PART 4

ENTERING AND WORKING IN INTERNATIONAL MARKETS

CHAPTER 14

FOREIGN DIRECT INVESTMENT AND COLLABORATIVE VENTURES

Instructor’s Manual by Marta Szabo White, Ph.D.

I. LECTURE STARTER/LAUNCHER

■ This chapter discusses foreign direct investment (FDI) and joint ventures. Compared

to exporting, these two foreign entry strategies are usually considered to be on the

“risky” end of the risk/return continuum.

■ Remind students that exporting is a relatively low-risk proposition with a low-level of

return. FDI, if successful, may bring high profits, but requires a high degree of control by

the focal firm, and certainly involves higher risk. Explain to students that FDI means that

a firm invests equity or capital in foreign countries to build, purchase, or acquire

production facilities, subsidiaries, sales offices, and/or other assets.

■ This is very different from exporting. Remind students that a company which exports

makes no equity investment in the foreign country: The only investment is the product

itself that is shipped, and usually the development of an independent intermediary in the

target country to handle local sales, marketing, and distribution.

■ One of the most common forms of FDI used by global companies is acquisitions, or

the purchase of already existing companies in new host country markets. In 2004, the

worldwide value of cross-national M&A activity was just under $2 trillion, compared to

$833 billion in 2003, and in 2014, more than 220 cross-border investments/acquisitions

valued at over $1 billion each. Historically, United States firms have accounted for

around half of global M&A activity, while European firms accounted for about one-third.

However, Europe’s share as a percentage of global M&A activity has been growing, and

today Europe’s share of global M&A activity is approaching one half.

■ Ask students why this is occurring. Ask students why we might expect to see more

European firms participate in FDI. You might suggest that the formerly fragmented

European national economies now realize the value of creating a true, single European

market.

■ Most recently, emerging market firms from such countries as China, India, and Russia

have been active in foreign direct investment. For example, the Russian firm LukOil

owns several hundred gas stations in the United States. In 2015, Anheuser-Busch

InBev acquired SABMiller for nearly $106 billion to create the world’s largest brewer,

with operations in more than 80 countries. In 2005, the Mexican cement company

CEMEX SA de CV made the largest acquisition ever by a Latin American company by

purchasing England-based RMC Group PLC for nearly $6 billion in cash. Meanwhile the

global economy is focusing much attention outside the U.S. In 2002, China by-passed

the U.S. and became the number one recipient of global FDI.

II. LEARNING OBJECTIVES AND THE OPENING VIGNETTE

LEARNING OBJECTIVES

After studying this chapter, students should be able to:

14.1 Understand international investment and collaboration.

14.2 Describe the characteristics of foreign direct investment.

14.3 Explain the motives for FDI and collaborative ventures.

14.4 Identify the types of foreign direct investment.

14.5 Understand international collaborative ventures.

14.6 Discuss the experience of retailers in foreign markets.

Key Themes

■ In this chapter, there are six themes:

[1] International investment and collaboration

[2] Characteristics of foreign direct investment

[3] Motives for FDI and collaborative ventures

[4] Types of foreign direct investment

[5] International collaborative ventures

[6] The experience of retailers in foreign markets

■ This chapter, the nature of FDI and collaborative ventures are explored

■ The drivers underlying the entry strategies are examined.

■ Several companies engaged in FDI, as well as best practices for investment and

partnering success are highlighted.

■ Retailers, a distinctive category of foreign investors in the services sector, are also

discussed.

■ This chapter is centered on four principal themes.

■ The first is an organizing framework for foreign market entry strategies. It discusses

control issues, resource commitment and flexibility as the variables for this framework.

■ The second theme is FDI. The authors discuss mergers and acquisitions as well as

international collaborative ventures, or joint ventures.

The authors classify FDI activities as follows:

■ Form of FDI- greenfield versus mergers and acquisitions.

■ Nature of ownership- wholly owned versus joint venture.

■ Level of integration- horizontal versus vertical.

■ The third theme is a discussion of motives for FDI and joint ventures.

■ The fourth theme is a discussion about the experience of retailers with foreign market

entry. This is an innovative section of this chapter as few texts address the challenges of

retailers in international business.

Teaching Tips

■ Ask students to review the principal entry strategies for internationalization. They

should name exporting, global sourcing, agency agreements such as licensing and

franchising, and FDI, including joint ventures and wholly owned subsidiaries. Ask

students to analyze which entry methods might be the most risky and why; and which

might bring the highest level of return or profits and why. Then, add a third variable

called control. Ask students which entry mode provides the company with the highest

level of control. Remind them that the highest level of control requires the highest level

of resource commitment from the company as well.

■ Discuss some examples of FDI. The textbook provides many, but consult recent

issues of the Financial Times or Business Week to find out the latest foreign equity

investments by global firms around the world. Choose one industry, for example, retail

general merchandise or retail supermarkets. Ask students to research, using Mergent

Online or other databases, to find out which companies compete globally in this

industry. U.S. firms include are Walmart and Target, U.K. firms include Tesco, French

firms include Carrefour, and German firms include Aldi. Supply articles or ask students

to research these companies to find out how they have tried to expand internationally.

■ Several international retailers including Walmart have expanded by acquiring national

firms. For example, Walmart acquired several underperforming German retail

organizations to build their business in that country. One reason for this approach is

was because German regulations did not permit Walmart or any other retailer to build

new hypermarket retail space. Unfortunately Walmart was not successful for several

reasons, but the case illustrates an interesting pattern of FDI by acquisition.

Commentary on the Opening Vignette:

HUAWEI’S INVESTMENTS IN AFRICA

Key message

■ The key message in this vignette is the transformation of a historically disadvantaged

continent to becoming a recent target of serious FDI.

■ With a population just over one billion, Africa is the world’s second most populous

continent.

■ Africa is characterized by:

◘ Unstable governments

◘ Poor economic conditions

◘ Poverty- most in sub-Saharan Africa live on less than 2 dollars per day

■ Recently, however, Africa has been growing economically in part due to increased

investment from abroad.

■ Targeted investments:

◘ Extractive industries: Petroleum and Mining

◘ High-value industries: Textiles and Telecommunications

● 85% of citizens own a cell phone in Ghana, Kenya, and South Africa

● 90% of citizens own a cell phone in the United States

■ Huawei Technologies is China’s largest telecommunications equipment manufacturer

and a key player in African FDI.

■ Huawei is China’s largest telecommunications equipment manufacturer, with annual

revenues of $32 billion, employing more than 140,000 people, including 7000 in Africa.

■ Despite challenges, Huawei’s profitable operations have leveraged economies of

scale, inexpensive labor, and numerous other advantages to keep costs low.

■ China is playing a key role by financing and providing needed development expertise.

Uniqueness of the situation described

■ African demand for mobile communications is surpassing many advanced economies.

■ Efficient operations allow Huawei to price its cell phones lower than Ericsson, Nokia,

and other competitors.

■ The ability of Chinese firms to operate profitably in poor countries is perhaps the main

reason China’s companies are outpacing firms from Europe, Japan, and North America

in expanding their presence in Africa.

■ Chinese investment in African telecommunications has fostered entrepreneurship and

created thousands of jobs.

■ In many ways, telecom infrastructure is the backbone of national economic activity.

■ Infrastructure investments contribute directly to economic development, and indirectly

by allowing businesses to interact in ways that foster synergies and commercial activity.

■ The expansion of cell networks allows Africans, many of whom live in isolated areas,

to find jobs and interact with important contacts.

■ Connecting to the Internet further enhances commercial growth.

■ As manufacturing costs in China rise and the African middle class expands; Chinese

firms will likely invest much more in Africa.

■ Various African countries are streamlining regulations and creating business-friendly

environments, increasing their attractiveness for more FDI.

Classroom discussion

■ Ask students to think about Raymond Vernon’s theory of the International Product Life

Cycle (Chapter 5), which is brought to life in this vignette, except that it is the life cycle

of FDI, not products; and leapfrogging concerns labor and technology to a lesser extent.

HIGHLIGHTED PORTION IS A RECAP FROM CHAPTER 5:

■ In a 1966 article published in the Quarterly Journal of Economics, “International

Investment and International Trade in the Product Cycle”, Harvard Professor Raymond

Vernon described the evolutionary process that occurs in the development and diffusion

of products to global markets.

■ Vernon built upon Ricardo’s comparative advantage, which argues that the highest

added value dictates labor specialization, and integrated this with the product life cycle

[introduction, growth, maturity, and decline] to explain dynamic trade patterns.

■ The International Product Life Cycle theory [IPLC] consists of three stages of

evolution: introduction, maturity, and standardization. See Exhibit 5.3

■ In the Introduction stage, a new product originates in an advanced economy with

abundant capital, specialized labor, R&D capabilities, and abundant, high-income

consumers who are willing to try new products, which are often expensive. It enjoys a

temporary monopoly.

■ In the Maturity phase, innovating country firms will engage in mass production and

seek export markets to other advanced economies.

■ As its production becomes more routine and the innovator’s monopoly power

dissipates, foreign firms are prompted to produce the standardized product which by

now earns only a narrow profit margin. Competition intensifies and export orders begin

to come from lower-income countries.

■ In the Standardization phase, knowledge capital has disseminated and mass

production is the dominant activity. Production shifts to low-income countries where the

imitators enjoy a competitive advantage by using cheaper inputs and low-cost labor to

serve export markets worldwide.

■ By now, the original innovating country may be a net importer of the product. It and

other advanced economies become saturated with imports of the good from developing

economies.

■ In effect, exporting the product has caused its underlying technology to become

widely known (knowledge transfer) and standardized around the world.

■ Early in the evolution of a product, manufacturing requires highly-skilled knowledge

workers in R&D.

■ When the product becomes standardized, mass production is employed, requiring

access to less expensive raw materials and low-cost labor.

■ As a product evolves through its international product life cycle, comparative

advantage in its production shifts from country to country.

■ Learning Point: The IPLC illustrates that national advantages are elusive; they do

not last forever. Firms worldwide are continuously creating new products and others are

constantly imitating them. The product cycle is continually beginning and ending.

■ Model Assumption: Vernon assumed the product diffusion process occurs slowly

enough to generate temporary differences between countries in their access and use of

new technologies. Not true.

■ Globalization and technology have shortened the IPLC from innovation to maturity,

and standardization, which explains the rapid spread of new consumer electronics such

as digital assistants and cell phones around the world.

■ Technological leapfrogging remains prevalent. Emerging market consumers are eager

to adopt new technologies as soon as they become available.

■ In this vignette, the highest added value dictates FDI, and if we integrate the IPLC

with this, then the movement of FDI from advanced to emerging to developing countries

is explained. This is precisely why Africa has become the focus of FDI. It promises high

added value, with inexpensive labor.

■ Moreover, FDI leapfrogging from one country to the next is further complicated by the

fact that initially only advanced countries engaged in FDI, now emerging countries are

players as well, with developing countries next on the horizon.

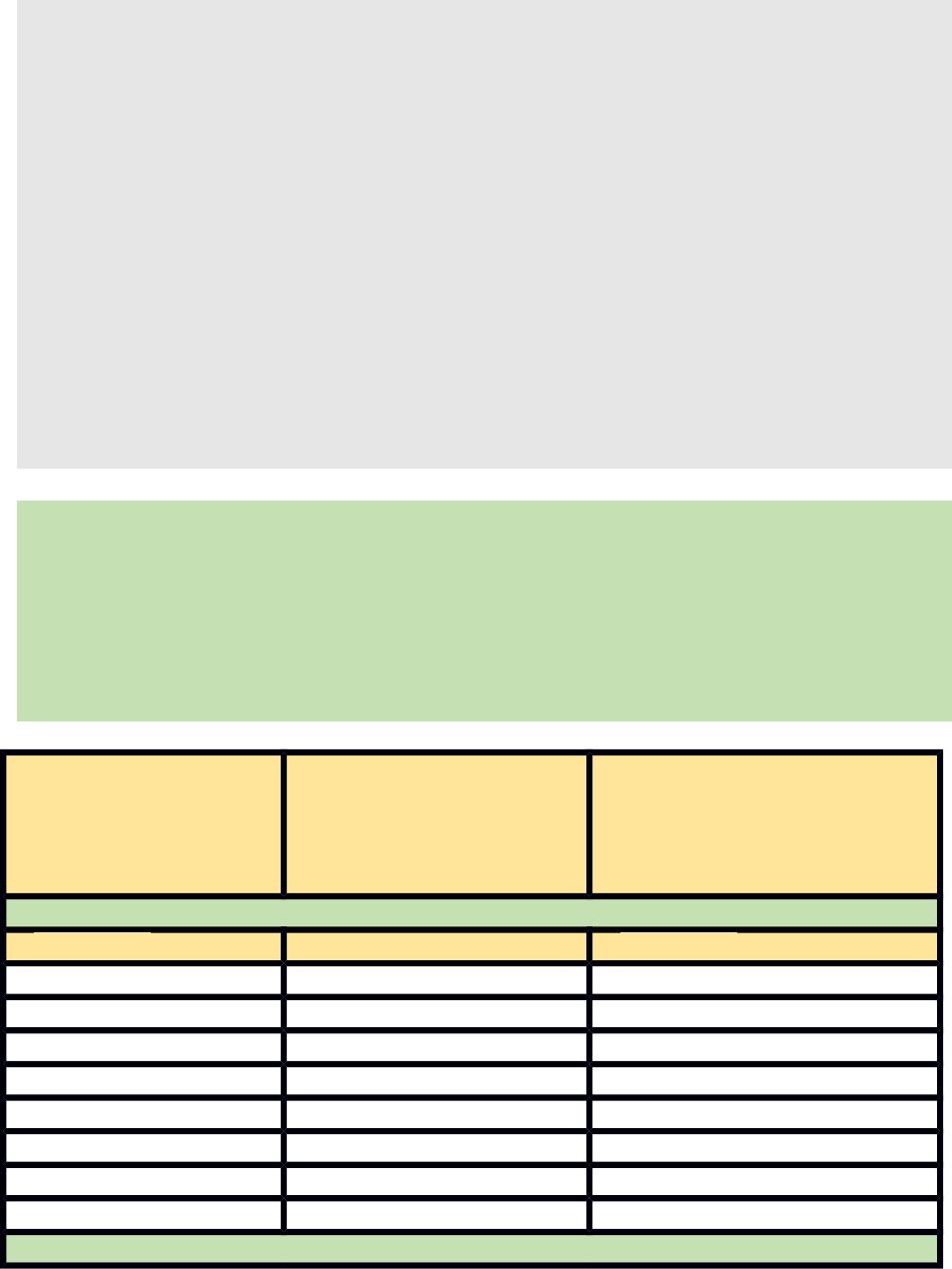

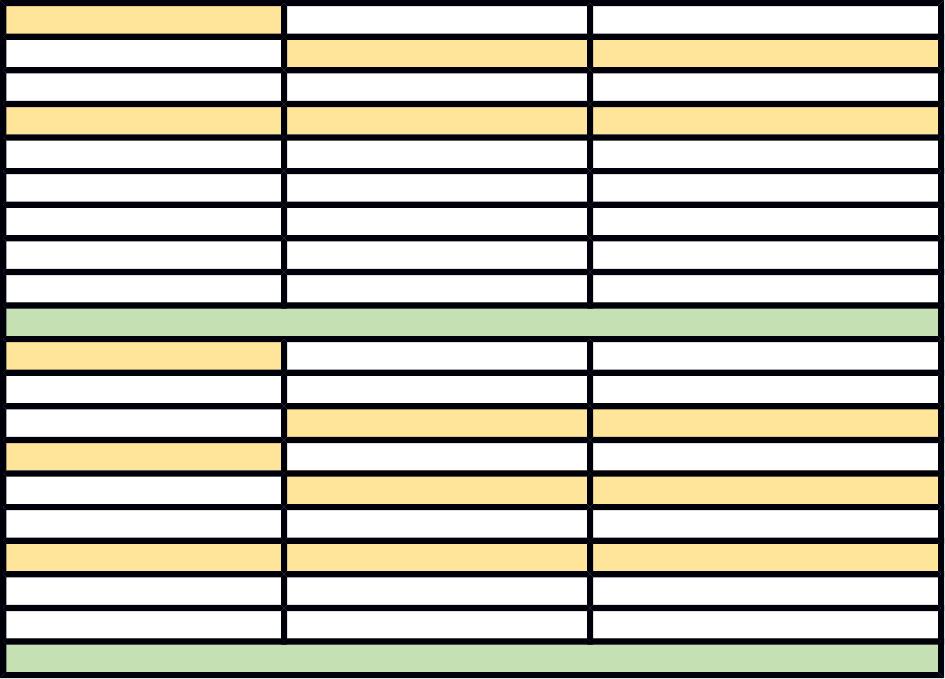

INITIATORS OF FDI

ACCORDING TO

ECONOMIC

DEVELOPMENT

STAGE

LIFE CYCLE STAGE RECIPIENTS OF FDI

FDI STAGE 1

ADVANCED INTRODUCTION ADVANCED

MATURITY

STANDARDIZATION

EMERGING INTRODUCTION

MATURITY

STANDARDIZATION

DEVELOPING INTRODUCTION

MATURITY

STANDARDIZATION

FDI STAGE 2

ADVANCED INTRODUCTION

MATURITY ADVANCED & EMERGING

STANDARDIZATION

EMERGING INTRODUCTION EMERGING

MATURITY

STANDARDIZATION

DEVELOPING INTRODUCTION

MATURITY

STANDARDIZATION

FDI STAGE 3

ADVANCED INTRODUCTION

MATURITY

STANDARDIZATION EMERGING & DEVELOPING

EMERGING INTRODUCTION

MATURITY DEVELOPING

STANDARDIZATION

DEVELOPING INTRODUCTION NEXT – DEVELOPING

MATURITY

STANDARDIZATION

The IPLC theory is linked to the evolution of FDI as exemplified in this vignette:

■ Having established a presence in Africa in the 1990s, Huawei has invested more

than $1.5 billion in Africa, with this region accounting for about 12% of Huawei’s annual

revenue.

■ Uganda- Huawei developed a government data center and several large-scale

projects connecting agencies to a central network.

■ Ghana- Huawei invested more than $100 million to develop telecom facilities.

■ Northern Africa- Huawei entered a joint venture with ZTE Corporation to expand

mobile networks in nine cities and build 800,000 phone lines.

■ Algeria- Huawei established a mobile network to complement a cell network

completed by ZTE.

■ 2015- Huawei and Global Marine Systems formed a joint venture to develop

telecommunications infrastructure in Africa.

■ China’s Africa investments benefit not only Africans, but also European and U.S.

firms.

■ These companies benefit from the roads, railways, telephony, energy systems, and

other infrastructure that Chinese firms have helped to develop.