102 SUPPLEMENT 7 CAPAC I T Y A N D CO N S T R A I N T MA N A G E M E N T

ACTIVE MODEL S7.2: Break-even Analysis

1. Use the scrollbars to determine what happens to the break-even

point as the fixed costs increase? the variable costs increase? the

selling price increases?

by 10%. In this case, if the variable costs rise by 10%, then the

BEP rises by 15%. If the price per unit increases by 10%, then

would the fixed costs have to decrease? the variable costs? How

much would the selling price have to increase?

Fixed costs, $5,000; variable costs by $1.75 from $2.25

to $.50; the selling price would need to increase by the same

S7.8 Actual (or expected) output = (Effective capacity) (Efficiency)

(Equation (S7.3))

5.5 cars 0.880 = 4.84 cars.

the maximum of 10, 6, and 8.

S7.10 Process time of each machine = 60 min/hr ÷ 4 units/hr

S7.11 Converting each capacity to a process time, Station 1 = 60

min/hr ÷ 20 units/hr = 3 min/unit (for both Machine A and

Machine B); Station 2 = 60 min/hr ÷ 5 units/hr = 12 min/unit; and

Station 3 = 60 min/hr ÷ 12 units/hr = 5 min/unit

S7.14 (a) Workstation C is the bottleneck, at 20 min/unit

(A different Part 1 can be worked on by Workstation A and

Workstation B simultaneously.)

S7.15 (a) Converting each capacity to a process time,

Sawing = Sanding = 60 min/hr ÷ 6 units/hr = 10 min/unit;

Drilling = 60 min/hr ÷ 2.4 units/hr = 25 min/unit; Welding = 60

min/hr ÷ 2 units/hr = 30 min/unit; and each Assembly = 60

140.71) = 140.71

min

S7.16 Break-even:

(8) – 50,000 (10) – 70,000

(8) 20,000 (10)

20,000 10 – 8

10,000

XX

XX

XX

X

=

+=

=

=

==

A

20,000

(a) 1,667 pizzas;

14 – 2

30,000

BEP

S7.20

X = 13,333 pizzas

S7.21 Given:

Price ( ) = $8 unit

Variable cost ( ) = $4 unit

P

V

500 2,000 units

.75 .50

F

BEPxPV

= = =

−−

104 SUPPLEMENT 7 CAPAC I T Y A N D CO N S T R A I N T MA N A G E M E N T

= = = =

−

= = =

=

$0.01

0.05

15,000 15,000

(a) $18,750

1 – 0.2

1 – 1

15,000 15,000

(b) – 0.05 – 0.01 0.04

375,000 copies

V

P

F

BEP

F

BEPxPV

S7.23 Option A: Stay as is

Option B: add new equipment

=

=

==

$

50,000 2.50 $125,000 and

37,500

1–

37,500 $125,000

1.75

1– 2.50

BEP V

P

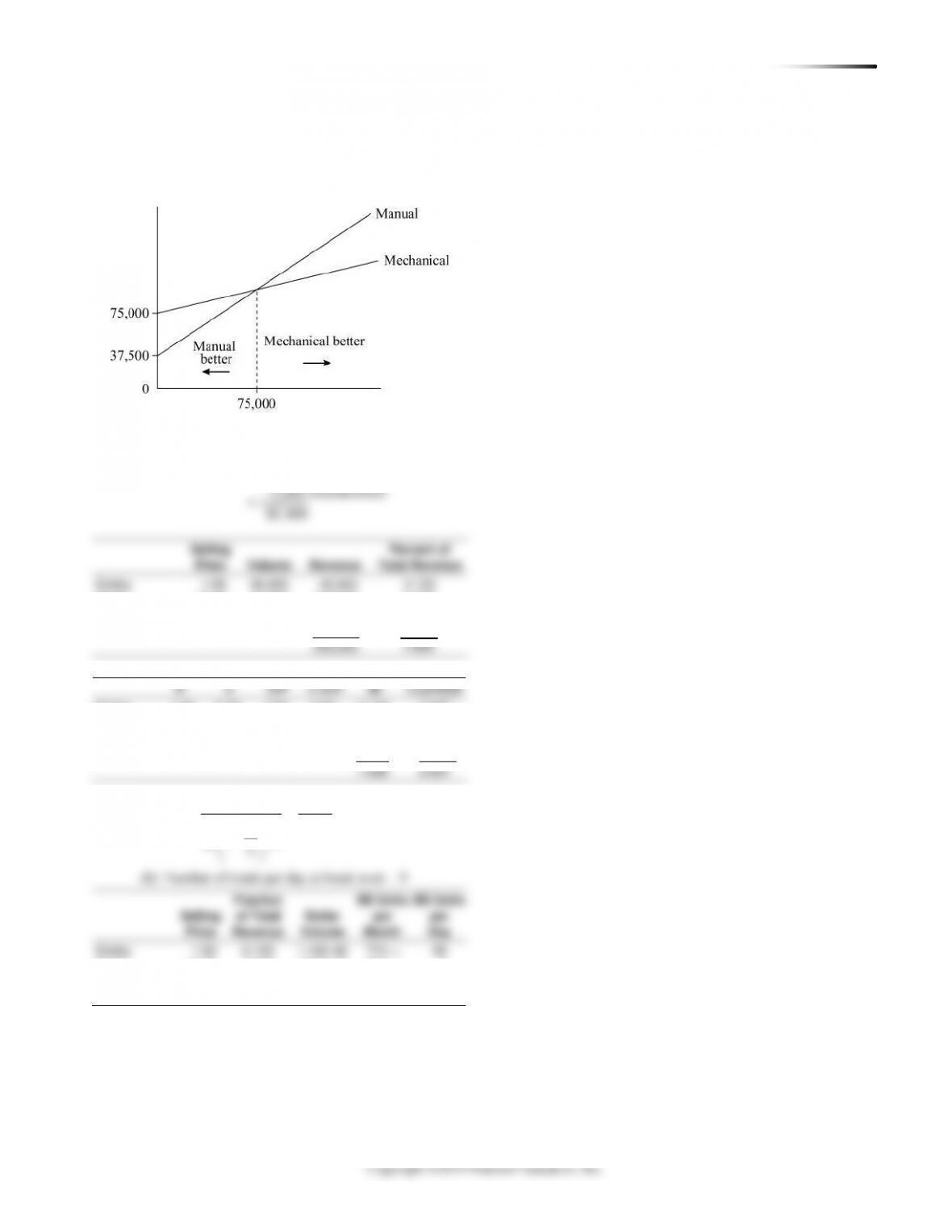

SUPPLEMENT 7 CA PA C I T Y A N D CO N S T R A I N T MA N A G E M E N T 105

(h) The manual process should be preferred over the mech-

anized process below 75,000 bags. The mechanized

process should be preferred over the manual process

above 75,000 bags.

S7.26 (a) Break-even volume:

Total fixed cost = $1,800 rent, utilities, etc.

106 SUPPLEMENT 7 CAPAC I T Y A N D CO N S T R A I N T MA N A G E M E N T

S7.27 (a) Break-even volume, where total fixed cost = labor

(at $250) + booth rental (at 5 $50) = $500.

Total sales at breakeven

(b) No. of wine servings × 25% of sales

=

at breakeven

986.19 × 0.25

= = 140.9 servings

$1.75

S7.28

Option A: EMV = (90,000 × .5) + (25,000 × .5) = 45,000 + 12,500

= $57,500

Option B: EMV = (80,000 × .4) + (70,000 × .6) = 32,000 + 42,000

= $74,000

S7.29

EMV for large line = [(Sales – Cost) × 2/3] + [(Sales – Cost) × 1/3]

= (200,000 × 2/3) + (–100,000 × 1/3) = $100,000

EMV for small line and no expansion = [(Sales – Cost) × 1/3]

+ [(Sales – Initial cost) × 2/3]

= [(300,000 – 300,000) × 1/3] + [(400,000 – 300,000) × 2/3]

= $0.0 + $66,666 = $66,666

Therefore, build a large line.

Decision tree solution:

S7.32

15

5600 5600 $1,765.35

3.17

(1 ) (1.08)

N

F

P

i

= = = =

+

or from Table S7.1:

NPV = F PVF8%, 15 = 5600 0.315 = $1,764

Item

(P)

Selling

Price

(V)

Variable

Cost

Var. Cost

Factor (%)

Total

Var. Cost

1– (V/P)

Estimated

Percent

Revenue

Contribution

Weighted

Revenue

Soft drinks

1.00

0.65

1.1

0.715

0.285

0.25

0.071

Wine

1.75

0.95

1.1

1.045

0.403

0.25

0.101

Coffee

1.00

0.30

1.1

0.330

0.670

0.30

0.201

Candy

1.00

0.30

1.1

0.330

0.670

0.20

0.134

Totals

1.00

0.507

Breakeven = TFC/wt contribution = 500/0.507 = $986.19

Now

Expense

20,000

1.000

Expense

5,000

0.893

Expense

5,000

0.797

Expense

5,000

0.712

Salvage revenue

7,000

0.712

Original cost

Excess labor per year

Maintenance per year

Salvage value

–3,750

–1,316

–1,154

–1,013

–8,900

–8,511

–5,000

Profit

1.00

–$775,000

$204,525

$185,850

$168,975

$153,675

$139,725

1

0

600

600

$545

2

0

600

600

$496

3

0

600

600

$451

4

0

600

600

$410

5

0

600

600

$373

Now

Expense

20,000

1.000

Expense

5,000

0.893

Expense

5,000

0.797

Expense

5,000

0.712

Salvage revenue

7,000

0.712

Original cost

Excess labor per year

Maintenance per year

Salvage value

–3,750

–1,316

–1,154

–1,013

–8,900

–8,511

–5,000

Profit

1.00

–$775,000

$204,525

$185,850

$168,975

$153,675

$139,725

1

0

600

600

$545

2

0

600

600

$496

3

0

600

600

$451

4

0

600

600

$410

5

0

600

600

$373

S7.33

Expense

Machine A

Machine B

Original cost

10,000

20,000

Labor per year

2,000

4,000

Maintenance per year

4,000

1,000

Salvage value

2,000

7,000

Year

Machine A

NPV Factor*

NPV

Now

Expense

10,000

1.000

–10,000

1

Expense

6,000

0.893

–5,358

2

Expense

6,000

0.797

–4,782

3

Expense

6,000

0.712

–4,272

–24,412

3

Salvage revenue

2,000

0.712

+1,424

–22,988

* NPV factor from Table S7.1.

(a) NPV of the three small ovens = –$8,511; NPV of the

two large ovens = –$5,855. Therefore, you should rec-

ommend that the firm purchase the two large ovens.

(b) The basic assumptions made with regard to the ovens

are:

◼ The ovens are of equal quality.

◼ The ovens are of equivalent production capacity.

(c) The basic assumptions made with regard to methodol-

ogy are:

◼ Future interest rates are known.

◼ Payments are made at the end of each time period.

S7.35 (a) Remember that Year 0 has no discounting.

Initial cost = $1,000,000 Yearly maintenance = $75,000

Salvage cost = $50,000 Yearly dues = $300,000

Interest rate = 0.10 No. of members = 500

108 SUPPLEMENT 7 CAPAC I T Y A N D CO N S T R A I N T MA N A G E M E N T

ADDITIONAL HOMEWORK PROBLEMS

S7.36 (a) Proposal A break even in units is:

Fixed cost 50,000 50,000 6,250 units

20 12 8SP VC = = =

−−

Fixed cost 70,000 70,000 7,000 units

20 10 10SP VC = = =

−−

S7.37 (a) Proposal A break even in dollars is:

12

20

Fixed cost 50,000 50,000 $125,000

0.40

11

VC

SP

===

−−

(b) Proposal B break even in dollars is:

$10

20

Fixed cost 70,000 70,000 $140,000

0.50

11

VC

SP

BEP = = = =

−−

S7.38 Set Proposal A = Proposal B; Solve for units

( ) ( )

(20 12) 50,000 (20 10) 70,000

(8) 50,000 (10) 70,000

(8) 20,000 (10)

20,000 10 8

20,000 2

10,000

A A A A B B B B

SP VC X F SP VC X F

XX

XX

XX

XX

X

X

− − = − −

− − = − −

− = −

+=

=−

=

=

S7.39 (a) Proposal A: Profit at 8,500 units

@ 8,500 for Proposal B:

(20 10)8,500 70,000 = 15,000

−−

Proposal A is best.

(b) Proposal B: Profit at 15,000 units

@ 15,000 units for Proposal A:

(20 12)15,000 50,000 = $70,000

@ 15,000 units for Proposal B:

(20 10)15,000 70,000 = $80,000

−−

−−

Proposal B is best.

S7.40 Investment A net income, using Table S7.2, 19,000

PVF9%, 7 – 61,000 = 19,000 4.486 – 61,000 = $24,234

Investment B Net Income

Year

NPV Factor*

NPV

Now

Expense

74,000

1.000

–74,000

1

Revenue

19,000

0.917

+17,423

2

Revenue

20,000

0.842

+16,840

3

Revenue

21,000

0.772

+16,212

4

Revenue

22,000

0.708

+15,576

5

Revenue

21,000

0.650

+13,650

6

Revenue

20,000

0.596

+11,920

7

Revenue

11,000

0.547

+6,017

23,638

* Table S7.1

Therefore, Investment A, with a payoff of $24,234, would be pre-

S7.41 Initial investment = $20,000

Cash Flows

NPV

Cash Flow 1

Cash Flow 2

Cash Flow 3

Year

Factor*

Cash

P

Cash

P

Cash

P

1

0.909

$1,000

$909

$7,000

$6,363

$10,000

$9,090

2

0.826

1,000

826

6,000

4,956

5,000

4,130

3

0.751

3,000

2,253

5,000

3,755

3,000

2,253

4

0.683

15,000

10,245

4,000

2,732

2,000

1,366

5

0.621

3,000

1,863

4,000

2,484

1,000

621

6

0.564

1,000

564

4,000

2,256

1,000

564

7

0.513

—

—

4,000

2,052

1,000

513

8

0.467

1,000

467

2,000

934

—

—

9

0.424

—

—

—

—

1,000

425

$17,127

$25,532

$18,962

*The NPV from Investment 2 is highest, at $5,532 (after the initial investment of $20,000 is subtracted).

102 SUPPLEMENT 7 CAPAC I T Y A N D CO N S T R A I N T MA N A G E M E N T

ACTIVE MODEL S7.2: Break-even Analysis

1. Use the scrollbars to determine what happens to the break-even

point as the fixed costs increase? the variable costs increase? the

selling price increases?

by 10%. In this case, if the variable costs rise by 10%, then the

BEP rises by 15%. If the price per unit increases by 10%, then

would the fixed costs have to decrease? the variable costs? How

much would the selling price have to increase?

Fixed costs, $5,000; variable costs by $1.75 from $2.25

to $.50; the selling price would need to increase by the same

S7.8 Actual (or expected) output = (Effective capacity) (Efficiency)

(Equation (S7.3))

5.5 cars 0.880 = 4.84 cars.

the maximum of 10, 6, and 8.

S7.10 Process time of each machine = 60 min/hr ÷ 4 units/hr

S7.11 Converting each capacity to a process time, Station 1 = 60

min/hr ÷ 20 units/hr = 3 min/unit (for both Machine A and

Machine B); Station 2 = 60 min/hr ÷ 5 units/hr = 12 min/unit; and

Station 3 = 60 min/hr ÷ 12 units/hr = 5 min/unit

S7.14 (a) Workstation C is the bottleneck, at 20 min/unit

(A different Part 1 can be worked on by Workstation A and

Workstation B simultaneously.)

S7.15 (a) Converting each capacity to a process time,

Sawing = Sanding = 60 min/hr ÷ 6 units/hr = 10 min/unit;

Drilling = 60 min/hr ÷ 2.4 units/hr = 25 min/unit; Welding = 60

min/hr ÷ 2 units/hr = 30 min/unit; and each Assembly = 60

140.71) = 140.71

min

S7.16 Break-even:

(8) – 50,000 (10) – 70,000

(8) 20,000 (10)

20,000 10 – 8

10,000

XX

XX

XX

X

=

+=

=

=

==

A

20,000

(a) 1,667 pizzas;

14 – 2

30,000

BEP

S7.20

X = 13,333 pizzas

S7.21 Given:

Price ( ) = $8 unit

Variable cost ( ) = $4 unit

P

V

500 2,000 units

.75 .50

F

BEPxPV

= = =

−−

104 SUPPLEMENT 7 CAPAC I T Y A N D CO N S T R A I N T MA N A G E M E N T

= = = =

−

= = =

=

$0.01

0.05

15,000 15,000

(a) $18,750

1 – 0.2

1 – 1

15,000 15,000

(b) – 0.05 – 0.01 0.04

375,000 copies

V

P

F

BEP

F

BEPxPV

S7.23 Option A: Stay as is

Option B: add new equipment

=

=

==

$

50,000 2.50 $125,000 and

37,500

1–

37,500 $125,000

1.75

1– 2.50

BEP V

P

SUPPLEMENT 7 CA PA C I T Y A N D CO N S T R A I N T MA N A G E M E N T 105

(h) The manual process should be preferred over the mech-

anized process below 75,000 bags. The mechanized

process should be preferred over the manual process

above 75,000 bags.

S7.26 (a) Break-even volume:

Total fixed cost = $1,800 rent, utilities, etc.

106 SUPPLEMENT 7 CAPAC I T Y A N D CO N S T R A I N T MA N A G E M E N T

S7.27 (a) Break-even volume, where total fixed cost = labor

(at $250) + booth rental (at 5 $50) = $500.

Total sales at breakeven

(b) No. of wine servings × 25% of sales

=

at breakeven

986.19 × 0.25

= = 140.9 servings

$1.75

S7.28

Option A: EMV = (90,000 × .5) + (25,000 × .5) = 45,000 + 12,500

= $57,500

Option B: EMV = (80,000 × .4) + (70,000 × .6) = 32,000 + 42,000

= $74,000

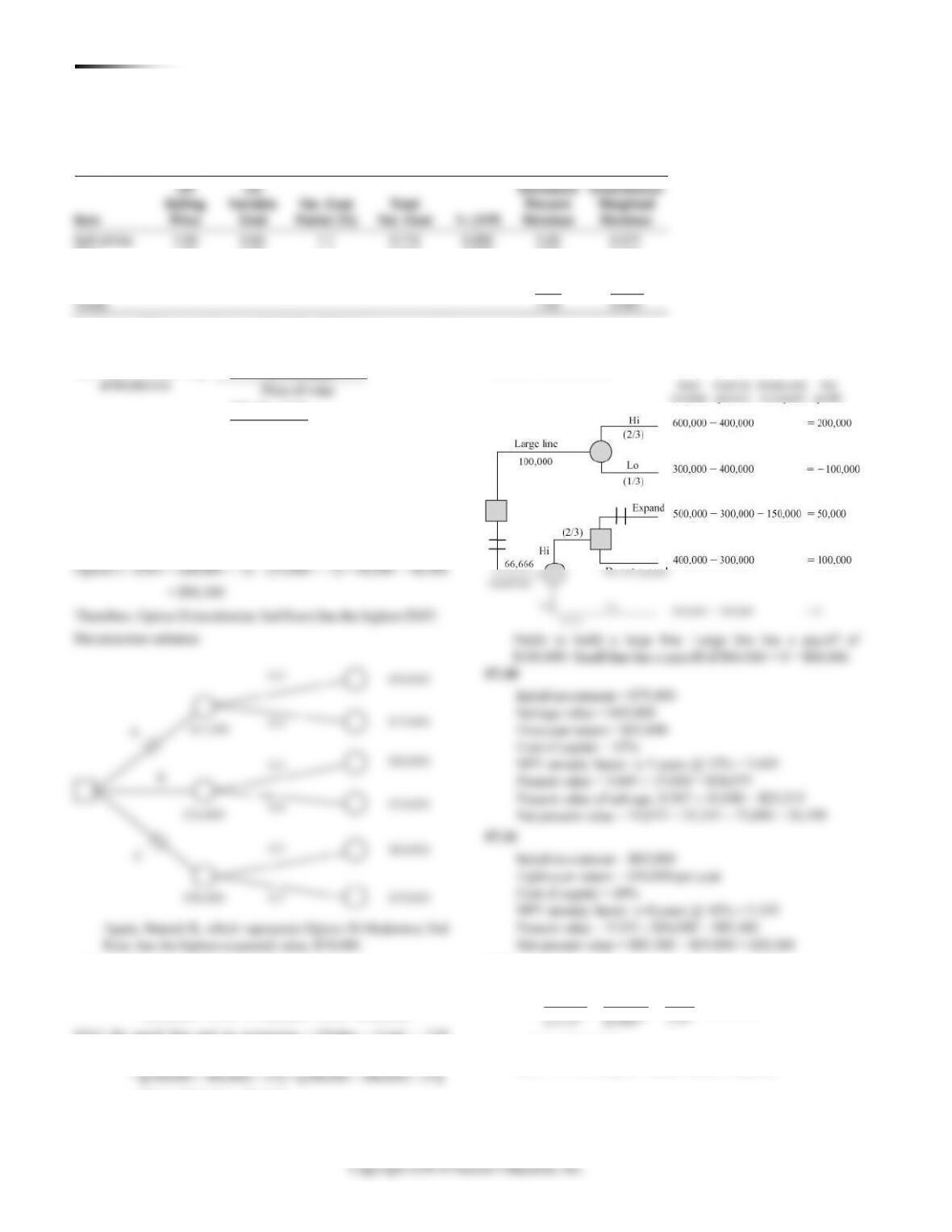

S7.29

EMV for large line = [(Sales – Cost) × 2/3] + [(Sales – Cost) × 1/3]

= (200,000 × 2/3) + (–100,000 × 1/3) = $100,000

EMV for small line and no expansion = [(Sales – Cost) × 1/3]

+ [(Sales – Initial cost) × 2/3]

= [(300,000 – 300,000) × 1/3] + [(400,000 – 300,000) × 2/3]

= $0.0 + $66,666 = $66,666

Therefore, build a large line.

Decision tree solution:

S7.32

15

5600 5600 $1,765.35

3.17

(1 ) (1.08)

N

F

P

i

= = = =

+

or from Table S7.1:

NPV = F PVF8%, 15 = 5600 0.315 = $1,764

Item

(P)

Selling

Price

(V)

Variable

Cost

Var. Cost

Factor (%)

Total

Var. Cost

1– (V/P)

Estimated

Percent

Revenue

Contribution

Weighted

Revenue

Soft drinks

1.00

0.65

1.1

0.715

0.285

0.25

0.071

Wine

1.75

0.95

1.1

1.045

0.403

0.25

0.101

Coffee

1.00

0.30

1.1

0.330

0.670

0.30

0.201

Candy

1.00

0.30

1.1

0.330

0.670

0.20

0.134

Totals

1.00

0.507

Breakeven = TFC/wt contribution = 500/0.507 = $986.19

S7.33

Expense

Machine A

Machine B

Original cost

10,000

20,000

Labor per year

2,000

4,000

Maintenance per year

4,000

1,000

Salvage value

2,000

7,000

Year

Machine A

NPV Factor*

NPV

Now

Expense

10,000

1.000

–10,000

1

Expense

6,000

0.893

–5,358

2

Expense

6,000

0.797

–4,782

3

Expense

6,000

0.712

–4,272

–24,412

3

Salvage revenue

2,000

0.712

+1,424

–22,988

* NPV factor from Table S7.1.

(a) NPV of the three small ovens = –$8,511; NPV of the

two large ovens = –$5,855. Therefore, you should rec-

ommend that the firm purchase the two large ovens.

(b) The basic assumptions made with regard to the ovens

are:

◼ The ovens are of equal quality.

◼ The ovens are of equivalent production capacity.

(c) The basic assumptions made with regard to methodol-

ogy are:

◼ Future interest rates are known.

◼ Payments are made at the end of each time period.

S7.35 (a) Remember that Year 0 has no discounting.

Initial cost = $1,000,000 Yearly maintenance = $75,000

Salvage cost = $50,000 Yearly dues = $300,000

Interest rate = 0.10 No. of members = 500

108 SUPPLEMENT 7 CAPAC I T Y A N D CO N S T R A I N T MA N A G E M E N T

ADDITIONAL HOMEWORK PROBLEMS

S7.36 (a) Proposal A break even in units is:

Fixed cost 50,000 50,000 6,250 units

20 12 8SP VC = = =

−−

Fixed cost 70,000 70,000 7,000 units

20 10 10SP VC = = =

−−

S7.37 (a) Proposal A break even in dollars is:

12

20

Fixed cost 50,000 50,000 $125,000

0.40

11

VC

SP

===

−−

(b) Proposal B break even in dollars is:

$10

20

Fixed cost 70,000 70,000 $140,000

0.50

11

VC

SP

BEP = = = =

−−

S7.38 Set Proposal A = Proposal B; Solve for units

( ) ( )

(20 12) 50,000 (20 10) 70,000

(8) 50,000 (10) 70,000

(8) 20,000 (10)

20,000 10 8

20,000 2

10,000

A A A A B B B B

SP VC X F SP VC X F

XX

XX

XX

XX

X

X

− − = − −

− − = − −

− = −

+=

=−

=

=

S7.39 (a) Proposal A: Profit at 8,500 units

@ 8,500 for Proposal B:

(20 10)8,500 70,000 = 15,000

−−

Proposal A is best.

(b) Proposal B: Profit at 15,000 units

@ 15,000 units for Proposal A:

(20 12)15,000 50,000 = $70,000

@ 15,000 units for Proposal B:

(20 10)15,000 70,000 = $80,000

−−

−−

Proposal B is best.

S7.40 Investment A net income, using Table S7.2, 19,000

PVF9%, 7 – 61,000 = 19,000 4.486 – 61,000 = $24,234

Investment B Net Income

Year

NPV Factor*

NPV

Now

Expense

74,000

1.000

–74,000

1

Revenue

19,000

0.917

+17,423

2

Revenue

20,000

0.842

+16,840

3

Revenue

21,000

0.772

+16,212

4

Revenue

22,000

0.708

+15,576

5

Revenue

21,000

0.650

+13,650

6

Revenue

20,000

0.596

+11,920

7

Revenue

11,000

0.547

+6,017

23,638

* Table S7.1

Therefore, Investment A, with a payoff of $24,234, would be pre-

S7.41 Initial investment = $20,000

Cash Flows

NPV

Cash Flow 1

Cash Flow 2

Cash Flow 3

Year

Factor*

Cash

P

Cash

P

Cash

P

1

0.909

$1,000

$909

$7,000

$6,363

$10,000

$9,090

2

0.826

1,000

826

6,000

4,956

5,000

4,130

3

0.751

3,000

2,253

5,000

3,755

3,000

2,253

4

0.683

15,000

10,245

4,000

2,732

2,000

1,366

5

0.621

3,000

1,863

4,000

2,484

1,000

621

6

0.564

1,000

564

4,000

2,256

1,000

564

7

0.513

—

—

4,000

2,052

1,000

513

8

0.467

1,000

467

2,000

934

—

—

9

0.424

—

—

—

—

1,000

425

$17,127

$25,532

$18,962

*The NPV from Investment 2 is highest, at $5,532 (after the initial investment of $20,000 is subtracted).