CHAPTER 7 AND APPENDICES

THE THEORY AND ESTIMATION OF COST

QUESTIONS

1. a. Sunk cost is a cost that is incurred in the past that is not affected by a current decision (except

b. Fixed cost is a cost that does not vary with the level of business activity.

c. Incremental cost is the cost associated with a particular activity. Marginal cost is the per unit

d. Opportunity cost is the amount forgone when choosing one activity over the next best

2. Incremental cost, variable cost, and marginal cost are considered “relevant costs” because they are

Opportunity cost can also be considered a relevant cost, but it depends on the situation. For

example, in the case of the decision to quit one’s job to pursue an academic degree full time, the

3. The firm’s short run cost function can be considered somewhat akin to a “mirror image” of its

production function. As reflected in Figure 7.1 of the chapter, when its marginal product increases,

Copyright © 2014 Pearson Education, Inc.

The Theory and Estimation of Cost 57

4. This statement is true. As indicated in the question above, the law of diminishing returns causes a

5. From the standpoint of the supply side of the market, the short run is time enough only for those

6. Economies of scale is the decrease in a firm’s unit cost of production as it increases all of its inputs

The main determinants of economies of scale are summarized in Table 7.4 of the chapter.

7. Diseconomies of scale is the increase in a firm’s unit cost of production as it increases all of its

inputs. The main determinants of diseconomies of scale are also listed in Table 8.4. Perhaps the

8. Economies of scope refers to the reduction in unit cost resulting from a firm’s production of two or

more products. This type of cost savings is related to economies of scale to the extent that a firm of

9. The learning curve indicates unit costs on the basis of an accumulation of output. The typical cost

10. As explained in the text, the experience curve is often considered synonymous with the learning

11. After reading the section “The Long-Run Average Cost Curve as the Envelope of Short-Run

Copyright © 2014 Pearson Education, Inc.

The Theory and Estimation of Cost 58

12. Accounting statements, as a rule, do not differentiate between costs and expenses which are

relevant to decision making and those that are not. Included in cost of goods sold can be such items

as fixed overhead and depreciation which is time-related (and not production-related). Thus, not all

13. This person is referring to the spreading out of fixed cost in as short-run situation. Economies of

14. In the economic short-run, at least one factor remains fixed. In estimating such cost functions,

economists assume that capital is fixed while labor is the variable factor. Thus, the data used in

this regression analysis must cover observations where quantities produced and costs change

15.

Some of the problems encountered and for which adjustments must be sought are the following:

a. Prices of labor, materials and other variable factors may change over the time period, and must

be adjusted to be consistent.

15. In the economic long run, there are no fixed costs. The economist usually assumes that changes in

the size of plant can occur. So, the regression method generally used is the cross-sectional analysis,

where observations on output and costs are taken from different plants at one point of time.

Copyright © 2014 Pearson Education, Inc.

The Theory and Estimation of Cost 59

a. Wage rates and other unit costs (e.g. utility bills) may vary from one geographical area to

b. The various plants may not be operating at an optimal level of technology. Plants in the sample

c. If the different plants in the sample belong to a different firm, there may be differences in

d. Some factors, especially labor, may receive their remuneration differently. For instance,

16. a. Engineering costs: based on data developed by experts (engineers), who estimate the optimal

b. Survivorship principle: Plants in an industry are categorized by size, and the proportion of total

Copyright © 2014 Pearson Education, Inc.

The Theory and Estimation of Cost 60

PROBLEMS

1.

Q TC TFC TVC AC AF AVC MC

0 120 120 0 X X X

2. Although the numbers are fictitious, this problem is actually based on a study conducted by one of

the authors. (See Philip K. Y. Young, “Family Labor, Sacrifice, and Competition: The Case of

However, in return Mr. Lee will receive the following:

a. The long hours of work reduces the attractiveness of owning one’s own business.

b. The profits have to be shared with his wife and brother. If he takes the job, his wife and brother

c. Although the forecast is that the profits in his own business and his salary will increase at the

Copyright © 2014 Pearson Education, Inc.

The Theory and Estimation of Cost 61

Copyright © 2014 Pearson Education, Inc.

The Theory and Estimation of Cost 62

3. Instructors should have an interesting time discussing this question. We recommend that this

There is no unique answer to this question because it all depends on the assumptions that one makes

about the cost conditions. However, based on the strict criteria of relevant cost (i.e. incremental or

variable cost), we suggest that the following estimate:

Boat fuel $45

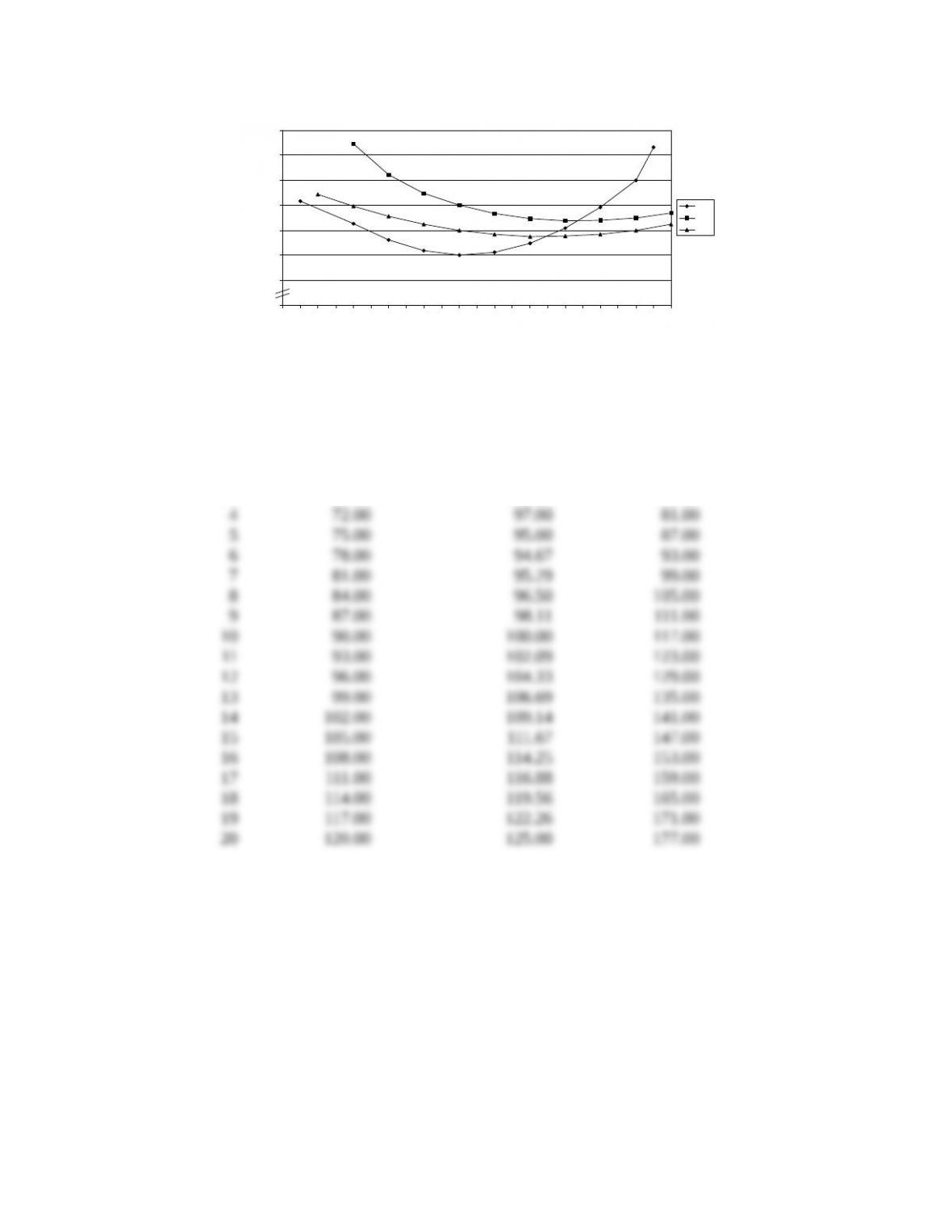

4. a.

Quantity Average Variable Cost Average Total Cost Marginal Cost

0

1 57.10 157.10 57.10

2 54.40 104.40 51.70

3 51.90 85.23 46.90

Copyright © 2014 Pearson Education, Inc.

The Theory and Estimation of Cost 63

Figure 7.1

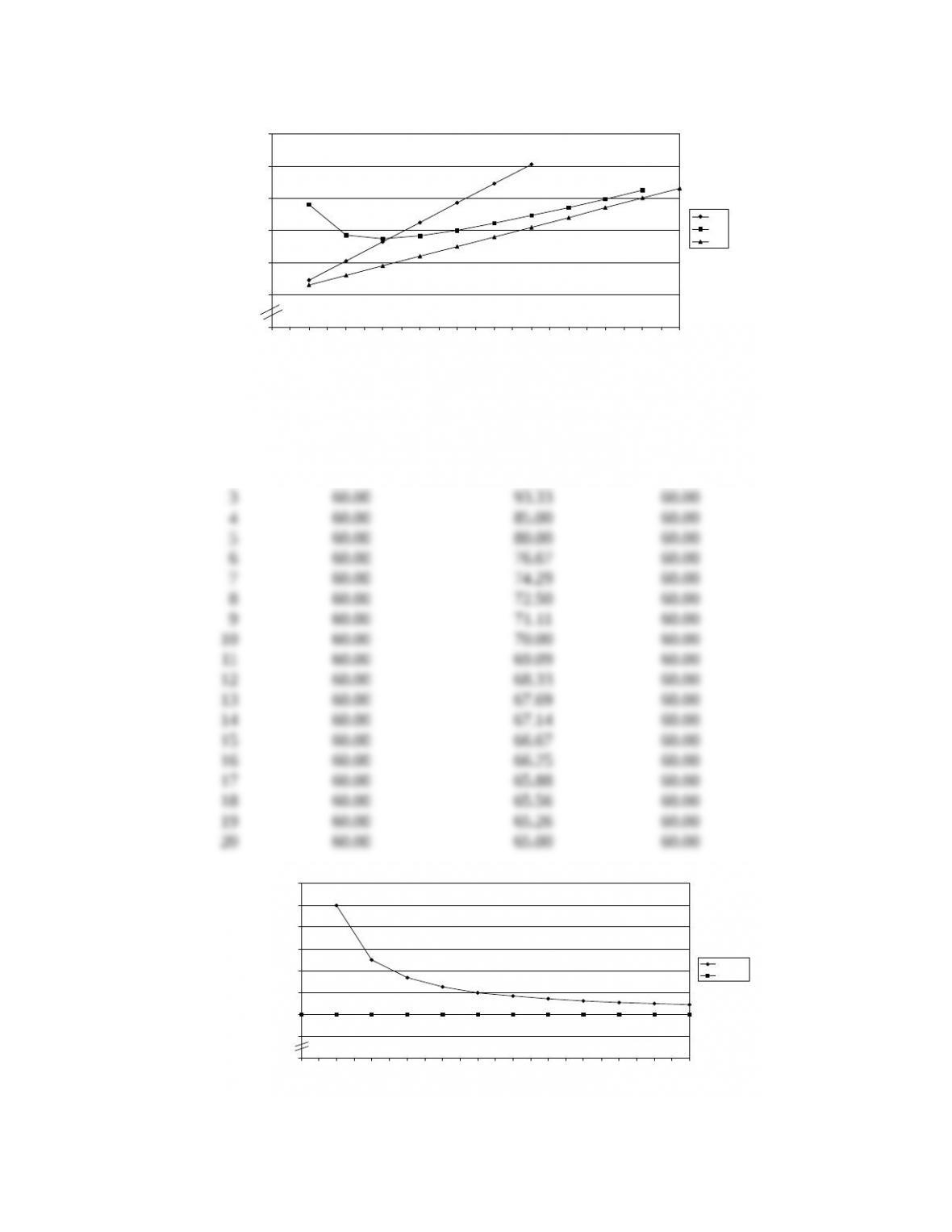

Quantity Average Variable Cost Average Total Cost Marginal Cost

0

1 63.00 163.00 63.00

2 66.00 116.00 69.00

3 69.00 102.33 75.00

Copyright © 2014 Pearson Education, Inc.

10

20

30

40

50

60

70

80

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

Q

$

MC

AC

AVC

The Theory and Estimation of Cost 64

Figure 7.2

Quantity Average Variable Cost Average Total Cost Marginal Cost

0

1 60.00 160.00 60.00

2 60.00 110.00 60.00

Figure 7.3

Copyright © 2014 Pearson Education, Inc.

40

60

80

100

120

140

160

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

Q

$

MC

ATC

AVC

40

50

60

70

80

90

100

110

120

0 2 4 6 8 10 12 14 16 18 20 22

Q

$

AC

MC=AVC

The Theory and Estimation of Cost 65

b. In the first equation, diminishing returns occurs at 10 units of output, the point at which MC

reaches its minimum point.

c. Students should simply observe how the MC intersects the AVC and AC lines at their minimum

5. a. FALSE Decision-makers should always use the replacement or current cost of raw

materials because it is considered to be relevant to the decision.

6. a. Only AC will shift downwards, because we assume that this move affects only fixed cost.

7. a. LRAC = 160 – 20Q + 1.2Q2

Copyright © 2014 Pearson Education, Inc.

The Theory and Estimation of Cost 66

b. Because of the particular functional form of the LRAC, we know that this firm experiences

Figure 7.4

8. a. This equation represents a quadratic cost curve. Total fuel cost (Y) is the dependent variable

and quantity produced (X) is the independent variable. Since the cost function includes a

b. This is a time-series analysis of the steel industry. The total cost equation shown is a straight

line. The marginal and average variable cost curves are horizontal, i.e. costs are constant. If

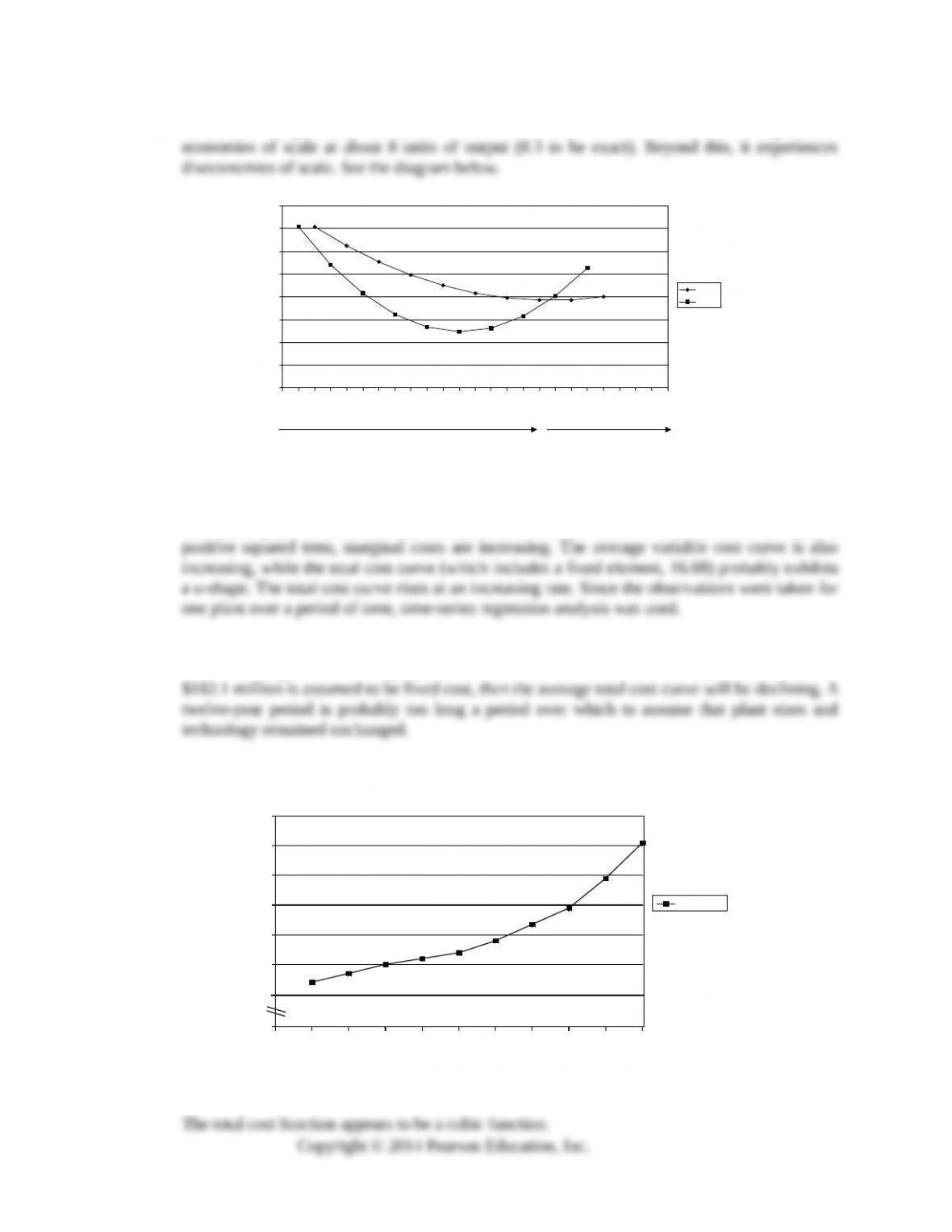

9. a.

Figure 7.5

0

20

40

60

80

100

120

140

160

0 1 2 3 4 5 6 7 8 9 10 11 12

Q

$

LRAC

LRMC

Economies of Scale Diseconomies of Scale

100

110

120

130

140

150

160

0 10 20 30 40 50 60 70 80 90 100

To tal Cost

0

TC ($)

Q

The Theory and Estimation of Cost 67

Copyright © 2014 Pearson Education, Inc.