46

Chapter 3

The Time Value of Money (Part 1)

LEARNING OBJECTIVES (Slides 3-1 to 3-2)

1. Calculate future values and understand compounding.

2. Calculate present values and understand discounting.

3. Calculate implied interest rates and waiting time from the time value of money

equation.

4. Apply the time value of money equation using an equation, calculator, and

spreadsheet.

5. Explain the Rule of 72, a simple estimation of doubling values.

IN A NUTSHELL….

This chapter is the first in a two-part unit on the time value of money. It provides an

introduction to financial mathematics, a sound understanding of which is imperative for a

student to do well in the later, more complex topics of corporate finance. The students

should be well grounded in measuring future values, present values, interest rates, and

number of periods necessary to achieve various cash flow streams.

The author covers the compounding and discounting techniques associated with single

cash outflows and inflows over a single period of time, such as a year, as well as over

multiple periods of time. He shows how time value problems associated with single cash

flow streams are a function of four variables, i.e., the present value (PV), future value

LECTURE OUTLINE

3.1 Future Value and Compounding Interest (Slides 3-3 to 3-11)

When a sum of money is invested into an account that pays a rate of interest for the

period during which the money is invested, the value of money at the end of the stated

period is called the future or compound value of that sum of money. This type of

calculation is done when determining the attractiveness of alternative investments or

Chapter 3 ◼ The Time Value of Money (Part 1) 47

when one is trying to figure out the effect of inflation on the future cost of assets such as

a car or a house. In the latter case, we use the expected annual inflation rate instead of the

rate of interest in order to calculate the future cost of the asset.

The Single-Period Scenario: In problems involving a single period such as one year, the

future value of a sum of money would equal the original sum plus the amount of interest

earned over that period.

FV = PV + PV × interest rate or FV = PV(1 + interest rate (in decimals)

Example 1

Let’s say John deposits $200 for a year in an account that pays 6% per year. At the end of

The Multiple-Period Scenario: If the amount of money is left in the account for multiple

periods such as 2 years or more, then the future value of a sum of money would be equal

to the original sum plus interest over the multiple periods involved plus interest earned on

the interest as well.

FV = PV × (1 + i)n

Example 2

If John closes out his account after 3 years, how much money will he have accumulated?

How much of that is the interest on interest component? What about after 10 years?

Methods of Solving Future Value Problems include the use of a formula, a financial

calculator, a spreadsheet program such as Excel, and the use of time value tables.

Method 1: The equation is the most time-consuming, although the least dependent

method that one can use. It requires a thorough understanding of the relevant

mathematical functions. To calculate the future or compound value (FV) of a sum of

money, the following formula would apply

FV = PV × (1 + i)n

where: PV = present value of the lump sum; i = the periodic rate of interest; and n = the

number of periods for which interest is to be compounded.

48 Brooks ◼ Financial Management: Core Concepts, 4e

Method 2: The TVM keys is quick and easy since all that has to be done is to enter the

values for the present value (PV), interest rate (I/Y), number of periods (N), and annuity

involved (PMT), and then solve for the future value (FV). It is important to let students

know that the PV should be entered as a negative (since it is an outflow) and that PMT

should be set to 0. Also, interest rates are to be entered in percent form, i.e., 12.13 for

12.13%, and not in decimal form.

Method 3: The spreadsheet like the calculator method, is also very quick and easy but is

even more versatile because it can be used to perform sensitivity analyses by varying the

input values, and allows for quick review of all the inputs used. Students should be

Example 3: Compounding of interest

Let’s say you want to know how much money will have accumulated into your bank

account after 4 years, if you deposit all $5,000 of your graduation gifts into the account

which pays a fixed interest rate of 5% per year, and leave it there untouched for all four

of your college years….

Formula Method:

The formula for solving this problem is as follows:

Future Value = Present Value × (1 + r)n

or

FV = PV × (1 + r)n;

Note that the total amount of interest earned over the four year period = $1077.53, and

can be broken down as follows:

Year 1: 5% × $5,000.00 = $250.00

Calculator Method:

PV = –5,000; n = 4; I = 5; PMT = 0; CPT FV = $6077.53

Spreadsheet method:

Rate = 0.05; Nper = 4; Pmt = 0; PV = –5,000; Type = 0; FV = 6077.31

Time value table method:

Chapter 3 ◼ The Time Value of Money (Part 1) 49

Example 4: Future cost due to inflation

Let’s say that you have seen your dream house which is currently listed at $300,000, but

unfortunately, you are not in a position to buy it right away and will have to wait at least

another five years before you will be able to afford it. If house values are appreciating at

the average annual rate of inflation of say 5%, how much will a similar house cost after

five years?

In this case, PV = current cost of the house = $300,000; n = 5 years; I = average annual

So the house will cost $382,884.5 after 5 years

Calculator method:

3.2 Present Value and Discounting (Slides 3-12 to 3-19)

Calculating the present value (PV) of a single sum of money that will be received after a

number of periods involves discounting the amount of interest that would have been

earned over that period at a given rate of interest. It is therefore the exact opposite or

inverse of calculating the future value of a sum of money. Such calculations are useful for

determining today’s price or value of an asset or cash flow that will be received in the

future. The formula used for determining PV is as follows:

( )

=

+

1

PV FV 1n

r

where, the term in brackets is the present value interest factor for the relevant rate of

interest and number of periods involved, and is the reciprocal of the future value interest

factor (FVIF) or (1 + r)n.

50 Brooks ◼ Financial Management: Core Concepts, 4e

Example 5: Discounting interest

Let’s say you just won a jackpot of $50,000 at the casino and would like to save a portion

of it so as to have $40,000 to put down on a house after five years. Your bank pays a 6%

rate of interest. How much money will you have to set aside from the jackpot winnings?

Here, the future value (FV) is $40,000, i.e., the down payment needed, and since n = 5

and i = 6%; we can solve for the present value of savings (PV) necessary by using the

following formula:

( )

=

+

1

PV FV 1n

r

( )

=

5

1

PV $40,000 1.06

PV = $40,000 × 0.747258

PV = $29,890.32

Note that $28,090.33 × (1.06)(1.06)(1.06)(1.06)(1,06) = $40,000

Thus, we have to discount interest of $10,110.67 off the FV of $40,000 to calculate the

PV or amount of saving needed.

Calculator method:

Spreadsheet method:

52 Brooks ◼ Financial Management: Core Concepts, 4e

Example 7: Solving for the number of periods involved

Let’s say that Jim realizes that a rate of return of 31.607% per year is pretty high and

lowers his sights by settling for an investment that will pay 12% per year. If he still hopes

to triple his money, for how many years will he have to keep the $5,000 worth of

graduation gifts invested?

PV = $5,000; FV = $15,000; I = 12%; n = ?

The appropriate equation to use is as follows:

( )

=+

FV

ln PV

nln 1 r

3.4 Applications of the

Time Value of Money Equation (Slides 3-21 to 3-37)

In this section, the author presents various real-life applications of the time-value-of–

3.5 Doubling of Money: The Rule of 72 (Slide 3-38)

Prior to the time when calculators were developed, the Rule of 72 was used to estimate

the number of years required to double a sum of money at a given rate of interest.

Basically, by dividing the rate of interest into 72, a fairly good estimate of the period

Chapter 3 ◼ The Time Value of Money (Part 1) 53

Questions

1. What are the four basic parts (variables) of the time-value of money equation?

2. What does the term compounding mean?

3. Define a growth rate and a discount rate. What is the difference between them?

A growth rate is the annual percentage increase, and the discount rate is the annual

4. What happens to a future value as you increase the interest (growth) rate?

5. What happens to a present value as you increase the discount rate?

6. What happens to a future value as you increase the time to the future date?

7. What happens to the present value as the time to the future value increases?

8. What is the Rule of 72?

9. Is the present value always less than the future value?

Yes, as long as interest rates are positive—and interest rates are always positive—the

10. When a lottery price is offered as $10,000,000 but will pay out a series of

$250,000 payments over forty years, is it really a $10,000,000 lottery prize?

The present value of the lottery is not worth $10,000,000. The total payments over

54 Brooks ◼ Financial Management: Core Concepts, 4e

Prepping for Exams

1. d.

6. c.

2. b.

7. d.

3. c.

8. b.

4. c.

9. a.

5. a.

10. b.

Problems

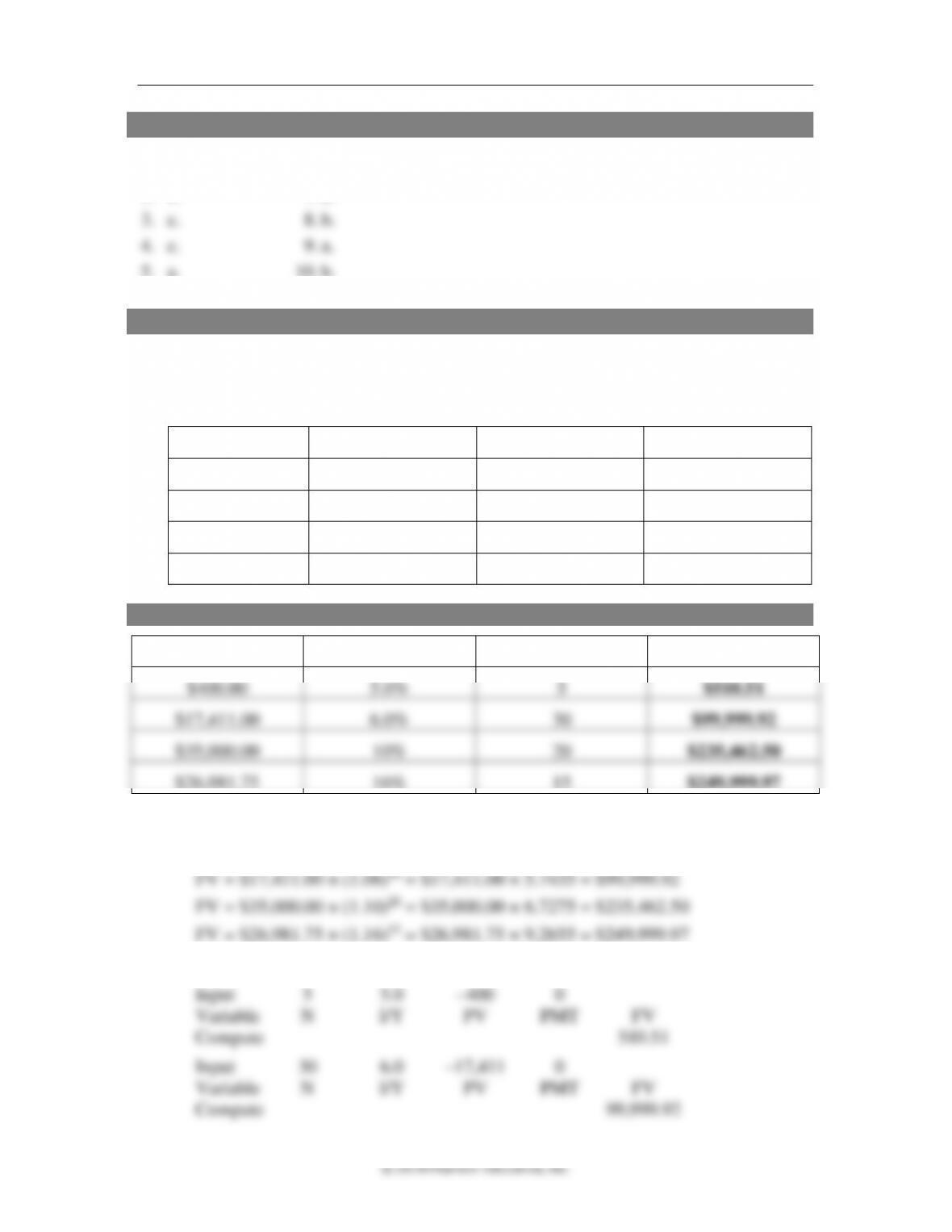

1. Future Values. Fill in the future values for the following table

a. Using the future value formula, FV = PV × (1 + r)n.

b. Using the time value of money keys or function from a calculator or spreadsheet.

Present Value

Interest Rate

Number of Periods

Future Value

$400.00

5.0%

5

$17,411.00

6.0%

30

$35,000.00

10%

20

$26,981.75

16%

15

ANSWER

Present Value

Interest Rate

Number of Periods

Future Value

$400.00

5.0%

5

$510.51

$17,411.00

6.0%

30

$99,999.92

$35,000.00

10%

20

$235,462.50

$26,981.75

16%

15

$249,999.97

a. With TVM formula (rounding to second decimal only for final answer)

FV = $400.00 × (1.05)5 = $400.00 × 1.2763 = $510.51

b. Time Value of Money Keys or Spreadsheet

© 2018 Pearson Education, Inc.

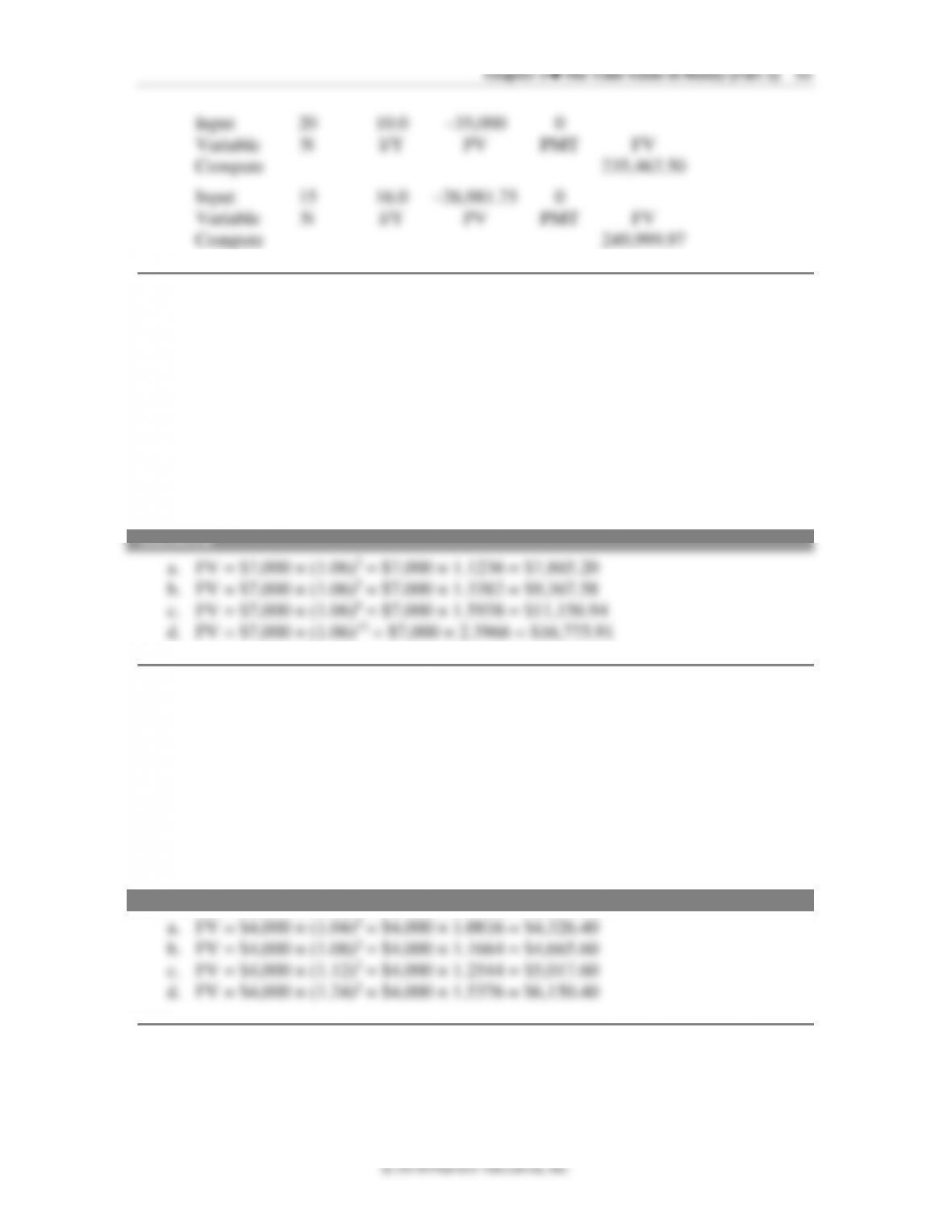

2. Future Value (with changing years). Dixie Bank offers a certificate of deposit with

an option to select your own investment period. Jonathan has $7,000 for his CD

investment. If the bank is offering a 6% interest rate, how much will the CD be worth

at maturity if Jonathan picks a

a. two-year investment period?

b. five-year investment period?

c. eight-year investment period?

d. fifteen-year investment period?

3. Future Value (with changing interest rates). Jose has $4,000 to invest for a two-year

period. He is looking at four different investment choices. What will be the value of

his investment at the end of two years for each of the following potential

investments?

a. bank CD at 4%.

b. bond fund at 8%.

c. mutual stock fund at 12%.

d. new venture stock at 24%.

ANSWER