13

Chapter 2

Financial Statements

LEARNING OBJECTIVES (Slide 2-2)

1. Explain the foundations of the balance sheet and income statement.

2. Use the cash flow identity to explain cash flow.

3. Provide some context for financial reporting.

4. Recognize and view Internet sites that provide financial information.

IN A NUTSHELL….

Although many business students find accounting to be rather boring and dry as a subject,

it is important to remind them that accounting is the official “language” of finance. It

provides managers and business owners with vital information via financial statements,

which can be used to assess the current health of the business, figure out where it has

been, how it is doing, and chalk up a planned route for its future performance.

In this chapter, we review the basic financial statements: the income statement, the

balance sheet, and the cash flow statement. However, unlike a formal course in

accounting, which trains students to actually prepare financial statements, the material in

this chapter mainly helps students read financial statements and understand how they are

linked together in calculating the cash flow of a company.

The value of a firm depends on the present value of its future cash flows. Thus, it is

imperative that students learn how to estimate the cash flows of a firm. Accounting

income that is reported in financial statements is typically not the same as the cash flow

of a firm because most firms use accrual accounting principles for recording revenues

and expenditures. Under accrual accounting, firms may recognize revenues at the time of

sale, even if cash is received at a later date. Similarly, the expenses recorded over a

period may not be the same as the actual payments made because firms are billed in units

of calendar time, i.e., monthly or quarterly, while the actual usage and payment may

follow a different pattern. As a result, accounting statements do not accurately reflect the

actual cash inflows and outflows that have occurred over a period of time. The cash

balance shown on the balance sheet is a true reflection of the cash available to a firm, and

the change in cash balance points out the net result of the cash receipts and payments that

14 Brooks ◼ Financial Management: Core Concepts, 4e

have occurred. Thus, by preparing a statement of cash flows, a manager can track the

sources and uses of cash from the operations, investment, and financing activities of the

firm and understand what has caused the cash balance to change from the prior period.

necessary to examine the performance of a firm.

LECTURE OUTLINE (Slide 2-3)

2.1 Financial Statements

The focus of the discussion in this section should be on the interrelationships among the

four financial statements— the income statement, the balance sheet, the statement of

retained earnings, and the statement of cash flow—and on the process by which these

end of the Lecture Outline.

The Balance Sheet: a firm’s current and fixed assets are listed, as well as the liabilities

and owner’s equity accounts that were used to finance those assets. Thus, the total assets

figure has to equal the sum of total liabilities and owner’s equity of a firm. J.F. & Sons’

balance sheet for the recent two years is shown below, along with the annual changes in

each account item.

(Slides 2-4 to 2-7)

J.F. & Sons’ Balance Sheet at the end of This Year and Last Year

Assets

This Year

Last Year

Change

Cash

318,000

1,000,000

–682,000

Accounts Receivable

180,000

180,000

Inventory

50,000

50,000

Total Current Assets

548,000

1,000,000

452,000

0

Gross Plant and Equipment

200,000

200,000

Land and Buildings

400,000

400,000

Truck

25,000

25,000

Less accumulated Dep.

–125,000

125,000

Chapter 2 ◼ Financial Statements 15

Net Fixed Assets

500,000

500,000

0

TOTAL ASSETS

1,048,000

1,000,000

48,000

Liabilities & Owner’s Equity

Accounts payable

100,000

0

100,000

Accruals

0

Deferrals

0

Total Current Liabilities

100,000

0

100,000

Bank Debt

500,000

500,000

Capital

500,000

500,000

Retained Earnings

–52,000

–52,000

Owner’s Equity

448,000

500,000

–52,000

0

TOTAL LIABILITIES & OWNER’S

EQUITY

1,048,000

1,000,000

48,000

The Balance Sheet has five sections:

• Cash account, which shows a decline of $682,000. An analysis of the Statement

of Cash Flows will help determine why.

• Working capital accounts, which show the current assets and current liabilities

that directly, support the operations of the firm. The difference between current

assets (CA) and current liabilities (CL) is a measure of the net working capital

(NWC) or absolute liquidity of a firm. For J.F. & Sons;

• Long-term capital assets accounts, which show the gross and net book values of

the long-term assets that the firm has invested into since its inception. The

accumulated depreciation figure shows how much of the original value of the

assets has already been expensed as depreciation.

16 Brooks ◼ Financial Management: Core Concepts, 4e

• Long-term liabilities (debt) accounts, which include all the outstanding loans that

the firm has taken on for periods greater than one year. As part of the loan is paid

• Ownership Accounts include the capital contributed by the owners (common stock

account) and the retained earnings of the firm since its inception. The sum of both

these components is known as owner’s equity or stockholders’ equity on the

Note: It is important to stress the point to students that the retained earnings figure

is an accumulated total of the undistributed earnings of a company since its

inception and that it is not cash available for future expenses or investment, since it

has already been used in the business

The Income Statement: shows the expenses and income generated by a firm over a past

period, typically over a quarter or a year. It can be thought of as a video recording of

expenses and revenues. Revenues are listed first, followed by cost of goods sold,

depreciation, and other operating expenses to calculate Earnings before Interest and

(Slides 2-8 to 2-10)

J. F. & Sons’ Annual Income Statement

Revenues

300,000

Cost of Goods Sold

150,000

Wages

20,000

Utilities

5,000

Other Expenses

2,000

Earnings Before Depreciation, Interest, Taxes

123,000

less Depreciation

125,000

Earnings Before Interest & Taxes

–2,000

less Interest

50,000

Earnings Before Taxes

–52,000

Taxes

0

Net Income (Loss)

–52,000

Chapter 2 ◼ Financial Statements 17

J.F. & Sons had earned an operating income of –$2,000 during their first year and after

accounting for interest they would show a loss of $52,000; thus, no taxes would be paid.

Now, the net loss of $52,000 is not the same as their change in cash balance (– 682,000)

because of three reasons: accrual accounting, non-cash expense items, and interest being

treated as a financing rather than an operating expense item.

• Issue 1: Generally accepted accounting principles (GAAP). Based on GAAP,

firms typically recognize revenues at the time of sale, even if cash is not received

in the same accounting period. Similarly, firms are billed for expenses that may

correspond to a later period. This is known as accrual-based accounting. Thus,

the yearly net income figure could be different from the change in cash balance

• Issue 2: Non-cash expense items. Some expenses shown on the income

statement (e.g., depreciation of $125,000) are actually annual charges (20%)

being shown based on the initial year expense of $625,000 for acquiring the truck,

the plant and equipment, and the land and buildings.

J.F. & Sons’ Cash Account details for the year ended December 31, 20XX

Debit

Credit

Owner’s Capital

500,000

Plant & Equipment

200,000

Bank Loan

500,000

Land & Bldg

400,000

Revenues

120,000

Inventory

100,000

Truck

25,000

Wages

20,000

Utilities

5,000

Other Expenses

2,000

Interest Expense

50,000

Ending Balance

318,000

• Issue 3: Classifying interest expense as part of the financing decision. In

finance, there is a preference to separate operating decisions (investment-related)

from financing decisions. Thus, interest expense is not deducted as part of

operating cash flow.

Thus, we can calculate J.F. & Sons’ operating cash flow (OCF) by adding back

depreciation and interest expense to its net income, i.e.,

Thus, although the firm is showing a negative net income (loss) of – $52,000 its cash

flow from operations of $123,000 is positive and considerably higher.

Statement of Retained Earnings is considered to be the fourth financial statement that

firms prepare and report. It shows how the net income for the past period was allocated

between dividends (if any) and retained earnings. For J.F. & Sons, the net loss of $52,000

Chapter 2 ◼ Financial Statements 19

Net New Borrowing = Ending Long-term Liabilities – Beginning Long-term

Liabilities

For J.F. & Sons,

Operating Cash Flow = – $2000 + $125,000 – 0 = $123,000

Net Capital Spending = $500,000 – 0 + $125,000 = $625,000

Change in Net Working Capital = $448,000 – $1,000,000 = – 552,000

were any dividends paid)

Hence, the cash flow identity holds,

i.e., Cash Flow from Assets = $50,000 = Cash Flow to Creditors and Owners

The Statement of Cash Flows, or the Sources and Uses of Cash Statement, as it is often

called, is compiled by taking information from the Income Statement and the Balance

Sheet and organizing it into three sections: cash flow from operating activities, cash flow

from investment activities, and cash flow from financing activities, so as to reflect the

change in the ending cash balance of the firm during that reporting period (quarter or

year). So the three sections of the cash flow identity explained above are related to the

three sections of the statement of cash flows in the following manner:

Note: Remind students that based on the accounting identity and double-entry

accounting principles explained earlier, an increase in an asset (except cash) would

result in a use of cash, while a decrease (sale) of an asset would result in a source of

cash. Similarly, an increase in a liability or owners’ equity would bring in cash while

a decrease would take away cash.

20 Brooks ◼ Financial Management: Core Concepts, 4e

J. F. & Sons’ Statement of Cash Flow

Operating Cash Flow

EBIT

–2,000

Depreciation

125,000

Increase in Inventory (Use)

–50,000

Increase in Accounts Receivable (Use)

–180,000

Increase in Accounts Payable (Source)

100,000

Cash Flow from Operating Activities

–7,000

Investment Cash

Flow

Invested in Plant & Equipment (Use)

–200,000

Invested in a Truck (Use)

–25,000

Land & Buildings (Use)

–400,000

Cash Flow from Investment Activities

–625,000

Financing Cash Flow

Interest Paid

–50,000

Cash flow from financing activities

–50,000

Net Sources (Uses) or Change in Cash Account

–682,000

Beginning Cash Balance

1,000,000

Net Cash Flow during current year

–682,000

Ending Cash Balance

318,000

Chapter 2 ◼ Financial Statements 21

Cash flow from operating activities would include the firm’s operating cash flow

calculated as follows:

Operating Cash Flow (OCF) = EBIT + Depreciation – Taxes as well as the changes in

the current assets (except cash) and current liabilities of the firm for that reporting period.

Cash flow from investing activities includes the cash used/generated in

purchasing/disposing fixed assets and other investments. For J.F. & Sons, given that this

has been its first year of operations, a fairly large use of cash ($625,000) has resulted

from the purchase of its plant, equipment, land, buildings, and a delivery truck.

Note: Since we have already added back depreciation for the year ($125,000) as part

of the sources of funds from operations, we account for the change in gross value of

Cash flow from financing activities includes the payment of interest, dividends,

reduction of the principal balance on debt, repurchase of stock, floating of new issues of

stock and/or bonds and increase/decrease in treasury stock. For J.F. & Sons, this past

year, the only cash flow from financing in the payment of interest of $50,000 on its

outstanding loan.

Free Cash Flow is another term used in conjunction with the cash flow from assets of a

firm. It refers to the cash available to pay the creditors and owners once the firm has

made the investments in working capital and capital assets necessary for continuing and

growing the business. The timing and amount of free cash flow generated by a firm is

critical to its valuation.

2.3 Financial Performance Reporting (Slide 2-22)

Publicly traded companies provide current and potential shareholders financial

performance information, company highlights, and management perspectives by

compiling annual reports. In addition, they are required to file quarterly (10-Q) and

Chapter 2 ◼ Financial Statements 23

A Comprehensive Example to show how the three

statements are prepared from the ledger entries

Let’s say that J.F. & Sons decide to start a business by contributing $500,000 of their

own money and borrowing $500,000 from a bank (10-year note) at the rate of

10%, per year. It is the last week in December.

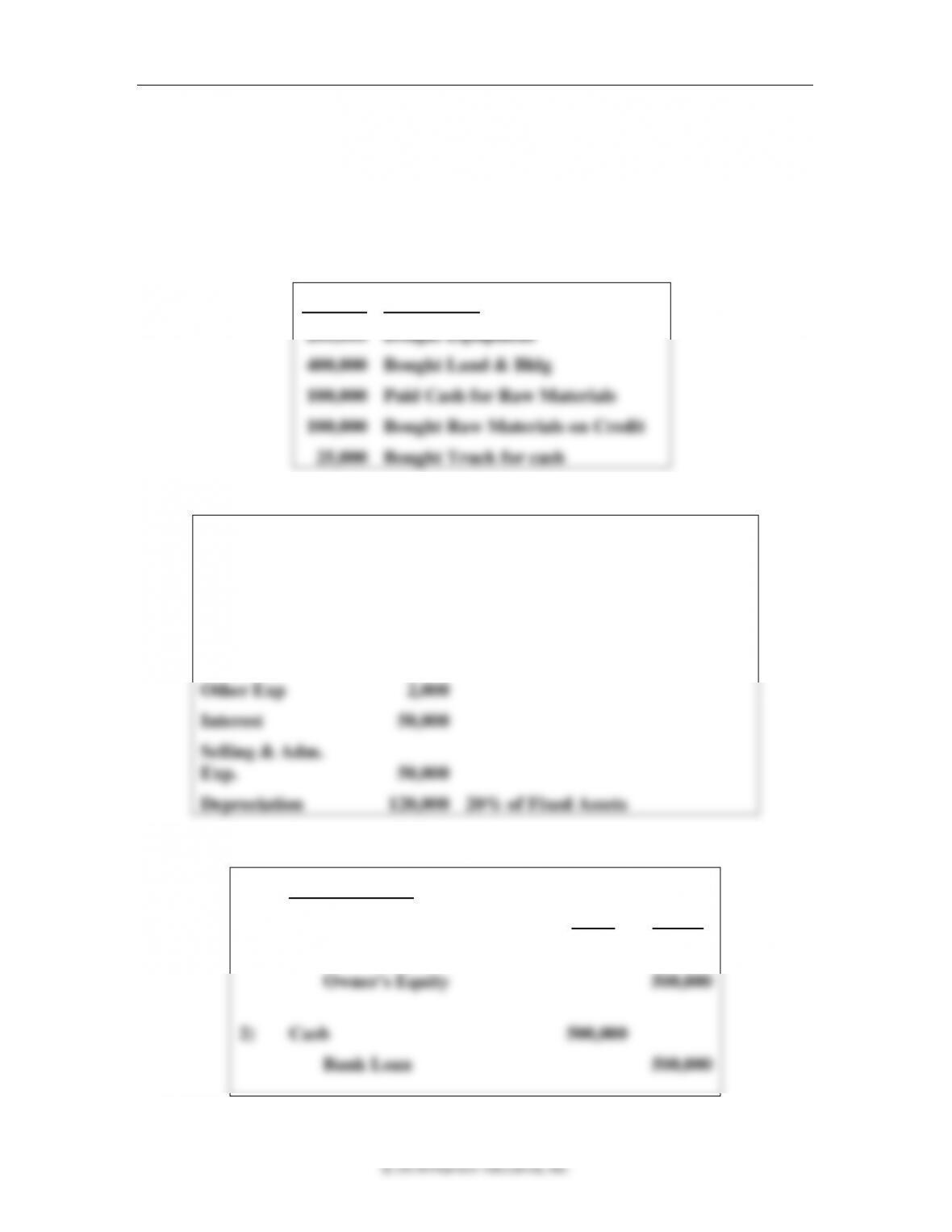

During the first quarter of the following year, they complete the following transactions:

Amount

Transaction

200,000

Bought Equipment

400,000

Bought Land & Bldg

100,000

Paid Cash for Raw Materials

100,000

Bought Raw Materials on Credit

25,000

Bought Truck for cash

By the end of the year, they have made the following transactions as well…

First Year transactions

Sales

300,000

[40% (Cash); 60% (Credit)]

CGS

150,000

Assume 50% of Sales

Wages

20,000

Utilities

5,000

Other Exp

2,000

Interest

50,000

Selling & Adm.

Exp.

50,000

Depreciation

120,000

20% of Fixed Assets

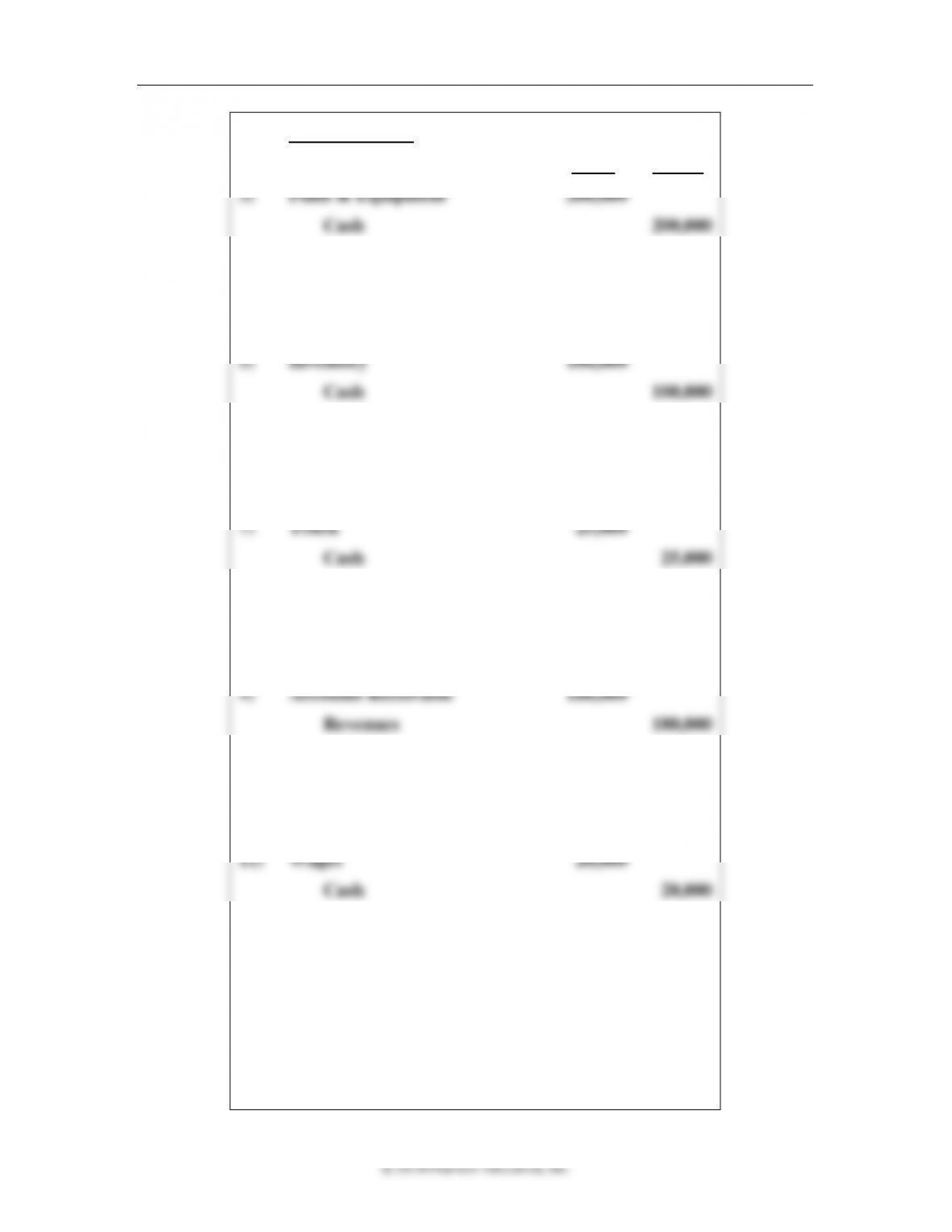

Let’s start by preparing the journal entries:

Journal Entries

Debit

Credit

1)

Cash

500,000

Owner’s Equity

500,000

2)

Cash

500,000

Bank Loan

500,000

24 Brooks ◼ Financial Management: Core Concepts, 4e

Journal Entries

Debit

Credit

3)

Plant & Equipment

200,000

Cash

200,000

4)

Land & Bldg

400,000

Cash

400,000

5)

Inventory

100,000

Cash

100,000

6)

Inventory

100,000

Accounts Payable

100,000

7)

Truck

25,000

Cash

25,000

8)

Cash

120,000

Revenues

120,000

9)

Accounts Receivable

180,000

Revenues

180,000

10)

Cost of Goods Sold

150,000

Inventory

150,000

11)

Wages

20,000

Cash

20,000

12)

Utilities

5,000

Cash

5,000

13)

Other Exp.

2,000

Cash

2,000

Chapter 2 ◼ Financial Statements 25

Journal Entries

Debit

Credit

14)

Interest Exp.

50,000

Cash

50,000

15)

Selling & Adm. Exp.

50,000

Cash

50,000

16)

Depreciation

120,000

Accumulated Dep.

120,000

Now, keeping in mind the accounting identity

i.e., cash flow generated from the investment in assets is paid back to creditors and the

owners; we can prepare the Income Statement, the Balance Sheet, and the Statement of

Cash Flows for the year.

Questions

1. In what type of accounting system must debits always equal credits? What is the

accounting identity? What is the connection between “debits always equal

credits” and the accounting identity?

Debits must always equal credits in a double-entry bookkeeping (accounting) system.

2. What is the difference between a current asset and a long-term asset? What is

the difference between a current liability and a long-term liability? What is the

difference between a debtor’s claim and an owner’s claim?

A current asset is cash or items such as accounts receivable and inventory that would

26 Brooks ◼ Financial Management: Core Concepts, 4e

© 2018 Pearson Education, Inc.

paid off in future business cycles or years. A debtor’s claim is a liability and has a

fixed dollar amount to the claim. An owner’s claim is a residual claim, and this claim

is for all the remaining value of the company once the debtors are satisfied.

3. Why is the term residual claimant applied to a shareholder (owner) of a

business?

The term “residual claimant” is applied to a shareholder because the value of their

claim is what is left over from the company assets once the creditors’ claims have

4. What is the difference between net income and operating cash flow?

To arrive at net income, companies record non-cash expense items and record revenue

5. What is the purpose of the statement of retained earnings?

6. Why do financial notes accompany the annual report? Give an example of a

financial note from an annual report. (Look up the annual report of a company

on its website and read its financial notes.)

Notes to the financial statements help explain many of the details necessary to gain a

7. What are the three components of the cash flow from assets?

8. What does an increase in net working capital mean with regard to cash flow?

9. How does a company return money to debt lenders? How do you determine how

much was returned over the past year?

Companies return money to debt lenders by paying the interest (cost of the borrowed

28 Brooks ◼ Financial Management: Core Concepts, 4e

ANSWER

a. The Balance Sheets for the two years are:

Assets: 2016 2017

Current Assets

Cash $1,300 $1,090

Accounts Receivable $2,480 $2,690

Long-Term Assets:

Plant, Prop. & Equip $8,400 $9,200

Liabilities

Current Liabilities

Accounts Payable $1,800 $2,060

Long-Term Liabilities

Owner’s Equity

Common Stock $4,990 $4,990

b. The Working Capital Accounts are Cash, Accounts Receivable, Inventory, and

Accounts Payable.

c. The Net Working Capital for 2016 and 2017:

Net Working Capital = Cash + Accounts Receivable + Inventory – Accounts

Payable