394

Chapter 12

Forecasting and Short-Term Financial

Planning

LEARNING OBJECTIVES (Slide 12-2)

1. Understand the sources and uses of cash in building a cash budget.

2. Explain how companies use sales forecasts to predict cash inflow.

3. Understand how production costs vary in terms of cash flow timing.

4. Explain possible ways to cover cash deficits and invest cash surplus.

5. Prepare a pro forma income statement and a pro forma balance sheet.

IN A NUTSHELL…

Financial forecasting and planning are tasks that every financial manager must perform

diligently in order to prevent cash flow problems and unnecessary higher costs of financing in

the future.

A cash budget is the basic financial planning tool for any individual or business, so the author

begins by identifying the various sources and uses of cash that are part of a cash budget. With

sales being the base variable, affecting almost all parts of a budget, the process of sales

forecasting is covered next. This is followed by an explanation of the timing of various

production costs and their consequential effects on possible cash deficits and surpluses. The

alternative sources available to cover cash shortages and the possible options for investing

surplus cash are then discussed. In the last section, the author illustrates the process of

preparing a pro-forma income statement and balance sheet as part of short-term financial

planning.

LECTURE OUTLINE

12.1 Sources and Uses of Cash (Slides 12-3 to 12-5)

Cash is considered to be the life-blood of a business. Cash shortages can be stifling and

expensive while excesses can lead to poor returns.

Because most businesses do not function on a pure cash basis, it is critical for them to forecast

their needs for cash in advance.

The cash budget is the analytical tool that estimates the future timing of cash inflow and cash

outflow and projects potential shortfalls and surpluses.

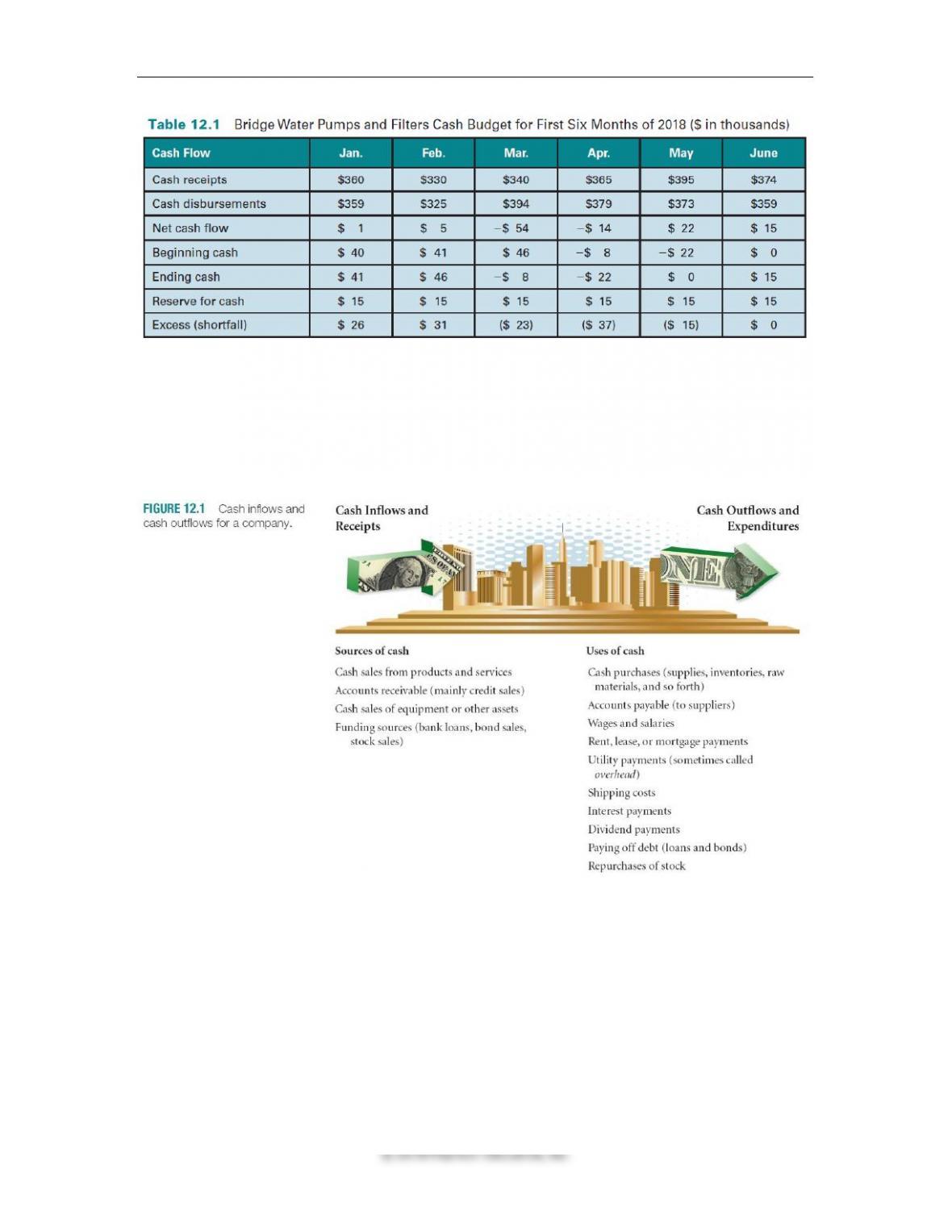

Table 12.1 presents the summary of a cash budget prepared for a hypothetical manufacturing

firm, Bridge Water Pumps and Filters.

Chapter 12 ◼ Forecasting and Short-Term Financial Planning 395

Notice how despite setting up a cash reserve, the firm is projected to have cash shortfalls in

three months and surpluses in two after all cash receipts and disbursements have been

forecasted for the first half of 2018.

Identifying all possible sources and uses of cash is essential for preparing a useful cash budget.

Figure 12.1 lists the various avenues of cash inflow and outflow typically faced by a firm.

This list can serve as a guide when preparing a cash budget.

12.2 Cash Budgeting and the Sales Forecast (Slides 12-6 to 12-10)

Because sales revenue is the base variable driving almost all other items in the cash budget, it is

important to forecast sales as objectively as possible.

Moreover, since there is usually a time lag between when a sale is made and when the cash

receipts come in, keeping track of when the firm receives cash from sales is as important as

determining when the sales materialize.

396 Brooks ◼ Financial Management: Core Concepts, 4e

Companies use internal data (information that is proprietary or unique to the firm) as well as

external data (publicly available information) sources to come up with objective forecasts of

sales.

Chapter 12 ◼ Forecasting and Short-Term Financial Planning 397

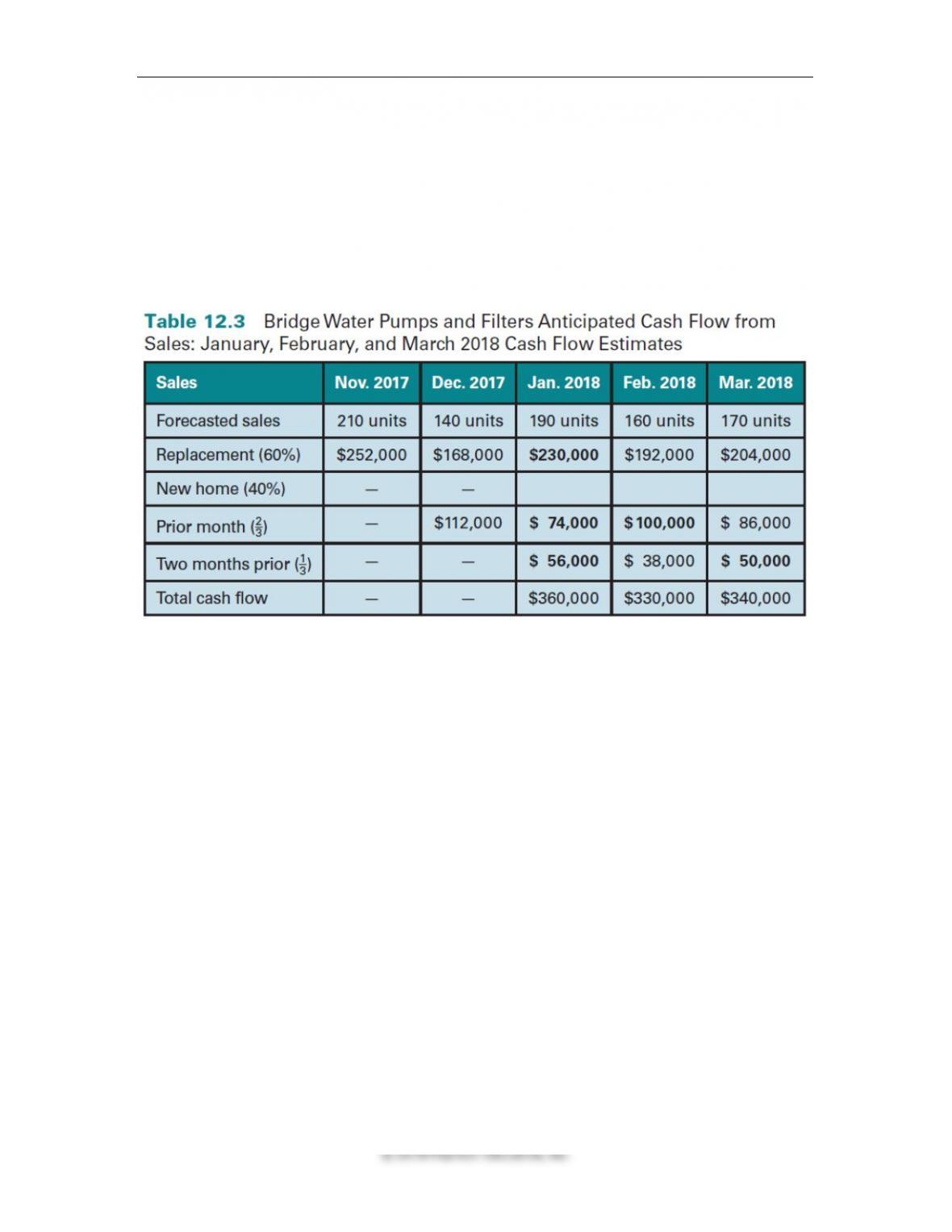

Cash Inflow from Sales: Firms typically sell products and services partially for cash and

partially on credit.

Thus, an analysis of a firm’s collection policy can help project cash inflow from sales.

It is quite common for firms to collect some of their receivables in the two months following the

sale, i.e., November 2017’s credit sales will be partially collected in December and January.

Table 12.3 presents an example of how the cash inflow from a firm’s forecasted sales are

allocated for the purpose of preparing a cash budget.

Managers often figure in a small percentage of the forecasted sales as bad debts when

preparing a cash budget.

Other Cash Receipts: Besides sales, which are the main contributor to a firm’s cash inflow, the

timing and magnitude of other occasional sources of cash such as asset sales, funds raised

through issuance and sale of securities, and income earned on investments (dividends, interest,

etc.) must be forecasted when preparing a cash budget.

12.3 Cash Outflow from Production (Slide 12-11)

The magnitude and timing of the various cash disbursements of a firm depend to a large extent

on its forecasted sales.

These cash outflow items include payments for raw materials, labor costs, overheads such as

utilities and rent, shipping costs, etc.

As in the case of sales, there is often a time lag between when the firm receives and records the

benefit, and when it actually makes the payment for it. The cash budget can be used as a handy

planning document to keep track of the projected disbursements.

Note: Students often assume that depreciation should be accounted for as a cash disbursement,

which is incorrect because depreciation is merely a tax write-off and not a cash outflow.

Chapter 12 ◼ Forecasting and Short-Term Financial Planning 399

statement) or total assets (balance sheet) for the coming year to develop pro forma financial

statements.

For example, let’s say that the cash balance for the prior year is $2 million and the total assets

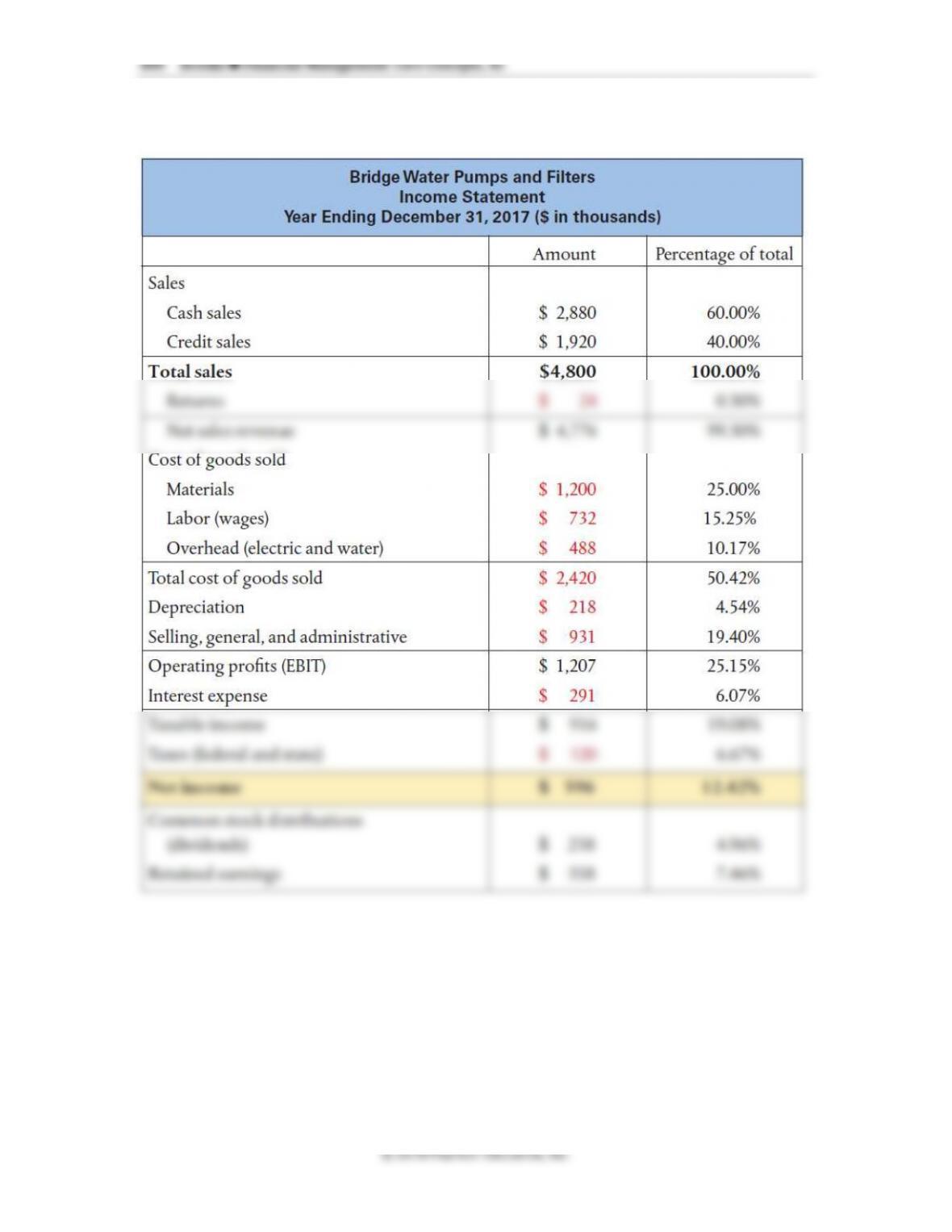

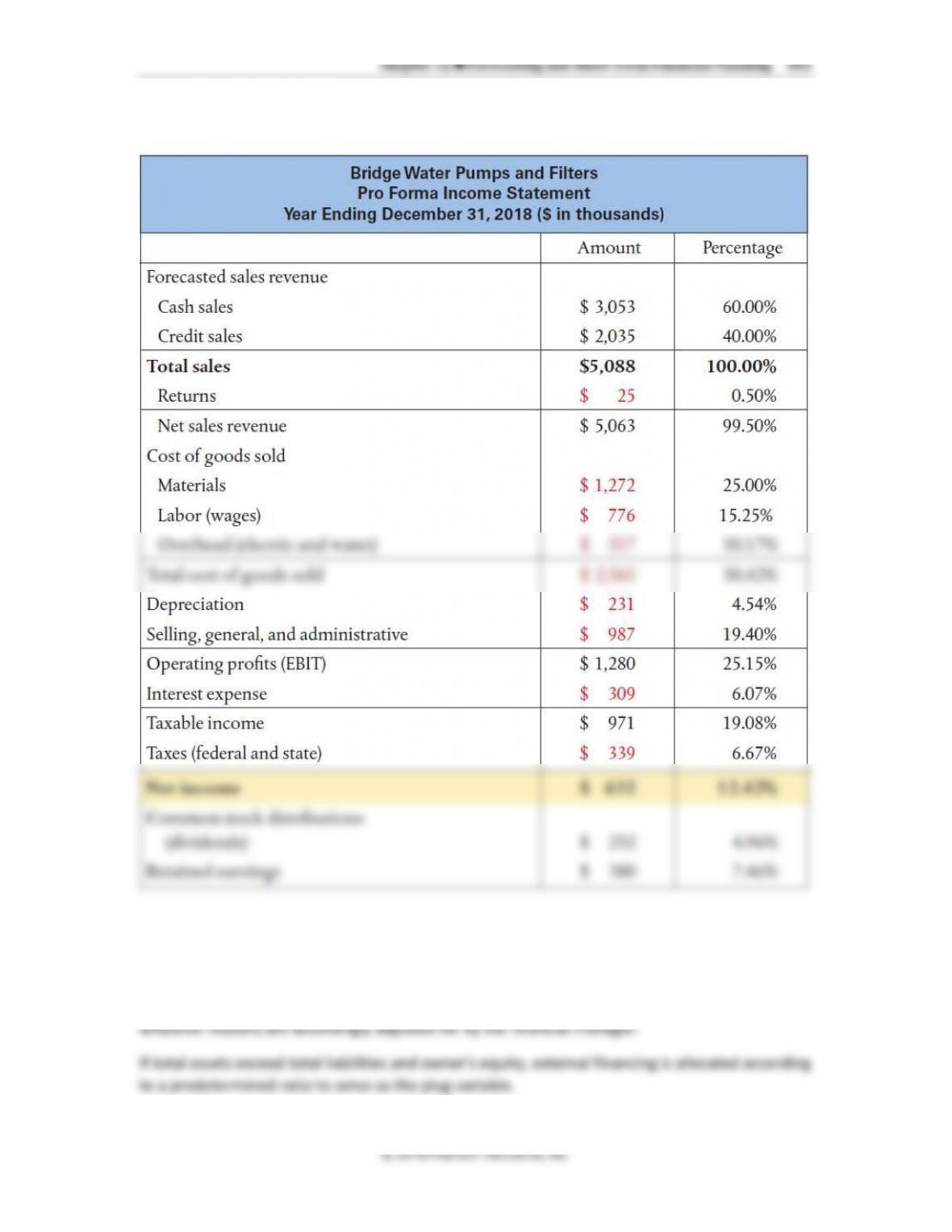

Pro Forma Income Statement: Figure 12.3 shows how each income statement item is

expressed as a percentage of sales.

Figure 12.4, shows how the pro forma income statement is developed, i.e., by multiplying the

percentages of each item to sales by the forecasted sales for the next period.

This approach, although a good first step, can be considered too simplistic in reality because

many financial statement items do not vary proportionately with sales. In particular,

depreciation decreases over time and cost of goods sold often declines due to economies of

scale.

The manager would have to fine-tune the forecasted values to make them more in line with

reality.

Chapter 12 ◼ Forecasting and Short-Term Financial Planning 403

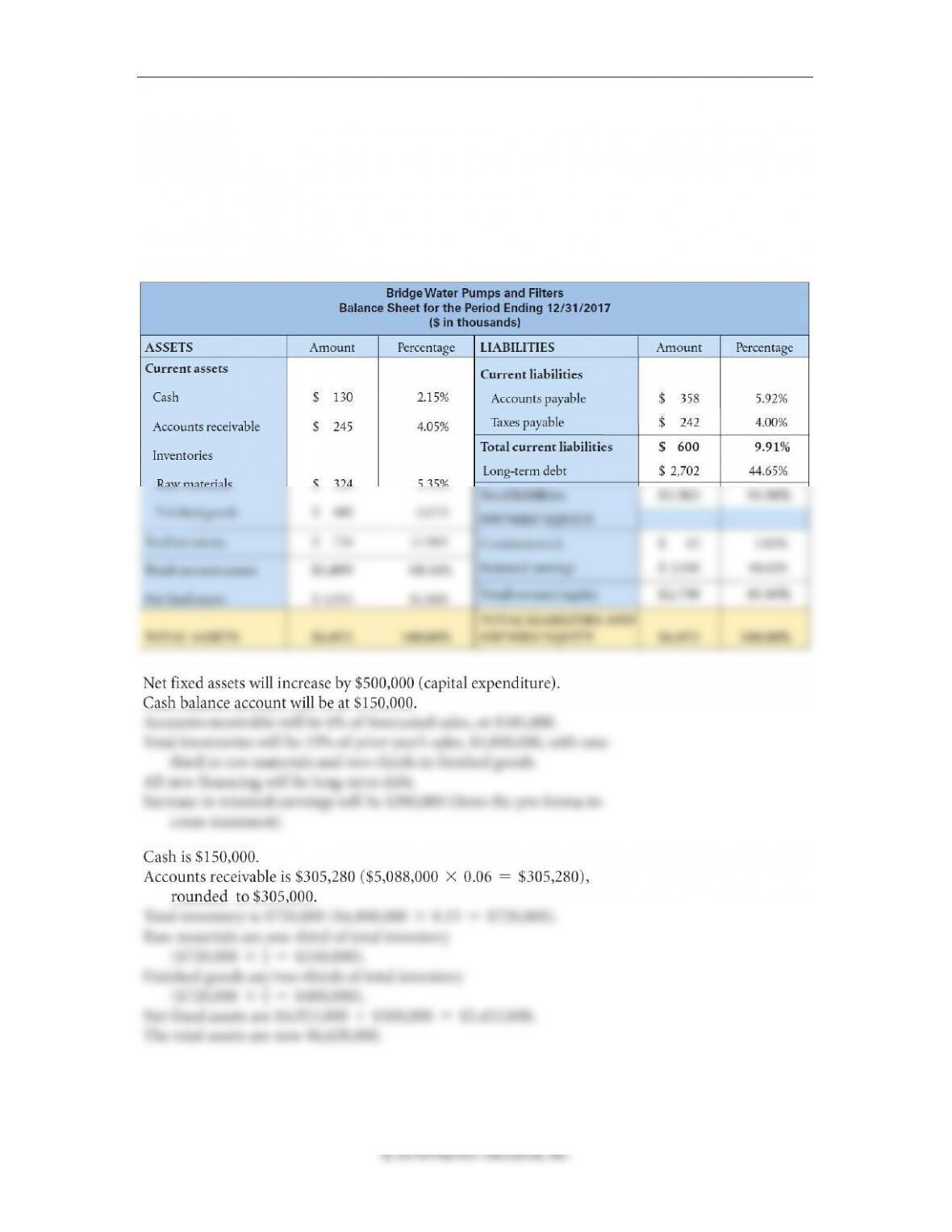

Figure 12.5 shows the balance sheet items of Bridge Water Pumps and Filters, expressed as a

percentage of total assets.

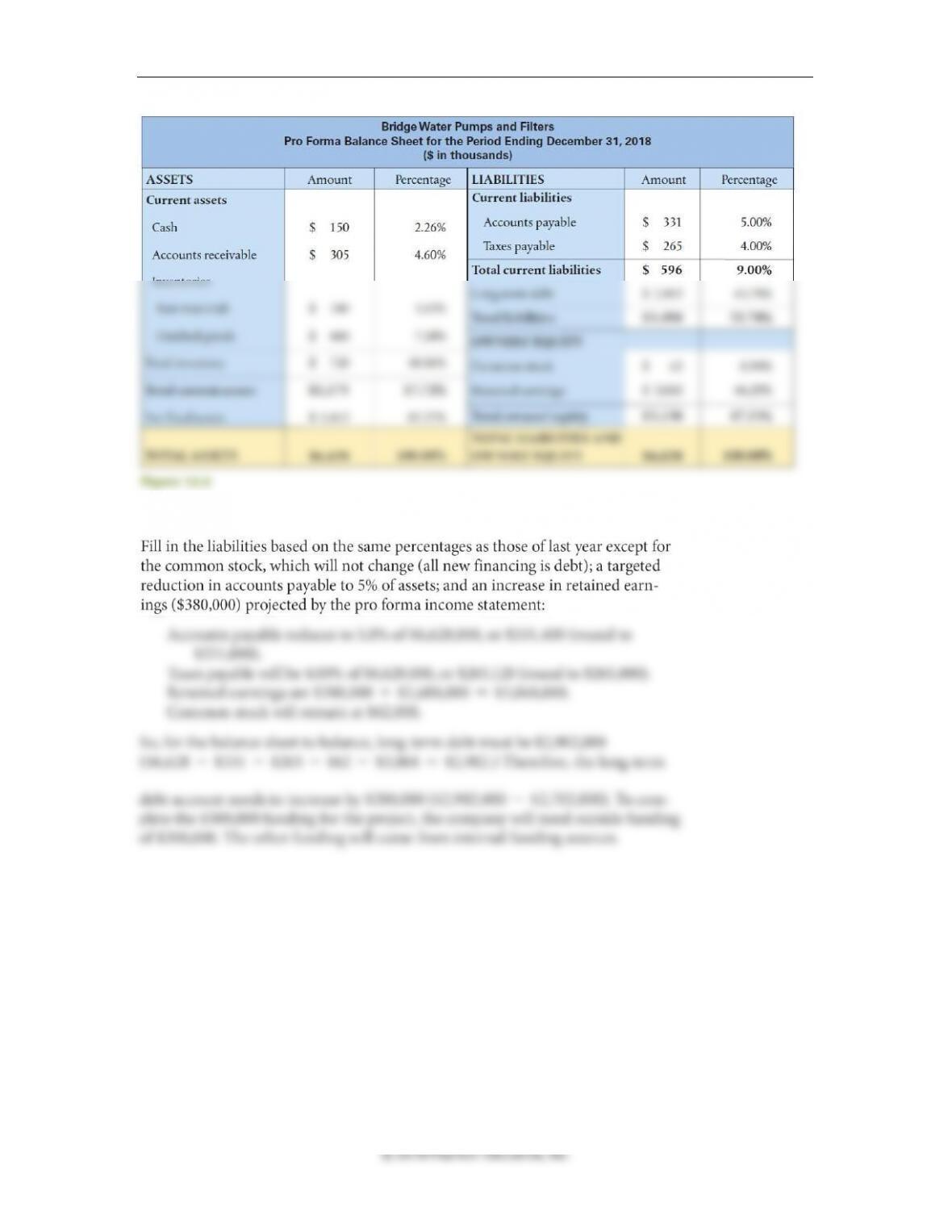

Based on the following assumptions, a pro forma balance sheet is developed in Figure 12.6.

Figure 12.5

404 Brooks ◼ Financial Management: Core Concepts, 4e

© 2018 Pearson Education, Inc.

Key calculations include:

Chapter 12 ◼ Forecasting and Short-Term Financial Planning 405

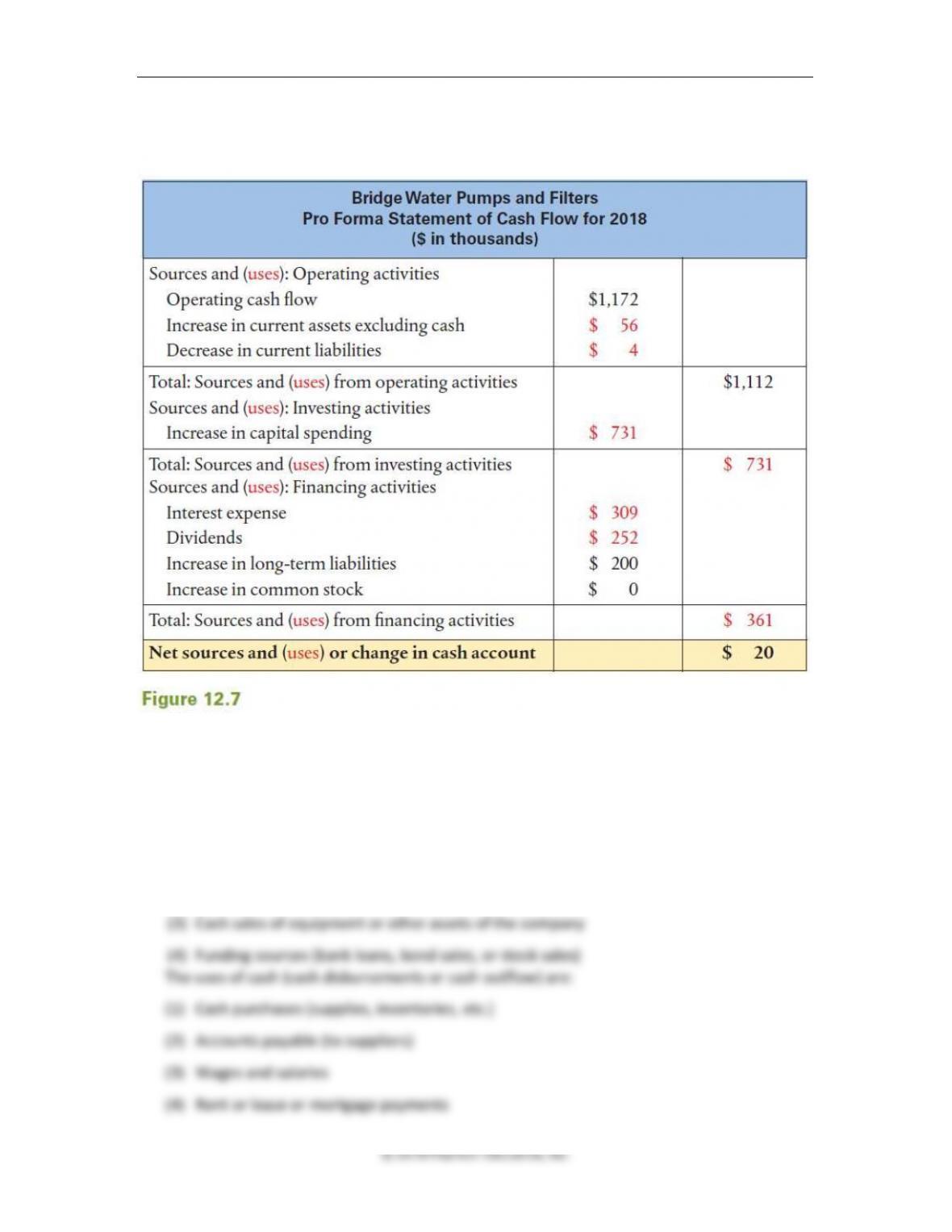

Finally, the pro forma cash flow statement (Figure 12.7) is prepared to tie together all the

changes in operating, investment, and financing cash flows.

Questions

1. What are a company’s main sources of cash for a company? What are a company’s main

uses of cash?

The sources of cash (cash receipts or cash inflow) are as follows:

(1) Cash sales from products and services

(2) Payments received on accounts receivables (mainly credit sales)

© 2018 Pearson Education, Inc.

2. What are two key timing issues with respect to predicting cash inflow for a sales forecast?

3. What are some of the production costs that are tied to the sales forecast?

4. What is a line of credit? Why would a bank require a company with a line of credit to have

a zero balance in its line of credit for at least sixty days a year?

5. What is the difference between a secured and an unsecured loan?

6. Why can excess cash be an opportunity cost for a company?

7. If a pro forma income statement has 5% for the net income line, what does this mean in

terms of a company’s total sales and per dollar sales?

8. When preparing a pro forma income statement, why would a finance manager make

changes in the prior year’s percentages for different line items? Give an example of a line

item that you would expect to vary in percentage every year as sales forecasts grow.

408 Brooks ◼ Financial Management: Core Concepts, 4e

Prepping for Exams

1. a

2. c

Problems

1. Sales forecasts. For the prior three years, sales for National Beverage Company have been

$21,962,000 (2015), $23,104,000 (2016), and $24,088,000 (2017). The company uses the

prior two year’s average growth rate to predict the coming year’s sales. What were the sales

growth rates for 2016 and 2017? What is the expected sales growth rate using a two-year

average for 2018? What is the sales forecast for 2018?

Remind students that this would be the geometric mean!

ANSWER

2. Sales forecasts. For the prior three years, sales for California Cement Company have been

$20,011,000 (2015), $21,167,000 (2016), and $22,923,000 (2017). CCC uses the prior two

year’s average growth rate to predict the coming year’s sales. What were the sales growth

rates for 2016 and 2017? What is the expected sales growth rate using a two-year average

for 2018? What is the sales forecast for 2018?

ANSWER

Chapter 12 ◼ Forecasting and Short-Term Financial Planning 409

© 2018 Pearson Education, Inc.

Growth rate 2017 = ($22,923 / $21,167) – 1 = 8.30%

Two year average = ($22,923 / $20,011)1/2 – 1 = 7.028966%

Sales Forecast 2018 = $22,923,000 × 1.07028966 = $24,534,250

Note, the growth rate was not rounded in the final sales forecast answer.

3. Sales forecast based on external data. Raspberry Phones uses external data to forecast the

coming year’s sales. The company has 8% of all new-phone sales in the United States and 6%

of all replacement-phones sales. Industry forecasts predict an additional 18 million new–

phone buyers and 31 million replacement-phone buyers in 2018. If the average Raspberry

phone costs $85, what sales revenues is the company forecasting for 2018?

ANSWER

4. Sales forecast based on external data. Nelson Heating and Ventilating Company estimates

the coming year’s sales revenue based on external data. The company’s main business is

new shopping mall construction, and it uses the square footage of each mall as a “yardstick”

for many financial statements and projections. The company does business in four Midwest

states. Last year, it completed heating and ventilating systems on four shopping malls with

an average size of 3,000,000 square feet for sales revenues of $9,600,000. Nelson is the

primary contractor for one-third of the new malls in the four- state area. This coming year,

nine new malls are being built with an average footage of 4,500,000 square feet. What is

Nelson’s anticipated sales revenue for the coming year?

ANSWER

5. Sales receipts. National Beverage Company anticipates the following first-quarter sales for

2018: $1,800,000 (January), $1,600,000 (February), and $2,100,000 (March). It posted the

410 Brooks ◼ Financial Management: Core Concepts, 4e

following sales figures for the last quarter of 2017: $1,900,000 (October), $2,050,000

(November), and $2,200,000 (December). The company sells 40% of its products on credit,

and 60% are cash sales. The company collects credit sales as follows: 30% in the following

month, 50% two months later, and 18% three months later with 2% defaults. What are the

anticipated cash inflows for the first quarter of 2018?

ANSWER

Chapter 12 ◼ Forecasting and Short-Term Financial Planning 411

© 2018 Pearson Education, Inc.

February Sales $1,600,000

Collected in February = $1,600,000 × 0.60 = $960,000

Collected in March = $1,600,000 × 0.40 × 0.30 = $192,000

Collected in April = $1,600,000x 0.40 × 0.50 = $320,000

Collected in May = $1,600,000 × 0.40 × 0.18 = $115,200

Not collected (bad debt) = $1,600,000 × 0.40 × 0.02 = $12,800

March Sales $2,100,000

Collected in March = $2,100,000 × 0.60 = $1,260,000

Collected in April = $2,100,000 × 0.40 × 0.30 = $252,000

Collected in May = $2,100,000x 0.40 × 0.50 = $420,000

Collected in June = $2,100,000 × 0.40 × 0.18 = $151,200

Not collected (bad debt) = $2,100,000 × 0.40 × 0.02 = $16,800

FROM

January Receipts

February Receipts

March Receipts

October

$136,800

November

$410,000

$147,600

December

$264,000

$440,000

$158,400

January

$1,080,000

$216,000

$360,000

February

$960,000

$192,000

March

$1,260,000

TOTAL

$1,890,800

$1,763,600

$1,970,400

6. Sales receipts. California Cement Company anticipates the following fourth-quarter sales for

2018: $1,800,000 (October), $1,600,000 (November), and $2,100,000 (December). It posted

the following sales figures for the third quarter of 2018: $1,900,000 (July), $2,050,000

(August), and $2,200,000 (September). The company sells 90% of its products on credit, and

10% are cash sales. The credit sales are collected as follows: 60% in the following month,

20% two months later, 19% three months later, with 1% defaults. What are the anticipated

cash inflows for the last quarter of 2018?

412 Brooks ◼ Financial Management: Core Concepts, 4e

Collected in July = $1,900,000 × 0.10 = $190,000

Collected in August = $1,900,000 × 0.90 × 0.60 = $1,026,000

Collected in October = $2,200,000 × 0.90 × 0.60 = $1,188,000

Collected in November = $2,200,000 × 0.90 × 0.20 = $396,000

Chapter 12 ◼ Forecasting and Short-Term Financial Planning 413

© 2018 Pearson Education, Inc.

December Sales, $2,100,000

Collected in December = $2,100,000 × 0.10 = $210,000

Collected in January = $2,100,000 × 0.90 × 0.60 = $1,134,000

Collected in February = $2,100,000 × 0.90 × 0.20 = $378,000

Collected in March = $2,100,000 × 0.90 × 0.19 = $359,100

Not Collected (bad debts) = $2,100,000 × 0.90 × 0.01 = $18,900

FROM

October Receipts

November Receipts

December Receipts

July

$324,900

August

$369,000

$350,550

September

$1,188,000

$396,000

$376,200

October

$180,000

$972,000

$324,000

November

$160,000

$864,000

December

$210,000

TOTAL

$2,061,900

$1,878,550

$1,774,200