538 Brooks ◼ Financial Management: Core Concepts, 4e

5. Break-even EBIT (with and without taxes). Alpha Company is looking at two different

capital structures, one an all-equity firm, and the other a levered firm with $2 million of debt

financing at 8% interest. The all-equity firm will have a value of $4 million and 400,000

shares outstanding. The levered firm will have 200,000 shares outstanding.

a. Find the break-even EBIT for Alpha Company using EPS if there are no corporate taxes.

b. Find the break-even EBIT for Alpha Company using EPS if the corporate tax rate is 30%.

c. What do you notice about these two break-even EBITS for Alpha Company?

6. Break-even EBIT (with taxes). Beta, Gamma, and Delta Companies are similar in every way

except for their capital structures. Beta is an all-equity firm with $3,600,000 of value and

100,000 shares outstanding. Gamma is a levered firm with the same value as Beta, but with

$1,080,000 in debt at 9% and 70,000 shares outstanding. Delta is a levered firm with

$2,160,000 in debt at 12% and 40,000 shares outstanding. What are the break-even EBITs

for Beta and Gamma, Beta and Delta, and Gamma and Delta Companies if the corporate tax

rate is 40% for all three companies?

© 2018 Pearson Education, Inc.

7. Pecking order hypothesis. Rachel can raise capital from the following sources:

Source of Funds

Interest Rate

Borrowing Limit

Parents

0%

$10,000

Friends

5%

$2,000

Bank Loan

9%

$15,000

Credit Card

14.5%

$5,000

What is Rachel’s weighted average cost of capital if she needs to raise

a. $10,000?

b. $20,000?

c. $30,000?

ANSWER

542 Brooks ◼ Financial Management: Core Concepts, 4e

© 2018 Pearson Education, Inc.

ANSWER

RE = Ra + (Ra – RD) × (D/E)

Current required cost of equity: 0.20 + (0.20 – 0.10) (0) = 0.20 or 20%

New required cost of equity: 0.20 + (0.20 – 0.10) (0.5/0.5) = 0.30 or 30%

544 Brooks ◼ Financial Management: Core Concepts, 4e

Once again this problem can be solved by adding the tax shield to the current after tax equity

value without debt.

VE = $25,000,000 (1 – 0.4) = $15,000,000

VL = VE + (D × TC)

a. $15,000,000 + ($6,250,000 × 0.4) = $17,500,000

b. $15,000,000 + ($18,750,000 × 0.4) = $22,500,000

15. Size of tax shield. Using the information from Problems 11 and 13 on Air Seattle, determine

the size of the tax shield with a corporate tax rate of 15%, 25%, 35%, and 45% if Air Seattle’s

capital structure is 50/50 debt to equity.

ANSWER

16. Size of tax shield. Using the information from Problems 12 and 14 on Roxy Broadcasting,

determine the size of the tax shield with a corporate tax rate of 15%, 25%, 35%, and 45%

if Roxy’s capital structure is 1/3 debt to equity. Determine the same if the capital structure

is 3/1.

ANSWER

Equity Slice (b)

$15,000,000

$11,250,000

$3,750,000

Equity Wealth (a + b)

$15,000,000

$17,500,000

$22,500,000

Equity Increase

$2,500,000

$7,500,000

Tax Shield

$0

$2,500,000

$7,500,000

Chapter 16 ◼ Capital Structure 545

© 2018 Pearson Education, Inc.

New debt issues with 25% debt = $25,000,000 × (0.25) = $6,250,000

Tax shield = (D × TC)

a. TC @15% ($6,250,000 × 0.15) = $937,500

b. TC @25% ($6,250,000 × 0.25) = $1,562,500

c. TC @35% ($6,250,000 × 0.35) = $2,187,500

d. TC @45% ($6,250,000 × 0.45) = $2,812,500

New debt issues with 75% debt = $25,000,000 × (0.75) = $18,750,000

Tax shield = (D × TC)

a. TC @15% ($18,750,000 × 0.15) = $2,812,500

b. TC @25% ($18,750,000 × 0.25) = $4,687,500

c. TC @35% ($18,750,000 × 0.35) = $6,562,500

d. TC @45% ($18,750,000 × 0.45) = $8,437,500

Chapter 16 ◼ Capital Structure 547

Solutions to Advanced Problems for Spreadsheet Application

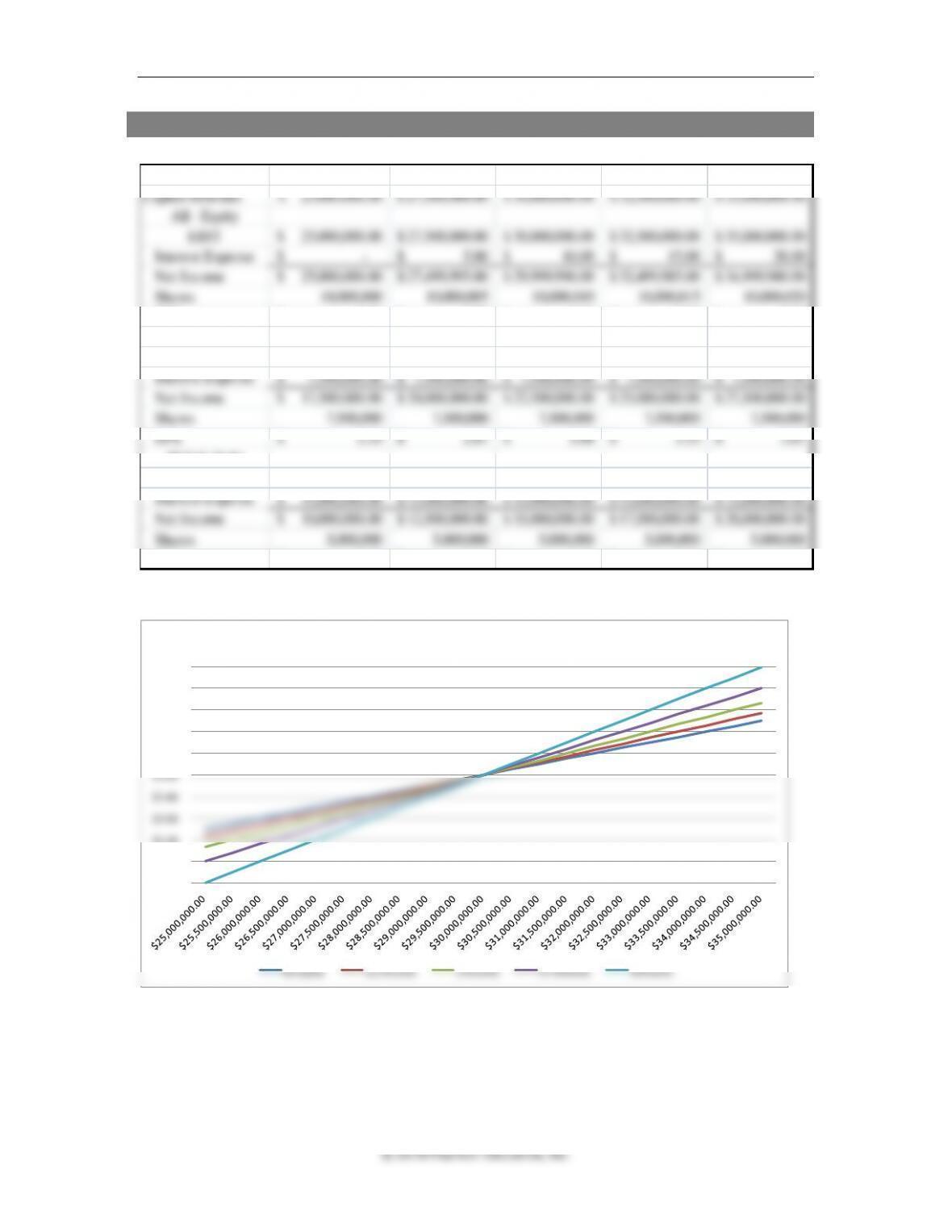

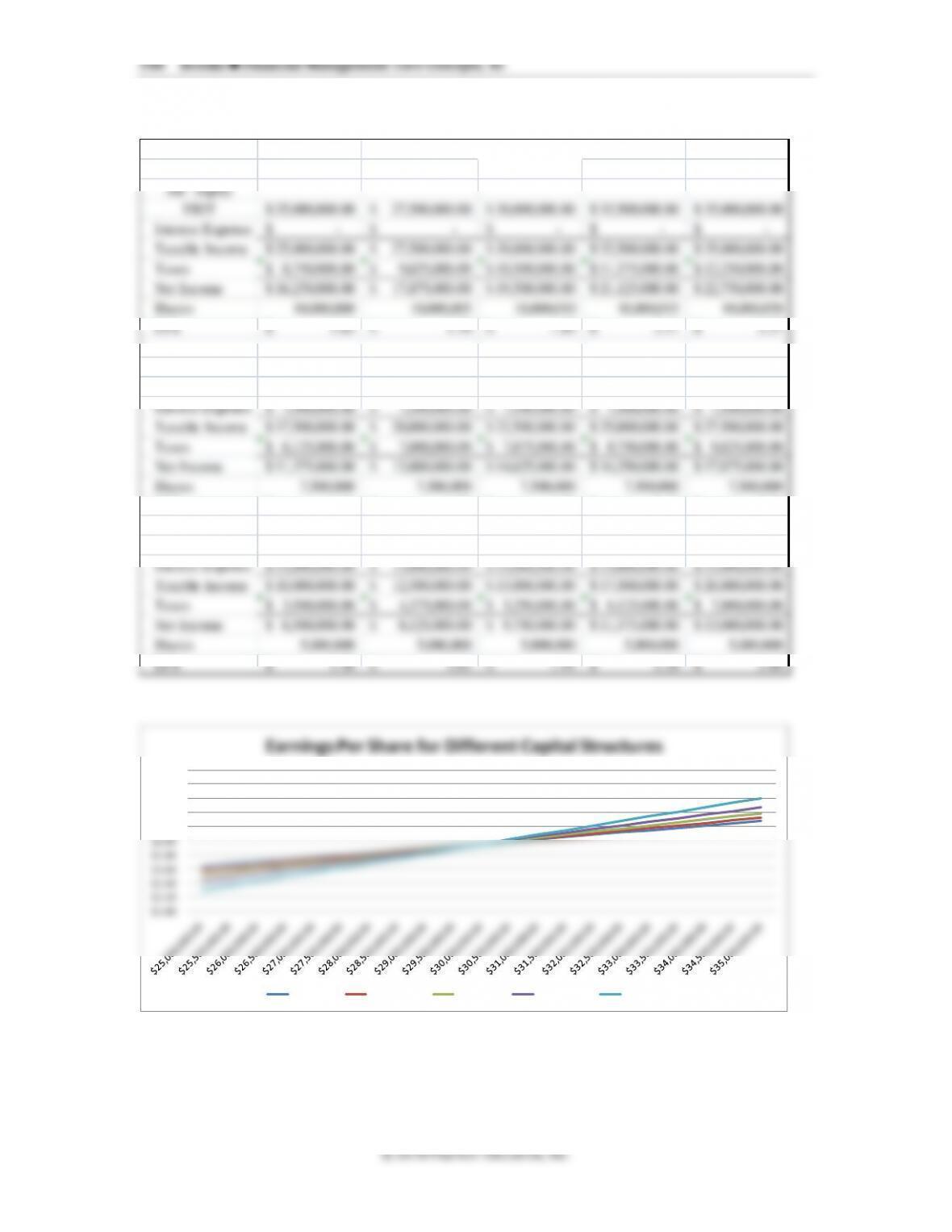

1. Break-even EBIT for different capital structures in a world of no taxes.

Jordan Enterprises EBIT

Capital Structure 25,000,000.00$ 27,500,000.00$ 30,000,000.00$ 32,500,000.00$ 35,000,000.00$

All – Equity

EBIT 25,000,000.00$ 27,500,000.00$ 30,000,000.00$ 32,500,000.00$ 35,000,000.00$

Interest Expense –$ 5.00$ 10.00$ 15.00$ 20.00$

Net Income 25,000,000.00$ 27,499,995.00$ 29,999,990.00$ 32,499,985.00$ 34,999,980.00$

Shares 10,000,000 10,000,005 10,000,010 10,000,015 10,000,020

EPS 2.50$ 2.75$ 3.00$ 3.25$ 3.50$

25.0 % Debt

EBIT 25,000,000.00$ 27,500,000.00$ 30,000,000.00$ 32,500,000.00$ 35,000,000.00$

Interest Expense 7,500,000.00$ 7,500,000.00$ 7,500,000.00$ 7,500,000.00$ 7,500,000.00$

Net Income 17,500,000.00$ 20,000,000.00$ 22,500,000.00$ 25,000,000.00$ 27,500,000.00$

Shares 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000

EPS 2.33$ 2.67$ 3.00$ 3.33$ 3.67$

50.0 % Debt

EBIT 25,000,000.00$ 27,500,000.00$ 30,000,000.00$ 32,500,000.00$ 35,000,000.00$

Interest Expense 15,000,000.00$ 15,000,000.00$ 15,000,000.00$ 15,000,000.00$ 15,000,000.00$

Net Income 10,000,000.00$ 12,500,000.00$ 15,000,000.00$ 17,500,000.00$ 20,000,000.00$

Shares 5,000,000 5,000,000 5,000,000 5,000,000 5,000,000

EPS 2.00$ 2.50$ 3.00$ 3.50$ 4.00$

$2.40

$2.60

$2.80

$3.00

$3.20

$3.40

$3.60

$3.80

$4.00

Earnings Per Share for Different Capital Structures

All Equity

12.5% Debt

25% Debt

37.5% Debt

50% debt

Chapter 16 ◼ Capital Structure 549

Solutions to Mini-Case

General Energy Storage Systems: How Much Debt and How Much Equity?

1. Why should GESS expect to pay a higher rate of interest if it borrows $4,000,000 rather

than $2,000,000?

2. Estimate earnings per share for plan A and plan B at EBIT levels of $800,000, $1,000,000,

and $1,200,000.

Plan A

EBIT

$ 800,000.00

$1,000,000.00

$1,200,000.00

Interest 9%

360,000.00

360,000.00

360,000.00

EBT

440,000.00

640,000.00

840,000.00

Tax 40%

176,000.00

256,000.00

336,000.00

Net Inc.

$264,000.00

$384,000.00

$504,000.00

Shares outstanding

300,000.00

300,000.00

300,000.00

E.P.S.

$0.88

$1.28

$1.68

Plan B

EBIT

$ 800,000.00

$1,000,000.00

$1,200,000.00

Interest 8%

160,000.00

160,000.00

160,000.00

EBT

640,000.00

840,000.00

1,040,000.00

Tax 40%

256,000.00

336,000.00

416,000.00

Net Inc.

$384,000.00

$504,000.00

$624,000.00

Shares outstanding

400,000.00

400,000.00

400,000.00

E.P.S.

$0.96

$1.26

$1.56

552 Brooks ◼ Financial Management: Core Concepts, 4e

Additional Problems with Solutions

1. Different loan rates. Diversified Holdings has four subsidiaries, each of which borrows funds

from the parent company and has a different success rate with the projects it undertakes.

Subsidiary A is successful with its projects 80% of the time, Subsidiary B gets it right 93% of

the time, Subsidiary C gets it 75% of the time, and Subsidiary D gets it 85% of the time. What

loan rates should Diversified Holdings charge each subsidiary for loans?

2. Benefits of borrowing. Loyola Turbo Engines is looking to expand its operations by adding

another manufacturing location. If successful, the company will make $750,000, but if it

fails, the company will lose $300,000. Loyola can borrow the required capital of 300,000 at

16%.

(a) If all their projections point to an 85% probability of success, should they borrow the

money and go ahead with the expansion?

(b) Above what minimum probability of success will the project be acceptable with a

discount rate of 16%?

Chapter 16 ◼ Capital Structure 555

© 2018 Pearson Education, Inc.

Equity value after tax with new structure = $7,692,307.70 × (1 – 0.35) = $5,000,000

New equity wealth after tax = $5,000,000 + $7,692,307.7 = $12,692,307.7

Or this problem can be solved by adding the current equity wealth unlevered to the tax

shield VL = VE + (D × TC)

$10,000,000 + ($7,692,307.70 × 0.35) = $12,692,307.7

5. Equity value in a levered firm. Sea Crest Corporation, which is an all-equity firm, has an

annual EBIT of $2,540,000, and a WACC of 15%. The current tax rate is 35%. Sea Crest Corp.

will have the same EBIT forever. If the company sells debt worth $3,250,000 with a cost of

debt of 10%, what is the value of equity in the unlevered and levered firm? What is the

value of debt in the levered firm? What is the government’s value in the unlevered and

levered firm?

ANSWER (Slides 16-48 to 16-49)