544

Chapter 17

Dividends, Dividend Policy, and Stock

Splits

LEARNING OBJECTIVES (Slide 17-2)

1. Understand the formal process for paying dividends and differentiate between the most

common types.

2. Explain individual preferences and issues surrounding different dividend policies.

3. Explain how a company selects its dividend policy.

4. Understand stock splits and reverse splits and why companies use them.

5. Understand stock repurchases and dividend reinvestment programs.

IN A NUTSHELL…

Firms have varying policies regarding the payment of cash and stock dividends to their common

stock holders. Some firms do not pay dividends at all, while others pay a constant rate of

dividends. In this chapter, the author explains the mechanics of paying dividends and

differentiates between the different types of dividends. He tries to identify the issues that

surround the different dividend policies that firms adopt and to understand the rationale behind

LECTURE OUTLINE

17.1 Cash Dividends (Slides 17-3 to 17-9)

Many firms pay cash dividends on a regular basis. The payments of these dividends do correlate

with economic times, as anything else, and in recessionary times firms may cease to pay

dividends or cut back on the amount they pay per share.

Buying and selling stock is typically done via stock brokers on organized stock exchanges like

the NYSE or through dealers in the over-the-counter market like the NASDAQ.

Declaring and Paying a Cash Dividend: A Chronology

Chapter 17 ◼ Dividends, Dividend Policy, and Stock Splits 545

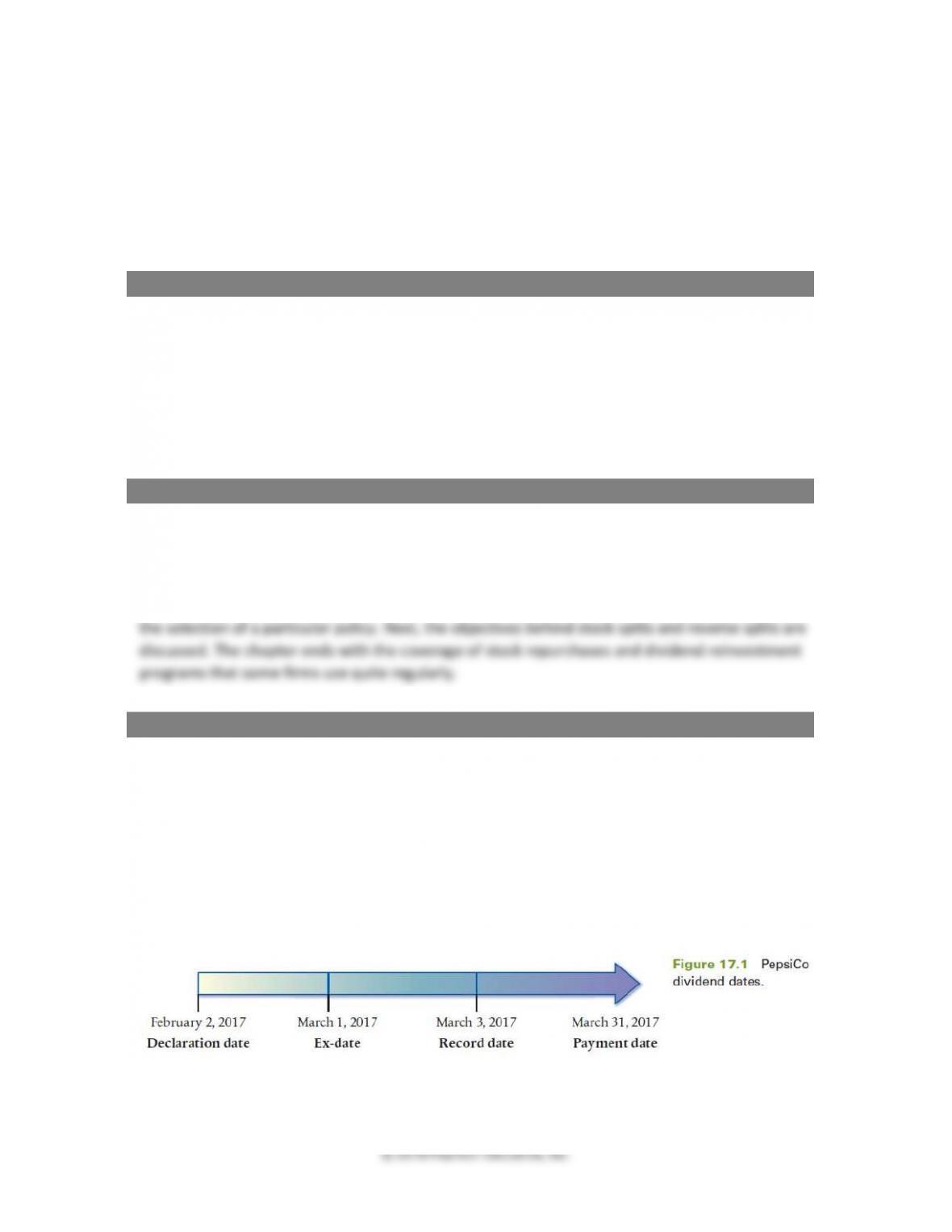

Figure 17.1 shows the typical time-line involved in the declaration and payment of dividends.

Four key dates include the following:

1. Declaration date is the day on which the board of directors announce that they will be

paying a dividend. The amount per share, the last day to record ownership information, and

2. Ex-dividend date, informally called the ex-date, is the date that establishes the recipient of

the dividend. It is two days before the date of record (discussed next). If you buy before the

3. The record date determines which shareholders are entitled to receive a dividend. The issuer

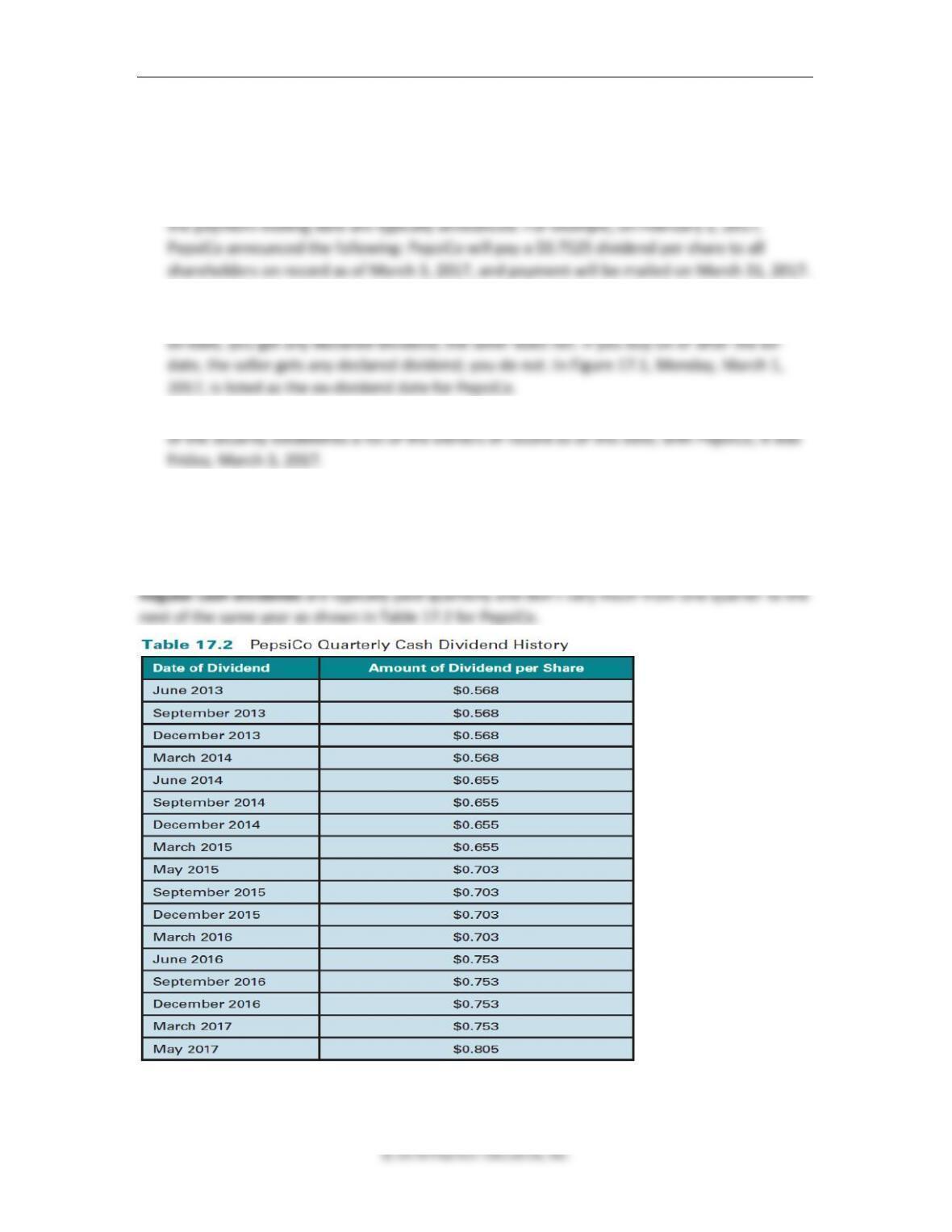

4. Payment date is the actual day on which the declared cash dividend is paid. For PepsiCo, it

was March 31, 2017.

Different types of dividends are declared by companies, including regular cash dividends,

extra dividends, stock dividends, and liquidating dividends.

© 2018 Pearson Education, Inc.

548 Brooks ◼ Financial Management: Core Concepts, 4e

© 2018 Pearson Education, Inc.

If the company pays $1.75 per share, the share price will go down by $1.75➔$6.25 per share.

Jill can take the dividend amount of $8,750 and purchase 1,400 shares. She will end up with

6,400 shares worth $6.25 each for a total of $40,000, thereby keeping the original value intact

and undoing XYZs dividend policy.

Dividends in a world of taxes would continue to remain irrelevant as long as the tax rate applied

to dividend income and capital gains is the same and if the price of the stock declines by the

after-tax value of the dividend.

Example 3: Do dividends matter with taxes and no capital gains?

So let’s say that the XYZ Co. declares a $1 per share dividend, and Jill is paying 25% taxes on

dividend income, but capital gains income is tax exempt. Also, we assume that the stock price is

$8 before the dividend declaration and drops by $0.75 (the after-tax value of the dividend) i.e.,

it drops to $7.25. Should Jill be concerned?

Example 4: Dividend policy with taxes and capital gains

Let’s say that the XYZ Co. declares $1 per share dividend, and that the price goes down by the

after-tax amount of $0.75 due to the tax rate of 25%. Moreover, capital gains are also taxable at

25% and Jill would be liable for capital gains tax because she had purchased the stock for $4 a

few months ago. Would it have been better for the firm to have not paid the dividend or was

the dividend payment irrelevant as far as Jill is concerned?

Chapter 17 ◼ Dividends, Dividend Policy, and Stock Splits 549

© 2018 Pearson Education, Inc.

Jill’s wealth would be worth $3,750 + ➔$35,714.29➔$39,464.29, which is lower than her value

with dividends. So in a world with taxes on dividends and capital gains on stock sales, DIVIDEND

POLICY DOES MATTER!

So it seems as if in a world like the one we live in, with dividends and capital gains being taxed at

more or less the same rate, dividend policy will matter at least to some types of investors. A lot

depends, of course, on the individual investor’s original purchase price, marginal tax rate, and

expectation about future stock prices.

Reasons Favoring a Low– or No-Dividend-Payout Policy: There are three commonly cited

reasons for a low- or no-dividend-payout policy:

The avoidance or postponement of taxes on distributions for shareholders, i.e., capital gains, are

not taxed till realized.

Higher potential for future returns for shareholders from firms reinvesting their own relatively

less costly internal equity in positive NPV projects.

Less need for additional costly outside funding because the firm is retaining and investing its

own profits.

550 Brooks ◼ Financial Management: Core Concepts, 4e

Reasons Favoring a High-Dividend-Payout Policy: There are two commonly cited reasons

for a high-dividend-payout policy:

Freedom from transaction costs: Unlike stock sales, which require the payment of brokerage

commissions, dividends are received without transactions costs

Certainty versus uncertainty: Unlike dividends, which are here and now, capital gains and future

performance on the stock are uncertain.

Optimal Dividend Policy: With investors’ marginal tax rates, income requirements, future

stock price expectations, and original basis in the stock being significantly different, any dividend

policy that a firm follows will leave some investors unhappy. So for any firm, the dividend policy

that is optimal is the one that suits the majority of their stockholders.

17.3 Selecting a Dividend Policy (Slides 17-27 to 17-32)

Some firms follow a “residual dividend” policy, i.e., they pay dividends only from leftover equity

after future capital requirements are met. The dividend per share fluctuates from year to year

under such a policy.

An alternative policy that many firms follow is termed a “sticky dividend” policy, under which

the firm keeps the dividend per share uniform for a few quarters to avoid sending a “false

signal” to the market that could come back to haunt them later.

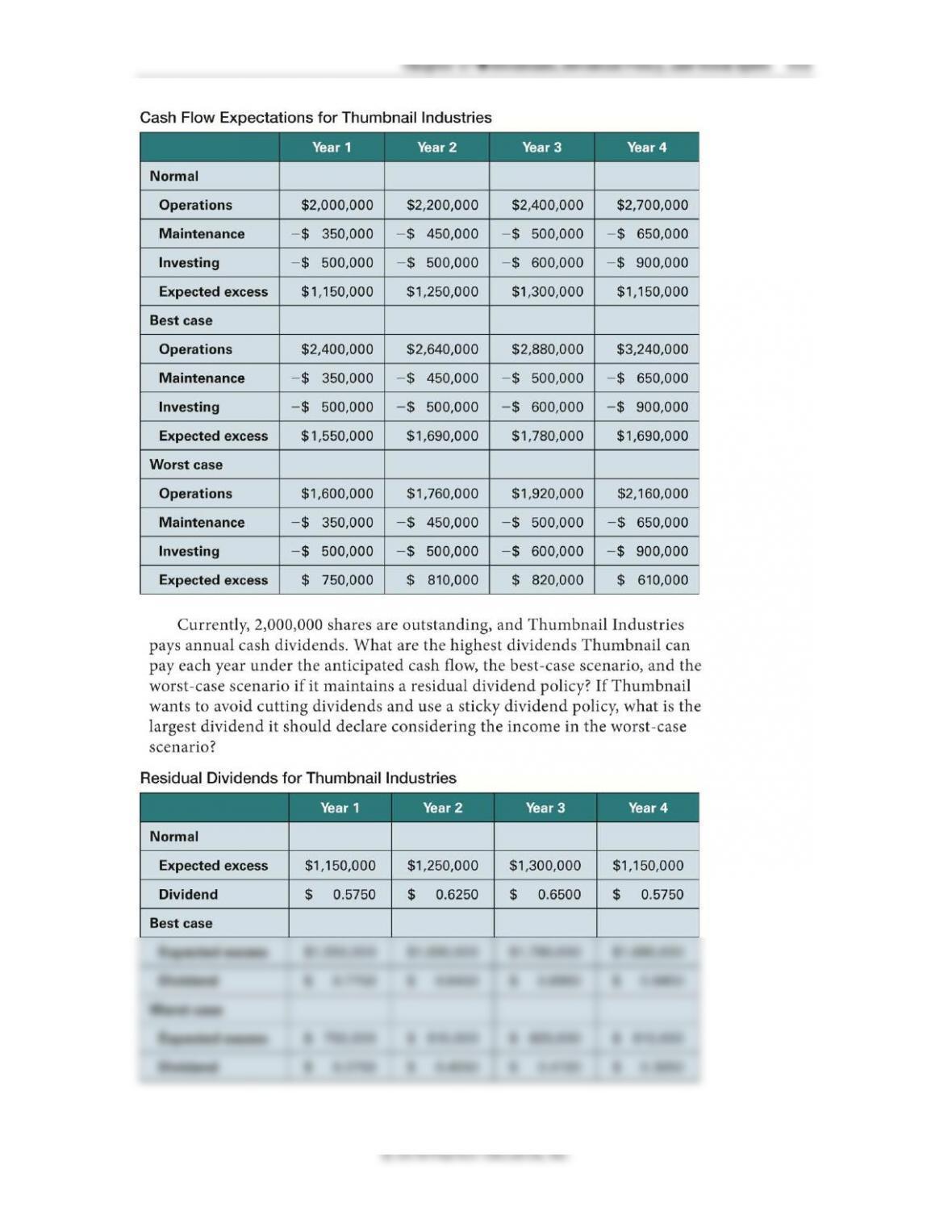

EXAMPLE 17.5 Selecting a dividend payout rate: Residual versus sticky

Problem Thumbnail Industries, makers of thumb drives for data storage, shows the following

anticipated cash inflow and outflow over the next four years. The company has estimated best–

case and worst-case scenarios in its cash flow projections in which operating inflow varies by

20%. In the best-case scenario, the company assumes inflow will be up 20%. In the worst-case

scenario, it assumes inflow will be down 20%.

556 Brooks ◼ Financial Management: Core Concepts, 4e

© 2018 Pearson Education, Inc.

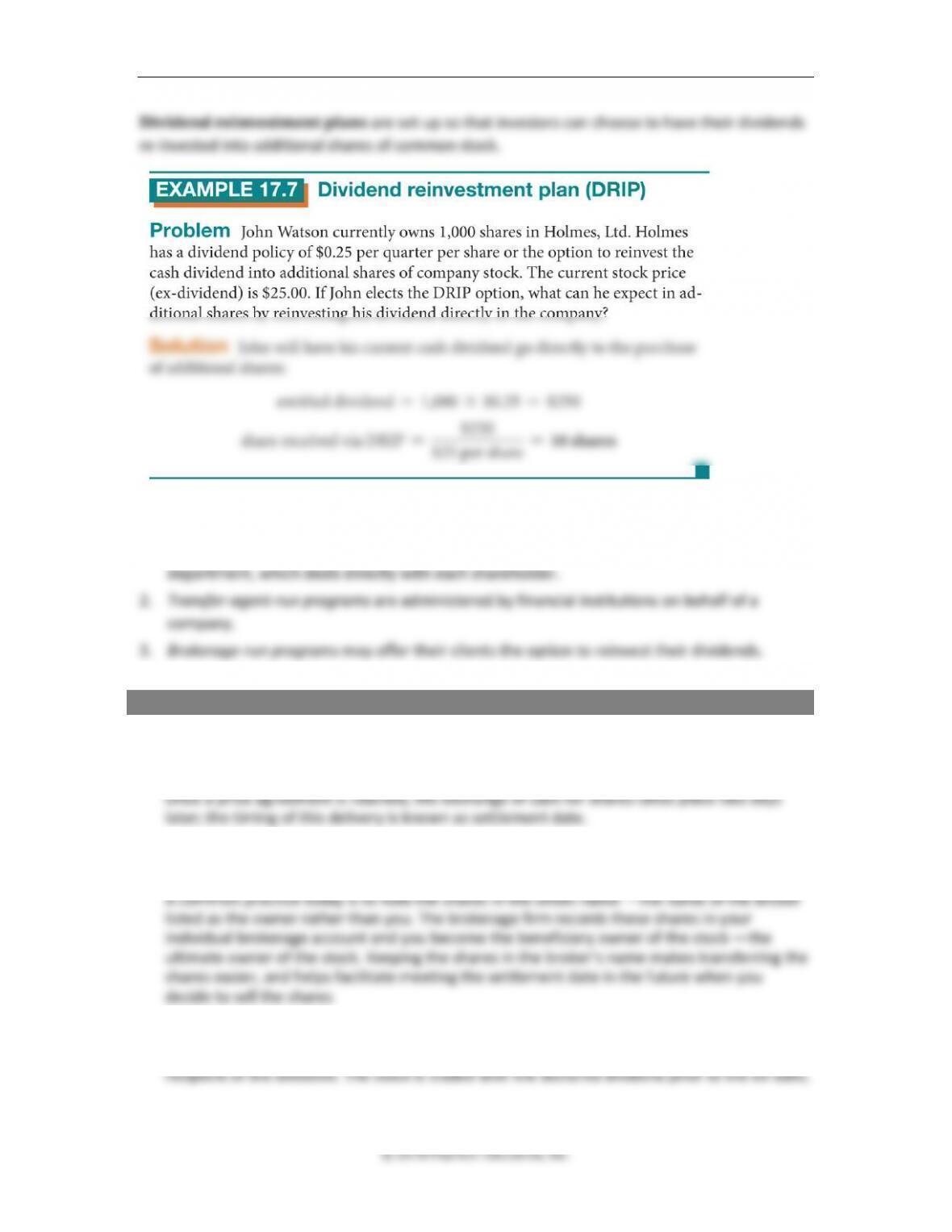

Dividend reinvestment plans are set up so that investors can choose to have their dividends

re-invested into additional shares of common stock.

DRIPs can be found in three types of investment programs:

1. Company-run programs are usually administered from the company’s investor relations

Questions

1. When you agree to buy a stock on the NYSE or NASDAQ, how much time after the agreed-

upon sale do you have to provide the necessary funds for the purchase? What is the name

given to the actual delivery of funds and stocks for exchange?

2. What does it mean to be a beneficiary owner of stock? Why would individuals find this

ownership stake convenient?

3. Explain why we use the term ex-date when pricing a stock that has a declared dividend.

The ex-dividend date —informally called the ex-date— is the date that establishes the

© 2018 Pearson Education, Inc.

© 2018 Pearson Education, Inc.