pattern of payments over the ten

5. Assume that Rose accepts Sam’s offer to finance the purchase with a ten-year,

interest-only loan. If Sam can reinvest the interest payments at a rate of 7% per

year, how much money will he have at the end of the tenth year?

PMT

–9,671,513.57

Chapter 4 ◼ The Time Value of Money (Part 2) 115

Additional Problems with Solutions

1. Present value of an annuity due. Julie has just been accepted into Harvard, and her

father is debating whether he should make monthly lease payments of $5,000 at the

beginning of each month on her flashy apartment or to prepay the rent with a one-time

payment of $56, 662. If Julie’s father earns 1% per month on his savings, should he pay

by month or take the discount by making the single annual payment?

ANSWER (Slides 4-45 to 4-46)

Use the TVM Keys from a Texas Instrument BAII Plus Calculator and round to two

2. Future value of uneven cash flows. If Mary deposits $4,000 a year for three years,

starting a year from today, followed by three annual deposits of $5000, into an account

that earns 8% per year, how much money will she have accumulated in her account at

the end of ten years?

ANSWER (Slides 4-47 to 4-49)

116 Brooks ◼ Financial Management: Core Concepts, 4e

© 2018 Pearson Education, Inc.

ALTERNATIVE METHOD:

Using the Cash Flow (CF) key of the calculator, enter the respective cash flows.

That is, CF0 = 0; CF1 = –$4000; CF2 = –$4000; CF3 = –$4000; CF4 = –$5000;

CF5 = –$5000; CF6 = –$5000

Next calculate the NPV using I = 8%; ➔NPV = $20,537.30133;

Finally, using PV = –$20,537.30133; n = 10; I = 8%; PMT = 0; CPT FV➔$44,338

3. Present value of uneven cash flows. Jane Bryant has just purchased some equipment

for her beauty salon. She plans to pay the following amounts at the end of the next five

years: $8,250, $8,500, $8,750, $9,000, and $10,500. If she uses a discount rate of 10

percent, what is the cost of the equipment that she purchased today?

ANSWER (Slides 4-50 to 4-51)

2 3 4 5

$8, 250 $8,500 $8,750 $9,000 $10,500

PV (1.10) (1.10) (1.10) (1.10) (1.10)

$7,500 $7,024.79 $6,574 $6,147.12 $6,519.67

$33,765.58

= + + + +

= + + + +

=

4. Computing annuity payment. The Corner Bar & Grill is in the process of taking a five-

year loan of $50,000 with First Community Bank.

The bank offers the restaurant owner his choice of three payment options:

1) Pay all of the interest (8% per year) and principal in one lump sum at the end of five

years;

2) Pay interest at the rate of 8% per year for four years and then a final payment of

interest and principal at the end of the fifth year;

3) Pay five equal payments at the end of each year inclusive of interest and part of the

principal.

Under which of the three options will the owner pay the least interest and why? Hint:

Calculate the total amount of the payments and the amount of interest paid under each

alternative.

ANSWER (Slides 4-52 to 4-56)

Chapter 4 ◼ The Time Value of Money (Part 2) 117

Under option 2: Interest-only loan