Chapter 10 ◼ Cash Flow Estimation 349

All-Terrain Tire Working Capital and COGS

Month

Anticipated

COGS

Beginning

Inventory

Balance

Ending Inventory

Balance

Working Capital

Increase

January

$192,000

4,000

5,000

$48,000

February

$240,000

5,000

7,000

$96,000

March

$336,000

7,000

8,000

$48,000

April

$384,000

8,000

12,000

$192,000

May

$576,000

12,000

30,000

$864,000

June

$1,440,000

30,000

39,000

$432,000

July

$1,872,000

39,000

22,000

–$816,000

August

$1,056,000

22,000

8,000

–$672,000

September

$384,000

8,000

2,000

–$288,000

October

$96,000

2,000

1,000

–$48,000

November

$48,000

1,000

3,000

$96,000

December

$144,000

3,000

5,000

$96,000

TOTAL

$6,768,000

$48,000

All-Purpose Tire Working Capital and COGS

Month

Anticipated

COGS

Beginning

Inventory

Balance

Ending Inventory

Balance

Working Capital

Increase

January

$2,220,000

60,000

54,000

–$222,000

February

$1,998,000

54,000

50,000

–$148,000

March

$1,850,000

50,000

60,000

$370,000

April

$2,220,000

60,000

65,000

$185,000

350 Brooks ◼ Financial Management: Core Concepts, 4e

Month

Anticipated

COGS

Beginning

Inventory

Balance

Ending Inventory

Balance

Working Capital

Increase

May

$2,405,000

65,000

68,000

$111,000

June

$2,516,000

68,000

75,000

$259,000

July

$2,775,000

75,000

80,000

$185,000

August

$2,960,000

80,000

70,000

–$370,000

September

$2,590,000

70,000

70,000

$0

October

$2,590,000

70,000

65,000

–$185,000

November

$2,405,000

65,000

60,000

–$185,000

December

$2,220,000

60,000

60,000

$0

TOTAL

$28,749,000

$0

Chapter 10 ◼ Cash Flow Estimation 351

All Tires Working Capital and COGS

Month

Anticipated

COGS

Beginning

Inventory

Balance

Ending Inventory

Balance

Working Capital

Increase

January

$4,880,000

128,000

133,000

$70,000

February

$4,950,000

133,000

117,000

–$750,000

March

$4,200,000

117,000

92,000

–$830,000

April

$3,370,000

92,000

117,000

$851,000

May

$4,221,000

117,000

118,000

$355,000

June

$4,576,000

118,000

116,000

$133,000

July

$4,709,000

116,000

104,000

–$631,000

August

$4,078,000

104,000

80,000

–$1,042,000

September

$3,036,000

80,000

86,000

$84,000

October

$3,120,000

86,000

100,000

$563,000

November

$3,683,000

100,000

165,000

$2,745,000

December

$6,428,000

165,000

135,000

–$1,270,000

TOTAL

$51,251000

$278,000

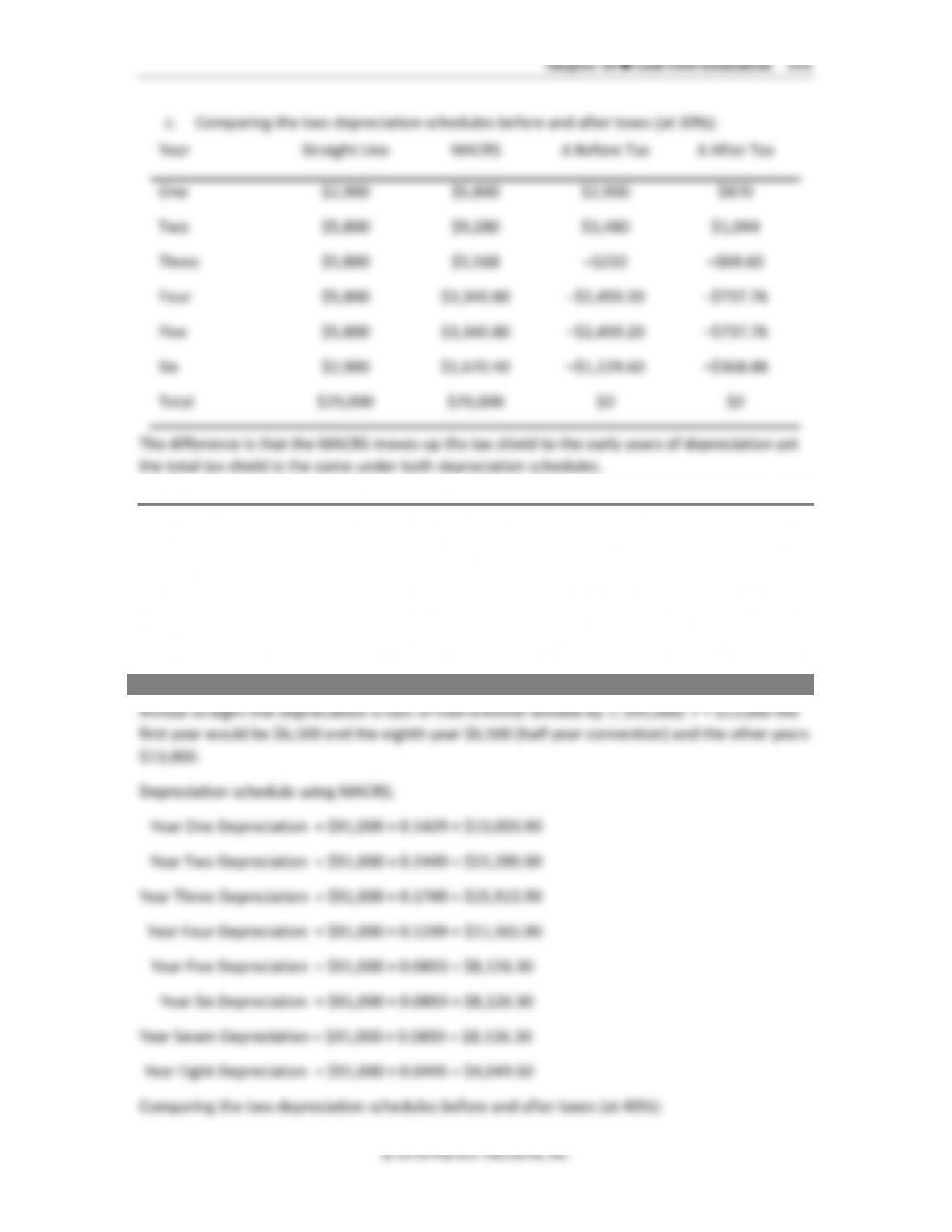

7. Depreciation expense. Brock Florist Company buys a new delivery truck for $29,000. It is

classified as a light-duty truck.

a. Calculate the depreciation schedule using a five-year life, straight-line depreciation, and

the half-year convention for the first and last years.

b. Calculate the depreciation schedule using a five year life and MACRS depreciation.

c. Compare the depreciation schedules from parts (a) and (b) before and after taxes with a

30% tax rate. What do you notice about the difference between these two methods?

352 Brooks ◼ Financial Management: Core Concepts, 4e

ANSWER

© 2018 Pearson Education, Inc.

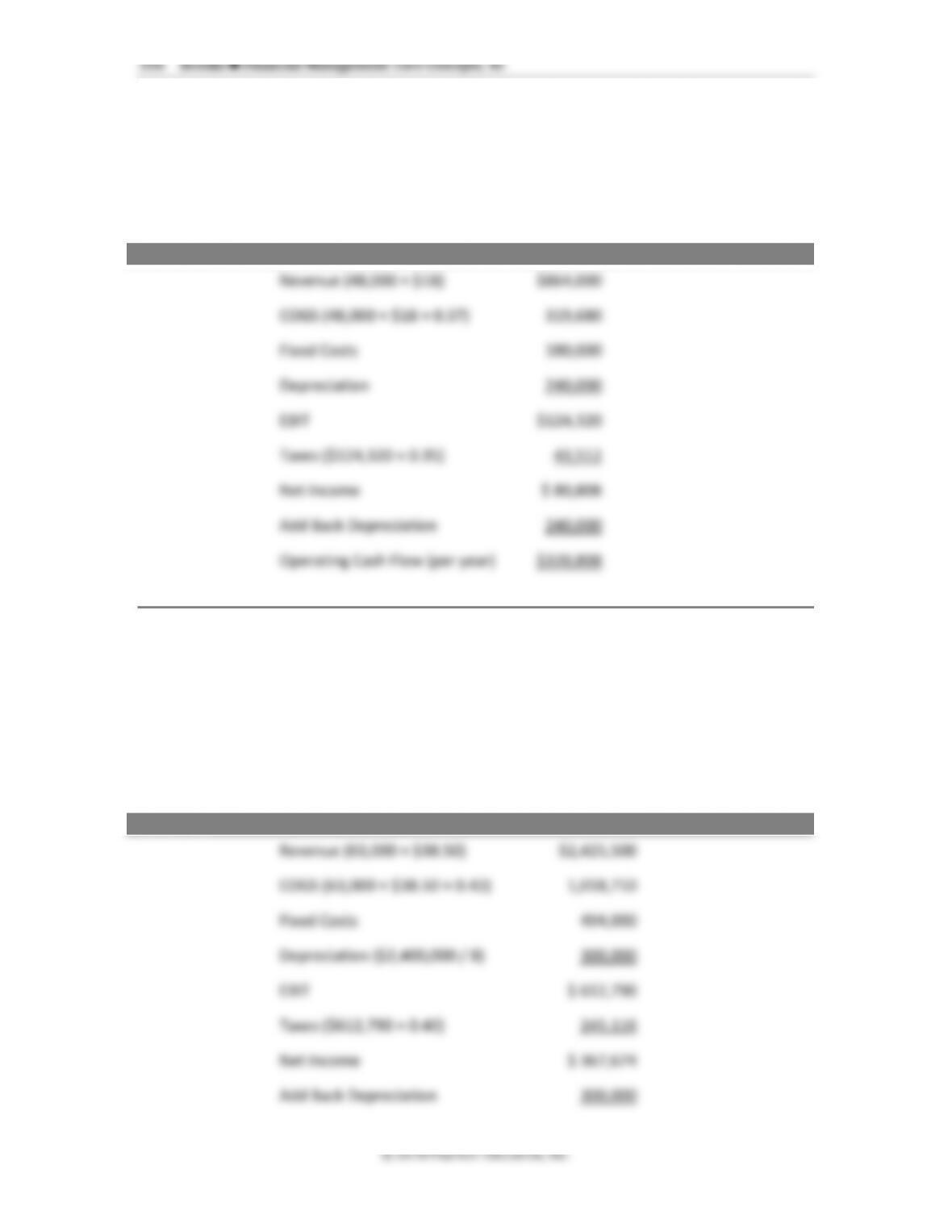

8. Depreciation expense. Richards’ Tree Farm, Inc. has just purchased a new aerial tree

trimmer for $91,000. Calculate the depreciation schedule using the property class category

of a single-purpose agricultural and horticultural structure (from Table 10.3) for both

straight line depreciation and MACRS. Use the half-year convention for both methods.

Compare the depreciation schedules before and after taxes using a 40% tax rate. What do

you notice about the difference between these two methods?

ANSWER

© 2018 Pearson Education, Inc.

9. Cost recovery. Brock Florist Company sold their delivery truck in problem (see Problem 7)

after three years of service. If MACRS was used for the depreciation schedule, what is the

after-tax cash flow from the sale of the truck (continue to use 30% tax rate) if

a. the sales price was $15,000?

b. the sales price was $10,000?

c. the sales price was $5,000?

ANSWER

The accumulated depreciation after three years using MACRS is $29,000 × (0.20 + 0.32 + 0.192)

Chapter 10 ◼ Cash Flow Estimation 357

© 2018 Pearson Education, Inc.

Operating Cash Flow (per year) $ 667,674

Chapter 10 ◼ Cash Flow Estimation 359

© 2018 Pearson Education, Inc.

Accumulated depreciation is 8 × $300,000 = $2,400,000

Basis = $2,400,000 – $2,400,000 = $0

Gain on Disposal = $210,000 – $0 = $210,000

Tax on Disposal = $210,000 × 0.40 = $84,000

After-tax cash flow at disposal = $210,000 – $84,000 = $126,000

( )

( ) ( )

8

8

1

1

1.14 1

$2,400,000 $667,674 $126,000

0.14 1.14

NPV

−

= − + +

NPV = –$2,400,000 + $667,674 × 4.6389 + $126,000 × 0.3506

NPV = –$2,400,000 + $3,097,248.81 + $44,170.44 = $741,419.25

Accept the project.

15. Operating cash flow (growing each year; MACRS). Mathews Mining Company is looking at

a project that has the following forecasted sales: first-year sales are 6,800 units and will

grow at 15% over the next four years (a five-year project). The price of the product will start

at $124 per unit and increase each year at 5%. The production costs are expected to be 62%

of the current year’s sales price. The manufacturing equipment to aid this project will have a

total cost (including installation) of $1,400,000. It will be depreciated using MACRS and has a

seven-year MACRS life classification. Fixed costs will be $50,000 per year. Mathews Mining

has a tax rate of 30%.What is the operating cash flow for this project over these five years?

Hint: Use a spreadsheet.

ANSWER

Set up in a spreadsheet

Year

1

2

3

4

5

Unit Sales

6,800

6,800 × 1.15

6,800 × 1.152

6,800 × 1.153

6,800 × 1.154

Price per unit

$124

$124 × 1.05

$124 × 1.052

$124 × 1.053

$124 × 1.054

Revenue

$843,200

$1,018,164

$1,229,433

$1,484,540

$1,792,583

COGS

$522,784

$631,262

$762,248

$920,415

$1,111,401

Fixed Costs

$50,000

$50,000

$50,000

$50,000

$50,000

Depreciation

$200,060

$342,860

$244,860

$174,860

$125,020

EBIT

$70,356

–$5,958

$172,325

$339,265

$506,162

360 Brooks ◼ Financial Management: Core Concepts, 4e

© 2018 Pearson Education, Inc.

Taxes (30%)

$21,107

–$1,787

$51,698

$101,780

$151,849

Net Income

$49,249

–$4,171

$120,627

$237,485

$354,313

Add Back

Depreciation

$200,060

$342,860

$244,860

$174,860

$125,020

OCF

$249,309

$338,689

$365,487

$412,345

$479,333

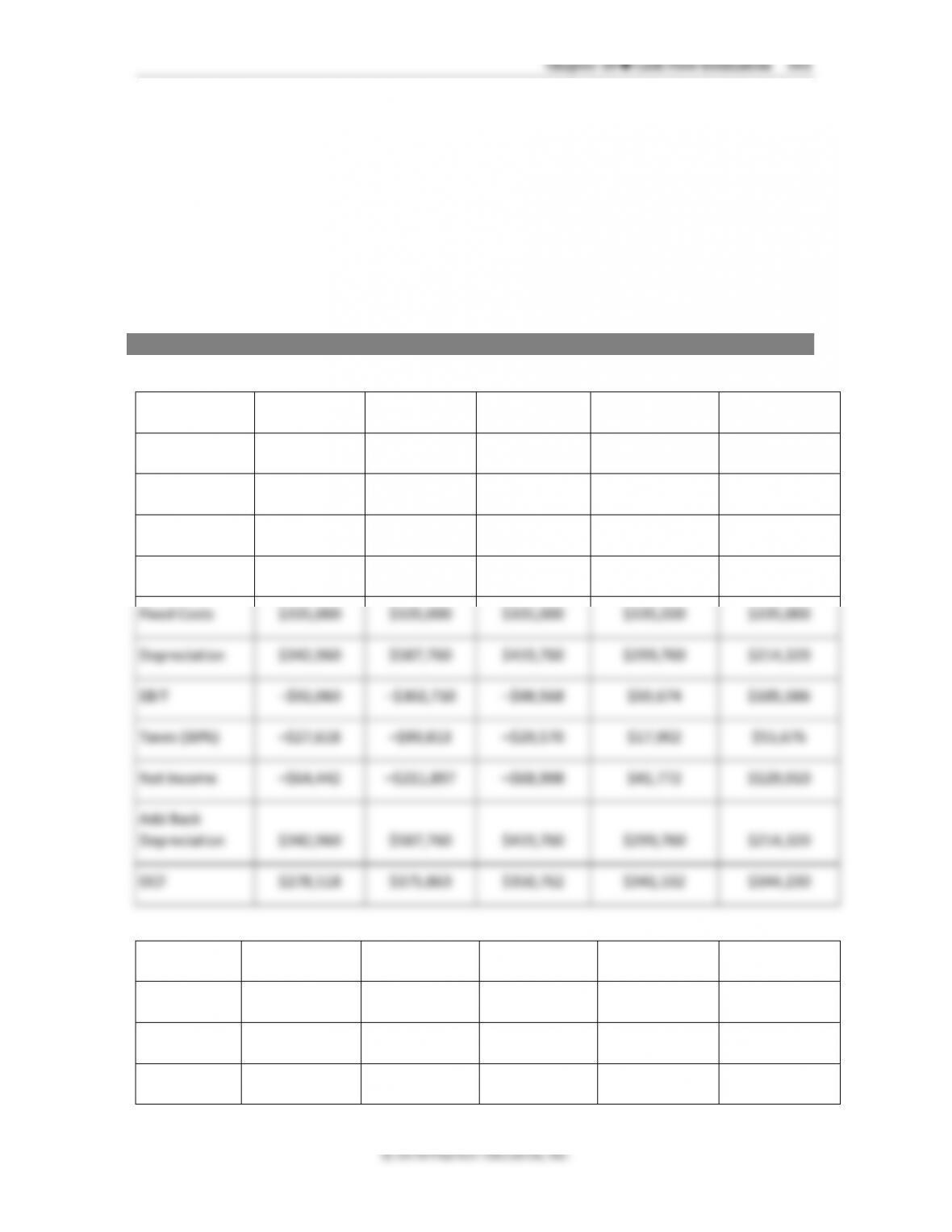

Revenue is Unit Sales × Price per Unit

COGS is Revenue × 0.62

Depreciation is as follows:

Year one $1,400,000 × 0.1429 = $200,060

Year two $1,400,000 × 0.2449 = $342,860

Year three $1,400,000 × 0.1749 = $244,860

Year four $1,400,000 × 0.1249 = $174,860

Year five $1,400,000 × 0.0893 = $125,020

Taxes are EBIT × 0.30

Net Income is EBIT – Taxes

OCF is Net Income + Depreciation

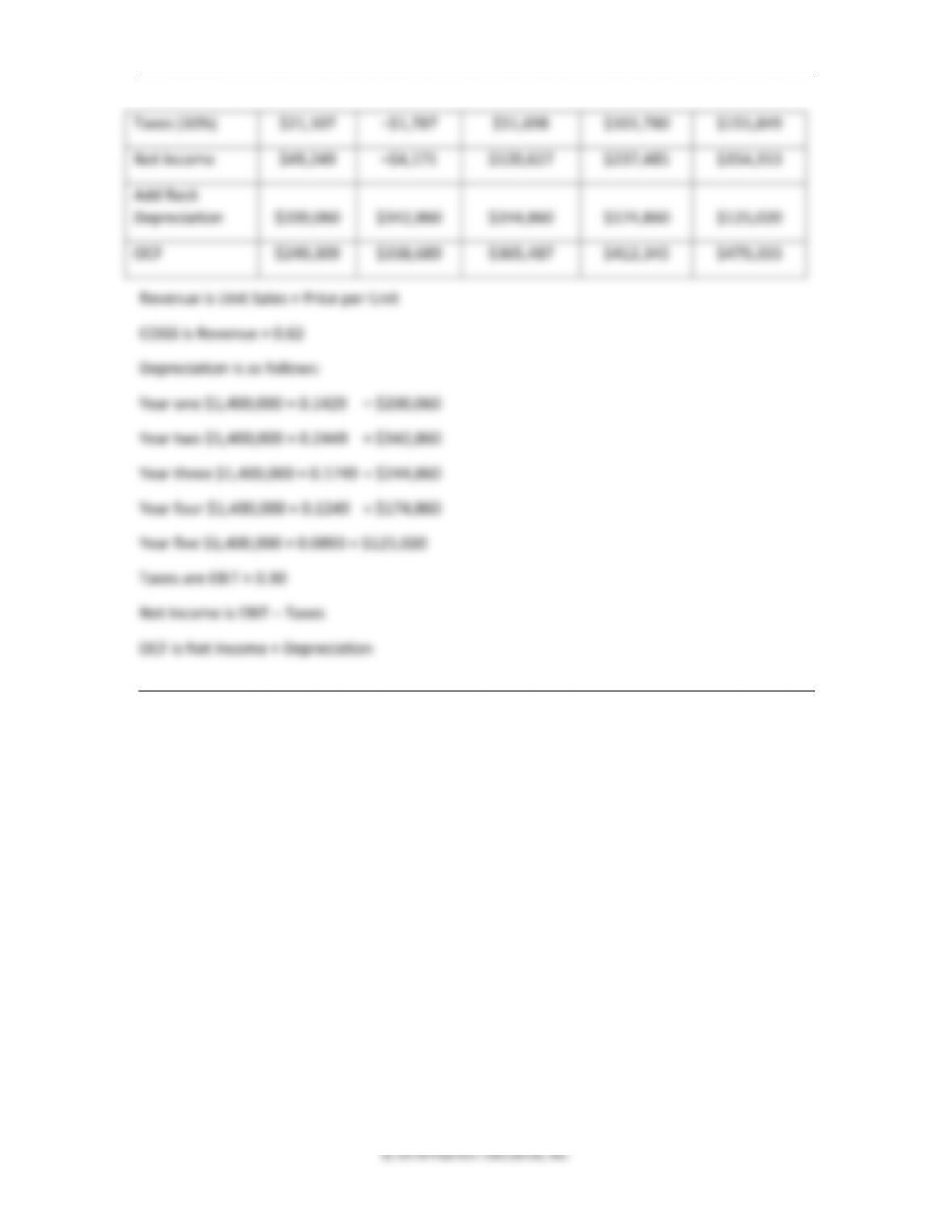

362 Brooks ◼ Financial Management: Core Concepts, 4e

COGS

$950,588

$1,005,995

$1,064,625

$1,126,679

$1,192,350

Fixed Costs

$335,000

$335,000

$335,000

$335,000

$335,000

Depreciation

$214,320

$214,320

$106,800

$0

$0

EBIT

$228,433

$273,766

$429,257

$586,829

$640,560

Taxes (30%)

$68,530

$82,130

$128,777

$176,049

$192,168

Net Income

$159,903

$191,636

$300,480

$410,780

$448,392

Add Back

Depreciation

$214,320

$214,320

$106,800

$0

$0

OCF

$374,223

$405,956

$407,280

$410,780

$448,392

Chapter 10 ◼ Cash Flow Estimation 363

© 2018 Pearson Education, Inc.

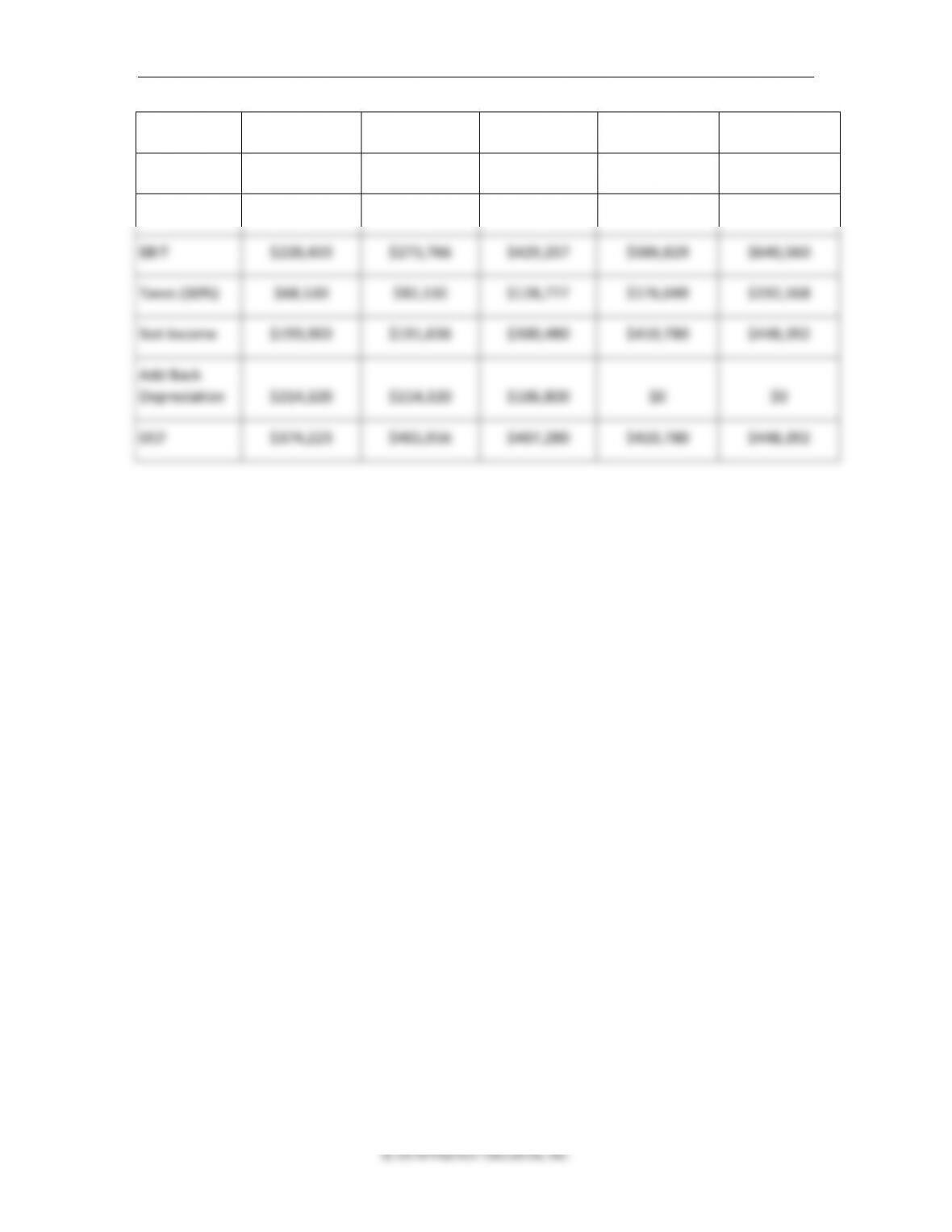

Revenue is Unit Sales × Price per Unit

COGS is Revenue × 0.55

Depreciation is as follows:

Year one $2,400,000 × 0.1429 = $342,960

Year two $2,400,000 × 0.2449 = $587,760

Year three $2,400,000 × 0.1749 = $419,760

Year four $2,400,000 × 0.1249 = $299,760

Year five $2,400,000 × 0.0893 = $214,320

Year six $2,400,000 × 0.0893 = $214,320

Year seven $2,400,000 × 0.0893 = $214,320

Year eight $2,400,000 × 0.0445 = $106,800

Taxes are EBIT × 0.30

Net Income is EBIT – Taxes

OCF is Net Income + Depreciation

17. NPV. Using the operating cash flow information from Problem 15, find the NPV of the

project for Mathews Mining if the manufacturing equipment can be sold for $80,000 at the

end of the five-year project and the cost of capital for this project is 12%. Hint: Use a

spreadsheet.

ANSWER

Find the after-tax cash flow at disposal of the equipment:

364 Brooks ◼ Financial Management: Core Concepts, 4e

© 2018 Pearson Education, Inc.

Accumulated depreciation = $1,087,660

Basis = $1,400,000 – $1,087,660 = $312,340

Loss on Disposal = $80,000 – $312,340 = –$232,340

Tax Credit on Disposal = $232,340 × 0.30 = $69,702

After-tax cash flow at disposal = $80,000 + $69,702 = $149,702

NPV = -$1,400,000 + $249,309 / (1.12) + $338,689 / (1.12)2 + $365,487 / (1.12)3 + $412,345 /

(1.12)4 + (479,333 + 149,702) / (1.12)5 = –$28,271.4

Reject the project.