CHAPTER 8

PRICING AND OUTPUT DECISIONS:

PERFECT COMPETITION AND MONOPOLY

QUESTIONS

1. All four of the characteristics listed in Figure 8.1A of Chapter 8 are important to ensuring that

a. Large number of relatively small sellers: This factor provides buyers with a considerable

number of easily available alternatives. If one seller tries to raise its price, consumers can turn

to the many others who would be willing to sell a product at the going market price. The

b. Standardized product: This ensures that the many alternative sellers mentioned above are

c. Complete information about market price: One of the many small sellers could get away with

d. Freedom of entry and exit: This prevents any possibility of sellers exercising some degree of

2. This question is answered in 1.d. above.

3. Although there are very few “perfectly competitive” markets, the basic short run and long run

Copyright © 2014 Pearson Education, Inc.

Pricing and Output Decisions: Perfect Competition and Monopoly 76

a. The increase in demand caused an increase in profits of those selling the product.

b. This prompted the entry of many new sellers, including IBM. (At one point in the early 1980s,

c. The increase in supply (particularly by the direct marketing “800 number” companies such as

Instructors may want to expand this point by discussing the factors that were more related to

4. From the standpoint of an individual, price-taking firm in a perfectly competitive market, the

5. The more alternatives (or substitute products) available for consumers, the more sensitive they will

6. a. According to economic theory, new firms enter the market when they see that firms already in

b. We believe that there is much truth in this statement. One of the risks that an entrepreneur takes

7. P>AVC is the per unit version of TR>TVC. When TR>TVC, the firm is earning a positive

8. “Normal” is akin to equilibrium in economic theory. When a firm earns a profit (i.e., a non-zero

9. A popular measure of financial performance being used by an increasing number of American firms

10. Perfectly competitive firms are price takers. This means that they can sell as much or as little as

Copyright © 2014 Pearson Education, Inc.

Pricing and Output Decisions: Perfect Competition and Monopoly 77

11. Revenue is maximized when marginal revenue becomes zero. Profit is maximized when MR = MC.

12. Here are three examples:

(1) Intel: Should we go into the “data farm”(or “farm business”)? In mid 1999, they said yes.

13. All the markets with the exception of the oil market would be considered pretty close to if not

14. Because of the long approval cycle for a new drug (up to 10 years) and the high cost, the patent

PROBLEMS

1. Given the market price and its cost structure, this firm will be incurring a loss. However, this loss

will not be as large as its fixed cost. In other words, this firm will have a positive contribution

2. a. FALSE Not if its loss is less than its fixed cost. See explanation of problem 1.

b. FALSE Even a pure monopoly has to consider the possibility of demand falling below

Pricing and Output Decisions: Perfect Competition and Monopoly 78

e. TRUE If P>AVC but P<AC, then the company will cover some of its fixed costs; thus,

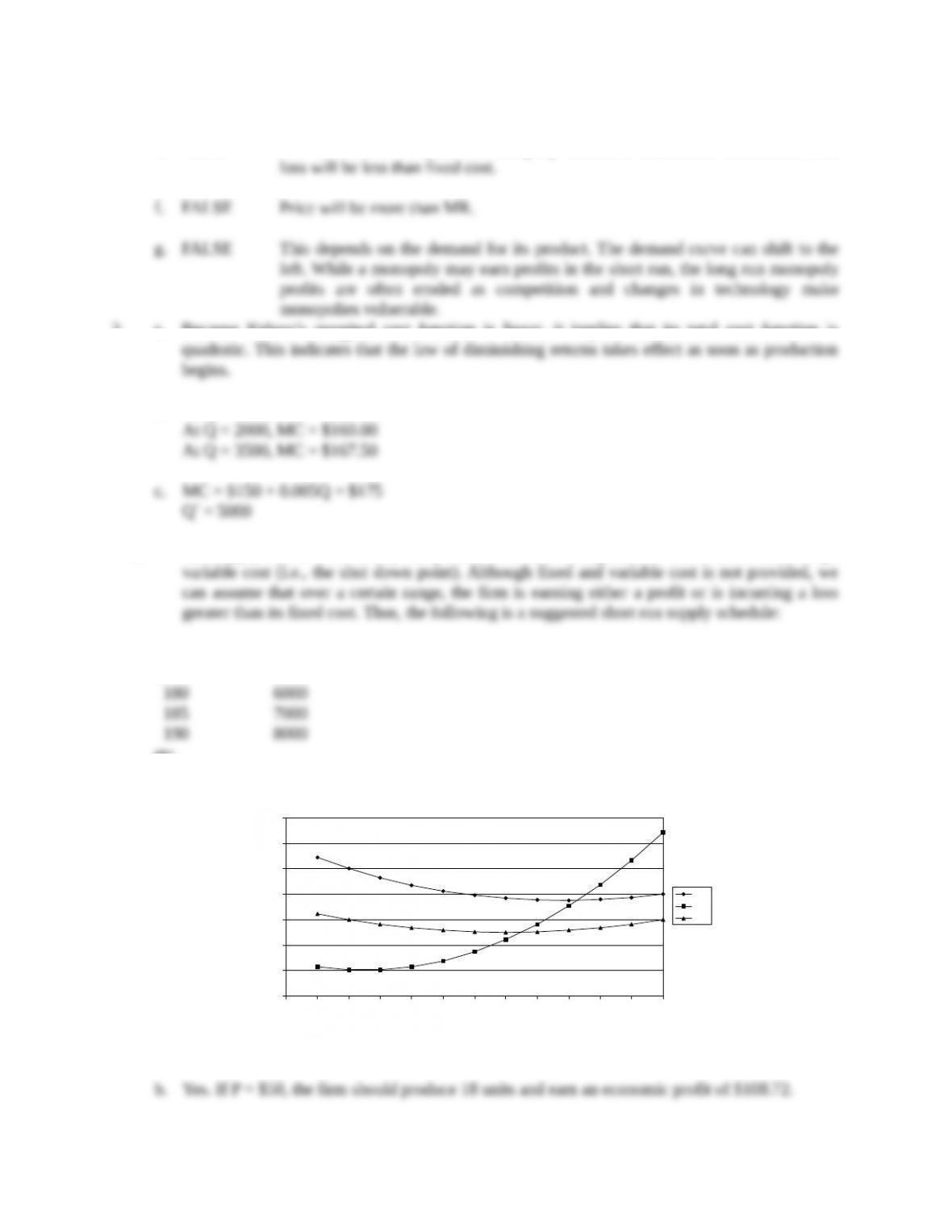

3. a. Because Kelson’s marginal cost function is linear, it implies that its total cost function is

b. At Q = 1500, MC = $157.50

d. The supply curve is essentially the portion of a firm’s marginal cost curve above its average

P Q

$175 5000

etc.

4. a.

Figure 8.1

Copyright © 2014 Pearson Education, Inc.

25

30

35

40

45

50

55

60

8 9 10 11 12 13 14 15 16 17 18 19 20

Q (Thousands)

$

AC

MC

AVC

Pricing and Output Decisions: Perfect Competition and Monopoly 79

c. If P = $35, then the best that the firm could do by operating would be to produce 14 units (i.e.,

Copyright © 2014 Pearson Education, Inc.

Pricing and Output Decisions: Perfect Competition and Monopoly 80

5. a. P* = $1090.

b. The above price would enable a firm to earn a maximum amount of total profit in the short run.

c. The firm would want to consider setting a price lower than $1090 if it wanted to increase its

There may be other reasons for lowering the price. For example, the firm may wish to use the

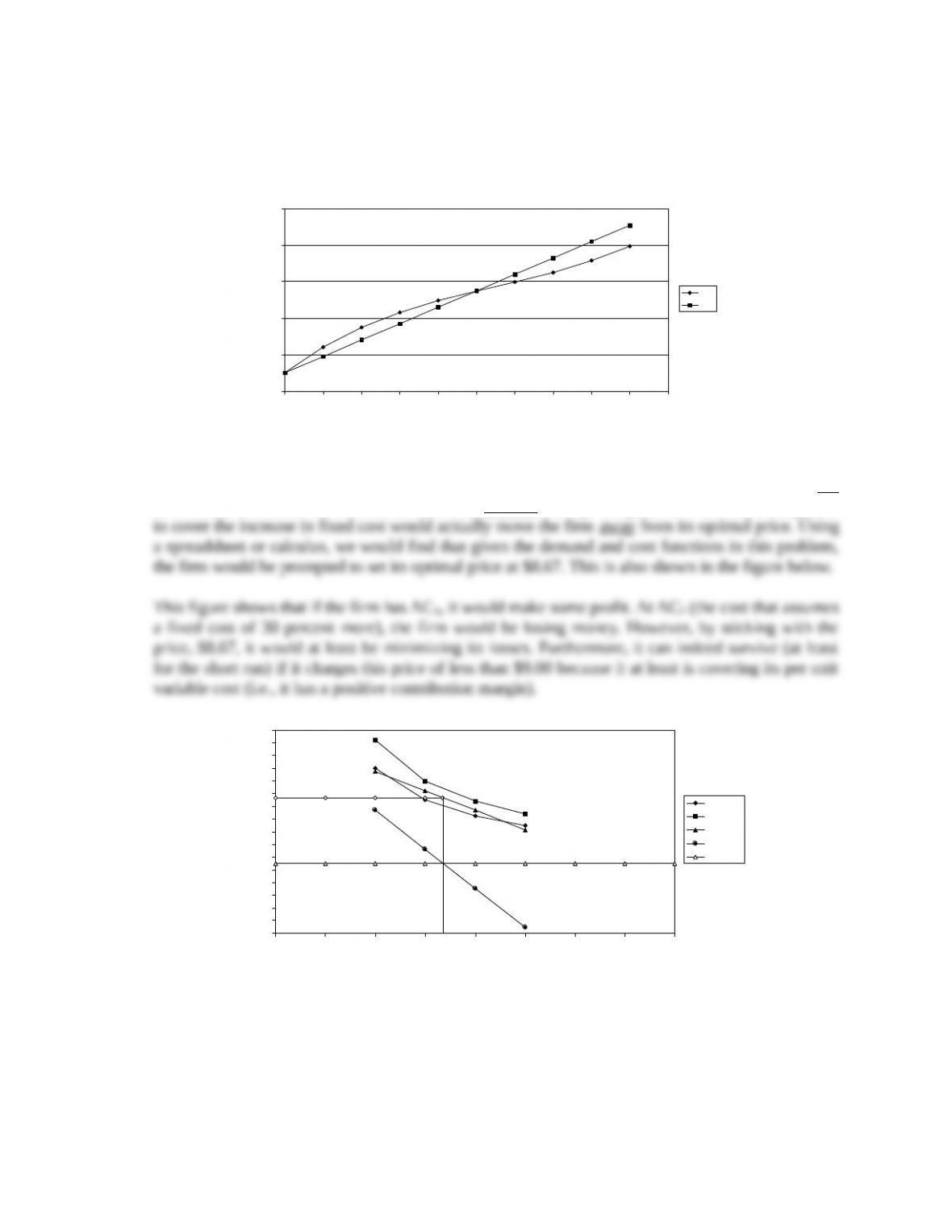

6. a. To solve this problem, we find the MR and MC functions, set them equal to each other, and

solve for the optimal Q. Using this Q, we then find the optimal P.

P = 853.37 – 0.06Q

This price can then be rounded to a more even number (e.g., $500).

b.

Figure 8.2

Copyright © 2014 Pearson Education, Inc.

3000 4000 5000 6000 7000

Q

$

D

MR

AC

AVC

MC

$512.36 = P*

Q* =

5683.47

0

Pricing and Output Decisions: Perfect Competition and Monopoly 81

7. a. To answer this question, we illustrate how Excel software can help to answer this question.

Using the online software provided for users of this text, we arrive at the following:

Quantity Price

Total

Revenue

Total

Fixed

Cost

Total

Variable

Cost

Total

Cost

Total

Profit

0 100 0 50 0 50.00 -50.00

The optimal price is $60 and the optimal quantity is 5.

We can be more precise if we employ calculus to find the short run profit maximizing price. Let

TR = 100Q – 8Q2

Using the formula for finding the roots of a quadratic equation, we arrive at:

b. In order to find the price that maximizes total revenue, we can use the spreadsheet above. We

see total revenue is maximized at a price of $52. Using calculus simply involves taking the first

Copyright © 2014 Pearson Education, Inc.

Pricing and Output Decisions: Perfect Competition and Monopoly 82

c. If the firm wanted to use a linear approximation of the cubic equation, it might simply derive

the linear equation in the manner shown in the figure below.

Figure 8.3

8. If we assume that the firm uses the MR = MC rule to determine its optimal price, then it should not

raise its price because the increase in fixed cost does not change marginal cost. In fact, raising price

Figure 8.4

Copyright © 2014 Pearson Education, Inc.

0

100

200

300

400

500

0 1 2 3 4 5 6 7 8 9 10

Q

$

TC1

TC2

–2

–1

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

0 10 20 30 40 50 60 70 80

Q

$

AC1

AC2

D

MR

AVC=MC

P

1*

= 8.67

Pricing and Output Decisions: Perfect Competition and Monopoly 83

9. Setting the derivative of the total cost function equal to the derivative of the total revenue function

and solving for Q yields the same result as setting the total profit function equal to 0 and solving for

Q.

TR = 170Q – 5Q2

Copyright © 2014 Pearson Education, Inc.

Pricing and Output Decisions: Perfect Competition and Monopoly 84

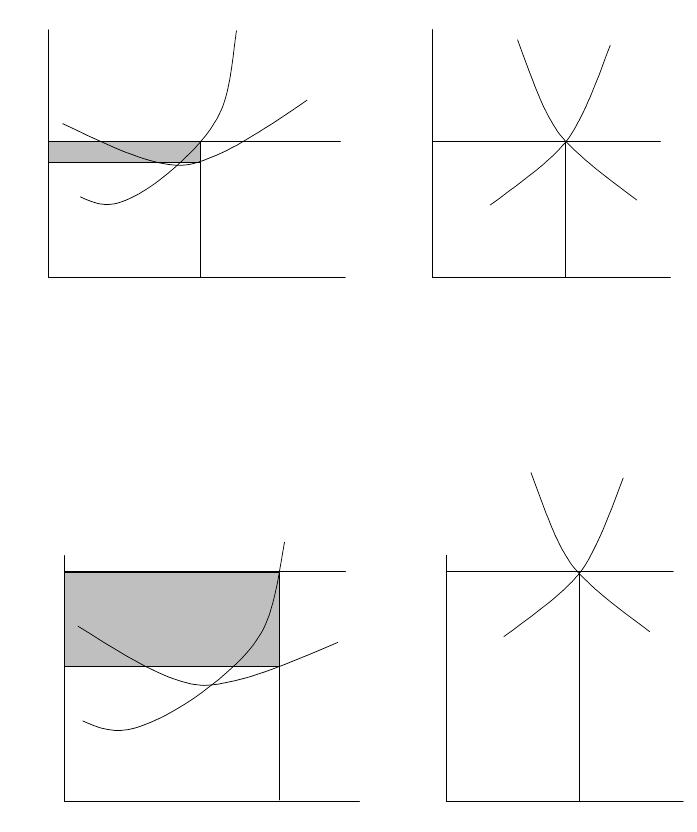

10. A “good” firm

Figure 8.5

Given market price P1, the firm is able to keep its cost structure low enough so that P = MC above AC.

A “lucky” firm

Figure 8.6

Given its cost structure, the firm is able to make an economic profit because the market price is so high.

Copyright © 2014 Pearson Education, Inc.

P

1

AC

MC

Q

1

D

S

P

1

Q

D

S

P1

Q

P1

AC

MC

Q1